By Bernard Hickey

Last week's column about the need for an intergenerational wealth and debt deal sure struck a nerve.

I was swamped with comments and emails from outraged baby boomers telling me to stop indulging in scapegoating and blame-gaming.

I was told to get back in my box with the rest of the lazy, selfish Generation Xers and Yers who were whingeing for no good reason.

I was told the youth of today never had it so good with all their Xboxes and iPads and 5% interest rates and should just buckle down and save hard like they did.

I was told the baby boomers had to cope with 20% interest rates and washing machines with wringers in their day and had to work harder and longer for less.

I was told they had worked hard and paid taxes all their lives and they were 'due' their pension at 65.

I was told they deserved their wealth and I was an ungrateful stirrer even suggesting these gains should be clawed back.

Here's a nice summary in this response to the article on NZHerald.co.nz from KC in NZ:

"Get over it Bernard. Why should anyone that has worked hard to get what they have give it up for a generation that doesnt want to work for it?"

It's worth rebutting the rebuttals because I think many people don't understand how our tax and welfare systems work, or what happened during the last 10 years in our property market.

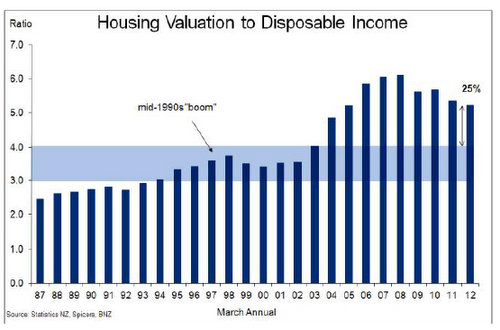

Firstly, the argument that it was just as hard to buy a house in the 1980s and 1990s as it is now. Productivity Commission figures show the national house price to disposable income ratio rose from around 2 in 1980 to around 3 in 2003, before doubling to almost 6 in 2008. It is now around 5. Treasury figures show the percentage of gross income needed for an average mortgage payment rose from around 35% in the mid 1990s to a high of 65% in 2008 when interest rates hit 10%. It is now around 45%. See more on home loan afffordability here.

Essentially, home buyers now paying almost twice as much to buy a house as they were in the 1980s and 1990s, relative to incomes. The relative costs are much worse in Auckland.

Property is much more expensive for first home buyers now than in the 1980s and 1990s when baby boomers were buying their first homes. First home buying would be impossible for most, particularly in Auckland, if interest rates were not now at record lows. It also requires both income earners in a home to stay working. The stay-at-home mum of the 1970s and 1980s is not an option now.

Secondly, the argument that baby boomers worked hard for that property wealth and don't deserve to have it taken off them. Reserve Bank figures show the net equity in housing wealth more than doubled from NZ$203.5 billion in 2002 to NZ$456.7 billion in 2007. Property owners' wealth rose the equivalent of more than 125% of GDP in 5 years.

That wealth fell from the skies.

It was not earned or built.

House values did not improve by NZ$253.2 billion because a few decks and conservatories and double garages were added. A housing boom fueled by a lack of new houses being built, a migration surge and an astonishing amount of easy lending created this wealth out of thin air, or more accurately, from indoor-outflow flow of thin air.

Finally, the argument that baby boomers paid their taxes and are 'due' their pensions and 'free' health care.

New Zealand has a pay-as-you-go pension and health care system. The baby boomers' taxes paid from the 1980s until now were used to pay for the relatively small amount of pensions and healthcare incurred by their parents, who fought and died in a few wars to ensure their kids could live comfortably in freedom.

The baby boomers' pensions and healthcare will be paid for by Generations X and Y and anyone else still paying taxes over the next 30 years. We do not have a European or US style social security system where insurance type payments are paid, saved and then withdrawn to pay for the retirement costs of those who made the payments.

I'll leave my final word to Stephen, a listener to a Radio NZ interview with World War Two veteran Bob Wood a couple of weeks ago.

"As his generation passes, I consider it important to acknowledge how great his generation was. They had a childhood marred by The Depression and a youth lost at war. They were educated by a generation almost lost in World War One. Social commentators have described Mr Wood's generation as the best generation, deservedly so. An acknowledgement of what they did is why I and others of the younger generation have been going to Anzac Day parades in recent years. That generation's children, the baby boomers, come across as shallow and self-absorbed in comparison. They dismantled the welfare state set up by the best generation and even disrupted Anzac day parades in the 1970s. They labelled these poor traumatised men as war criminals. I would like to say to the Bob Woods -- thankyou, thankyou, thankyou."

112 Comments

As a member of the powerful BB generation I think we deserve a good bashing. The NZproperty industry is distorted, greedy for decades and far to dominate in comparison to other industries.

Fundamentally - looking into the current worldwide circumstances - we failed miserably creating a better world after the war. I cannot believe how many people here are ignoring the facts.

Our generation accepted unethical, greedy and corrupt behaviour – almost in silence.

The increasingly negative impact not only directly on us humans, but our environment and nature are visible everywhere.

What’s left is a big mess on many fronts, which the next generation has to "clean up" – almost unbearable and prohibitively expensive.

…and for once BB’s should stop and tell their grand- children good night stories – otherwise we never see most needed changes.

Wrong Bernard. Sure you got some unfortunate and silly responses Bernard. But mostly you got some quite reasonable ones. It's an easy out for you to select some of the silly ones and argue on that basis. But it's not acceptable to act 'hurt' in an attempt to promote your position.

I followed that discussion closely. I am seeing the intergenerational strife that is being promoted as meeting the same need as blaming outsiders. It's too like 'red under the bed' - 'hairy arms of unionism' and 'Germans roasting babies.'

Try a little harder Bernard. You can do better than this.

Wolly's reply on this thread says it all. Post at 22 Jul 12, 6:03am

==== quote from Wolly's post ===

Now the rebuttal.......an appropriate thread because the bubble is Bernard's problem not the older generation who upset him because they have pension rights, if they live past 65!

Today in the Herald Bernard trots out his 'rebuttal' to the BB comments aimed at his belief that they are the cause of the problems facing gen X and Y. His entire argument stands on the high cost of housing for X and Ys.

What he fails to see...and therefore fails to tackle...is the real reason for the bubble existing in the first place. Bernard would do better to look at the role of the banks in NZ and of the govts and the RBNZ over the last two plus decades....indeed since the time the great credit based splurge began.

Yes the oldies today took advantage of the easy credit pumped into the economy by the banks with the full support of the useless and gutless govts...let's forget about the RBNZ because they are just an arm of govt. To that extent he can blame the BBs of today but only to that extent.

Now I will sit back and wait for Bernard to rebutt my point...or to embark on a mission to bring to the attention of the public, the dirty little banking/govt secret that in my opinion holds the key to the economic disease that is stuffing this country.

Why should all Kiwi have to accept that banks have a right to create and sell credit with the full support of gutless politicians, into an economy already saturated with debt, for the sole aim of keeping bubble property prices intact to protect bank balance sheets and bank bosses bonuses, with fat profits every year sent to Australia?...answer that Bernard!

==== end quote =====

Like Wolly I will wait and see whether Bernard will address the real issue or will continue to fuel inter-generational hatred.

Not exactly sure I understand what you are trying to say here.

Perhaps you might be so kind to rephrase

Bernard, your heading has a graph for real house prices.

You quote house buying ratios - against real wages.

Please in all fairness now show us the relevant graph for real (inflation adjusted) wages for the same period.

Got ya! Since 1980 the actual rises were tiny. Since 1985 the wealth 'effect' was based on debt.

Your fabled ratio is based on fragmented fact.

Got ya!

Got ya Bernard

Its the low wages since 1985 that cause the problem. Not the property values.

Proof of my point is the fact that in 1975 a household could live off a tradesmans wage. Since 1985 two incomes have been needed to live a similar lifestyle.

