Here are my Top 10 links from around the Internet at 10 to 12 pm, brought to you in association with New Zealand Mint for your reading pleasure.

I welcome your additions and comments below, or please send suggestions for Tuesday's Top 10 at 10 via email to bernard.hickey@interest.co.nz. Remember that registered commenters can more easily include links out in their comments. Use the box in the right hand column to register. We're turning off unregistered comments from September 12.

I'll pop any surplus suggestions I get into the comment stream under the Top 10.

1. Norse god of thunder - Is the solution to the world's energy problem a rare metal named after the Norse God of Thunder.

Ambrose Evans Pritchard writes at The Telegraph about the wonder metal Thorium and its ability to replace uranium as a clean source of nuclear energy.

There is no certain bet in nuclear physics but work by Nobel laureate Carlo Rubbia at CERN (European Organization for Nuclear Research) on the use of thorium as a cheap, clean and safe alternative to uranium in reactors may be the magic bullet we have all been hoping for, though we have barely begun to crack the potential of solar power.

Dr Rubbia says a tonne of the silvery metal – named after the Norse god of thunder, who also gave us Thor’s day or Thursday - produces as much energy as 200 tonnes of uranium, or 3,500,000 tonnes of coal. A mere fistful would light London for a week. Thorium eats its own hazardous waste. It can even scavenge the plutonium left by uranium reactors, acting as an eco-cleaner. "It’s the Big One," said Kirk Sorensen, a former NASA rocket engineer and now chief nuclear technologist at Teledyne Brown Engineering.

"Once you start looking more closely, it blows your mind away. You can run civilisation on thorium for hundreds of thousands of years, and it’s essentially free. You don’t have to deal with uranium cartels," he said.

2. The problem with Bernanke - Steve Keen nails the problem with Ben Bernanke's speech on Friday night.

Bernanke’s recent Jackson Hole speech didn’t contain one reference to the key force driving the American economy right now: private sector deleveraging. The reason the US economy is not recovering from this crisis is because all sectors of American society took on too much debt during the false boom of the last two decades, and they are now busily getting themselves out of debt any way they can.

Debt reduction is now the real story of the American economy, just as real story behind the apparent free lunch of the last two decades was rising debt.

The secret that has completely eluded Bernanke is that aggregate demand is the sum of GDP plus the change in debt. So when debt is rising demand exceeds what it could be on the basis of earned incomes alone, and when debt is falling the opposite happens.

3. The size of the task - Eric Johnston at The Age reports that Australian banks will have to find A$150 billion of foreign and local funding over the next 12 months.

The giant funding task will put Australian banks in competition with other banks and governments and around the world that are seeking to raise trillions of dollars from bond markets.

Global demand for funds, particularly the longer-term debt which is sought by banks, will keep banks under pressure to raise interest rates until at least the middle of next year.

Of the local lenders, Commonwealth Bank has the biggest requirement, eyeing $50 billion over financial 2011. Westpac is eyeing $40 billion, while ANZ and National Australia Bank are each planning to raise between $20 billion and $25 billion.

By comparison, the Australian government is expected to borrow about $38 billion for its funding needs.

4. The problems with CFDs - Stuart Washington and Adele Ferguson from The Age have done an investigation of Contracts for Difference (CFD) traders in Australia. It is not pretty reading.

CFDs are clearly controversial. No one comes out of it looking good. Investors are described at 'cat's meat'. The market is described as an 'unscrupulous casino' and the instruments as 'Contracts for Dickheads.' HT Kevin via IM.

BusinessDay can reveal the aggressive recovery actions are the unadvertised flip side of some providers' business model, part of which is based on profits made from investor losses.

In the case of the country's second-biggest CFD provider, CMC, internal company documents and extensive interviews show that until recently it operated like an unscrupulous casino: identifying the least savvy investors; acting to capture their losses, and using mechanisms to manipulate win rates. As a sign of just how badly stacked the odds are, these unsophisticated investors are referred to as "cats' meat" by some industry participants.

