Here's my Top 10 links from around the Internet at 7 pm in association with NZ Mint.

I welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

I'll pop the extras into the comment stream. See all previous Top 10s here.

My apologies for no Top 10 yesterday. I was off in Hamilton singing for my supper and here again in Auckland today. Nigel Farage is a hoot at #10.

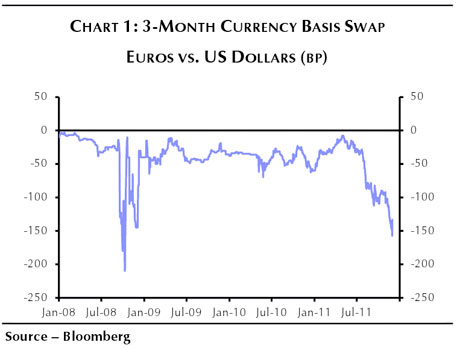

1. Here's why the central banks had to act last night - European banks were finding it nigh on impossible to get hold of US dollars at reasonable prices.

See the chart below showing the cost for banks of swapping euros into US dollars to service their US dollar debts. Back to Lehman levels.

There were rumours one really big European bank was about to collapse.

That's why the US Federal Reserve and its central banking mates were forced to take desperate action overnight.

But it hasn't really solved the problems.

What appeared to be a liquidity issue is now a full blown solvency issue that needs much more than the quick fix delivered last night by the US Federal Reserve.

Here's Jill Treanor at the Guardian.

Capital Economics explains that eurozone banks have had trouble being able to get funds in dollars, which is why the Bank of England joined the Federal Reserve, the Bank of Japan, the ECB, the Bank of Canada and the Swiss National Bank in taking measures to make it easier for banks to obtain dollars.

The upshot is that banks have been charging each other more and more to turn their euros into dollars and that the rates have been reaching levels close to those when Lehman Brothers collapsed in September 2008. Hence central banks decided to act.

But, Capital Economics cautions:

"Welcomed as the news was, we do not think it signals a turning point in the crisis. After all the dollar funding in the eurozone is symptomatic of a broader liquidity squeeze. And even if banks in the eurozone have less of a liquidity problem on their hands today than in they did in late 2008, they have a greater solvency problem".

2. Who's left to bail out the governments - Nomura research head Jon Peace makes a good point about the latest twist in the crisis.

Jon Peace, head of European bank research at Nomura, said: "It is an evolution of the crisis from three years ago, when countries took on the risks of the banks. Back in 2008, there was a lender of last resort – countries bailed out banks. This time it is governments that need a lender of last resort – but there is no obvious lender of last resort."

While the massive bank bailouts of October 2008 – in the month after Lehman collapsed – worked for a while in shoring up banks, confidence is again ebbing , even though the banks are much stronger then they were three years ago. This time the problems for banks is not the holes ripped through their books by exposure to US sub-prime loans, but their exposure to the governments of the eurozone – which are in turn searching for their own bailouts.

Explaining why getting access to dollars funding is important, Peace said: "The French banks do a lot of dollar-based lending, but there's not a natural source of deposits so they do it by wholesale funding [borrowing huge sums on the international money markets]. But US money market funds have withdrawn their exposure to European banks because they are worried about the sovereign risk."

3. Keep an eye on Iran and Israel - Stuff keeps blowing up in Iran in unexplained ways that may well be linked to Mossad. Now rockets are being fired at Israel from Iran's mates in southern Lebanon.

This could all easily go pear-shaped in a big hurry.

Things keep blowing up in Iran. On Monday the big bang was in Isfahan, and the black smoke billowed from the direction of the nuclear plant on the edge of the city. More than 24 hours later, Iran's official news sites had taken down an initial report and photograph and were offering an array of conflicting accounts instead. But if it was not yet even known exactly what blew up, the conclusions being rushed to were plain enough: 1) that it was something either military, or atomic, or both, and 2) that Israel had somehow caused it to happen.

Support for this view arrived a few hours later in Israel's northern Galilee region, in the form of four 122-mm Katyusha rockets. The rockets, which caused no injuries, were launched from southern Lebanon, which is controlled by Hizballah, a client of Iran. If the timing was a coincidence, it was a nice-sized one: There's been no attack like it for more than two years.