Now a typical family needs three incomes (Working for families) just to get by.

If the housing costs are the reason - how do you explain the record low outgoings due to the current interest rates? Cheap!

Got ya Bernard!

The bottom chart shows house prices to disposable income. That tells the story just as well.

cheers

Bernard

The reason Anzac day celebrations in the 70s attracted protests were because of the support of the establishment, mainly made up of these "poor traumatised men", for the insane war in Vietnam.

Yes BH: Look at the data: 30 plus years plus of credit funded everything.

See the way asset prices/(values??) have gone up compared to the preceeding 30/50/100 years.

Look at Japan to see how things trend (bear) down, - sure occasion bull runs, within the drive down.

Looks like being in the market and long for the long haul will do capital, more a sense of timing needs be considered.

When some finance/prop/lender type sells you with :.... because it always goes up" its time to leave the room..

And: highest risk free yield you get now is paying down the mortgage(s)..

Cactus Kate has her own take on Bernard's smoke screen

==== quote from Cactus Kate ===

The newspaper editors sense impending circulation rises from those smart enough to read but not smart enough to think and have conjured it up for the benefit of their banking and real estate advertising clientele.

==== end quote from Cactus Kate ===

ask Cactus Kate. I'm sure she will tell you.

mist42nz,

Re

First up: Accusing BH of emotive discussion, then promptly launching a monotribe of same, with no supporting reasoning, is very poor form and lousy for any kind of analytical process.

Really? So you are agreeing that BH launched an emotive diatribe? And you are agreeing with the general proposition that BH's lack of supportive reasoning is very poor form and lousy for any kind of analytical process.? Just saying that is one way you could interpret your post.

I quoted one small part of that post by Cactus Kate. I thought she pretty much had that part of the article right.

In general terms, I disagree with a large portion of Cactus Kate's world view. And I agree with certain portions of BH's. But I totally disagree with BH on this particular thread.

My prediction is that this meme, if he continues promoting it, will lead to violence. And not to solutions.

I also disagree with GBH on many of GBH's comments. However, I agree with his view that

===== quote from GBH =======

... in this blame game , which Bernard drearily drags out everytime he has nothing sensible to write about , the " baby-boomers " are spoken of as if they are an exclusive club , a band-of-brothers , with special handshakes and a hearty " well met my fellow boomer " .....

We don't exist in isolation , Bernard ....... and we don't all vote for the pork-barrel politics which has ruled the country continuously since 1999 .....also , I'm sure that a plentitude of traditionalists & gen X's voted for the seriously dopey welfare policies that Michael Cullen & Bill English have introduced & supported ....

===== end quote from GBH =======

I know that in the 1960's the LVR was waaayyyy different to what it is now.

If you have taken the time to read Steve Keen's analysis of the change in LVR from 1960's through to current then you might begin to understand where I place a large part of the blame.

In addition, have you had any look at the politicians responsibilities in all this?

- Changing immigration rules to allow high net worth individuals in so that the property bubble can be propped up. For example, have you had a look at the property purchases that James Cameron has executed in the Wairarapa. Gee, that was a success for any gen-x, gen-y in that market. Bit hard to compete with James Cameron's buying power. But hey - he is one of those dastardly Baby Boomers isn't he?

- Immigration policies clearly intended to continue high growth in Auckland. Rodney Hide stating another 1 million in the next 30 years. <sigh> Auckland used to be a nice place to live. Sadly the traffic is turning it into just another congested crap hole.

- No mention of the hot money coming out of China into Auckland's property market.

Politician's abdicated in their entirety any oversight of the Reserve Bank and the banking system. There is still a mind-set that the RB Governor is all seeing and all knowing and absolutely deserves his 600K salary. The evidence over the past couple of decades indicates to me that the RB does not know what they are doing. And if they do, then shame on them.

Bollocks is what I say. Both to BH's theme here. And to a large part of the governmental decisions over the past 40 years. And to the RB's neo-classical economic's stupidity

But lets just ignore all of that and blame one demographic. I have followed interest.co.nz for 4 years or so.

At the moment I am feeling a deep sense of disappointment at the lowering of the intellectual standard.

..... we could , if we chose to , line up our current crop of politicians and ask them directly , why are they refusing to listen to the Retirement Commissioner .....

Much of that which Bernard wails about has been canvassed many times over the years by the RC , and has been completely ignored by the government of the day , both Labour and National ....

..... various independent economic think-tanks & taxation commissions have also been set up by successive governments , and their reports have been cast aside too , written off as " ideological burps " , by the very finance ministers who solicited them .

You do realise that retirement is always paid for out of current economic productivity don't you? This is kind of obvious, as people who are retired are not productive (BTW, they are only un-productive in GDP terms) so they are purely a drain on GDP (again GDP a dubious measure of productivity).

The issue with the government books which you are pointing two should hardly be conflated with this fact.

So in effect they in the past and even now have made the assumption that there will be an economy to do that and that things like population etc are neutral....when in fact these are all diabolocal misnomers. The Cullen fund at least was an attempt to deal with the population bulge....

Beyond that look at the state of the private provisioning,

a) Its run by mostly incompetant lemmings who I wouldnt trust to pull carrots let alone get anywhere near my money.

b) Its made the share market into a short term knife fight.

c) Its looking to implode to 10% of its curent value if the Great Depression is a decent indication (and it is IMHO).

Not just the OAP of course, the healthcare costs are set to rocket....ergo given what will be 20 years of economic very hard times I cant see how this will be paid for, therefore it will not.

regards

How about we line ourselves up first, we voted them in. Funny thing butt it seems to be the goal of the right....lets not forget the Cullen fund or kiwisaver.....where attempts to address the future problems.

So we employ second rate wood workteachers, cut throat banksters and career politicos who make a mess, so why are we not surprised its a cluster****.

regards

Nice to see the Hickeys of this world moaning even more.

The shriller they get the healthy the house market must be.

Your complaints are like music to my ears Bernard.

I don't see Bernard's piece as generating inter-generational warfare.

He's just saying house prices are out of kilter to incomes and that's casting a pall over the nation's economic future.

I agree - and it's in large part due to too easy credit combined with the all too human penchant for 'keeping up (appearances) with the Joneses' and 'wanting it all today'.

I think house prices in NZ need to come down further. For NZ's sake and the sake of my children, I hope they do, even though that will make me 'poorer' on paper.

Antz

Yes, I agree, paper money Ive never seen or will see anyway.

It will also be yet another slap in the face of Treasury who need it...we are rich according to them as we have an asset......which is only saleable when you can sell it.....idealogical clap trap and we pay for it....duh.

House price will fall, BB bulge etc alone will ensure it....post peak oil, a second debt driven great depression....all nasty downward effects, even one would do it but all three?

regards

Possibly we need to address the massive oversaving of some parts of the world ( Asia & the oil exporters ) ...... which has led to cheap credit sloshing around the markets of the Western world economies ..... money which has slopped into consumption , unsustainable welfare packages , and house price bubbles ....

..... and take to task those countries ( particularly China & Germany ) who've deliberately utilised a rigged currency system to gut the manufacturing competitiveness of other jurisdictions , such as the USA .......

..... or we could just bring back the age old remedy of defenestration , and biff Bernard the Baby Boomer bully out of his office window .......

Hmmmmmm ?

The points made by BH are reasonable, I am surprised at the vitriol in the comments, both last week and this. They suggest a guilty conscience. To not only fail to acknowledge having the wind at one's back, but to go further and suggest that such luck was somehow deserved is insulting. People who worked far less in life have received far more than my eldest daughter, who graduated first in class from high school, but missed out on grants anyway because the bar was even higher than that.

