Here's my Top 10 links from around the Internet at 8 pm today in association with NZ Mint.

We welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read today is #3. Spain's bailout solves nothing.

1. Just wipe out the debt - I never thought I'd see the day.

The FT has just reported on the idea of the Bank of England simply deleting the government bonds it bought with its money printing.

This is effectively debt forgiveness on a massive scale.

Some might even call it a clever type of Debt Jubilee.

Neil Collins writes that it's one way to successfully reduce Britain's crushing debt load.

It need not sell its £325bn pile of gilts and in practice it can’t. Were it to try, the market would demand a ruinous premium. In 1976, the UK government was obliged to pay over 15 per cent for 20-year money.

So why not just pulp the certificates (or their electronic equivalent)? This heretical thought has occurred to Jim Leaviss at M&G, who points to its magical impact on the UK’s public finances. The debt would shrink from 63 to 41 per cent of gross domestic product, creating financial headroom for all those lovely infrastructure projects.

Whisper it quietly, but something like this is already happening. The Chinese can’t spend their US T-bill mountain; if they tried to swap them for meaningful amounts of real US assets, the rules would be changed, just as they were against Bunker Hunt.

Debt destruction is inevitable across the west, whether by default, inflation, or some form of forgiveness, before growth can resume.

Writing off the debt in central banks may be intellectually uncomfortable, and Zimbabwe’s hyperinflation shows what can happen, but Mr Leaviss may have hit upon the least painful way out of our economic slough of despond.

2. Hoarding - CNBC has a useful article showing who is buying all these US government bonds. It's not necessarily the Chinese or the US Federal Reserve.

Wealthy individuals and 'Mas and Pas' are the buyers. This is the problem. So much capital is parked, hoarded in government bonds by fearful and elderly investors or fearful and profitable companies. Apart from in the PIIGS, bond yields are at record lows.

We have a problem now with too much wealth concentrated in the hands of wealthy older people and corporates who are unwilling to use that money to invest in creating new companies and jobs.

"The conventional view is that 10-year Treasury yields have been pushed down to 1.5 percent and 10-year (Treasury Inflation Protected Securities) yields to -0.5% by the actions of the Federal Reserve and the safe haven demand from foreign investors," Capital Economics said in a research note. "The reality, however, is slightly different."

The demand among average investors has swelled so much, in fact, that they bought more Treasurys in the first quarter than foreigners and the Fed combined.

Households picked up about $170 billion in the low-yielding government debt during the quarter, while foreigners increased their holdings by $110 billion.

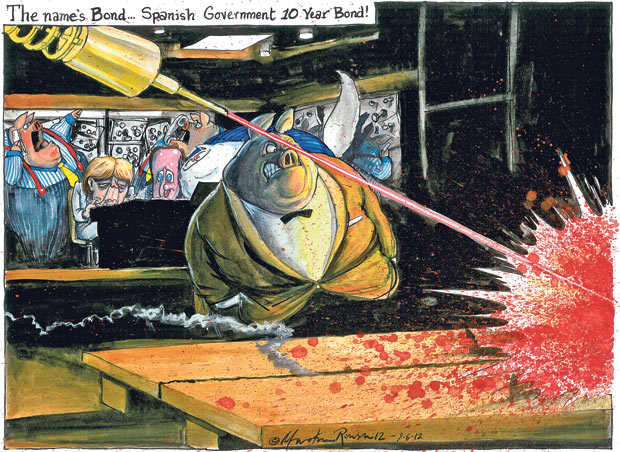

3. Nothing is solved - I can't quite understand the euphoria now racing around global stock markets after the weekend deal by Europe's rescue funds to lend 100 billion euros to Spain so it can then re-capitalise its banks.

The basis problems are not solved. Spain has too much debt. All this has done is add yet more debt to the pile to buy the economy time to start growing and pay it off.

But as we've seen, the sheer weight of the debt is slowing growth to the point where the debt is obviously unsustainable. Austerity programmes, which Spain has just started, make it worse.

What is really needed is for the debt to be written off. But that would be financially painful for the European Central Bank and voters in Spain.

The entire Global Financial Crisis seems to be an exercise in passing the debt parcel until the music stops. The unsustainable solution is some form of Debt Jubilee where the debt is forgiven and the highly financialised global banks are broken up and stopped from using their banking licenses to gamble in their own right on markets.