"How many missiles have they prepared themselves for?" Iran's defense minister asked on Sunday, speaking of Israel. "10,000? 20,000? 50,000? 100,000, 150,000 or more?" Brig. Gen. Ahmad Vahidi made his remarks before 50,000 volunteer recruits at Bushehr, site of Iran's newly minted nuclear power reactor.

4. The last refuge to which a scoundrel clings - Patriotism. So goes the Bob Dylan lyric.

Now the Italians are so desperate to sell their government bonds they are appealing to the patriotism of the Italian people in a similar way to the Greeks, who launched an appeal to expat Greeks in America to buy Greek bonds. Those who bought them now face 60% plus haircuts. Silly buggers.

The Italian Banking Association is promoting “BTP-Day” today, with lenders waiving fees for clients who buy government bonds and bills known as BTPs and BOTs at branches. The initiative, originally proposed by a Tuscan businessman, will be repeated on Dec. 12.

“Italian savers may be bondholders of last resort as banks and institutional investors are reducing holdings of government bonds,” said Wolfram Mrowetz, chairman of investment firm Alisei SIM in Milan, in an interview.

Giuliano Melani, a 51-year old financial consultant in the Tuscan town of Quarrata, paid for a full-page advertisement in the Italian newspaper Corriere della Sera on Nov. 4, exhorting his fellow citizens to acquire government bonds to show that Italians “are one people, a great people.” He said taking part in “BTP Day” will show the foreigners that “we Italians are not afraid and believe in our country.”

5. Thinking about the Future - Reuters reports many large European corporates have started planning for the end of the Eurozone.

When Novo Nordisk's chief financial officer met marketing colleagues last Friday the conversation moved far beyond the usual discussion of sales and performance. Jesper Brandgaard asked a simple, far-reaching question: how would the firm set prices for two pivotal new insulin products if the euro collapsed?

The Danish firm, the world's biggest maker of insulin for the treatment of diabetes, sits outside the euro zone but sells into it. It's a question that is being echoed - in various forms - in the boardrooms of banks, brokerages, trading houses, law firms and the world's leading manufacturers.

"It's hard to make detailed plans but we need to think through how our pricing strategy would fare if there were suddenly a dismantling of the euro," Brandgaard told Reuters. "How do we avoid falling into a trap? This is the first time I've asked such a question. It's a topic that is increasingly on the radar."

6. A continent stares into the Abyss - Der Spiegel reports some economists in Germany are calling for the reintroduction of the Deutschemark on Day X.

I'm not kidding. They aren't either.

Here's what they're saying in one of Germany's most prominent news organisations. The chart below shows the looming bond auctions that could trigger all this grief.

Hans-Joachim Voth, an economic historian who teaches in Barcelona, feels that the euro's days are numbered. He considers it advisable for economically strong countries like Germany to withdraw from the euro, because, so he argues, "not every stupid economic idea has to be defended to the bitter end." In theory, says Voth, the upcoming Christmas holidays could be a good time to take this step, because, as he argues, it's important to take the markets by surprise.

Dirk Meyer, a professor at the Helmut Schmidt University in Hamburg, also argues that the Germans should take the initiative and leave the euro zone as quickly as possible. He has even come up with a concrete time frame. Under his scenario, it begins on a Monday, or "Day X." On the preceding weekend, the government will have issued the surprise order that banks remain closed on this Day X. The bank holiday is needed to incorporate all savings and checking accounts into the changeover.

The specific problems of the current U.S. economy—the drastic increase in unemployment and sluggish increase in output—overlay a tendency of much longer duration, a drastic and rapid increase in the inequality of income. Every economy of complexity produces an unequal distribution of the good things in life. But the period immediately following World War II showed a considerably increased equality of income compared with either the Great Depression or the previous period of relative prosperity.

Since the middle 1980s, this tendency has been reversed. In the United States, median family income (adjusted for size) has remained virtually constant since 1995, while per capita income has risen at about 2 percent per annum. The difference in income between college graduates and those with only high school degrees increased at a rapid rate, even during the period before 1990 when per capita income grew very slowly. Further, the proportion of the college-age population enrolled in college, which had been rising rapidly, stopped increasing and has remained the same for thirty years.

