Here's my Top 10 links from around the Internet at 10 am. I welcome your additions and comments below. If you have any links you think are must reads for tomorrow's Top 10 at 10 please email them to me at bernard.hickey@interest.co.nz I don't think I'll ever have to resort to cannibalism.  1. Brian Gaynor at NZHerald.co.nz has out some interesting details about New Zealand's foreign exchange market and argues that someone has to do something about making it less volatile to protect small exporters. He points out that more New Zealand dollars trade every day than Russian roubles, Chinese Yuan and Indian Rupee. Our daily turnover to GDP ratio is 43%. Astonishing. Gaynor says its a problem that needs discussion but doesn't have an immediate solution.

1. Brian Gaynor at NZHerald.co.nz has out some interesting details about New Zealand's foreign exchange market and argues that someone has to do something about making it less volatile to protect small exporters. He points out that more New Zealand dollars trade every day than Russian roubles, Chinese Yuan and Indian Rupee. Our daily turnover to GDP ratio is 43%. Astonishing. Gaynor says its a problem that needs discussion but doesn't have an immediate solution.

Currency controls are not an option for New Zealand because it would be impossible for our Government to set the right exchange rate level and then support this against potential attack from US and European hedge funds. However, the collapse of Line 7, and the difficulties faced by the dairy sector, shows that the NZ dollar market offers great potential for international speculators while hindering the country's exporters. Clearly, there should be far more high level discussion on the state of the NZ dollar market and any measures we can introduce to reduce its volatile and speculative characteristics while assisting our export sector.

2. Brent Sheather, a stock broker and financial adviser, talks in NZHerald.co.nz about the new rules coming in for financial advisers and suggests the only real solution to the problem of advisers recommending bad investments is to get rid of commissions and just pay fees for advice.

Financial advisers can either be paid by way of commission from the product provider or by way of a fee directly from the client. Bond-based products typically pay lower rates of commission than equity-based products and the safest investments, like government bonds, pay no commission whatsoever. Similarly, exchange-traded index funds which have the lowest management fees in the industry don't pay any commission or trailing fee. No surprises, then, that commission-based advisers don't generally recommend government bonds or ETFs. In contrast, the fee-based model, in which an adviser charges the client a set percentage of the funds to be invested, is potentially more attractive to investors, providing the percentage charged is the same for all products sold. Under the fee-based model a financial planner will be disinterested as to whether he or she sells bonds, property or shares and is thus able to focus on what is good for the client, rather than what maximises income. The removal of commission and trailing fee payments by product providers would change the investment advisory landscape in an instant and do more "to promote the sound and efficient delivery of financial advice and to encourage public confidence in the professionalism and integrity of financial advisers" than any legislation ever could.

3. Here's a sign of the times. China has joined a growing movement of countries protesting over a clause in the recent American cap and trade carbon legislation which imposes a tax on imports from nations without carbon emissions caps, FT.com reported. This little bombshell in the legislation is threatening to spark a global trade war. Trust American politicians to find a way to restrict trade. To be fair the bill still has to pass the senate and Obama is not keen, but his protestations don't sound that strong.

After the passage of the House bill by a narrow vote last week, President Barack Obama warned imposing carbon border taxes might send a protectionist signal. "I think there may be other ways of doing it than with a tariff approach," he said. The bill now moves to the Senate, where it is likely to receive an even rougher ride from moderate Democrats concerned about imposing more costs on US businesses.

4. This could only happen in America. Bernie Madoff has hired a 'prison consultant' to help him avoid being incarcerated in the nastiest prison, TimesOnline reported. It seems there is an industry of these consultants.

A sentence above 30 years usually places an inmate in a high-security category, meaning that Madoff would be assigned to a prison housing violent offenders including murderers and rapists. Ed Bales, of Federal Prison Consultants, which is not involved in the case, said that Madoff was likely to be held in isolation, known as "the hole", at least at first. "He could cause a lot of problems because it's a very high-profile case. People may react very badly to him," Mr Bales said. "He is going to have white supremacists who do not like the Jewish population. He has got some enemies he is going to have to face." It is even possible that Madoff could be upgraded for his own safety to the only Supermax facility, where inmates are locked up for 23 hours a day and never get to mix with the general prison population. John Webster, of National Prison and Sentencing Consultants, said: "Next to being a sex offender, people who are perceived as stealing from the elderly are not perceived as very popular folk in prison. Everyone has a mother. I think there is going to be some form of retaliation."