Here's the FT with an editorial saying why Spain is not saved:

The key dysfunction of the euro, however, is not addressed. Rather than sever the lethal embrace between stressed sovereign debt and weak banking systems, a cash advance to bail out banks with taxpayer funds adds to the burden of Madrid’s public finances. If the state of Spanish banks is much worse than expected, this action could amount to lending the country rope with which to hang itself – repeating the Irish mistake.

Until this prospect is banished, markets will not regain confidence in Spain, despite the strengths of its corporate sector, its structural reforms and a speedy macroeconomic adjustment. What is needed are bank resolution rules that cap taxpayer exposure. This means writing down shareholders and converting uninsured and unsecured debt into equity when banks cannot raise the capital they need.

4. 'The run on the periphery will continue' - BusinessInsider reports here the views of Barclays' Antonio Garcia Pascual on the problems in Southern Europe

Should market events accelerate the ongoing capital reversal (and a Greek exit remains a material contagion risk), given the contagion to other weak economies (eg, Italy has been trading at a spread versus Spain of c.30-70bp for 10y bonds), it would be unlikely that the financial assistance could be circumscribed to the banks only or even to Spain alone. And for that, there are no sufficient rescue funds readily available (ie, for multi-year full-fledged programmes for Spain and, depending on contagion dynamics, for Italy as well).

So long as the euro area does not remove the tail risk of potential FX redenomination for periphery countries, medium- and long-term investment commitments by foreign capital (or even domestic) are unlikely and that creates a growth disadvantage in the periphery. And without growth prospects, there is little hope to emerge out of the crisis.

5. Shoved down the queue - Bloomberg reports I\investors who thought they were first in line if anything went pear-shaped in Spain are now waking up to the realisation they have been usurped.

Investors holding bonds issued by Spain and its banks will probably rank behind official creditors in the queue for payment after the nation asked for a bailout of as much as 100 billion euros ($125 billion).

“This is state financing, and the risks of an equity injection into the banks will stay with Spain,” said Alberto Gallo, head of European macro credit research at Royal Bank of Scotland Group Plc in London. “Spain needs a systematic restructuring of its banking system, which could entail haircuts to subordinated bank debt. Official lenders on the other hand are likely to demand seniority.”

If the cash were to come from the ESM, its treaty provides it with preferred creditor status, junior only to the International Monetary Fund. The EFSF isn’t explicitly a preferred creditor, prompting Finland’s Finance Minister Jutta Urpilainen to demand collateral if the facility were used to advance the money. Even so, the Greek example showed that official lenders aren’t willing to accept losses, preferring to force private bondholders to take greater writedowns in a restructuring.

6. What the deposits are doing - Gordon Chang writes at Fortune about China's decision to ease monetary policy last week and why it may not be enough to boost the economy. It turns out some of the banks did not pass the cut on to term depositers, fearing an outflow of funds.

Just about every analyst says that Beijing has plenty of firepower to stimulate. “China again has space for a forceful response if necessary,” said the IMF’s David Lipton last week. That’s not quite right. Beijing has to drop deposit rates when it cuts lending rates to maintain bank margins, and that is in fact what the central bank did on Thursday, reducing the benchmark one-year rate for deposits by 25 basis points.

Surprisingly, the country’s five largest banks did not go ahead and drop their deposit rates, instead keeping them the same by setting them at the maximum allowed under new liberalized rules. Why did they do that? Probably because they were worried about triggering outflows. In April, more than $100 billion in household deposits fled the banks, undoubtedly due to negative interest rates.

7. 'We are not Uganda' - El Mundo reports Spain's PM sent a stunning text message to his Finance Minister during the fevered talks over the weekend to agree a bailout. HT BusinessInsider

"Resist, we are the 4th power of the EZ. Spain is not Uganda."

Translation: We're a major power, not some random IMF-case banana Republic.

The followup message (according to Google translate) "if you want to force the redemption of Spain will prepare 500,000 billion euros and another 700,000 for Italy, which will have to be rescued after us."

Bottom line: hold out for something good. We are powerful, and if they don't give in, the whole thing will go down. It will cost Europe 500 billion if Spain goes bust, and then another 700 billion if Italy goes bust.