Clearly, the bulk of the gains from increased productivity went to a small group of upper-income recipients. Indeed, closer study has shown that the bulk of the increase went to the top 1 percent of income recipients and much of that to those in the top .1 percent.

The causes of this growing inequality are varied. There has been a steady attack on the use of the tax system as a means of equalizing income. Income and estate taxes were once the most directly effective factors in redistribution. The top rate in the federal income tax was over 90 percent in the 1950s and is about 35 percent today.

8. The hedge funds are in control - This anonymous letter posted on Reddit is apparently from a first year analyst at a hedge fund. He/she wrote this for Occupy Wall St.

Hard to know if he/she is real, but it's worth a read.

Hedge funds. These guys are basically the vehicles of choice for ultra-rich people to get into the financial markets, besides family offices and private wealth managers. What are hedge funds? They are funds that have a 1-5 million deposit minimum, cater to the mega-rich, and can invest in anything without regulatory restrictions, use leverage to pump up their exposure by 15x, and pretty much eat up a vast majority of the industry's profits.

These guys invest in EVERYTHING. Instruments you've heard of - stocks, bonds, forwards, futures, currencies, and instruments that you, me, or anyone else have never even heard of, much less know anything about: commodity future swaptions, FRA/OIS swaps, CLOs, exotic future options, p-notes, index/commodity/equity exposures, and a huge array of OTC (over-the-counter) instruments that no regular investor would ever have access to.

Why I bring this up: the financial markets are rigged. 99% of the investing public has access to services such as basic brokerages, 401k/IRA's, mutual funds, pension plans, etc. Some of these services, especially pension funds, will invest into hedge funds, who take an additional 2 and 20 (meaning 2% of assets plus 20% of capital gains).

What this means is that if you go any of the traditional retail routes, you are utterly screwed facing off against the hedge funds.

And here's the final bit:

What does this all mean? It means the hedge fund industry is making a gigantic proportion of the profits. The top .1% is earning nearly half of the profits in the industry, through not just hedge funds, but other similar vehicles.

The finance industry is a complete scam, designed to funnel money from the 99% investing public into the hands of the top .1%. Sure, some of you will make good money, but stastically, the rest of us will lose, and who is feeding off us? Hedge funds, and the .1%. You have better odds going to a casino and playing slots, the worst-paying game in the house, but still better than the stock market.

Also, the government is in bed with the financial industry. Tax loopholes give hedge funds and other top players the ability to write off losses and not pay taxes on gains for years at a time. For income they derive from the hedge fund (profits), they pay only 15%, rather than the 35% income tax charged to most people earning 80k and above. Meanwhile, you have to pay taxes for not just your own income but also capital gains.

9. How rich are the super rich? - Mother Jones has a great selection of charts on wealth inequality in America. Well worth a click.

10. Totally entertaining speech from Eurosceptic Euro MP Nigel Farage - He called in this video below for all the Eurocrats around him to be fired.

It seems to capture quite nicely the mood in Europe.

39 Comments

Here's Ambrose at the Telegraph on what the central bank intervention really means:

The move came once it was clear that Europe's prostrate banks would struggle to roll over $2 trillion (£1.3 trillion) of debts denominated in dollars. Data from ratings agency Fitch shows that US money markets have slashed funding for French banks by 69pc and German banks by 50pc.

Strains have been ratcheting up over the past two weeks. European banks are mostly shut out of the dollar market, or only able to raise money for a week at a time.

The so-called "stress alarm" – the euro/dollar three-month cross currency basis swap – spiralled down to minus 166 points early on Wednesday, uncannily like the last days before the Lehman crisis metastasized in October 2008.

"Concerns have been building that Europe's banking system could go into meltdown," said Marc Ostwald from Monument Securities. "But the central banks may also have been worried that eurozone politicians will fail to deliver much at their December summit, so they need a mechanism in place to cope with the fall-out."

