Top 10 at 10: Goldman's 'financial meth lab'; 'Unsustainable Chinese growth'; Dilbert

17th Jul 09, 10:29am

by

Here's my Top 10 links from around the Internet at 10 am. I welcome your additions in the comments below and please send any suggestions for Monday's Top 10 at 10 to bernard.hickey@interest.co.nz A quick reminder to gloaters that my humble pie party is this afternoon at the Gables pub in Herne Bay in Auckland at 5pm. This is to 'celebrate' me halving my forecast for house price falls. Also, I am not an overpaid speed bump.

1. America's Federal Deposit Insurance Corp (FDIC) and the Federal Reserve are looking at bringing in some sort of tax to reduce the size and risk-taking of 'too big to fail' banks, Bloomberg reports after an interview with FDIC boss Sheila Bair. HT Felix Salmon

1. America's Federal Deposit Insurance Corp (FDIC) and the Federal Reserve are looking at bringing in some sort of tax to reduce the size and risk-taking of 'too big to fail' banks, Bloomberg reports after an interview with FDIC boss Sheila Bair. HT Felix Salmon

The FDIC will propose slapping fees on the biggest bank holding companies to the extent that they carry on activities, such as proprietary trading, outside of traditional lending. The idea goes beyond the Obama administration's regulation-overhaul plan, which would have the Fed adjust capital and liquidity standards for the biggest firms, without any pre-set fees. "What we have suggested is financial disincentives for size and complexity," Bair said in a July 9 interview. Fed Chairman Ben S. Bernanke told lawmakers last month that restricting size is a "legitimate" option.Should New Zealand have a special tax for our big four banks, which are equally too big to fail? Or maybe they should just pay up the NZ$2.4 billion in back taxes they owe? 2. Now the serious players are laying into Goldman "Vampire Squid" Sachs. Here's former Democrat Labour Secretary and Clinton right hand man Robert Reich.

Goldman's resurgence should send shivers down the backs of every hardworking American who has lost a large chunk of retirement savings in this economic debacle, as well as the millions who have lost their jobs. Why? Because Goldman's high-risk business model hasn't changed one bit from what it was before the implosion of Wall Street. Goldman is still wagering its capital and fueling giant bets with lots of borrowed money. While its rivals have pared back risks, Goldman has increased them. And its renewed success at this old game will only encourage other big banks to go back into it.

3. Structured Finance expert Janet Tavakoli says on CNN that that Wall St, including Goldman Sachs, owes the American public and should pay up.

3. Structured Finance expert Janet Tavakoli says on CNN that that Wall St, including Goldman Sachs, owes the American public and should pay up.

Goldman can now compete with the largest U.S. banks and borrow money at interest rates pushed as close to zero as possible by the Fed. Goldman gets a further benefit: favorable accounting rule changes. In addition, Goldman issued $30 billion of debt with a valuable government guarantee that remains outstanding. Meanwhile, the American public faces a rising unemployment rate, falling housing prices, rising unemployment, higher local taxes and a dismal economic outlook. Interested men with reputations and fortunes at stake rode roughshod over public interest. The American public is owed part of the profits Goldman was able to make because of the largesse of our Congress. Wall Street's "financial meth labs," including Goldman's, massively pumped out bad bonds and credit derivatives that have melted down savings accounts, pension funds, the municipal bond market and the American economy. Risky assets, leverage and fraud led to acute distress in the global financial markets. The biggest crime on the American economy may go unpunished with no consequences to the perpetrators. The biggest crime was not predatory lending, but predatory securitizations, packages of loans that did not deserve the ratings or prices at the time they were sold. They ballooned what should have been a relatively small problem into a global crisis. Wall Street owes the American public for its key role in bringing the global economy -- and in particular, the U.S. economy -- to its knees. Goldman is not alone in owing the American public. It is not the worst of all of the Wall Street firms. But among all of Wall Street's offenders, it is the most well-connected, and Goldman was the firm that cleaned up the most as the result of government bailouts.4. The government has done a deal with Australia to allow New Zealanders to bring their Australian pension savings home with them. Great. I have a little pot I'd like to get my hands on too. Here's the full Bill English release. 5. The Wall Street Journal wonders here whether China's 7.9% growth is sustainable, given it was based on Chinese government spending and rampant new lending.

