Top 10 at 10: Gareth Morgan wants tougher RBNZ rules for housing lending; Euro doubts abound; Corn syrup's ugliness; Dilbert

4th May 10, 5:56pm

by

Here are my Top 10 links from around the Internet at 10 to 6 pm (!) My apols. It's been a disconnected day in Wellington for me. I welcome your additions and comments below or please send suggestion for Wednesday’s Top 10 at 10 to bernard.hickey@interest.co.nz

1. 'Put down your bible Alan' - Gareth Morgan has used a column in the NZHerald to call on the Reserve Bank to use tougher capital adequacy rules for bank lending to housing than are currently set under international rules. I'm sympathetic, but I suspect the Reserve Bank wants to be a bit careful before torpedoing the banks and the property market. I can understand Gareth's drive for something -- anything -- to tilt the economy back on track to productive investment.

1. 'Put down your bible Alan' - Gareth Morgan has used a column in the NZHerald to call on the Reserve Bank to use tougher capital adequacy rules for bank lending to housing than are currently set under international rules. I'm sympathetic, but I suspect the Reserve Bank wants to be a bit careful before torpedoing the banks and the property market. I can understand Gareth's drive for something -- anything -- to tilt the economy back on track to productive investment.

Which is to blame, tax or the Reserve Bank? Who cares - surely policy advisers can see that it's the combination that matters. You could align our tax regime with international norms, or you could use a hammer to crack a nut - and develop a unique tax system just for property running into all the boundary definition problems of what is and what isn't property (just as the Tax Working Group suggested). Or the Reserve Bank could just stop being such a blind adherent to the Old Testament, and acknowledge that because of the absence of taxing capital gains in New Zealand, it is not appropriate to follow blindly the international bible of bank prudential guidelines - those that instruct banks to favour lending on mortgage to lending on any other activity. If the capital gains aren't taxed, we can't afford to slavishly follow the international template. We'd all breathe a sigh of relief, if the Reserve Bank could be so insightful. It would help issues like mis-allocation of capital and low productivity growth, reducing the bias toward household spending running faster than taxable income, and reducing imbalances such as inflation and an entrenched and large current account deficit. This, instead of its drone-like adherence to central bank credos from the large Western economies that have totally different conditions to us, would give Prime Minister John Key at least a chance at scoring his "step change" in economic performance. All in all there are no downsides. Well, perhaps some for (Property Investors Federation President Andrew) King's constituency, but I'm sure the national interest would weigh more favourably. All we need is for the ostriches to pull their heads up and Alan Bollard to put his bible down.2. 'We don't buy it' - Investors in European government debt are not convinced that the giant bailout package for Greece will save the euro, Bloomberg reports.

“The euro is just patently overvalued,” said Richard Franulovich, a senior currency strategist at Westpac Banking Corp. in New York, who predicts a decline to $1.30 this month. “My complaint is that the package requires some extremely harsh austerity measures that simply won’t be put into place.” Greece’s three-year financial lifeline requires the nation to cut its budget deficit below the EU limit of 3 percent of gross domestic product by the end of 2014, a year later than originally planned. The deficit was 13.6 percent last year, the region’s second-largest after Ireland. The austerity measures include a second set of wage cuts for public workers and a three-year freeze on pensions. “There’s never been a country that’s undertaken to save so much and there’s never been a country that’s succeeded in saving so much,” said Lutz Karpowitz, a currency strategist at Commerzbank AG in Frankfurt. “It’s very, very negative.” Unions in Greece representing more than 500,000 civil servants called a 48-hour strike starting May 4 to protest what they have called “savage” budget cuts. Local government workers called a strike for today. Teachers are also on strike from tomorrow and a general strike, the third this year, is planned for May 5.3. China's sky will fall - Marc Faber, the author of the 'Gloom, Doom and Boom' report, reckons China will crash within a year, Bloomberg reports.