Andrew Roberts, rates chief at RBS, said European bank stress was reaching extreme levels. "They couldn't allow a sudden stop to the system. This at least takes away the precipice risk for now, but Europe is not going to able to tackle this crisis properly until Germany agrees to cross the Rubicon and accept massive bond buying by the ECB," he said.

There is little evidence yet that Berlin is willing to lift its veto on eurobonds or an ECB blitz. Chancellor Angela Merkel said it was "not appropriate" for to Germany drop its objections as a quid pro quo for backing from other EU states for treaty changes to police budgets. German finance minister Wolfgang Schauble said mass bond purchases and eurobonds are both illegal under EU treaties and remain "out of the question".

Jesse Eisinger at ProPublica is always worth a read:

Last week, I had a conversation with a man who runs his own trading firm. In the process of fuming about competition from Goldman Sachs, he said with resignation and exasperation: “The fact that they were bailed out and can borrow for free — It’s pretty sickening.”

Though the sentiment is commonplace these days, I later found myself thinking about his outrage. Here was someone who is in the thick of the business, trading every day, and he is being sickened by the inequities and corruption on Wall Street and utterly persuaded that nothing had changed in the years since the financial crisis of 2008.

The insiders have a critique similar to that of the outsiders. The financial industry has strayed far from being an intermediary between companies that want to raise capital so they can sell people things they want. Instead, it is a machine to enrich itself, fleecing customers and exacerbating inequality. When it goes off the rails, it impoverishes the rest of us. When the crises come, as they inevitably do, banks hold the economy hostage, warning that they will shoot us in the head if we don’t bail them out.

And I won’t pretend this is a widespread view in finance — or even a large minority. You don’t hear this from the executives running the big Wall Street firms; you don’t hear it from the average trader or investment banker. From them, we get self-pity. For every one of the secret Occupy Wall Street sympathizers, there are probably 15 others like Kenneth G. Langone, who, like downtrodden people before him, is trying to reclaim and embrace a pejorative, “fat cat.”

FYI the Chinese are actually quite worried. Here's Reuters.

http://www.reuters.com/article/2011/12/01/china-europe-debt-idUSL4E7N10EN20111201

The world economy is facing a worse crisis now than in 2008 and stimulating growth should be a priority for global policymakers, a Chinese vice finance minister said on Thursday.

The comments by Zhu Guangyao marked the latest grim warning from a Chinese official over the state of the world economy. Vice Premier Wang Qishan said in November that a chronic global recession was certain.

chinese manufacturing slows again:

http://www.bbc.co.uk/news/business-15978863

wait till the Europe recession really kicks in in 2012, then see what happens in China

was it Chanos who was predicting a Chinese crash in 2012????

Here's Nomura thinking the unthinkable via FTAlphaville:

Redenomination risk: Which Euros will stay Euros?…

Since the risk of some form of break-up is now material, investors should be thinking about “redenomination risk”: Which Euro denominated assets (and liabilities) will stay in Euro, and which will potentially be redenominated into new local currencies in a break-up scenario?

And how 'expensive' will goods and services be in the new currency?

When the Eauro was adopted the price of things changed significantly in The Netherlands and Germany (and likely other countries), particularly for things like flowers and dining out. A 22 Guilder bunch of flowers (22 Guilder = 10 Euro approx.) instead of costing 10 Euro, pretty much cost 22 Euro instead.

Re. 1 & 2. How did we ever get to thinking that the solution to having too much debt was ... more debt?!

"The money supply is still growing. The data contradicts the premise that the QE program was terminated. Easily explained. The initiative turned global to produce Global QE. The USFed has been accommodating the Europeans and Wall Street banks, so that the broken insolvent big Euro banks can be propped with more phony money. The Euro Central Bank is printing money heavily or else borrowing in heavy volume from the USFed Dollar Swap Facility. Without bond market buyers, the EuroCB has reluctantly filled the void and has been buying the Italian Govt Bonds. Recall that big Euro banks are huge sellers of sovereign bonds. The USFed never stopped printing money to buy USTreasury Bonds, which ramps up each month as USGovt debt piles up each month. Recall that foreign creditors are net sellers of USTBonds. The USTBond auctions have not failed, and for a reason. The USFed is buyer of last resort. Where the bids came from has been kept quite secretive. It is the USFed, which never stopped QE. In fact, Global QE is the mainline policy nowadays, and it has turned into hyper-inflation under the sleepy eyes of both investors and the financial press. Why the investment community relies upon the central bank liars and the financial press dimwits is proof of national stupidity in my view. Intelligent people are wondering if QE3 will emerge when QE never ended!!"

