Here are my Top 10 links from around the Internet at 10 past 2pm. I welcome your additions and comments below or please send suggestions for Wednesday's Top 10 at 10 via email to bernard.hickey@interest.co.nz

1. A toe deeper in hot water - Gareth Morgan has bravely put his toe even deeper in the hot debate around health rationing in this NZHerald column. He is absolutely right to stir this one up. Politicians would prefer simply to shut their eyes and put their fingers in their ears and chant 'LA LA LA LA...' when this is raised, but it has to be dealt with. Here's Gareth's big toe in some hot water:

Empirical-based objective indicators such as QALYs (quality adjusted life years) which indicate what impact treatments have on the number of quality years of life that can be expected for the patient, and CPACs (clinical priority assessment criteria) which tell us the chance of success a certain procedure might have for a given patient as well as how material the improvement will be for that particular patient - are the tools of the rationing trade.

Who then is the ideal leader of the public's quest for rational rationing? A national health committee that's apolitical and led by leaders of the professions involved - docs, nurses and managers - determining on a national basis, the prioritisation schema is the only credible way forward. The sector has to provide the leadership for the public. We don't know how to make the call and it's self-evident that politicians responding to lobbyists have demonstrated incapacity as well.

The result of the allocation should be that the patient's geographical location is irrelevant, their advocacy irrelevant, and the political regime of the day should be irrelevant. A national health system, rationing its limited resources in an equitable and transparent way, led by health sector professionals in the public interest, with politicians only having to set the overall budget, is overdue.

Whisper it quietly. Who wants to set up a death panel?

2. A golden mystery - The Telegraph reports that a tiny footnote in the Bank of International Settlements' (BIS) annual report seems to have unnerved the gold market. Some players fear the BIS could dump 380 tonnes or 20% of the world's annual gold output onto the market. But its not so simple, the Telegraph finds. Some are also thinking the BIS has bailed out either another central bank or a major bank on the quiet. Plenty for gold bugs, who are prone to the odd conspiracy theory, to chew over.

Economists and gold market-watchers were determined to hunt down which bank is short of cash – curious about who is using their stash of precious metal for what looks suspiciously like a secret bailout.

At first it looked like the BIS was swapping gold with a troubled central bank. After all, the institution is the central bankers' bank and its purpose to conduct transactions with national monetary authorities.

3. Inexorable funding pressures -Stephen Bartholomeuz at businessspectator.com.au has taken a close look at the longer term funding needs of the big four Australian banks in the context of huge demand for funds from European banks and governments over the next couple of years. He makes some good points. The end result is higher funding costs and deleveraging. Sound familiar?

He points out the Australian banks have already been working hard to lengthen their funding. They may even have to do the unthinkable and borrow long to lend long. Heaven forbid. Whatever next. A bank that doesn't borrow short and lend long?

Westpac, with the biggest wholesale funding task, has been particularly aggressive, regularly featuring among the biggest bank borrowers in the globe. Nevertheless, depending on their balance sheet growth, the four big Australian banks will have to raise roughly A$150 billion over the next two or three years – in competition with the rest of the international sector and governments.

Some of the Australian banks are already taking the view that whatever short-term funding they have is essentially irrelevant – in planning for their medium needs they need to get to the point where their reasonable expectations of growth are funded entirely with, at worst, borrowings that mature beyond 12 months.

Given the likely accelerated global scramble for term funding, and despite the prospective short to medium-term cost, it is in the interests of the banks and their economies to pull forward their anticipated funding needs and temporarily abandoning the classic banking model (and depressing their profitability) by borrowing long to lend long.

4. Election can't come soon enough - Australian Prime Minister Julia Gillard is apparently looking for an election date smartish, the Australian reports. Soon won't be soon enough for the big four Australian banks, who are all desperate to put up their mortgage rates to reflect higher funding costs, but know they can't do it before the election.

There is nothing more politically popular than beating up the banks during an election campaign.I wonder if this will become an election issue for the banks here next year? I'm already hearing murmurings under the surface between banks and politicians about the Core Funding Ratio in particular. The last thing the government needs during an election year is a lending freeze. Or are higher rates better? Either will hurt.

Cost pressure facing the big banks was highlighted by Westpac's move in late June to raise $800 million in five-year funding at 35 basis points more than a similar deal seven months ago. A report by Macquarie Equities Research shows the banks could justify increasing their standard variable lending rates, but were likely to be dissuaded by the political environment.

The banks have tentatively agreed to restrict rate rises to the RBA's official moves in the short term, but are expected to move after the election, which could be called as early as this week.