She worked her way through Uni, earning first in honors Chemistry, getting by in a flat that was actually a slum, but the best she could afford, growing veggies in the less than stellar Dunedin climate to feed herself. She managed her student loan amounts skillfully so that she would not overspend. She never bought anything new, and still after 4 years came out with a $35k debt, of which she already paid back $10k.

What jobs were offered someone of her calibre in New Zealand? Lets see, Speight's and Dulux had some part time contract work in their respective testing divisions. Real nice reward for years of sacrifice, eh? She took one of them, worked til the end of the contract and was offered PhD to work on research, so she is back to UNI, flatting and scraping by.

You people have no friggin idea what you are talking about all set up in your nice sitchies. In the end I won't be crying for you as you find no one lining up to buy your ridiculously overpriced houses so you can get into a private nursing home because there are no funds left to pay for your retirement.

The source of the current crisis is that the older generation cashed out their unearned property bonanza for their own benefit and did not reinvest the surplus. Instead the money has been spent on the regular vacations retired folk these days enjoy. Jetting around the world and buying property, and then you have the nerve to talk about the younger generation squandering their money? Please.

Why did she not go overseas with those qualifications? Plenty of work in petrochemicals or pharmaceuticals etc for well qualified, smart chemists.

I'm sorry, I don't see how this relates to the discussion of job opportunities for young graduates, which are almost non-existent. Again, the level of virtiol reserved for the younger generation who will be expected to deliver on the pension promises for the people trawling this site I find disconcerting. I can't imagine how you could have arrived at the assumptions you have laid out here. They certainly bear no resemblance to the case I presented, and your comments are baseless.

Moving on.. I believe NZ is at a crux point of investment. Too much investment in non-productive sectors (finance, real estate), not enough investment in productive sectors. What will turn that around? For starters, CGT, to move money out of property, and lower lending rates for individuals and small businesses (and I don't mean mortgages) not bailouts for banks. I like Steve Keen's debt jubilee idea, but that's because I hold no debt, so under his plan, I'd have a windfall!!! Ok, now you can all pile on that one!

Exactly! Nicely said and very very accurate of the BS now young people must face. It will not be hard for us gen X's & Y's to get them on side. And believe me, we do feel for them. The 90's was no picnic for us for very similar reasons & we have not forgotten

If you look at the USA its pretty clear that a (useless) degree isnt going to do a lot of good in the future....even good degrees are worth thinking twice on.....

Tell your daughter to bugger off and get a job abroad....she has to look after herself, too many NZ companies are happy to exploit ppl....

regards

I agree that the time of getting a Bachelors degree in 'Commerce' and expecting to be set for life is long gone. The tide is receding in tertiary education and diminishing returns are what we are seeing in the marketplace. I've come to see that for those people who are meant for academia, there will be rewards in the future, but it is not the guaranteed pathway for everyone, and has only been so for a short period.

I wouldn't presume to advise her on what to do next, only she can decide that. I bring it up because if she goes, we all lose. The steady devolution of our economy toward tourism (which is now on the wane and which is arguably a path to poverty as it only produces low wage jobs), and a few lucrative exports points us in the direction of southern Europe's future.

During her undergraduate she did some research on the kiwifruit virus. This stuff is important to us economically. Who is going to solve problems like the virus rapidly closing down the kiwifruit industry? This discussion is just the tip of the iceberg. I honestly don't worry about her, she will land on her feet no matter what, she has already proven her resilience. I am concerned for us as a country, and how we avoid the fate of Greece.

Antz ain't wrong about the overpriced housing. But Millie above gets into the group warfare with a quite senseless vigor. Just stop it Millie. Shame on you.

What is a worry is not that the oldies have money, but how many of them don't have a bean. 20% of people who die right now get a 'funeral benefit' because they don't even have that few thou to get themselves buried. I think that a real worrying indicator.

The kids are having it tough too. Maybe we need to think we are all in this together

It is the end of the Ponzi boom. We are all in the crap. We need to recognise the standard of living we all enjoyed is just not sustainable. Setting up scapegoats might make some feel better but won't produce anything else.

Obviously the article below is not from NZ but it is worth thinking about in the context of this discussion. http://www.marketwatch.com/story/retirees-hit-hard-by-foreclosures-2012-07-19?siteid=nwhwk

" While financial planners often advise people to pay off their mortgage before they retire, fully 24% of households headed by a 75-year-old or older person had mortgage debt in 2010, up from 6% in 1989, according to the AARP report, which cited the Federal Reserve’s Survey of Consumer Finances.

Mortgage debt also increased among other 50+ Americans: 54% of families headed by a 55- to 64-year-old had mortgage debt in 2010, up from 37% in 1989. And 41% of families headed by a 65- to 74-year-old owed money on a mortgage, up from 22% two decades earlier."

Would our numbers look any different? It may be that many BB's are not sitting on capital, they are effectively renting from the bank.

In America mortgage payments are tax deductible so what people do is take out a life insurance policy to cover the mortgage amount owing, in addition to any other life insurance policy they might have, the payments for which are also tax deductible, and when the breadwinner dies the mortgage is payed off. That might explain the high number of over 75's who still had a mortgage as stated in the article.

From the same article:

For one, older Americans greatly increased their mortgage-debt load in the two decades preceding the housing-market crash, with the 75+ age group notching the greatest increase in mortgage debt over the past 20 years.

“This increase partly reflects increased borrowing that was spurred by historically low interest rates and high home values prior to the housing market collapse,” the report said. “It may indicate that the oldest borrowers have tapped their home equity to finance their needs in retirement.”

Historically low interest rates and high home values? Yes, that sounds exactly like NZ.

No KH, not senseless vigor, but vigor which is quite justified. I have a big problem with intergenerational inequity. IN fact, I stand up whenever I see situations which are patently unjust. When young people wake up to exactly what has been stolen from them, then my little rant will sound pitiful in comparison. Be afraid, my friend, be very afraid. No amount of "reasonable discourse" at that point is going to do anything. You could try harder, right now, to put yourself in the shoes if the coming generations and get onside, rather than attempting to justify the inexcusable.

robby217 asks why this talented young person has not fled NZ. Interesting, as this is the crux of the argument isn't it? Advocating more brain drain, leaving NZ high and dry with a shrinking tax base and little innovation. In the long run we all lose for indulging oldies in their wildest retirement fantasies a la un-means tested pension, gold card, high home equity, etc. At some point we are going to have stop sacrificing every other age group in order to appease Grey Power. The war as you call it has been waged for decades, by older generations looting the kitty and leaving the younger to pick up the tab- that is well and truly a declaration of war. We didn't wake up yesterday to find this problem. The systematic policy bias toward older voters has left NZ without a future. Unless it changes up its game right quick.

I take it that you don't vote for NZ First !

... Winnie's gonna be in a pickle trying to dream up ways to buy your vote ...

Do you receive WFF , by the by ?

And yet, Millie, to most BBs it has just happened...

The problem is that the old age pension, when first created, went to a tiny proportion of our population (because people didn't live as long) and then they usually only received it for a few years before dying anyway. So, it was no huge drain on the tax take.

The problem is that the age of entitlement of the pension hasn't kept up with our increased longevity. I suspect eligibility for national super would cut in at about age 80, not 65 or even 67, if we'd kept it more aligned with that proportion of our entire population as at it's inception.

I'm not advocating that the age for super be raised to 80! Just observing how much our expectations are different to those of 2-3 generations ago.

Does anybody have some facts around this (rather than my supposition)?

Antz

For what it's worth , my supposition is that the pension should currently kick in around 70 - 72 years , if it had been indexed for the increasing longevity of the population .....

.... a statistician , someone with skills and an acturial table , may be able to pin-point a more exact retirement age .....

Partially answering my own question above ...

"People aged 65-plus reached 2.1 percent of the population in 1891 and 3.8 percent by the 1901 Census." (sourced from here: http://www.goodreturns.co.nz/article/976486047/super-history-nz-s-super-system-unique.html)

1898 was when the old age pension was first introduced - it was income tested, asset tested, set at about one third of a working man's wage) and might be received "upon application in a public court session"!