If you find this confusing, thats because it is. What ever the Fed is doing, the real money supply (thats the stuff spent from day to day) is shrinking. The supply of bank money is what QE increases, but this doesn't mean a definite increase in the number of US dollars in circulation because somebody needs to borrow them before they enter the real US economy.

Mist42nz,

Yes this was a concern of observors of political-economy since the 19th Century and continuing into the 20th Century with iconoclastic economists such as Frederick Soddy.

To illustrate the inexorable force of usury capital unchecked, Marx poked fun at Richard Price’s calculations about the magical power of compound interest, noting that a penny saved at the birth of Jesus at 5% would have amounted by Price’s day to a solid sphere of gold extending from the sun out to the planet Jupiter. [11] “The good Price was simply dazzled by the enormous quantities resulting from geometrical progression of numbers. … he regards capital as a self-acting thing, without any regard to the conditions of reproduction of labour, as a mere self-increasing number,” subject to the growth formula Surplus = Capital (1 + interest rate)n, with n representing the number of years money is left to accrue interest.

http://michael-hudson.com/2010/07/from-marx-to-goldman-sachs-the-fictio…

The historical background paper is available today. Well worth a read.

http://idl-bnc.idrc.ca/dspace/bitstream/10625/7278/1/67694.pdf

The fundamental funtions of money are mutally incompatible, which is why humanity has used parallel dynamically interrelated systems, up until the modern era. Credit and commodity money have existed side by side throughout history, though their preeminence relative to one another have shifted throughout the Ages. From the 15th Century commodity money displaced the use of credit, because merchants of the era, were exploiting market imperfections by virtue of monopolistic practices (Crown monopolies), and capitalizing on volatile demand/supply dynamics due to economic and population growth. They wished to have stable store of wealth, though they ended up paying for it, with 100 years of unprecedented inflation.

"This is particularly the case about the 16th Century Price Revolution, which is the one associated with the first clear expositions of the Quantity Theory of Money (Arestis and Howells, 2001-2). But and in general historians stress the real causes of inflation based on neo-Malthusian models that emphasize demographical forces, in which money is endogenous

Prices increased, still according to Tooke, as a result of bad harvests, the depreciation of the external value of the currency that increased the price of imported goods, and higher interest rates, which led to higher financial costs. Reversal of these trends in the post-Napoleonic War period, hence, explains the deflationary forces in action, and the end of the price revolution."

Making an analogy and then drawing conclusions based on the analogy is unlikey to prove correct. If it was a battery you would run out of energy, in the battery for a start.

Thermodynamic laws only work because their underlying physical quantities follow conservation laws. Money does not follow a conservation law, banks create it essentially on demand, so money doesn't follow a conservation law. That is the beginning and end of it.

What's tomorrow?....oh it's Friday....must be due another bank survey that points to growth and recovery...hey anyone know the metal value of all the euro coins in circulation....!

So, that's actually a "Top 14" today, Bernard ... ?

not pretty indeed. Thats what hapens when you have bubbles.

Adelaide is not as bad, but not great. But there's a fair amount of investment - massive new hospital, mines etc. I did hear today that house prices here are down 5.5%. Thats one thing the aussies are behind kiwis on - realising that house prices do fall!

Interesting the stats about construction employing (directly / indirectly) 8% of labour force in Melbourne. Wonder what it was at the peak in Auckland, fairly similar I would have thought. Thats why it surprises me that Auckland's economy hasn't tanked.

Whats keeping it up? What are the mainstays of Auckland's economy???

Finance?

Construction?

Tourism?

Hospitality?

Retail?