The providers make their money luring the unsophisticated to trade products that are banned in the US and are considered by the corporate regulator as "much riskier than a flutter on the horses or a night at the casino'' because potential losses are unlimited.

ASIC commissioner Greg Medcraft said it would be immoral and unethical if providers were relying on dumb or inexperienced customers to lose money so the providers could profit. But - given that net unhedged customer losses translate directly to gains for providers - this is part and parcel of some providers' business models.

And BusinessDay's investigations reveal, to the surprise of ASIC, the premeditated nature of how CMC Markets has profited from those least able by using the C-Book category. CMC went to some lengths to hide its profiling from its customers, stating in the document obtained by BusinessDay: "IT IS ESPECIALLY IMPORTANT THAT NONE OF THE INFORMATION IN THIS SECTION IS RELAYED TO CLIENTS."

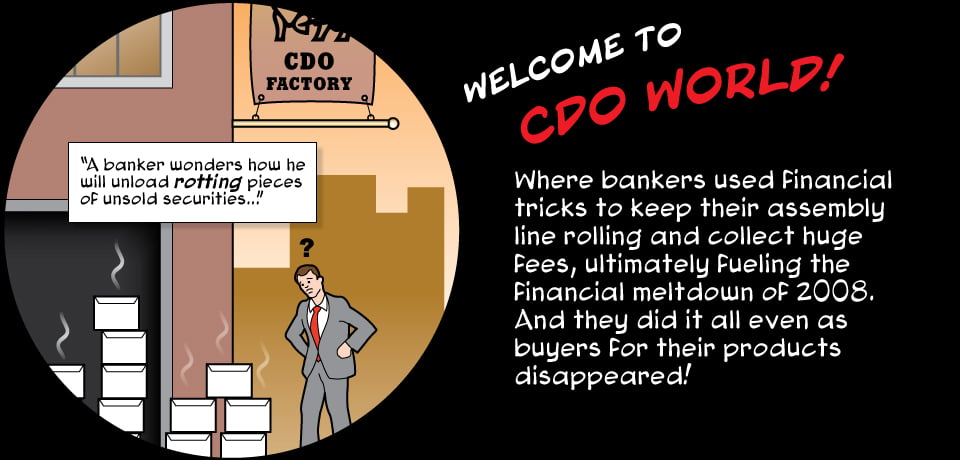

5. How Wall St extended and pretended - ProPublica and NPR have written a cracking analysis of how Wall St kept the mortgage Ponzi scheme going through 2006 anf 2007. Anyone who has read Michael Lewis' 'The Big Short' will find this familiar.

Over the last two years of the housing bubble, Wall Street bankers perpetrated one of the greatest episodes of self-dealing in financial history. Faced with increasing difficulty in selling the mortgage-backed securities that had been among their most lucrative products, the banks hit on a solution that preserved their quarterly earnings and huge bonuses: They created fake demand. A ProPublica analysis shows for the first time the extent to which banks -- primarily Merrill Lynch, but also Citigroup, UBS and others -- bought their own products and cranked up an assembly line that otherwise should have flagged.

The products they were buying and selling were at the heart of the 2008 meltdown -- collections of mortgage bonds known as collateralized debt obligations, or CDOs. As the housing boom began to slow in mid-2006, investors became skittish about the riskier parts of those investments. So the banks created -- and ultimately provided most of the money for -- new CDOs.

Those new CDOs bought the hard-to-sell pieces of the original CDOs. The result was a daisy chain that solved one problem but created another: Each new CDO had its own risky pieces. Banks created yet other CDOs to buy those. Individual instances of these questionable trades have been reported before, but ProPublica's investigation, done in partnership with NPR's Planet Money, shows that by late 2006 they became a common industry practice.

6. Does this seem fair? - People who pay cash are paying more for their goods and services than those who pay with credit cards because many people who use credit cards get rewards that are paid for through merchant fees. The implication is that people paying cash should pay a lower price than those paying with credit cards.

That's the conclusion of some research from the Boston Federal Reserve. And here's the New York Times' version of it.