By the 2006 census, 12.3% of the population was aged 65 plus (sourced from Stats Dept website).

In 2006, those aged 80 and over comprised 3.3% of the population (my calculation based on Stats Dept info).

By 2011, the 80 and overs comprise 3.5% of the estimated population (again my calculation based on Stats Dept info).

I think it's likely to be closer to 80 than 72-73, GBH, provided one compares with the admittedly limited pensions of 1898. Your estimate might be closer to the truth if one compared with the 1938 legislation.

Antz

no relationship to financial means and no consideration of this obvious on a finace blog... too funny!

Yes but Millie, the reality is jobs for chemists are more scarce in NZ than globally, and unless your daughter also has entrepreneurial skill+capital to perhaps start a business in NZ it is always difficult straight from university.

I'm not saying I disagree with some your sentiments. Many NZ companies seem to have this mentality where they are unwilling to train people, poor at planning for change or succession, yet expect experienced workers to miraculously appear.

I'm not saying go overseas forever but there is certainly the opportunity to learn from the best companies in the world with regard to areas of the chemical sciences etc. Hopefully these people who leave and return later will be able to bring back skills and expertise as well, I don't think it has to be a one-way street.

What price would houses, our currency and our interest rates for savers be now if most of the funding for mortgages had to be sourced locally rather than from offshore investors.

What about this for an idea. Remove capital gains tax from Share trading and investments in New Zealand and see if that helps the housing affordability crisis.....

So Millie, the not-so-subtle-anymore subtext of your message above leads me to ask:

At what stage are you and fellow co-horts of Adolf Hickey at in planning your first konzentrationslager for over 65s......

Not that old yet, but I'm guilty of having worked and managed to pay off one house (which if I sold would only replace a house of similar state).

Guilty too of holding down a job still, and reading your vitriol about me and others like me, I now have an inkling of what a working class Jew in 30s Germany must have felt like. The anti BBer Nazis will come for me sooner or later, but I'm not rich enough to flee.

Somewhere like Ohura perhaps where the cold will kill us off more quickly?

Ummm... probably a rather a silly comparison to make really, Anne. I think someone venting a little frustration at the status quo is hardly going to don jackboots and start exterminating baby boomers...

Wind it back a little... it's starting to look like '... thou doest protest too much....'

And by mentioning Nazi's you thereby invoke Godwins law and bring your role in the discussion to a close.

Millie is clearly not advocating any sort of threat against you and yours - She is telling you of the threat that she sees becoming a reality if things don't change. I'm in the BB age group and I am very concerned with intergenerational inequality. I had free education, I had a job when I left work, I owned a house most of my life.

I know I was lucky - and was surfing a wave of cheap energy and booming economies rather than being any cleverer, or more merited than this current generation.

The BBers simply by being a large demographic have had the priviledged position of being a voting majority through most of their lives. They've therefore elected pollys who give them what they want, Child benefit when we had kids, travel perks now we are retired.

So when the majority consistently stacks the deck in their favour - Shouldn't they be worried when at the end of the game they suddenly find they no longer hold all the cards?

I can see the warning signs - can't you?

Godwin. LOL. Wasn't me who said 'be very afraid' to oldies as a group. Nor was it Anne.

And the to the representaton that it was a warning not a threat. Tui 'yeah right' to that

Well Millie. Could you suggest a colour and design for the patch for the old people to sew on to their jackets now. So when your 'little rant' is over, the squads will know who to take away. And we should not be sorry for them, after all they were warned by Millie.

A patch doesn't seem such a bad idea to me. As a tail-end baby boomer myself, I wouldn't mind something that would distinguish me, who has never voted relentlessly in my own interests and who has sympathy for young people, from other members of my generation with their grotesque sense of entitlement and righteousness and who speak with such viciousness of their own children's generation. All that disgusting crap about how young people expect so much these days because they have mobile phones and X boxes. It's called capitalism and it's called technological progress. Things get cheaper and thus much more widely available. That was the same for colour TVs and record players in their time. And I'm really tired of the bullshit about how tough baby boomers had it. They didn't - they're making it up.

of course they had it tough... livining in the snow in the middle of the road, naked, of course... they had to take out third and fourth mortgages just to put food on the the centre white line... while working three jobs each requiring 12 hour shifts a day....

What always surprises me, is their fathers (of the BBs) gave up their youth to go and fight a war in Europe, the Pacific and North Africa so their kids could live in a free and better society. Maybe that was the problem, lots now have the expectation that everyone should be providing more and more for them... dad did it, now the bloody kids should!

Generic Property Mogul Boomer to young person - "hey kids, if you can't find a job in NZ with your excellent education and can't afford to buy a house, piss off overseas, we don't want you whinging and whining here... we had it tough, living in the snow in the middle of the road, naked, of course..."

Do you expect to get a pension? Feel quite entitled to that do you?

I had a giggle about this- no patches or logos are necessary, are they? I hate to say it, but the ID marks are already there- wrinkles, balding and glasses. Egads! I've got the liver spots and reading glasses already! How can I go marching everyone else into the camp when I'm pruning up as fast as anyone? Do you think I'm any less prone to aging? The Grey power voting block is historically powerful because WE ALL GET THERE eventually. Vulnerbility + Voting Rights = Grey Power. A very motivated constituency.

As others have said, shared sacrifice will win the day. But I don't see how that happens when the minute the topic is raised, the older generation goes on the offensive and beats up on the messenger. Everyone has got to come to the table... without beating the drum of "I worked hard all my life...blah blah blah"... Focusing on how to share an ever shrinking pie as fairly as possible, level playing field and all that.

Some good comments abut how economic contraction exposes the sore spots- youngsters vs oldsters, and about offshore financing. I think it all comes back to CGT and getting money moving within NZ. And getting used to lower expectations.

Seriously - maybe we have a cross generational poverty. Oldies can't afford their own funerals. Young ones can't afford to buy a house.

maybe also what has happened the middle class has been hollowed out financially (again all ages) We have and always have had poverty stricken working classes. Now we are facing a middle class poverty. Maybe thats the reason for all this hatred and blaming.

at last someone states the obvious.

The baby boomers voted for Rob Muldoon and a his Think Big projects that raided the NZ Super Fund of that time so now the honey pot that they now dip into has lesser dollar value, the baby boomers have had the biggest chance to change the direction of NZ but have voted for successive governments that have failed to address fundamental issues surrounding the WIFM mentality of some NZers; this attitude has been handed down to Gen X & Y. The "blame" is now inter-generational and the surgence of the loopy green fraternity who will perpetuate the low GDP of the country with their No Mining, No Fishing, No Forestry, No Oil Drilling. No Foreign Farmers, No City Expansions Where are the taxes going to come from unless NZ agressively sets out to utilise the resources available and use the thousands of acres available to build new housing on, which will ultimately help to keeping housing inflation down to a normal level.

lies, damn lies and statistics

So it was ONLY baby boomers that voted for Rob Muldoon? A fair bunch of the younger ones wouldn't have been able to vote in 1975...

Plus, there were a fair few Depression era people voting in those days?

And lets just forget about the election where MORE people voted Labour, but due to FPP, National (Muldoon) won.

.... in this blame game , which Bernard drearily drags out everytime he has nothing sensible to write about , the " baby-boomers " are spoken of as if they are an exclusive club , a band-of-brothers , with special handshakes and a hearty " well met my fellow boomer " .....

We don't exist in isolation , Bernard ....... and we don't all vote for the pork-barrel politics which has ruled the country continuously since 1999 .....also , I'm sure that a plentitude of traditionalists & gen X's voted for the seriously dopey welfare policies that Michael Cullen & Bill English have introduced & supported ....

