Here are my Top 10 links from around the Internet at 10 to 1pm. I welcome your additions and comments below or please send suggestions for Friday's Top 10 at 10 via email to bernard.hickey@interest.co.nz

1. Buckle up tight - It's finally dawning on the Australians that they're living in the biggest housing bubble on the planet. This BusinessDay/Colmar Brunton survey shows that for the first time this year Australians believe prices will fall or be flat.

This is ominous. If house prices really slump in Australia that will make their banks (which means our banks) a lot more nervous about lending more into property.

If foreign lenders get wind of this it will push up the cost of all that foreign borrowing that Australians have done. When the Australian banks are punished we will be punished too. Let's hope the Europeans, the Japanese, the Chinese and the Americans don't notice. Or there's another crisis somewhere else to distract them... Fingers crossed.

Meanwhile, don't be too surprised if the banks tighten up their lending criteria and start lifting interest rates more than any increases in the Official Cash Rate.

SENTIMENT among Australian property investors is turning increasingly bearish, according to the latest Investor Pulse poll of investors conducted by Colmar Brunton and BusinessDay. For the first time this year, the number of investors expecting house prices to remain flat or fall outweighs those who see prices rising. The fundamental reason for the shift in sentiment is a dawning belief that Australian housing is in a ''bubble'' that at some point will burst and return to historic levels of affordability.

When asked about recent comments by famed US fund manager and property bubble expert Jeremy Grantham - who described Australian and British property as the only two of 34 bubbles he had studied that had not yet burst - 43 per cent of investors agreed that reversion to the mean would involve considerable pain. Only 25 per cent of investors disagreed with the bubble diagnosis and 32 per cent were undecided.

2. Just to ram it home - The Economist has come out and described the Australian housing market as the world's most overpriced, the Australian reports.

The Economist magazine this week declared that Australian property had the poorest return on investment of the 20 countries it evaluated.

The Economist's analysis calculated what it called the "fair value" of housing, based on the current ratio of house prices-to-rents to historic ratios. It found that Australian property was the most overvalued at 61 per cent. Next on the list was land-poor Hong Kong (53 per cent overvalued), followed by Spain (50 per cent overvalued).

Last month, US financial commentator Edward Chancellor said that Australia was in the midst of an unsustainable housing bubble. Mr Chancellor, a published author who is believed to have been among the first to predict the Global Financial Crisis, estimated Australian house prices were more than 50 per cent above their fair value - a once in 40-year event.

3. Tax crackdown - German authorities raided the offices of Credit Suisse overnight on the hunt for more detail to show Credit Suisse helped clients avoid paying tax, CNN reports.

This is all about governments hunting for money everywhere they can and no one is safe, even the rich guys with the best bankers and lawyers.

We're seeing that here too as the IRD gets much more aggressive in hunting down cases like the Trinity forestry tax scheme, the Penny vs Hooper case and the bank structured finance case. This will become a theme of coming years. Increasingly aggressive governments backed by a grumpy middle class will target the wealthy and not so wealthy who are deemed to not be paying their fair share. Fair enough.

The German case really got going when someone inside Credit Suisse leaked a bunch of CDs with data to the authorities. Or they were stolen. No one is quite sure. I can think of no better use for former Cold War era intelligence officers than stealing this sort of stuff.

The Düsseldorf prosecutors' investigation -- which started several months ago and is said to involve more than 1,000 individual cases -- is one of a number based upon information allegedly stolen from banks and sold or provided to German authorities. The inquiries have been controversial because they seem to be based on stolen information.

Some authorities have refused to purchase data. In many cases, uncertainty over what bank information might be circulating has caused concerned customers to come clean to authorities about their assets held outside Germany to escape possible prosecution.

The inquiries come as authorities round the world have stepped up efforts to curb tax evasion after the financial crisis and have contributed to occasional flare-ups between Germany and its smaller neighbours.

4. QE II is coming - Jim Grant of the very influential newsletter Grant's Interest Rate Observer (one of my heroes) talks here in this Bloomberg interview about why the US Federal Reserve is preparing to print again.

Zerohedge puts its spin on the interview here.

Jim Grant, one of the most respected voices in the financial industry, joins Zero Hedge and others, who see that the only choice the Federal Reserve has now that the temporary and shallow reprieve from the clutches of the deflationary depression is over, is to print more money in the form of another iteration of QE.