Macquarie analyst Michael Wiblin said National Australia Bank could be the first to lift rates after the election because its 7.24 per cent standard variable rate was the lowest of the four majors (by 12 basis points).

5. No so much 'eating bitterness' - The New York Times reports here about the problems China's factories are having now finding cheap and easy workers. The new Chinese workers are less pliant and want higher wages with more time off. There's a delightful phrase in the story about workers no longer wanting to 'chi'ku' or 'eat bitterness'. The term we'd use is 'swallowing rats'

In recent months, as the country’s export-driven juggernaut has been revived and many migrants have found jobs closer to home, the balance of power in places like Zhongshan has shifted, forcing employers to compete for new workers — and to prevent seasoned ones from defecting to sweeter prospects. The shortage has emboldened workers and inspired a spate of strikes in and around Zhongshan that paralyzed Honda’s Chinese operations earlier this month. The unrest then spread to the northern city of Tianjin, where strikers briefly paralyzed production at a Toyota car plant and a Japanese-owned electronics factory.

Although the walkouts were quelled with higher salaries, factory owners and labor experts say that the strikes have driven home a looming reality that had been predicted by demographers: the supply of workers 16 to 24 years old has peaked and will drop by a third in the next 12 years, thanks to stringent family-planning policies that have sharply reduced China’s population growth.

In Zhongshan, many factories are operating with vacancies of 15 to 20 percent, compelling some bosses to cruise the streets in their BMWs and Mercedeses in a desperate hiring quest during crunch time. The other new reality, perhaps harder to quantify, is this: young Chinese factory workers, raised in a country with rapidly rising expectations, are less willing to toil for long hours for appallingly low wages like dutiful automatons. But the more immediate challenge is to the Chinese export machine, which churns out about a third of China’s gross domestic product. Stanley Lau, deputy chairman of the Hong Kong Federation of Industries, whose 3,000 members employ more than three million workers, said he had been advising factory owners to offer better salaries, to treat employees more humanely and to listen to their complaints.

“The young generation thinks differently than their parents, they have been well protected by their families, and they don’t like to ‘chi ku,’ ” Mr. Lau said. The expression “chi ku,” or eat bitterness, is a time-honored staple of Chinese culture. But for young workers in Zhongshan, it is not the badge of honor that an older generation wore with pride.

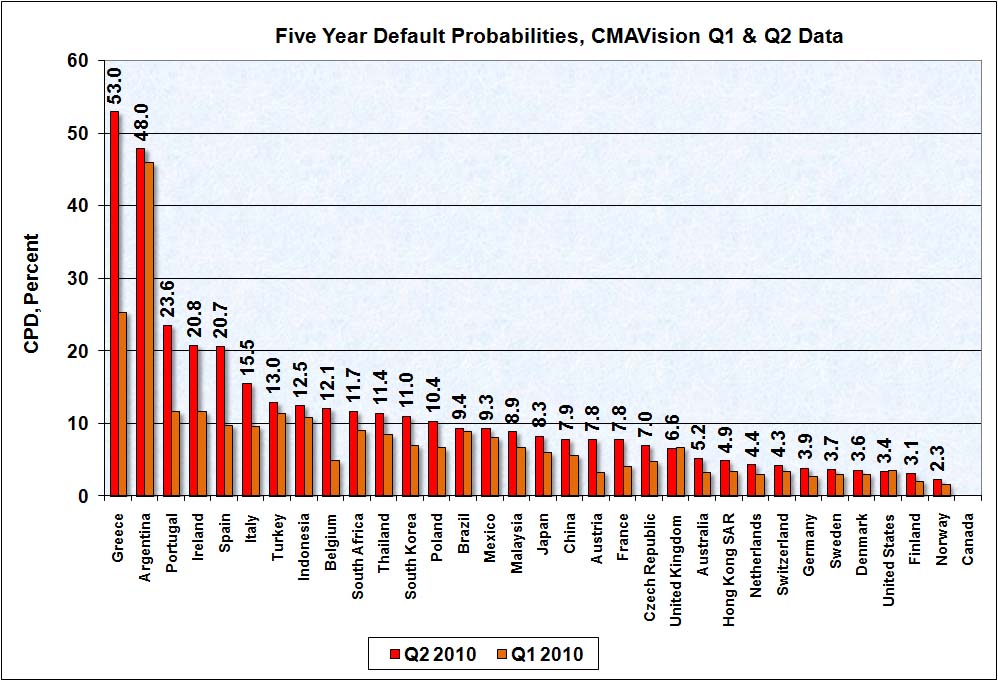

6. Australia's sovereign default risk - 'Some investor guy' over at the CalculatedRisk blog has worked out what the markets are expecting will happen with various countries' sovereign debt over the next five years. He/she has worked out what the expected default rates for the individual countries are. Australia's risk of default has nudged up to 5.2% with a few others in the last couple of months in the wake of the European Financial shenanigans. The chart with the full list is below.