If someone can tell me how these sectors will prosper in the coming year, and support house prices, I'd love to know, with the international circumstances! Moving forward, as Aussie and China weaken on the back of Europe's problems, and there is very little opportunity to cut the OCR (unlike Aus where there is sitll plenty of room to cut), where does NZ go?

according to ASB Auckland is going strong....

http://www.stuff.co.nz/auckland/local-news/6060881/Auckland-economy-still-leads-the-pack

No. 1 - My night, month and maybe my year has been made.

Catchphrase for 2012, "I want you all fired."

LOve it.

WESTPAC DEEPLY WORRIED.

Whilst westpac in nz seem to be on drugs and in economic lala land, their international colleagues are deeply concerned. Front page of the Australian newspaper has a london based westpac economist sounding very bearish saying the global events 'should scare the living daylights out of us'

do you have a link for the article please

The Australian has a Paywall on some/new articles. There's an idea for BH.

Why is a paywall an idea? Im not aware any have worked.....the whole idea behind the Internet is instant and anywhere information....you cant hold a monopoly rent when you have no gates....

FT etc are doing it.....I dont read them any more.....there are lots and lots of alternative free sites to gather info....and many of them are less biased politically than ones that think they deserve it....

regards

I didn't say it was a good idea - just a possibility. It can work by paywalling new & big stories thus encouraging more paid subscriptions.

Yes, agree - it simply sends readers/surfers elsewhere. All the main providers wuld need to execute their paywall simultaneously.

But then, you do have to admit we are enjoying this site, interest.co.nz, for free - for entertainment & even for financial advice. And BH has costs - webhosting, web development, staff writers, office expenses - which we all enjoy for free.

No - I am not being paid by interest.co to act as an undercover lobbyist! Just an idea .....

However this is really an aggregation site more than anything else......and there are as many interesting links from contributors as written by BH's team....if not more...the chart data though is interesting......

regards

Yep, with a paywall the majority just won't bother to read the articles behind it, and that impacts on the views for advertising. Registering and faffing with credit card numbers sets the arseache threshhold too high for most people.

NZ Herald tried having paywall on selected articles and it was a disaster. What kind of lunatic would pay actual money to read Garth George's idiot dronings?

exactly....

regards

Im not so sure its of much value.....eg

MINING billionaire Robert Friedland had some comforting news for the industry yesterday, declaring that Australia did not need to worry about the financial travails of Europe and that global warming was much more desirable than global cooling."

So....laughably, totally wrong.....

http://www.theaustralian.com.au/business/mining-energy/tax-aside-austra…

Interesting that the right wiing press seem to be convinced a paywall is the way to go. I wonder who actually pays the subscriptions, is it the CEOs who read such stuff ou fo their own pockets or do they "expense" it.......

So they maybe paying for a biased view of the world that will do them harm.....interesting....why not pick up a bible and chant in the corner..........

regards

"4. The last refuge to which a scoundrel clings - Patriotism. So goes the Bob Dylan lyric."

And once again Samuel Johnson rolls over in his grave and wonders why he even bothered.

Top work, Bernard...you're a credit to journalism.

Great top 10.....why do I need nightmear on elm street when I have BH's top ten.....glad I didnt read it last night...."inheritance" is way less scary.

;\

regards

If the likes of even me could see this end game a year + ago....why couldnt govn leaders.....

regards

Yes a fine top ten Bernard ...one for the file as coming events pan out....to reflect upon as it were..! Although GBH won't be altogether happy with the tone ,I'm sure he will appreciate the effort.

Happiness !

..... it's just Bernard's gloomy-guss spin on everything that bugs me , Count ...... for example , instead of reporting that Europe is staring into the abyss , one could counter that Europe is being dragged kicking & screaming back into the harsh light of reality . They're wailing 'like stuck pigs , 'cos the game is up . The bloated bureaucracies of the EU have failed , utterly , as we knew they would . The onerous 25 hour working weeks , the platinum pensions for life & wife , the retirements at age 40 , the subsidies for farmers to produce sweet feck-all ....

.. And the Germans don't wanna give up on a game rigged in their favour , surprise that !

The unwinding of the Eurozone may be a tadge ugly for a year or three , but we'll all benefit in the longer term , when Europe has un-merkelised itself .

And that is a fair interpretation too GBH.....a bit of leveling required to put the new foundations down.