....oh , and if you think we're being snarky and getting up your nose , Bernard ..... have a looksie at the comments column in the NZ Herald ..... don roberts / OccamsRazor / and the crew all give you a right old spray for your blame-game-intergenerational-war rubbish .... I only got through page one of the comments , the general tone was to tar & feather the Hickster !

'Me thinks thou doest protest too much' GBH!!! Have a glass of Penfolds and chill.... the genXers and Yers will cover your bills...

....... who wants to be beholden to someone else ..... that's the rub !

I'll be happily swinging in my hammock , on a tropical beach , in my dotage ..... nary a pension in sight ..... sucking on a refreshing mango slushie ......

Governments assume that we want all this welfare junk , WFF , & CPI indexed pensions which they dream up.... but it's rubbish really , not being willing & able to survive by your own wits and planning . .

Did the BB's have to deal with a floating NZD? No!

"I was told the baby boomers had to cope with 20% interest rates " true but..........they also got 20% interest on savings at the time + NO RWT!

Short memory problems BB's?

Let it be known to you BB's. We ARE going to screw you over just like you did us. You failed this country, you took and took and gave nothing and still expect that pension + no CGT.

Forget it. Your days are numbered. With every yearly decline in NZ living standards the anger at you lot will grow and at the same time the 'power' will change hands. YOU ARE DOOMED

What a nasty post from somebody who calls themselves "Justice"

Justice is a relative term. Can be sweet for some & nasty for others depending on which end of it you are at. I find greed & the boosting about it quite nasty . Particularly from a generation that never paid for their uni education

So... Is it just the Baby Boomer's that went thru Uni that you will be targeting?

Yes, Justice, I didn't have to pay the cost of my uni education, other than a modest amount. Still I did two seasons in the freezing works, a couple of years of summer vacations in the railway yards, and two summers behind the wheel of truck - for Dominion Breweries and Hawkes Bay Farmers - to cover my expenses. I'm sorry there is a generation that has missed out on these kinds of work experiences. I look back with fondness on them now - I have left out many other jobs I did as well.

To balance out my experience I have paid in full our son's student loan and all his living expenses. He went to uni at 16 and got a Masters with distinction in record time. This contribution by my wife and I left us financially stressed to the point where all we now own is a bunch of share certificates - that's right NO property. The shares, though, I believe, are about to rock.

Rarely is there "justice" Something we all have to live with - unless you are one of the 1% or a member of the oligarchy running the show. Just make the most of your life. There's a day of reckoning for all those smug with their assets, imo. I would suggest you don't go down the path of the "drab duo" on this message board. Their manaical bitterness will probably shorten their lives , or even worse prolong their miserable existence.

Justice, Did we baby boomers die with Muldoon? Not... we have lived through every calamity and the poor judgment of every politician since, along with you, global and domestically.

The mistake made by us was to increase the expectations of our children; working your way up through the shark infested waters is not in their vocabulary. All toys are an expected given...chose a varsity degree in some far fetched ongoing folly of fun that will never get you a job. Why grow up? BB parents will continue to carry you...

Yep there have been some property gains made but much of that is severely negated by increasing weekly costs associated with supporting a very expensive intrastructure. Mainly from the income and support expectations from all levels of the community.

Expect many BB's to be working beyond 70, if they can find a job. Expect to learn to expect less.

there is nothing worse than having the expecation of a certain retirement to have it taken off you...much worse then never having had it at all. Unless you are very wealthy you will pay.

Bernard struggling for copy again this weekend, and pulls out one of his guaranteed favourites to generate a response - well done Bernard, I'm sure it will continue to do so in the future as well as the blame game will always remain popular.

What a sad thread. We are all in this together, my father helped me Im helping my children, lots of love no anger in my family, no blamming someone else, just getting on with it. I try and teach my chilren to accept responsibility for their mistakes and move on. Personal responsibilty no blaming anyone else. Take it on the chin and move on. Work with what you have.

I read a while back that I think %50 of adults over 50 in the Uk had less than £5000 in the bank. We have been fleeced by the Banking, Realestate and Insurance industries, aided and abetted by ignorant or selfish geedy politicians.

The problem is its very hard to start a business in NZ and make any money but Capital gain requires little work ,skill or brains and is mostly tax free. We all need a roof over our head. What the hell did we expect the outcome to be, we got held to ransom.

I think its going to get much tougher than this, more like the 30's but worse for many. Listened to John keys speech at the National party conference, sounded like he was playing the crowd, they must have the brains to see through it, mustn't they?

have a look at this

http://forums.wallstreetexaminer.com/topic/1044427-creditors-have-big-l…

On the money A.J......although mine (father) was in no position to help me, I would absolutely support the sentiment of your post..

We are all in this together................and nobody promises us tomorrow....do what we can with sincerity and resolve.

It still saddens me Bernard cannot see past his frustration, cannot see the language he uses is devisive, cannot see his time to be alienated is coming ready or not.

Maybe an opiarectomy would help you Bernard, ...that's where they sever the cord that connects your eyes to your annus.....to rid you of that shitty outlook on life.

Fell from the sky..............................my ass...!

Sorry to tell you this guy's but we're talking about a failure of leadership. A failure to stop what was patently and obviously sheer stupidity to many of us.

Blame who you want it wont change anything, we are just at the blame stage, anger is building, acceptance is still a long way off. We all get to vote, the youger voters could use social media and turn this country on its head, just needs some leadership.

Those at the top intend to take a lot move than they have so far.

The problem is prevasive across all ages I think. The Ponzi finncial system has caused us to think we could have a greater standard of living than was realistic compared to our productivity. Maybe we are going to have to have so many fewer things. All of us.

Could we please forget this “us and them” intergenerational envy thing and try to focus on some of the issues and seek some answers and solutions.

At the outset I declare that I am a baby-boomer and, along with other investments, I have two investment properties.

Firstly, please do not stereotype property investors as just baby-boomers. I know of a number of young astute property investors (i.e. long term investors and not “20 properties in two years” ilk); one a student who purchased his first investment property six years ago while still at school, another, a thirty year Maori female investor, who looks very closely at yield rather than expectations of short term capital gain and is a executive member of our local property investors association, and a step son who has an investment property before thirty without any parental assistance.

However, I accept that many property investors are of an older generation who have built up equity over time and have then have been able to use that equity to invest in property; this is part of a life-stage and I suspect many of the X and Y generation will likewise experience this same life-stage in the future. The Baby-boomer property investors have been fortunate in their timing.

I appreciate the difficulty many young first home currently (I emphasize “currently”) have. One needs to expect times during one’s life time when wider economic circumstances will seriously impact on one’s plans to achieve economic security and it has not always been easy for baby-boomers who rightly point out interest rates of 25% in the early eighties were crippling.

In this debate the many now retired people who have built up a cash nest egg are finding their expected bank investment returns well below what they thought it would be four or five years ago, and it looks likely that low interest rates, as Tony Alexander says, are with use “for YEARS to come”. For young first home buyers this should be seen as a positive; and lets us not get into the argument that it is at the expense of the older generation - it is a matter of current economic circumstances.

I think that we also need to ask why property is the investment of choice for many (of all ages).

As Philip Macalister in the “Herald on Sunday” this morning points out, the conviction of two directors and COE of Capital+Finance is a good place to start. It is not only the collapse of this and other financial companies, but also the culture that prevails much of the financial sector. The Hotchins and Petrovichs et al are extreme examples of a culture where the interest of the investor are a distant third behind the interest of self and profit; it is therefore not surprising therefore many choose property as their investment. The financial market and commercial sector really need to address this.

The fundamental issue with superannuation is whether it is either a universal (i.e. government) or individual responsibility. Given the flip-flopping over the past 35 years where two Labour Governments have established funds to meet expect shortfalls universal superannuation, successive National Governments have effectively destroyed these. Baby-boomers have until now been led to believe that a basic level universal superannuation will be available in their retirement.