Whether this will be another $2.5 trillion, like last time, which was the price of an 18 month delay of the inevitable, or a $5 trillion concerted global effort, as Ambrose Evans-Pritchard believes, is irrelevant: the only option the central printers, pardon, bankers, have left is to flood the market with yet more worthless paper (keep an eye out on the doubling in the price of gold the second QE2 is publicly announced, which will also double as the obituary for all fiat paper).

5. 30% tax hike needed - Britain's Office of National Statistics has done a 26 page study showing that Britain's true public debts are closer to 4 trillion pounds, not the 1 trillion pounds previously estimated, once you take into account the public pensions and healthcare promises currently made. The National Institute of Economic of Social Research has estimated that current taxpayers ought to be paying 30% more in taxes to relieve future generations of this unfair burden. Here's The Independent's version of the story.

The true scale of Britain's national indebtedness was laid bare by the Office for National Statistics yesterday: almost £4 trillion, or £4,000bn, about four times higher than previously acknowledged.

It quantifies the burden that will be placed on future generations, and it is the ONS's first attempt to draw together the "off-balance-sheet" liabilities that have been accumulated by the state. The figures imply a huge "intergenerational transfer" – broadly in favour of today's "baby boomer" generation at the expense of younger people and future generations. The debt primarily consists of the cost of public sector and state pensions, and of payments promised to private contractors under private finance initiatives.

If the current generation of taxpayers wanted to remove the higher bills facing their children and grandchildren, they would now be paying around 30 per cent more in tax.

In research published alongside the ONS data, the National Institute of Economic and Social Research (NIESR) said that current taxpayers ought to be paying around 30 per cent more in tax to relieve future generations of that "unfair" burden. That also takes account of the additional health needs of the baby boomers as they reach their autumn years.

Failure to cut back now or raise taxes – and there is little sign of the population clamouring to make life easier for the as-yet-unborn – will leave future taxpayers with an additional burden of £200,000 each over their lifetimes to pay for the public services enjoyed by this and previous generations. Even with current plans to reduce the deficit, the tax bill would still be as high as £150,000 over the life of someone born in 2011.

Are things any different here in New Zealand? I'm going to Wellington next week to report on a conference organised by the Retirement Commission on the issue of intergenerational equity. Maybe we need some similar research. Your views?

6. The problem with democracy - Many in America are wondering about democracy's ability to govern wisely, particularly given the capturing of the arms of government by the banking and big business elites and the failure to turn around the economy. Some are even suggesting the overthrow of democracy, according to Zerohedge, which links to an essay by Dominic Hobson of Global Custodian.

Consumer sovereignty is far more powerful a constraint on the rich than political sovereignty. Indeed, even the erosion of the rich by democracy is ultimately self-defeating, for it eliminates that class of men and women in public life who are under no financial pressure to remain at their posts, pursuing policies in which they no longer believe. It is no coincidence that the democratization of politics has been accompanied by a decline in resignations on points of principle or of honor. The vast majority of modern politicians simply needs the money.

But even the restoration of a rentier political class would not be enough to restore the blessings of good government. As long as politicians must compete for votes, they cannot govern honestly, or even disinterestedly. They cannot reverse decisions or policies that have proved unworkable. They must persist, even in intellectual error, and cannot escape a certain narrowness of vision. To release politicians from this predicament, a revolution is required.

That revolution must be one not of blood, but of constitutional and political ideas. It must put an end to democracy without limits, before the prosperity of the species is destroyed and liberty extinguished...

The only lasting solution to the plague of unlimited democracy is to attack democracy at its moral foundation: the political equality of the citizen

7. The pain in Spain - Ambrose Evans Pritchard at The Telegraph has written about the likely defaults by Spain's city councils. The European crisis is far from over.

Spain's federation of regional governments said councils were heading for slow "asphyxiation", with many facing a payroll cut-off next month.

Pedro Arahuetes, mayor of Segovia and head of the federation's finance committee, told The Daily Telegraph that councils had lost up to 30pc of tax revenues because of the property and construction crash, and a further 20pc in funding cuts by Madrid.

The body has called for a moratorium until 2012 on debts to central government, which is itself slashing wages by 5pc as a quid pro quo for backing from the EU's €750bn (£626bn) rescue. Council debt is just 3pc of Spanish GDP, so default risk is modest. The greater worry is political as Spain's depression grinds on.