5. Ambrose Evans Pritchard at The Telegraph reckons civil unrest can't be ruled out as unemployment jumps sharply in developed economies and wage deflation sets in.

The Centre for Labour Market Studies (CLMS) in Boston says US unemployment is now 18.2pc, counting the old-fashioned way. The reason why this does not "feel" like the 1930s is that we tend to compress the chronology of the Depression. It takes time for people to deplete their savings and sink into destitution. Perhaps our greater cushion of wealth today will prevent anotherGrapes of Wrath, but 20m US homeowners are already in negative equity (zillow.com data). Evictions are running at a terrifying pace. Some 342,000 homes were foreclosed in April, pushing a small army of children into a network of charity shelters. This compares to 273,000 homes lost in the entire year of 1932. Sheriffs in Michigan and Illinois are quietly refusing to toss families on to the streets, like the non-compliance of Catholic police in the Slump. We are moving into Phase II of the Great Unwinding. It may be time to put away our texts of Keynes, Friedman, and Fisher, so useful for Phase 1, and start studying what happened to society when global unemployment went haywire in 1932.

6. This is an exceptionally cool way to chart bank assets, market capitalisations and capital over time. HT Felix Salmon. This a must click to the Council of Foreign Relations. Fantastic charts. Felix points out the European banks are particularly worrisome.

Check out where that financial-failures chart ends: with five European banks all having assets of more than $2.5 trillion, and none of them looking particularly well capitalized. No US bank is that dangerous, partly because no US bank is that big "” and US banks are dangerous enough. All five of those European banks are too big to rescue, and none of them is particularly well regulated. How do we fix this problem? I have no idea. But I do know that it's a huge problem, and that no one is even beginning to address it.

7. William Buiter explains in this video at The Telegraph why the banks will need more cash. 8. Australian economist Steve Keen, who is famous for arguing Australian house prices will collapse, has a monster post over at DebtDeflation with a bunch of cracker charts, including the one below showing the link between debt deleveraging and unemployment. It's long but well worth a read.

The reason that most economists continue to underestimate this downturn is because (a) the downturn is being driven by deleveraging from literally unprecedented levels of private debt, and (b) the neoclassical theory of economics, which dominates academic and market economics alike, ignores the role of private debt in the economy. The reason that I anticipated this crisis four years ago is that I reject the mainstream "neoclassical" approach to economics, and instead analyse the economy from the perspective of Hyman Minsky's "Financial Instability Hypothesis", in which private debt plays a crucial role. In our credit-driven economy, demand is the sum of GDP plus the change in debt. If debt is low relative to GDP, then its contribution to demand is relatively unimportant; but if debt becomes large relative to demand, then changes in debt can become THE determinant of aggregate demand, and hence of unemployment. That is manifestly the case in America today. Under the stewardship of neoclassical economics in the personas of Alan Greenspan and Ben Bernanke, the growth in private debt has not merely been ignored but has actively been encouraged, in the dangerously naive belief that the private sector is being "rational" when it borrows.

9. Michael Pettis is a professor at Peking University's Guanghua School of Management and is one of the few English-writing economists on the ground in China who knows whats really going down behind The Great Firewall. Here he writes that "China's Loan growth isn't boosting my confidence in China's Green Shoots"

9. Michael Pettis is a professor at Peking University's Guanghua School of Management and is one of the few English-writing economists on the ground in China who knows whats really going down behind The Great Firewall. Here he writes that "China's Loan growth isn't boosting my confidence in China's Green Shoots"

Credible rumors suggest that new loans in June will hit RMB 1.2 trillion or more, as banks rush to inflate their quarterly loan numbers, just as they did in March, on the assumption that any cap in quarterly loan growth will be based on the previous quarter's numbers. I would argue that new lending in 2009, running at 2 to 3 times the new lending over the same period in 2008, is not at all normal and is very unlikely to be healthy.These are amazing numbers. The People's Daily article indicates, I think, the schizophrenic attitudes prevalent in China today, with growing nervousness in some circles about the consequences of this explosion in lending riding side by side with a determination to keep it up.