However this is not just an immediate future issue. KiwiSaver is woefully inadequate as a means for individual responsibility as it is neither compulsory nor are the levels of contribution (by individual and employer) anything like significant enough compared to that of Australia.

For Generation X and Y the issue of superannuation is not only the immediate cost but whether they will have universal superannuation or will it is an individual responsibility. Certainty needs to be address for all, baby-boomers, and generation X and Y.

The only benefit of intergeneration warfare is the ratings of this site!

However, I accept that many property investors are of an older generation who have built up equity over time and have then have been able to use that equity to invest in property;

I think the fact that the equity you talk of was unearned and untaxed galls the many.

A similar principal position, in any other area of commercial interest , say government debt attracts an income tax levied at the marginal rate on all capital gains above the certified entry price.

The inequity of this fiscal position has favoured those bold and leveraged enough to capitilise it and place shelter beyond the reach of most new entrants.

i am so glad that my wealth has fallen from the sky because i have watched a lot of it disappear as soon as i drove it off the car yard.

can't have it both ways i suppose

There's no doubt that housing is much more expensive relative to income than it was prior to the 1990s

Although I largely agree with Bernard, I don't think the discrepancy is quite as large as he argues though on a "net" basis . For example, my dad paid horrendously high income tax as an upper middle income earner throughout the 1970s and 1980s. And consumer goods were generally a lot more expensive

It's still art SoreL....cheers for that.

Sore loser,

Happy to answer some of those questions.

Interest.co.nz is owned by David Chaston. I'm an employee earning a salary and paying PAYE. I don't and cant' claim 'expenses'.

My wife and I own the house we live in. The irony of all this is I'm one of those to benefit from the largesse falling from the sky. We bought in Auckland 2005 and no doubt have plenty of equity, assuming of course we could sell it, which we've thought about doing in the latest surge of activity. Our focus is on debt repayment.

I'm 45, so I'm on the fringes of the generation I criticise. In many ways I criticising people in my situation, although I have in effect invested time and effort in helping David build up this business to employ 10 people. It has no debt is not funded from mortgages.

I'm very keen to build businesses and employ people and provide a useful service to as many people as possible.

Lots of other questions there. Sorry, but have to head home.

cheers

Bernard

Mr Hickey will not respond to any of the comments above, what he wrote on a wet & boring Sunday morning was designed simply to get a few more comments from those with nothing else either better to do. Black is white, wanna fight about it & boost my website ratings too?

FYI from an emailer:

Dear Bernard: I was highly amused with your emotional and, in the terms of economic psychology, naive article of last week and then this emotive response to those who responded emotionally. Yes the baby boomer generation is going to put a strain on NZs resources......but as you and I both know this problem has been recognized for over 20 years. In New Zealand both Labour and National gvts have applied the Ostrich approach to dealing with the problem, Now they will have to pull their head out of the sand. However They like every OECD state will likely take the simple thing ( rather than thought out planned options) of doing, as you reflect, raising the retirement age As for your articles on raising the retirement age: Clearly from a psychological view point your assumptions are based on the fact that the "Pie" that superannuation is paid from is going to stay the same or reduce. Of course you say "every one knows that" but lets look at some general principles( of course there are exceptions): 1. People starting their careers ( age range 18-35) tend to be more innovative and are prepared to take more risks. thus group is the one that develops and drives the economy forward. 2. Raising the retirement age again will force that group, who would exit the work , to remain in their positions blocking promotions and new entrants into their industries. 3. Those, above 55, who find they have no work opportunities through redundancy illness or other will still get support,from the state in the form of unemployment benefit, sickness benefit and I suspect (IMHO) bizarrely training allowances. 4. Young people with the get up and go the economy needs, on finding the opportunities they seek less available in New Zealand than in the past , will take the easiest path. They will leave NZ taking their Youthful drive out of the NZ economy and will reduce the NZ economy's ability to raise more taxes to support those needing it ( not just superannuants). 5. A recent report( I am sure you can find it) was commented on in a UK paper about two weeks ago. That report noted that the current austerity measures being taken in the UK would be less necessary if the UK increased the number of immigrants allowed into the UK. Effectively the report stated the economic stimulus that would result from increased population would increase the tax money available to the UK treasury. Initially you may not see these points as valid but step back and have a look at what has been happening in mainland Europe over the last 20 years. Unlike New Zealand where the accepted norm is that graduates start working at the age of 21-24 years ( depending on the qualifications they get) Graduates enter their first full time position when they are aged 28-35 years of age often before that age they work in unpaid internships. They are unlikely to change jobs to find a more personally suitable career path. because of the difficult of finding work they are often less willing to take risk and will simply follow the old ways of doing things....IE: innovation is stifled. As I noted earlier you have taken the accepted view point that Superannuation is affordability. That view point is parallel to the one that has seen small hospitals in New Zealand closed down(As one of many examples). Rather than introducing policies that bring more money into New Zealand its easier to take a defeatists view pont and close down infrastructure and social support. The UK report I referred to ( sorry can't recall its name) suggests another approach...one that is unpalatable in the UK and I guess likewise in NZ . Increase immigration substantively. I am sure there are other approaches that will also increase NZs foreign eranings and the tax take ( with out increasing taxes or cutting back on support) NZers need to decide what sort of country they want to live in. Do they want a US style capitalism where the sick old and unemployed find they have to live on the streets while the richer get richer or Does New Zealand wish to take a grow your way out of the problem. Regards IanIan

Many thanks.

A couple of points in response. You say the youth will generate the growth by being young and innovative.

It's true there will be innovation, but proportionally less because the young cohort is proportionally smaller. Also, the young will struggle to get access to risk equity capital to build their businesses because the investors/savers are overwhelmingly older and more interested, given their age, in more stable and lower risk assets such as bonds.

Here's more on this from NZIER

cheers

Bernard

As a early BB, I will get my pension in 2 years time. I remember the bomb sites in Cardiff very well, life for us was very very hard in the early fifties. It taught us not to waste anything and to be very careful with our money. By the time I left school I had never been to a coffee shop or a resturaunt.

I was engaged at eighteen and we saved everthing we had for our house deposit. We arranged dates in advance as nobody had phones. When we bought our first house in 1971 my workmates told me I was mad to take on a huge mortgage, but we did. We had second hand furniture, an old black and white TV and we grew vegies at the bottom of the garden. A night out was a drink out at the pub once every few weeks and fish n chips on the way home.

I started work at 7.15am, had a10min teabreak at 9.00am where I had a homemade sandwich and coffee from a flask. At midday we had 1 hour lunchbreak where we ate more homemade sandwiches and more coffee in a flask and read the newspaper. 4.15 pm was finish time but because I had a mortgage I worked 1 hour overtime, I also worked 7.15 am to 12.30pm on Saturdays, played soccer in the afternoon and again worked sunday 7.15am to 4.15pm. We had two weeks holiday in July, 2 days off at Easter, Spring and Autumn Bank holidays and Chrismas day off, back at 7.15am on Boxing day and New years Day.

I worked in the car industry as a highly skilled modelmaker, I had to use big band saws and planers without extraction, we used fibreglass again without protection so now I am deaf and have a lung disease.

When we had children no calls on phones at home, no my wife had to go to the post office to call me. I had two days off, unpaid.

It was us babyboomers that changed all this so that you have an easier and safer time of it. Please respect what we did for you then.

Go into op shops raising money for charity, visit a Red Cross meeting or a Rotary meeting, yes you will find us baby boomers saving the country millions though our charitable work.

Respect. I can say as a Gen Y that I have never had to suffer that kind of hardship, when we grew up in the 80's and 90's nothing like that happened where I came from, I reckon everyone should take a leaf out of your book, even today I pay $4.50 for a coffee every day and don't think that is extravagant spending, I smoke cigarettes and cigars and drink a lot too. Times need to change, but before they change we need to change ourselves.