8. Here's the solution - California's unemployed have migrated up to the rivers of northern California to dig gold out of river beds with shovels. That way they can make some money... The Telegraph has the story of David Basque, a former carpenter who now lives in a tent and makes US$1,000 a month prospecting for gold. The chart links to an interesting article in the Economist questioning the continued rise in the price of gold. Bonus!

8. Here's the solution - California's unemployed have migrated up to the rivers of northern California to dig gold out of river beds with shovels. That way they can make some money... The Telegraph has the story of David Basque, a former carpenter who now lives in a tent and makes US$1,000 a month prospecting for gold. The chart links to an interesting article in the Economist questioning the continued rise in the price of gold. Bonus!

Now, day after day, David rises from the floor of his yurt – a round tent patterned after an ancient American Indian design – grabs his machinery and hits the Klamath river. His yurt is up in the hills west of the little frontier town of Yreka in far-north California and there are months when he can gouge $1,000 worth of gold out of the river.

‘I’d be in tough shape without it,’ he says.

There was a time – 1849, to be precise – when the desperate, the poor and those simply seeking a new life came to California from all over the nation. And when a handful of pioneers found gold in the Sierra foothills, Gold Fever turned into a frenzy. The idea was that you’d come here, sink your pick into the ground and make a fortune. Today – driven by the Great Recession, soaring gold prices, and a new, desperate energy among the jobless and the dreamers – there is a new gold rush going on in California. It takes a certain kind of person to be a New 49er, the kind of person who embraces living outdoors much like a mountain man, yet there are more and more of them.

The best measure of exactly how many is the number of mining claims on file with the US Bureau of Land Management in California; five years ago there were 15,606, in late 2009 that had increased to 23,974.

9. Financial engineering on a grand scale - Satyajit Das has written in the FT.com about the European rescue fund (EFSF) and how it is essentially an exercise in financial engineering and will fail. Well worth a read.

Major economies have over the last decades transferred debt from companies to consumers and finally onto public balance sheets. A huge amount of securities and risk now is held by central banks and governments, which are not designed for such long-term ownership of these assets.

There are now no more balance sheets that can be leveraged to support the current levels of debt. The effect of the EFSF is that stronger countries’ balance sheets are being contaminated by the bail-out. Like sharing dirty needles, the risk of infection for all has drastically increased.

The reality is that a problem of too much debt is being solved with even more debt. Deeply troubled members of the eurozone cannot bail out each other as the significant levels of existing debt limit the ability to borrow additional amounts and finance any bail-out. The EFSF is primarily a debt shuffling exercise which may be self defeating and unworkable. The resort to discredited financial engineering highlights the inability to learn from history and the paucity of ideas and willingness to deal with the real issues.

10. Totally irrelevant video - Here's Rachel Maddow with a report about deja vu all over again with a couple of US oil spills. HT Emille via email

2 Comments

FYI Vance Arkinstall of Dominion Finance Fame has resigned as the CEO of the Investment, Savings and Insurance Association because he faces criminal charges over misleading and false investment statements...

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=10658924

cheers

Bernard

And FYI this interesting one courtesy of Gertraud

http://theautomaticearth.blogspot.com/2010/07/july-14-2010-is-it-time-t…

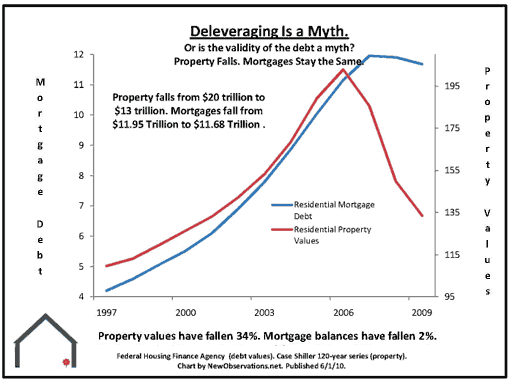

It points out that the US is not deleveraging, in large part because housing equity has collapsed but debt remains.

{kind=link}

Americans seem now to be feeling a tad revolutionary. They are realising the big 6 banks have won a taxpayer funded bailout of monstrous proportions and home owners are left to pay off crushing debts over decades.

cheers

Bernard

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.