We are going to get 8% growth this year come what may. Since late last year I have been writing about how this everything-but-the-kitchen-sink strategy of throwing everything possible into countering the effect of the global contraction on the Chinese economy might result in higher growth this year and next but will make China's necessary transition even more difficult and will almost certainly result in much slower growth over the longer term.

I am more certain than ever that this is the correct analysis. The biggest damage is likely to be in the banking sector, which will then create problems in the fiscal accounts.

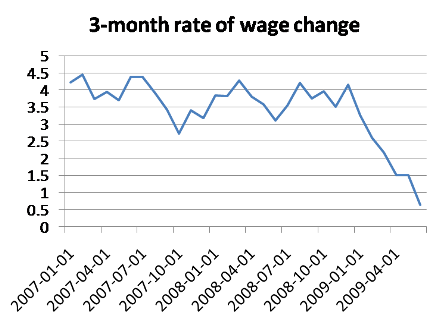

Wages in America are falling, Paul Krugman points out with this chart below. Maybe a debt deflation spiral will be the problem, rather than an inflation explosion.  10. Ever thought your bank has you by the short and curlies? Or maybe they even have your soul? Reuters reports a Latvian banker is now asking borrowers to pledge their soul as collateral.

10. Ever thought your bank has you by the short and curlies? Or maybe they even have your soul? Reuters reports a Latvian banker is now asking borrowers to pledge their soul as collateral.

Such a deal is being offered by the Kontora loan company, whose public face is Viktor Mirosiichenko, 34. Clients have to sign a contract, with the words "Agreement" in bold letters at the top. The client agrees to the collateral, "that is, my immortal soul." Mirosiichenko said his company would not employ debt collectors to get its money back if people refused to repay, and promised no physical violence. Signatories only have to give their first name and do not show any documents. "If they don't give it back, what can you do? They won't have a soul, that's all," he told Reuters in a basement office, with one desk, a computer and three chairs.

10. (bonus!) Here's how the other people live. Hedge fund managers' wives are struggling in New York, Tatiana Boncompagni at TimesOnline reports from personal experience. There's not a lot of sympathy in evidence.

Here in New York there is a quiet revolution taking place. The once-almighty hedge funders are finally getting their comeuppance and almost everyone is happy to have a bird's-eye view of their long (and, thus, quite entertaining) fall from grace. From my perch, it is easy to understand why. While I associate with the super-rich, their wealth is on another plane. They have retinues of staff. I am privileged compared with most but I pick up Cheerios from my own floor, make the beds and cook all the meals. How many of us non-hedgie types have not felt a pang of jealousy on hearing about a friend's posh holiday or new penthouse apartment, or the renovation of their multimillion-dollar home? And, try as we might, it's hard to feel sorry for the women who have to make do with one of Jimmy Choo's faux-skin handbags because they can no longer afford the real thing. Much as I hate to generalise, I'd still venture to say that if hedgie wives had been more discreet, had chosen not to flaunt their wealth through obscenely lavish birthday parties for their kids and spouses, and hadn't gone on about their latest handbag, we might feel a bit differently now. But, alas, there is no return policy for a decade of conspicuous consumption.

10 (Another bonus!) The good economist folks over at VoxEu look at the 30% fall in global trade in the first quarter of 2009. The chart referred to below is a tad worrying.

"...trade has fallen fast and furiously since the onset of the financial crisis in the fall. Figure 2 compares trade growth (month over same month the previous year) in this crisis and in the previous downturns, using monthly data in constant US dollars for a balanced sample of 31 countries that report data from 1960 through March 2009. While growth leading up to the crisis was a bit higher in this episode, it still looked quite similar to the previous downturns. What is most evident from the picture is that the trade drop over the last few months has been much steeper and more severe than other recent episodes. This likely reflects the magnitude of this downturn and the increased responsiveness of trade to income in recent years."

.jpg)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.