Investor Marc Faber said China’s economy will slow and possibly “crash” within a year as declines in stock and commodity prices signal the nation’s property bubble is set to burst. “The market is telling you that something is not quite right,” Faber, the publisher of the Gloom, Boom & Doom report, said in a Bloomberg Television interview in Hong Kong today. “The Chinese economy is going to slow down regardless. It is more likely that we will even have a crash sometime in the next nine to 12 months.” China is “on a treadmill to hell” because it’s hooked on property development for driving growth, Chanos said in an interview last month. As much as 60 percent of the country’s gross domestic product relies on construction, he said. Rogoff said in February a debt-fueled bubble in China may trigger a regional recession within a decade. The government has banned loans for third homes and raised mortgage rates and down-payment requirements for second-home purchases.4. Better than nothing - US banks didn't tighten credit further in the March quarter, which US economists are leaping on as a sign of progress, Bloomberg reported. This is the problem at the core of the developed world. Banks are not growing lending, despite having ample cash on deposit with central banks. They are doing their best to rebuild their capital and equity by restricting lending growth and saving profits generated by borrowing cheaply for short terms and lending at higher rates at longer terms. At some stage the worm will turn, but it will be slow.

The smallest proportion of banks in two years restricted standards on business lending, the Fed’s survey of senior loan officers released today showed. Also, more banks than in the previous survey expressed a greater willingness to make installment loans to consumers, the central bank said in Washington. “This is just one more feather in the cap of the recovery in the financial markets,” said Michael Darda, chief economist at MKM Partners LLC in Greenwich, Connecticut. “We’re going in the right direction. The report is on an improving track which is consistent with improving spreads in the credit markets.” The shortage of credit, as banks tightened loan standards and many consumers and businesses paid off debt, has impeded the recovery. The central bank cited “tight credit” among the reasons for its April 28 decision to keep interest rates at zero to 0.25 percent for an “extended period.”5. Maggie Redux - Niall Ferguson, the author of the Ascent of Money, has some frightening views on what faces the leaders in Britain after the election result is clear later this week. He thinks the IMF will have to be called in and Britain needs Maggie now more than ever. HT Robert Weincove via email. The Vancouver Sun has the report.

The situation of the United Kingdom in fiscal terms is in fact worse than the situation of Greece. That may come as a surprise to you, but if you look at the most recent paper on the subject published by the Bank for International Settlements, it is very clear. The trajectory of U.K. public debt over the next 30 years, absent a major change of policy, will take it to a mind-blowing 500% of GDP, which is about 100 percentage points worse than Greece. If Britain had done what many right-thinking people thought it should do and joined the euro, the situation of Britain would be worse than that of Greece today. The only reason that Britain isn’t an honourary member of the PIIGS club, along with Portugal, Ireland, Italy and Spain, is that it stayed outside the eurozone and therefore reserves the right to debase the currency as an exit strategy. I don’t know about you, but I don’t find that very cheery as a prospect So, Britain has a massive fiscal crisis that is just about to break. Whoever wins this election … they are going to have a ghastly task on their hands to try to reform a system of entitlements and welfare and state subsidy that has hugely expanded under Gordon Brown since 1997. I think Britain was more ready for Thatcherism in 1979 than it is today, and yet it needs it more today than it did then.6. Pedalling hard - Goldman Sachs has employed all manner of PR flacks now to rebuild its public reputation. CEO Lloyd Blankfein is even out doing the political talk shows in the United States. He is back-pedalling furiously. This is almost a year after the publication of Matt Taibbi's seminal 'Vampire Squid' article in Rolling Stone. A bit late now Lloyd, as Felix Salmon at Reuters points out.

The fact is that arrogance and secrecy are in Goldman’s institutional bloodstream, and that this particular crisis can’t easily be managed away. Blankfein’s going to have to get used to bad press — and to that bad press applying serious downward pressure to his share price. It will be years, if ever, before Goldman is rehabilitated.

