The head of the New Zealand Police Financial Intelligence Unit (FIU) is calling on businesses whose activity is overseen by anti-money laundering laws to play a more proactive role in trying to stop nefarious activity.

In the FIU's latest Suspicious Activity Report, Detective Inspector Christiaan Barnard who heads up the FIU, is calling for a change in mindset from so-called reporting entities, who are businesses supervised under the Anti-Money Laundering and Countering Financing of Terrorism (AML/CFT) Act. Barnard says NZ faces a huge organised crime problem with our money laundering risk being assessed at more than $1.35 billion annually.

"The criminal abuse of our financial system is not something we are going to arrest or restrain our way out of. Prevention is central to the success of the AML/CFT Act and this is where the reporting entities play a crucial role," says Barnard.

"There needs to be a mindset shift within reporting entities, where a risk-based approach is coupled with a response that has community outcomes as the central focus. When we consider the risk reporting entities identify through SAR [suspicious activity report] reporting, where the threshold is ‘reasonable grounds to suspect,’ reporting entities are exposed to customers who they believe are likely to be engaging in some type of criminal activity. Currently there is a belief that SAR submission is done in order for law enforcement to intervene. However, there is only a finite amount of investigative resource available so, generally speaking, reporting entities need to change their mindsets from being detectors to being disruptors, preventers, and deterrents."

"If you believe that it is likely that your customer is engaging in some type of criminal activity, then I would encourage you to be more proactive in refusing to conduct transactions and moving to de-risk. We want to push criminals to the margins and into the hands of those non-compliant operators where we can more effectively deploy our law enforcement resource. This is not without its risks of unintended consequences. To improve reporting entities’ ability to detect bad actors there needs to be more education, more guidance, information sharing enabled through good laws, and improved analysis to inform tactical and operational risks," Barnard adds.

He goes on to say that while the FIU and the three AML/CFT Act supervisors - the Reserve Bank, Financial Markets Authority and Department of Internal Affairs - carry significant responsibility, reporting entities also need to ensure they're being proactive in their understanding of risk and the various techniques used to launder money or finance terrorism. This, Barnard says, is so they can recognise potential criminal activity, and on top of reporting it, proactively address it themselves.

The FIU collects, analyses and disseminates financial information received under the AML/CFT Act on behalf of the Commissioner of Police. Amongst the information the FIU receives from reporting entities are SARs detailing the specific circumstances and reason for suspicion. SARs may or may not involve financial transactions and includes a synopsis of why the activity is considered suspicious.

Like this investigative piece? Support our journalists. Find out how.

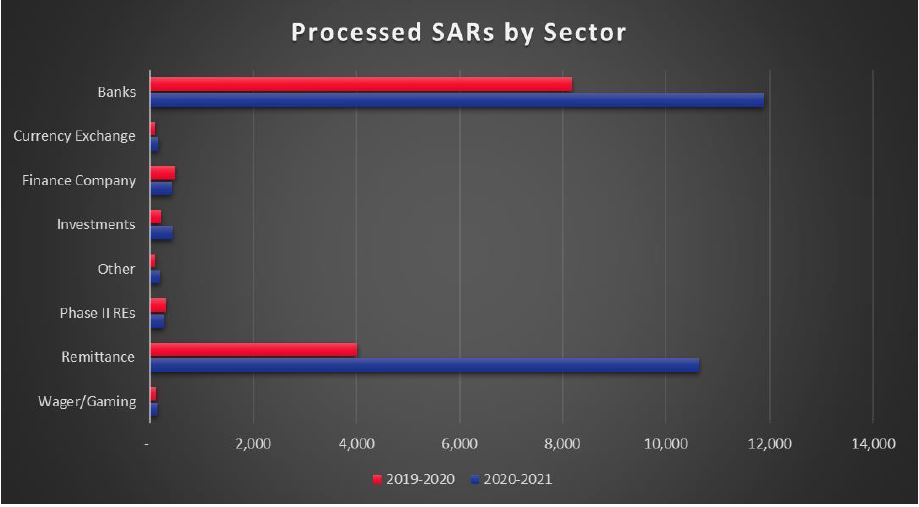

Over the 2020-2021 year, SARs increased significantly year-on-year, with an 80% increase in transaction-based reports and 35% increase in activity-based reports.

"Most categories of reporting entities increased their reporting – from an 18% increase in the wager and gaming sector to an 165% increase in the remittance sector. However, reporting by Phase II [real estate agents, lawyers and accountants] and finance companies decreased by 10% and 13% respectively. Transaction volumes within SARs and prescribed transaction reports (PTRs) increased significantly – over 100%," the FIU says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

4 Comments

Imagine the car dealers refusing to sell Mercedes, BMWs, Range Rovers etc in order to avoid taking dirty money. Hah!

Best place to park money is buying property despite scrutiny.

Dont push your job onto businesses, just because you cant do it yourself. That is just going to increase the costs for every user.

The problem then becomes unworkable regulations, and the poor businesses get saddled with the blame if something does slip through. So just slows everything down.

What a joke when the government is the least fiscally responsible organisation. There is not limit to their waste and incompetence.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.