This partly explains why funding costs for the Australian (and New Zealand) banks have risen in recent months.

As of June 30, 2010, the weighted average expected default rate is 7.4%. When weighted by value of debt outstanding, CDS pricing worldwide points to 7.4% of it defaulting within 5 years.

If the outstanding sovereign debt was still $34 trillion as reported at 12/31/09, that’s $2.5 trillion of defaulted debt. If the trend of increased borrowing has continued to $36 trillion at 6/30/10, it’s about $2.7 trillion of defaulted debt.

7. Peak oil - Global insurance market, Lloyds of London and Chatham House, have issued a warning about the effect of peak oil on insurance costs and business costs, The Guardian reports.

HT AndyH via email

The Lloyd's insurance market and the highly regarded Royal Institute of International Affairs, known as Chatham House, says Britain needs to be ready for "peak oil" and disrupted energy supplies at a time of soaring fuel demand in China and India, constraints on production caused by the BP oil spill and political moves to cut CO2 to halt global warming.

"Companies which are able to take advantage of this new energy reality will increase both their resilience and competitiveness. Failure to do so could lead to expensive and potentially catastrophic consequences," says the Lloyd's and Chatham House report "Sustainable energy security: strategic risks and opportunities for business".

The insurance market has a major interest in preparedness to counter climate change because of the fear of rising insurance claims related to property damage and business disruption. The review is groundbreaking because it comes from the heart of the City and contains the kind of dire warnings that are more associated with environmental groups or others accused by critics of resorting to hype.

8. It's a bigger hole - Britain's budget deficit is closer to 2 trillion pounds than the official estimate of 1 trillion, according to the Centre for Economics and Business Research, HT Gertraud via email. The Daily Mail reports this would increase public debts to 138% of GDP from 62%.

The national debt - forecast to reach £932m by next spring - does not include a number of expensive liabilities, such as the cost of civil service and town hall pensions and projects funded under the Public Finance Initiative. Putting these liabilities into the official figure would add £1.13 trillion to Britain's whopping overdraft, according to CEBR.

9. Chinese credit rating - This is fun. China is now looking to get into the credit rating business to challenge Moody's and Standard and Poor's. Shanghai Daily.com reports that Danong International Credit Rating Co has put a AA negative rating on US government debt, putting it below Chinese debt and debt from 11 other countries, including Australia and New Zealand on AAA. China is developing its own international satellite news network, its own news agency service and now its own credit rating service. How long before Chinese banks start expanding internationally in a serious way. HT Gertraud via email.

Dagong, founded in 1994 to rate Chinese corporate debt, says it is privately owned and pledges to make its judgments impartially.

Dagong's chairman, Guan Jianzhong, said the current Western-led rating system is to blame for the global crisis and Europe's debt woes. He said it "provides the wrong credit-rating information" and fails to reflect changing conditions. "Dagong wants to make realistic and fair ratings," he said.

Dagong's report covered 50 governments and gave emerging economies such as Indonesia and Brazil better marks than those given by Western agencies, citing high growth.

10. Totally irrelevant video - Ever wondered if you could get Darth Vader's voice on your GPS. Apparently TomTom managed to get Darth into a studio. "Is there any way you could breathe a little quieter...?"

1 Comments

FYI to all. Chinese stocks are down 2% after the central bank rejected calls to ease curbs on property speculation, Reuters reported.

"Chinese stocks fell 2 percent on Tuesday on reports that Beijing will not relax tougher property measures any time soon, weighing on the Australian dollar and curbing early gains in Asian shares."

And here's the Bloomberg version with the key detail

"Authorities intensified a crackdown on property speculation in April. Besides raising minimum mortgage rates and down- payment ratios for some home purchases, the government has pledged to boost land supply and the construction of low-cost public homes. Officials may also trial a property tax, according to state media. China needs to “normalize” monetary policy to stablize economic growth, the China Business News reported Wu Xiaoling, a former People’s Bank of China deputy governor, as saying. Wu called last year’s policy “extremely loose,” the report said."

cheers

Bernard

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.