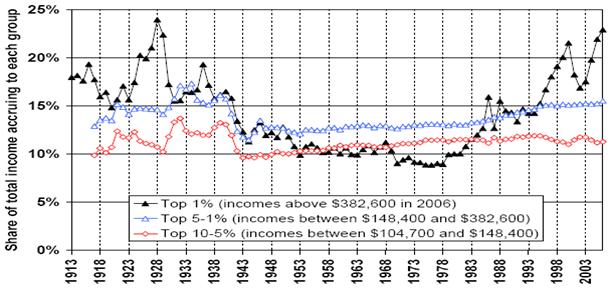

“How can Greece grow out of its debt if there is deflation?” asked Jean-Paul Fitoussi, a professor of economics at the Institut d’Études Politiques in Paris. “Deflation increases the debt burden, so we are following this virtuous circle that is bringing us toward hell. Economics has nothing to do with virtue, which can kill an economy.” There is also some doubt whether this latest package of 110 billion euros over three years will be enough to calm the markets, which may then turn on other vulnerable countries, like Portugal or Spain. Some countries that use the euro — Germany, in particular — need to pass legislation to come up with the money, although European Union officials said Sunday night that funding would be in place before May 19, when the next major tranche of Greek debt must be rolled over. Embedded in the euro and thus no longer in control of its own currency, Greece cannot take the easy way out of its debt by devaluing. So Greece must either cut its spending sharply or default on its loans — which would badly damage German and French banks carrying a lot of Greek debt.8. Very rich hate the super rich - James Kwak at Baseline Scenario has an interesting chart and piece on how rich Americans view the recent activities of the very rich investment bankers that helped get America (and the world) into this big mess. Kwak points to some research done by Rortybomb (Mike Konzcal) which shows a lot of the wealthy are very angry about what the very wealthy have done. This chart is fascinating as it shows just how much of the income is now being gobbled up by the richest of the rich. It's at its highest point since just before the Great Depression.

One of Konczal’s points is that one group that is opposed to Wall Street — and supports stronger reform — is people who are doing well, but not nearly as well as the bankers and fund managers in the top 1%. He focuses in particular on certified financial analysts — people who make a lot of money and know how the financial system operates, and are outraged at Wall Street. 68% of them support the Volcker Rule to prevent banks from engaging in proprietary trading. Konczal calls it the “rage of the 1.5% class.” Michael Lewis, in an interview with Christopher Lydon, said that in his book tour, a lot of his audiences are well-off and moderate well-off professionals — doctors, dentists, lawyers, small business owners, etc. These are people who (at least according to them) followed the rules, worked hard, paid their taxes, made a fair amount of money, etc. — and just saw the economy almost collapse because of what they see as the shenanigans of a tiny, tiny elite that plays by a different set of rules. Lewis or Lydon (I can’t recall which) called it a “revolt of the petty bourgeoisie.”

9. Corn glorious corn - This is a fascinating report in the New York Times about how American food manufacturers are turning away from high fructose corn syrup after years of facebook, youtube and other consumer campaigns have pushed consumers towards more natural sugars. This movement away from high energy manufactured foods is not going away. That is a good thing. Even ConAgra, the biggest of the big ugly Agrigusinesses, has stopped putting corn syrup into its Ketchup. How long before Fonterra faces such a campaign for all the commoditised versions of milk-based proteins and fats to be removed from the food manufacturing process?

9. Corn glorious corn - This is a fascinating report in the New York Times about how American food manufacturers are turning away from high fructose corn syrup after years of facebook, youtube and other consumer campaigns have pushed consumers towards more natural sugars. This movement away from high energy manufactured foods is not going away. That is a good thing. Even ConAgra, the biggest of the big ugly Agrigusinesses, has stopped putting corn syrup into its Ketchup. How long before Fonterra faces such a campaign for all the commoditised versions of milk-based proteins and fats to be removed from the food manufacturing process?

Hunt’s ketchup is among the latest in a string of major-brand products that have replaced the vilified sweetener. Gatorade, several Kraft salad dressings, Wheat Thins, Ocean Spray cranberry juice, Pepsi Throwback, Mountain Dew Throwback and the baked goods at Starbucks, to name a few, are all now made with regular sugar. What started as a narrow movement by proponents of natural and organic foods has morphed into a swell of mainstream opposition, thanks in large part to tools of modern activism like Facebook, YouTube and Twitter and movies like “Food, Inc.” and “King Corn.” As a result, sales of the ingredient have fallen in the United States. Charlie Mills, an analyst at Credit Suisse, says that the combined United States sales of high-fructose corn syrup for Archer Daniels Midland, Tate & Lyle and Corn Products International were down 9 percent in 2009, compared with 2007. A further decline is expected this year, he says.10. Totally irrelevant video - Jon Stewart from The Daily Show has picked up on this mad PowerPoint slide that the US military were using in Afghanistan. Remember we pointed to it in our Top 10 last Wednesday.

| The Daily Show With Jon Stewart | Mon - Thurs 11p / 10c | |||

| Afghanistan Stability Chart | ||||

|

||||

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.