FYI from a reader via email:

Hi Bernard,

I suspect that the stream of negative comments your piece has been receiving on the Herald website, means that you have touched the same nerve yet again.

Another point: unemployment in the 1970's and early 1980's was extremely low compared to now, especially for youth. You could get a decent paying apprenticeship straight out of high school at 15, without going to uni and without getting into student debt. So by the time you were 25 you could be a fully qualified tradesperson and freehold in your own home.

Kind regards

FYI from a reader via email:

Dear Mr Hickey The past really was another country. Until the Employment contracts Act for example people had award wages, overtime and all sorts of others worker’s rights (and jobs) which have since evaporated. Also State Advances Loans. So agree with you about house affordability between then and now. But it is a shame when people get into the habit of generalising about entire generations. Believe it or not lots of us baby boomers were idealistic and civic minded. But it should be remembered that Mrs Thatcher and Ronald Reagan (who were not baby boomers) championed unregulated capitalism which gave corporates and banks increased global power and less responsibility. Yes some baby boomers, like those in the 1980/1990’s governments in NZ did slavishly follow their lead. Agree the current trend is just unsustainable. But please remember which generation it was which created Grey Power, the generation before the baby boomers! It is now a case of over 65’s being victims of their own “success”, sticking out like sore thumbs with their gold cards and the only universal benefit left in this country. So students, children, the working poor and the rest are really doing it hard – just check out the massive increase in demand at foodbanks right throughout the country and our disgraceful child poverty statistics. Unless New Zealand comes up with a magic solution to increasing this country’s prosperity to the point where a good percentage of the diaspora returns here and starts paying taxes sufficient to afford the steadily increasing “super bulge” there needs to be some or all of the following: Means testing for super and gold card Abolishing entitlement to super for under age spouses Increasing the eligibility age by two months per year starting RIGHT NOW. As an Australian living here I can assure you that over the ditch oldies are not starving but, more importantly, the attitude there is a slightly pitying attitude towards those who have not managed to provide for their own old age and are thus dependant on handouts. A bit of a contrast to the entrenched entitlement attitude here. As big an elephant in the room as the super is how on earth is our public health system going to cater for a massive increase in costs to care for the aged?Elizabeth

FYI from a baby boomer in Britain, Jeremy Paxman.

cheers

Bernard

The BBC's top tax dodger - didn't hear him blowing any front running whistles.

FYI from a reader via email:

Hi Bernard

I am a huge fan of your's and love how you openly address the great wealth and policy bias that follows the baby bomber generation.

their other major privelidge is a politically impotent oposition, in the form of gen x and y.

I would love to read more on this topic and was wondering if you could please recommend a couple of books to start on.

Kind regards

Nick

Cheers.

Here's one book that's good from David Willetts, who is a minister in

the current British government.

http://www.amazon.co.uk/The-Pinch-Boomers-Childrens-Future/dp/1848872313

This provocative and thought-provoking book argues that the baby

boomer generation have thrived at the expense of their children. The

baby boom of 1945-65 produced the biggest, richest generation that

Britain has ever known. Today, at the peak of their power and wealth,

baby boomers now run our country; by virtue of their sheer demographic

power, they have fashioned the world around them in a way that meets

all of their housing, healthcare and financial needs.

In this original

and provocative book, David Willetts shows how the baby boomer

generation has attained this position at the expense of their

children. Social, cultural and economic provision has been made for

the reigning section of society, whilst the needs of the next

generation have taken a back seat. Willetts argues that if our

political, economic and cultural leaders do not begin to discharge

their obligations to the future, the young people of today will be

taxed more, work longer hours for less money, have lower social

mobility and live in a degraded environment in order to pay for their

parents' quality of life. Baby boomers, worried about the kind of

world they are passing on to their children, are beginning to take

note.

However, whilst the imbalance in the quality of life between the

generations is becoming more obvious, what is less certain is whether

the older generation will be willing to make the sacrifices necessary

for a more equal distribution. "The Pinch" is a landmark account of

intergenerational relations in Britain. It is essential reading for

parents and policymakers alike.

cheers

Bernard

FYI from a reader via email:

Hi Bernard. Enjoy your website, and some of your comments. However challenge many of your assumptions on NZ Super, and the alleged costs of aged population? I also have reservations about media handling on this issue, the commentary is all one way, and dissenters to your view, and the likes of Fran O'Sullivan and Hooten, etc. Not a conspiracy but editorial bias!!! Enclose a recent letter to the Listener, not published, I wonder why?Len Bayliss a New Zealand economist said in 1996 ”doomsday rhetoric characterizes NZ media handling of retirement income policy” and the Listener editorial June 23 illustrates this. The focus by commentators on 2050/ 2080 projections are too far out in time to be useful, and must be viewed very cautiously.

Superficial comment on “the burden of the ageing population” abound, rarely commenting on the fact superannuation policy is far more than a monetary formula. It is linked to issues of physical security, personal well being, economic productivity, social health and the distribution of income and wealth. New Zealand’s superannuation scheme is a recognized world leader, with a simple structure, and low cost administration, with no exceptions, e.g. surtax often lead to sham trusts or avoidance schemes.

The dollar cost of NZ super as a proportion of GDP is also exaggerated. Unlike many other countries New Zealand does not pay a tax free Superannuation pension. That needs to be factored into the numbers; the current after tax figure is 3.7% of GDP a very low figure, and future projections within a reasonable time frame (2030), show around 6%, also a sustainable figure.

Many of today’s seniors are economically active, boosting the participation rate and paying tax. We should talk about “multipliers” more people working means increased output, stimulating the economy, and increasing productivity. Voluntary and unpaid work needs to be factored into the costs, and seniors are involved in less crime and Road accidents, all providing economic benefits.

The debate to date has been unbalanced, the stage set by right wing commentators and economists, not a good mix for sound social policy. Current measures used to assess the community cost for supporting the senior age group are error ridden and most comments overstate the extent of existing knowledge and its degree of certainty. Roger Hurnard a consultant on NZ retirement issues, in his 2011 paper “Mixed messages :the future direction of NZ retirement income policy”:, provides an excellent introduction to this issue, and the Retirement Commissioners “2010 review paper” on Retirement income, is a thoughtful and restrained discussion paper. Knee-jerk assumptions and screaming headlines are counterproductive to a useful debate and sound outcomes.

I agree we don't have a problem if we keep growing as strongly as we did from 2000 to 2007.

But even the RBNZ is now saying our trend growth rate has halved to 1.5% and the Finance Minister said this weekend that the Global Financial Crisis could last 15-20 years.

Wouldn't we be irresponsible not to consider what these things mean?

cheers

Bernard

"I agree we don't have a problem if we keep growing as strongly as we did from 2000 to 2007."

trouble is... that growth was "fools gold"... Completely based on Credit growth.... akin to digging a deep hole.

I don't think it is possible to growth our way out of our problems and issues.

i'm guessing it will be credit growth that gives us the short term reprieve ..of any meaningful, renewed GDP growth...

I also think Bernard has got it wrong about Baby boomers..

The primary beneficiaries ...who are also the culprits.... is the "financial Sector" of the global economy...

The growth of the financial sector...which has been on the back some some really..really flawed central Bankers policies ( theyre all in the same bed).... has been profound!!!....Utterly profound.

We have the "financialization" ...of almost everything.

People forget that only 50yrs ago the family home was just that..... simply a family home.

look at what it is now..!!!!

I think Bernard is beating/whipping the wrong horse.!!!

Cheers Roelof

Bernard: Right now 20% of the people who die have to have a 'funeral benefit' paid out by WINZ. I bet you there is a significant chunk - say another 20% of those who die - who have the $5K to bury themselves - but nothing else.