"Now that government efforts to boost growth have started to work, we are likely to see increased uncertainty and disagreement in official circles about when is the appropriate time to reverse course and withdraw policy stimulus," said RBC Capital Markets in a note. Also Thursday, the finance and economic committee of the National People's Congress, China's legislature, warned that the government must prevent the "extraordinary growth" of credit that could lead to inflation risks and problems for the financial system. It said China should strengthen credit checks and prevent a rebound in bad loans.6. This is a cracking analysis of America's debt problem by Karl Denninger. A must read I reckon. Is our debt problem much better? Fitch thinks not.

There is only one way to re-base the economy and get it to grow on a sustainable basis: Consumption must be paid for by current income and some fraction of current income must in addition be put into capital formation. There are only two ways to get there:Those are the only two choices folks. The math is never wrong and it is crystal clear. That every politician and media channel is not spending every spare minute talking about this is criminal malfeasance and a massive fraud being perpetuated upon the public. The Fed's and The Administration's (both past and current) programs have not and will not work because the underlying cause isn't that consumers aren't "stimulated" enough or that "money (credit) is too tight." The underlying cause of our economic malaise is that we have cheated on a math test for more than 20 years and the teacher - the cold, hard facts of mathematical law, has caught up with us. No amount of fancy arm-waving or "financial engineering" changes any of the above - it can't. The fact of the matter is that your real standard of living, as defined by per-capita income compared to your expenditures, has decreased quite materially over the last 20 years. We have made up the difference with debt, not by increasing output. This is why we now have virtually every family "needing" to have two people working, it is why we continue to play the "credit roulette" game, and it is why we are teetering on the edge of the economic abyss, irrespective of the so-called "green shoot" crowd.

- We can withdraw all of the political support for the lying that has allowed this debt to accumulate in the first place, calling it what it is: accounting fraud. This will in turn force massive bankruptcies to take place among both individuals and financial firms. Once that process is complete we will have cleared the excessive debt from the system and the economy can then grow organically as a consequence of productivity gains and production, with those who were imprudent appropriately punished by the free market, and those who were prudent rewarded by it.

- We can continue to allow those who made imprudent loans to lie about the value of these "assets". There will be no sustainable economic growth so long as the excess debt load remains. There is a high probability that at some point we will enter a "death-spiral" where interest expense exceeds excess income at which point we will literally suffer an economic collapse, and there is absolutely no way to determine exactly where the "tipping point" is. A foreign creditor could trigger such a collapse at any time were they to withdraw their support of Treasuries, for example, either as a consequence of a choice or an economic crisis at home that forces them to stop buying.

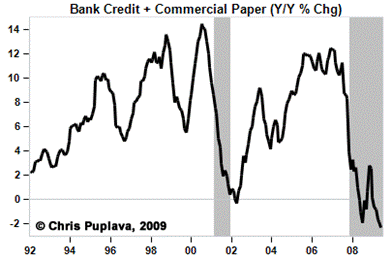

7. Mish at Global Economic Analysis talks about the collapse of the Commercial Paper market for non-government guaranteed corporates in America. Not too many green shoots there.

7. Mish at Global Economic Analysis talks about the collapse of the Commercial Paper market for non-government guaranteed corporates in America. Not too many green shoots there.

The commercial paper market is vanishing and it will not come back. Indeed, it's the end of the free lunch for corporations to be able to perpetually roll over short-term debt effectively achieving long term financing at short-term rates. This decline in commercial paper is indicative of the fundamental shift in the risk appetite of banks, investors, and consumers alike. This secular shift in willingness to take on risk also applies to credit cards, home equity lines of credit, mortgages, lending in general and of course consumer spending in general. These attitudes shifts are a huge part of the deflationary environment we are in.

8. And I thought my credit card bills were bad. This story from New Hampshire is a chuckler.

8. And I thought my credit card bills were bad. This story from New Hampshire is a chuckler.

When Josh Muszynski checked his bank account online, he didn't expect to find a $23 quadrillion debit. "If it were to be true that someone actually compromised that money and got that money, they could do some severe damage with that amount of money," he said.9. This is great from the WSJ on the new stars of the blogosphere.

Americans trying to understand the nail-biting financial trauma of the past several months are flocking by the millions to a surprisingly lively source of enlightenment: blogs written by economists. Such blogs are thriving in this recession, driven by intense interest from policymakers, investors, academics and people like Zina Poletz, a Minneapolis public-relations executive who says she had little interest in economics before the financial crisis intensified last fall. "I never thought I'd be sitting up late at night reading what [Federal Reserve chairman] Ben Bernanke thinks, but now I do," she says.10. Steve Keen's Debtwatch has another missive on which economists called it right.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.