9. Some people have too much money - FT reports a firm has started in Britain as a Wedding Proposal planner. They charge you to plan the proposals.

I can sort of understand Wedding Planners, even if it's a tad indulgent.

But Wedding Proposal planners?

Comment with your examples of people who have too much money.

10. Totally Jon Stewart on Mitt Romney's wealth. And John Kerry's wealth. Hilarious in a gotcha sort of way.

9 Comments

Re Item 9 Maybe Bernard Hickey with own subscription to FT online (4 links in 1 Top 10)?

Regarding #9, how about people who buy Swarovski crystal bandages?

Should the UK use it's Bank of England cash to pay of debt?

I have just had a look at the british Budget figures they spent 43 billion pounds servicing the debt.

Total debt is 1278 billion pounds.

The amount the bank of England has is 325 billion pounds. Using this would reduce debt by 25% and save 10.75 billion pounds.

Their deficit is 90 billion pounds so they are about 11% closer to a balanced budget.

Now total debt is 85% of GDP in 2011 this step would reduce debt to only 63% of GDP.

In addition the Bank of England would make 10.75 billion on these bonds and would need to replace this revenue.

While this step would give the UK more breathing room and opportunity to reduce interest rates this is not a solution to the problem to further austerity. Of course they could print more money to get rid of the debt but this would increase inflation.

This guy thinks they should do more infastructure projects what is he surgesting and doing so can easily mean the savings get put into projects of dubious economic value. (All in the name of national interest - I.e. winning the next election.) And it would take time for these projects to get started due to planning and contracting rules (Just in time to help a Labour Government perhaps?)

This idea could help but it is no solution to the problem, the budget still requires balancing.

Ok my sources were Wikipedia - but then I don't want to have to look through piles of unhelpful pdf files in a british Government website trying to find the debt numbers amoungst the politcal wiffle woffle. I am unsure if FT references are correct they look different to the numbers I have found.

I am always puzzled when people think of inflation as only printing money.

To have inflation there needs to be increase in prices and wages.

Is anyone on this site expecting any grow of his/her salary along the numbers that monies are being printed.....

Prices rising are a consequences of inflating the money supply (inflation) relative to goods and services in the economy.

Without an increase in money supply, should prices go up in some areas, it just leaves less money circulating in the rest of the economy.

"Sorry, I seem to have got lost. I was after the bailout department; I'm big, I owe a lot of money on my credit card, and I want someone to give me a lot of money but not to ask any questions about what I spend it on."

Interesting comment on china,

"I start this analysis with China being a kleptocracy – a country ruled by thieves.

8><--------

(a). The children and relatives of CPC Central Committee members are amongst the beneficiaries of the wave of stock fraud in the US,

(b). The response to the wave of stock fraud in the US and Hong Kong has not been to crack down on the perpetrators of the stock fraud (so to make markets work better). It has been to make Chinese statutory accounts less available to make it harder to detect stock fraud.

(c). When given direct evidence of fraudulent accounts in the US filed by a large company with CPC family members as beneficiaries or management a big 4 audit firm will (possibly at the risk to their global franchise) sign the accounts knowing full well that they are fraudulent. The auditors (including and arguably especially the big four) are co-opted for the benefit of Chinese kleptocrats."

http://brontecapital.blogspot.co.nz/2012/06/macroeconomics-of-chinese-k…

regards

Bank bond holders and shareholders in the western world have already had their debt forgiven by tax payers.

My understanding is that, relative to everybody else in Europe except the Germans, Spains main problem was an enormous real estate bubble that collapsed leaving behind terrible unemployment and a bankrupt banking system.

Passing the banking problem on to an already underwater public sector is a repeat of the Irish mistakes. It needs something a bit more radical that leaves most of the problems with the people who took the risks.

Cant the government of Spain let the insolvent banks go , just pick up the assets and put them into a new bank which starts trading immediately. They could borrow some money from the ECB to provide a capital base and just start again using the same infrastructure with a different name. Tax payers would be guaranteeing the new bank but at least they would get the benefits of any profits , and there should be some. Bond holders, shareholders and depositors would do their dough but that is what happens when a business collapses.

As long as there is a functioning bank left so business can go on in the world at large who cares who owns it?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.