The reward programs create “an implicit money transfer” to credit card users from noncard users (i.e. cash payers) because of the across-the-board price increases merchants put in place to cover the costs of accepting the cards. “This retail price markup for all consumers results in credit card-paying consumers being subsidized by consumers who do not pay with credit cards,” the researchers wrote in the report.

The use of credit cards and rewards, according to the report, is positively correlated with income, meaning that lower-income consumers tend to be the ones not using credit cards and instead paying cash.

7. Low rates cause deflation? - Here's an idea put forward by one of the US Federal Reserve governors. Very low interest rates for a very long time actually cause deflation. Columbia professor Rajiv Sethi writes about it here. Here's the thinking.

Long-run monetary neutrality is an uncontroversial, simple, but nonetheless profound proposition. In particular, it implies that if the FOMC maintains the fed funds rate at its current level of 0-25 basis points for too long, both anticipated and actual inflation have to become negative.

Why? It’s simple arithmetic. Let’s say that the real rate of return on safe investments is 1 percent and we need to add an amount of anticipated inflation that will result in a fed funds rate of 0.25 percent. The only way to get that is to add a negative number—in this case, –0.75 percent. To sum up, over the long run, a low fed funds rate must lead to consistent—but low—levels of deflation.

8. Third World America - Arianna Huffington has written a book called Third World America, which seems to have captured the mood in the world's biggest economy. It details "how our political and business leaders have abandoned the middle class and betrayed the American Dream." HT Andrew. Here's Janet Tavakoli on the same subject.

9. Fantastic swearers are liars - A study of 30,000 conference calls by CEOs and CFOs about their earnings has found those that swore a lot and said things were 'fantastic' were lying about their financial affairs. The Economist has the story.

Deceptive bosses, it transpires, tend to make more references to general knowledge (“as you know…”), and refer less to shareholder value (perhaps to minimise the risk of a lawsuit, the authors hypothesise). They also use fewer “non-extreme positive emotion words”. That is, instead of describing something as “good”, they call it “fantastic”.

The aim is to “sound more persuasive” while talking horsefeathers. When they are lying, bosses avoid the word “I”, opting instead for the third person. They use fewer “hesitation words”, such as “um” and “er”, suggesting that they may have been coached in their deception. As with Mr Skilling’s “asshole”, more frequent use of swear words indicates deception.

10. Totally irrelevant video - This is a trailer for a documentary about Ravi Shankar called Raga. It's not funny or rude. Looks fantastic. HT Emily Perkins via Twitter.

16 Comments

Here's Albert Edwards with his rather bearish view on the stock market

http://www.telegraph.co.uk/finance/markets/7966529/Stock-markets-face-a…

HT Andrew

cheers

Bernard

Re: thorium - there have been several very good threads on the subject @ the oildrum. Make sure and read the discussion threads - there are many interesting comments of a technical nature:

http://www.theoildrum.com/node/4971

http://www.theoildrum.com/node/3450

The idea of thorium use is not new. A bit of history

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9MTE4OTN8Q2hpbGRJRD0tMXxUeXBlPTM=&t=1

Former Clinton era Labour Secretary Robert Reich says lower interest rates simply encourage big businesses to buy each other and cut more jobs. Interesting thought. HT John Walley

http://robertreich.org/post/1033774961/warning-why-cheaper-money-wont-m…

"Cheaper money won’t necessarily create the kind of spending that generates more jobs. In fact, right now it’s having the opposite effect. When consumers and small businesses can’t and won’t borrow more, big businesses use cheap money to bid up the prices of corporate assets and cut payrolls. What we need now is more jobs, not bigger corporations. And that means focusing on the demand side of the economy, not the supply side."

cheers

Bernard

Re: 1.

http://www.chemicalforums.com/index.php?topic=7845.0

I presume Rubbia is Rubia. Note the date: This is nothing new.

Nuclear power manifests as electricity, of course. So we will all be driving electric cars with field-windings of copp.......oh dear. and mcp's incorporating rare earth.......s......oh dear, oh dear.

Some of us have already thought our way down that track, Mr AP. It may be that Thorium has a place in energy supply, but really we have left the lead-and-investment time too late, vs peak fossil-fuels.