What would need to change even if a return to seperate currencies would be the Fractional Reserve Banking doctrine in the light of what has beset them ...kicking and screaming indeed.

The too big to fail one size fits all must be addressed head on....in order to look toward any sort of sane recovery something has to give ...or in this case be allowed to fail.

And fail in a most spectacular way.....!

And the sun will come up and someone will have krispies and toast and maybe some juice for breakfast......and so on and so forth.

Hubbard Managed Fund Statement statement from Grant thornton as at March 2010 about 420,000. Now (bullshit removed) 178,000.

My theory is tha AH had a personallity disorder. He saw his investors as an extention of himself (as narsissists do?) and got off on the adoration. He was free to tell porkies, as he is only telling them to himself.

Strange but this is a debt issue not liquidity...

"One reason is to make sure that the banks have the liquidity they need to stay afloat. A widespread domino-like cascade of bank failures would be disastrous and this provides insurance against that possibility. In addition, even without bank failures a loss of liquidity is troublesome. As liquidity dries up, interest rates rise and the loans that businesses and consumers need become harder or impossible to get. That can have a large negative impact on economic activity."

http://www.cbsnews.com/8301-505123_162-57333882/will-the-feds-move-to-h…

Yet we see rally everytime the most in-consequential plus happens....to me you (a private "investor") only plays a "game" like this when desperate and there are no other options.....like a double or quits gamble ....yet they can take their money out while ahead....wierd...

regards

You will notice that the paper newspaper - e.g. NZ Herald has more stories then the online site - the online site slowly adds the extra items from the paper version over 24 hours - so there is a subtle difference in that blended model.

So, purchasers of the paper version get a slight reward for the $1.90

If thats all they read....

regards....

So the ECB etc have been consistantly wrong, either that or afraid to admit it....they had the opportunities to fix things 3 yeasr ago....and no one did, that to me is negligent in the extreme, almost treasonious.......

oh and austerity was going to work...and the euro is safe....

"One cut after another: many economists say that there is a clear risk of deflation. What are your views on this?

“I don’t think that such risks could materialise. On the contrary, inflation expectations are remarkably well anchored in line with our definition – less than 2%, close to 2% – and have remained so during the recent crisis. As regards the economy, the idea that austerity measures could trigger stagnation is incorrect.”

Incorrect?

“Yes. In fact, in these circumstances, everything that helps to increase the confidence of households, firms and investors in the sustainability of public finances is good for the consolidation of growth and job creation. I firmly believe that in the current circumstances confidence-inspiring policies will foster and not hamper economic recovery, because confidence is the key factor today.”

"Will you say whether the euro itself is at risk?

“The euro is a very credible currency. It has kept its value from the start in a way that is remarkable and has ensured price stability for 11½ years. Average annual inflation in the euro area over this period has been 1.98%, in line with our definition of price stability, and this is the best result recorded since the Second World War in all of the euro area economies. A currency which safeguards price stability is a major asset in the eyes of investors, both domestic and international.”

Is the sovereign debt crisis worse than the sub-prime crisis?

“I will say that the situation we are experiencing at the moment, in Europe and in the world, was triggered by the financial crisis, which had a very significant impact on the deterioration of public finances everywhere. It is a global phenomenon. I am confident that governments will manage to overcome these difficulties.”

http://www.ecb.int/press/key/date/2010/html/sp100624.en.html

great.........

Re the hedge fund letter ... "Hard to know if he/she is real" ... but easy to know that he/she doesn't know what he/she is talking about.

The financial system is broken, but it's not the hedge funds that are the problem, it's the TBTF banks and their central bank enablers. Many hedge fund managers were sounding the alarm and not listened to back in 07/08 and still today.

The point about having access to financial instruments that the public don't have access to is a red herring because the public would have no use for these instruments anyway and none of them guanrantee any sorts of great returns, they are only as good as the manager using them.

People shouldn't be angry at hedge funds, just because some of them were competent and made money. They should be angry at the incompetence of the TBTF banks, central bankers, politicians, pension funds, ratings agencies etc etc.

While the sentiment of the letter is justified, it's totally mis-directed and naive (sums up the occupy movement).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.