The problem is we are all in deep fincial doo doo in this country. As the result of profligate spending both personally and by governments over many years. Young people are in trouble financially as well.

Encouraging the kicking of one group by another is not going to solve it, and increases the nastiness of our society. It's actually not a practical solution Bernard.

We need to take the financial services industry drain out of our system. And set up compulsory saving which prefunds people's retirement. Yes that second necessity will reduce current disposable incomes markedly. But in the long run you can only consume what you produce.

The alternative is that our current 30 year olds will arrive at retirement with no income prospects at all. And find the people who you have been blaming are no longer available kick. But I suppose they could shoot themselves.

Perhaps we need less expensive funerals?

we could go without the sausage rolls.

And without "funeral directors".

Dead right.

I think we would need sausage rolls. But as revealed on this very site - there is no land shortage- we could plant Granny in the garden ourselves. Sausage rolls and a few beers. Total cost say $50.00. MInd you the way it's going with the improvished New Zealander. Beers might have to be cut off the list

Find a mate who does home brew.

Home brew will have to be it. Some chap called Hickey reckoned Gran the boomer was loaded with cash. We had a conversation with her but she was difficult. After her 'fall' we found she had been right all along. Not a bean !!

Want to end "intergenerational inequality"?

Too easy. 100% inheritance tax. That'll get em squealing!

I guess it wasn't doing anything. Food, water quality, biota, bees?

Nup, there it was, just waiting for housing tracks.

Good-o.

.

Encourage people to leave Auckland......ease pressure there, and boost provincial areas.

Rezoning plus compulsory aquisition?

Bernard, not so long ago i was reading an article of yours in which you said that you were sucked in by Rogernomics. How you believed all the bull but now your eyes are wide open. Well Bernard, you are, or are supposed to be, a finacial journalist. If you really are a journalist you would have taken the trouble to check your facts before being sucked in. Sucked in just like those creapy journos who clapped Mr Whittle at Pike River. No doubt as a financial journalist you were, at the time, passing on the good word about how great Rogernomics was and, no doubt enjoying the ride while it lasted and encouraging others to accept this bizzar economics.

Now it has all turned to custard you wont look in the mirror at the part you played, you just push the blame onto somebody else.

SO Bernard, pray tell all, did you warn people against Rogernomics or sing it's praises? Come clean.

FURTHER

I thought that BB's were born straight after WW11. That is , born in the 40's and 50's and you say

"Property is much more expensive for first home buyers now than in the 1980s and 1990s when baby boomers were buying their first homes"

So you are saying that they were 40 or 50 years old when they bought their first house?

No, it was the children of the BB's buying houses in the 80's and 90's and would have been born in the 60's and 70's which puts them in the 40's and 50's age bracket today.

FURTHER Bernard you say

"The stay-at-home mum of the 1970s and 1980s is not an option now."

ARE you listenning Bernard "WHOSE FAULT IS THAT?"

Who sat on their litte bottoms and allowed all these things to be taken off them?

FURTHER you say

"Reserve Bank figures show the net equity in housing wealth more than doubled from NZ$203.5 billion in 2002 to NZ$456.7 billion in 2007. Property owners' wealth rose the equivalent of more than 125% of GDP in 5 years."

SO, acording to your analysis, only BB's gained from this because they were the only ones to own houses.

AND

What are you supposed to do, if the house you live in doubles in value and puts up your rates and insurance, FEEL GUILTY?

There seems no point in trying to explain anything here except

Maybe you are just looking for a crisis to add to your list. You have

The Euro Crise

The China crisis

The GFC crisis

The LIBOR crisis

The housing bubble crisis

The pension affordability crisis

And of course

The BB crisis

Take a good look Bernard because if you look at all these crisis you will see they all lead to one conclusion. I will leave you to wake up and find it for yourself.

Mike B

The baby boomers were born between 1946 and 1964. Therefore boomers were buying first homes typically between the early 1970s and the mid 1990s.

Bernard

My daughter is 30 years old, is a solo mum (9 year old daughter).

Now this is A FACT and if you do not believe me then I BET YOU $20,000 and i will prove it.

About 3 years ago my daughter was a laborer on the minimum wage and flatting. She got sick of landlords mucking her about so she went to ALL the banks for a mortgage. They all turned her down except SBS which gave her a 100% mortgage on a small flat in Christchurch. About that time i believe you were telling everyone to get out of houses because the price was going to collapse 30%, but you can correct me on that.

At the time she fixed her mortgage at about 8% that i recall and currently is locked in at i think 7%.

She does not have a flash car. Nor does she have the internet. She does not have a big flat screen TV or a fancy cell phone. She has none of these fancy gadgets BUT SHE DOES HAVE HER OWN HOME.

So if she can get into her own home why cant the rest of you. Because your all lazy,and want everything and all moaners instead of getting on with it.

So Bernard, OR ANY OF YOU WINGERS OUT THERE, care to take on my bet?

Getting knocked up to some poor sucker who earns heaps is a fantastic career choice for NZ women!! What does she get 20% of his after tax income (who can't get ahead on $400+/wk). Why can't she get a job, re-train and be a productive member of society instead of being a leach...

This is far from a success story - NZ taxpayers or the sugar daddy are funding you daughter build assets - the DPB is not a method to get ahead.

geeeez goldenfox, how did you read that into MikeB's post. His daughter was working at a labouring job 3 years ago when her daughter was 6 yo. She was (still is?) working.

@iconoclast,

Thanx

Yes she is working but has had a promotion because she is a hard and dedicated worker. She is now paid a little more, but only a few dollars more. She is doing some exams and if she passes hopes to get another pay rise.

@goldenfox

My daughters flat in in Hornby, Christchurch it did get some EQ damage she gets Zero, zilch from the childs father. In fact she needed a bed and the father said if she got one on hire purchase he would pay for it, but he did'nt and now she has to pay that as well.

If you believe i am a liar then take on my bet ALL BETS WELCOME.

Bernard WHERE'S YOUR BET?

Alex, the BB hater WHERE'S YOU BET.

Comon take me on the more the merrier.

BUT none of you will because all all full of schite

FYI from a reader via email:

Bernard, Now that the super storms you ignited have died down may I suggest that we need to remember NZ Super is already substantially means tested - something that seems to be forgotten in the hype and hysteria that invariably surrounds the debates re the boomers vs the rest and the affordability of NZ Super. http://www.workandincome.govt.nz/manuals-and-procedures/deskfile/nz_superannuation_and_veterans_pension_tables/new_zealand_superannuation_tables.htm On the continuum from a single living alone on just super at $ 698 / fortnight to an individual - married on 33 % tax of $ 405 who has lost 42 % of his individual entitlement. This is a very significant element of means testing. The pragmatist in me says the simplicity of the existing National Super scheme has great attraction if your going to have some form of super. I am also of the view that many in physical work simply cannot work beyond 65 and some won't even make it to 60 - yet many will have to work well beyond 65 to make if affordable in a macro sense. Yet we can't go on living longer with all the associated health costs at current contribution levels. No doubt you have see the Stats NZ household survey of individuals over 65's investment incomes. Two thirds have zero and the other third have ~ $ 1000 pa. Trust income could be an issue here - but any way you cut it the numbers are damn near zero ! National Super is here to stay with all that that implies. It's great that your are able to elucidate the major issues facing this nation - and there sure are some for those who choose to think for themselves. I have just seen the latest current account forecasts for 2016/17 - a trade deficit and $ 20 Billion C/A deficit. We really are becoming dependent upon the kindness of strangers for our lifestyle. Another day's problems - also intractable.Cheers, John

Cheers John.

I agree NZ Super is actually a pretty good scheme. I also have

misgivings about changing the current means testing system.

But somehow we need to make our sums add up over the next couple of decades.

cheers

Bernard