The problem now (and I suspect what is in back of the piece) is that he can't get research funding, and has gone for the exposure, as they do. No funding because the fiscal world overshot the ability to produce forward capital, indeed, went into injury-time carrying debt. Lots of.

The no-comprende would be funny, had it not been so obvious for so long.

#4 - LOL! The Google add for the article slamming CFD's was for CMC markets which are slated in the article.

Re. #6 - I am always annoyed by retailers in NZ who, when I propose to pay with cash, refuse to give me a discount. When I travel to the US and the UK many retailers will suggest to me that if I pay with cash they will give me a discount. Why do NZ retailers dislike cash buyers?

Some links to Thorium. Fascinating. From what I gather the principle was known since 1939!!!

Come to think of it - in the 40's after the first Nuclear Bomb in Hiroshima, I was a small child then, my father mentioned that he envies me because I will experience in my lifetime that in order to provide heat and energy in a house we will go to a store, buy a little box, put it in the cellar and have and endless quantity of energy supply for our house.

We talked about this many times, I remember it well, it excited my children's fantasy.

There must have been information about this Thorium possibility around then and my father just clothed it into language a child could understand.

A pity tie Americans decided to develop the weaponry branch back then.

Dann puts the boot into Hubbard:

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=106…

Mind you I dont think he goes anywhere near far enough with his comments on Hubbard's apparent wrong doings.

Not before time!

Hubbard has had an incredibly easy ride from the press. However as it sinks in that this guy is likely responsible for the loss of hundreds of millions of taxpayers money the back lash should begin.

Ross - good read.

Cheers.

Professor Fekete wrote a paper a couple of years back -THE REVISIONIST THEORY AND HISTORY OF DEPRESSIONS - that included the concept of lowering interest rates casing deflation. The key insight is businesses/entrepenours getting trapped in a falling interest rate environment - sounds familiar - leading to bankruptcies and consequent deflation. "As interest rates fall, a vicious spiral is set in motion. Lower rates send prices lower, and lower prices send rates lower still. Bond speculators take advantage of the opportunity created by open market operations. They frontrun the Fed in buying government bonds first. The resulting fall in interest rates bankrupt productive enterprise that could not extricate itself from the clutches of debt contracted earlier at higher rates. The debt becomes ever more onerous as its liquidation value escalates past the ability to carry it. In addition, inadequate depreciation quotas undermine the financial structure of all firms, as explained above. The squeeze on capital causes wholesale bankruptcies among the producers. While they clearly have the power to put unlimited amounts of irredeemable currency into circulation, central banks have no power to make it flow in the “approved” direction. Money, like water, refuses to flow uphill. In a deflation it will not flow to the commodity and real estate markets to bid up prices there, as central bankers have hoped. Rather, it will flow downhill, to the bond market, where the fun is, bidding up bond prices. As the central bank has made bond speculation risk free, the bond market will act as a gigantic vacuum cleaner sucking up dollars from every nook and cranny of the economy. The sense of scarcity of money becomes pervasive. In feeding ever more irredeemable currency to the money market the central bank cuts the figure of a cat chasing his own tail. Contrary to the universal delusion that goes by the name “Quantity Theory of Money”, more fiat money pushes interest rates lower and falling interest rates squeeze producers more. They cut prices in desperation and cry out for the creation of still more fiat money. To be sure, they get what they ask for. But their medicine turns out to be their poison." http://professorfekete.com/articles\AEFRevisionistTheoryHistoryOfDepressions.pdf Good stuff, any comments out there?

No comment, waste of time, tomorrow all will be decided on SCF debacle

Kiwidave - good read. Makes sense of nonsense, so to speak.

Blimey..for a minute here I wondered what the hell he was doing in a hole like Lahore!

Protesters in the eastern city of Lahore slapped donkeys with shoes and pelted them with rotten tomatoes on Monday to vent their anger at the latest Pakistani cricket fixing scandal. .....Telegraph.

They held a gun to your head and forced you to borrow that money didn't they Iain!... If only you had opted to save up your pennies until you could afford to build with no debts.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.