By Bernard Hickey

Like any successful politician, John Key knows the saying that a week is a long time in politics.

He is a master of not over-committing to a public stance or taking the long term support of the public for granted.

The Prime Minister knows when to hold 'em, and he knows when to fold 'em, as he discovered last week when his 'eyesore' comments triggered a public backlash against any taxpayer money being used to build the Sky City Convention centre.

His stance changed within days, proving his Ali-esque ability to roll with the punches and dance around the ring to avoid a knock-out blow.

A week is not that long in the world of mortgages and interest rates, but these days a lot can change in a month or two. Just before Christmas the Reserve Bank of New Zealand was still forecasting higher interest rates by the end of 2015 and most people thought a recovering global economy would eventually start to push up inflation and interest rates.

Fast forward to late February and everything has changed.

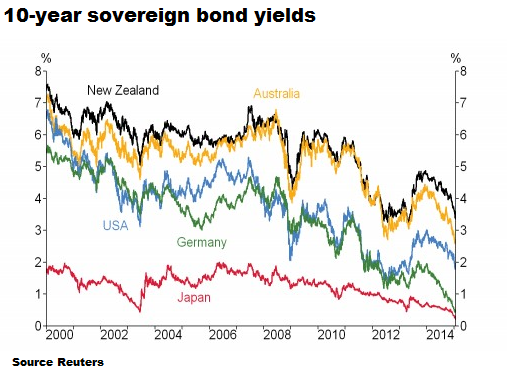

Eighteen central banks have cut interest rates or launched "Quantitative Easing" programmes whereby they create money out of thin air to buy Government bonds. All of New Zealand's major trading partners have either eased monetary policy or have set their interest rates near 0% for years. The Reserve Bank itself has said the Official Cash Rate is on hold for the foreseeable future.

The scale of the cheap and easy money pulsing around the globe is mind blowing.

Central banks in Sweden, Denmark, Switzerland and the European Union have cut their deposit rates to below 0%. That means other banks have to pay the central banks to look after their money.

JP Morgan estimates there is now US$2 trillion invested in Government bonds that are yielding negative interest rates.

That means investors are so convinced that prices are falling and the money printing will go on for years that they are willing to effectively pay their Governments to look after their money. Two year Swiss Government bond yields are now below minus 1.2%. German ten year 'bunds' are yielding 0.3% per annum and the wisdom of the crowds in global bond markets have been driving bond yields ever lower for most of the last decade.

In the last month our two largest trading partners, China and Australia, have eased monetary policy and are expected to cut interest rates even more in the months to come.

Yet New Zealanders, and the Prime Minister, are apparently unshakeable in their belief that interest rates can't fall much lower than they already have and that any interest rate with a 5 in front of it is a great deal.

That was clear in the near euphoria that greeted the TSB's announcement on Waitangi weekend that it would offer a 10 year mortgage for the apparently astonishing rate of 5.89%. Surely, people thought, that rate will never be repeated.

One television network led its nightly news bulletin with the sensation of it.

The next Monday morning Mr Key reflected the nation's celebratory mood in a breakfast television interview with the comment that a 10 year mortgage was a "good thing" and would give borrowers a lot of confidence.

Yet since TSB's announcement, fixed mortgage rates have fallen further. HSBC even set the same 5.29% rate for every mortgage from 1 year to five years. The average two year mortgage rate has dropped from over 6% to under 5.4% since October.

So it's worth challenging the national assumption from the Prime Minister down that interest rates can't fall any further and that fixing for as long as humanly possible with a rate with a 5 in front of it is a good idea.

The assumption is that 5% is 'below normal' and a quick reading of history would suggest that is true. The average two year mortgage rate in New Zealand over the last 10 years is 7.2% and just six years ago it was well over 9%.

But what if the new 'normal' is something much lower than 7%?

The global bond markets have come to that conclusion and both global and local economies keep surprising central banks with unusually low inflation rates and even deflation, despite often solid economic growth and exploding asset prices. It's as if the usual inflation-generating parts of the economic machine are broken.

There is a growing body of thought that cheap and powerful new technology such as smart phones, ageing populations and the globalisation of services are driving prices down all around the world in a way not seen since all of the 1800s, when the first age of industrialisation created regular deflation and interest rates were typically around 3%.

The disconnect between New Zealanders perceptions about 'normal' mortgage rates and the rest of the world is cavernous. In Britain banks offer initial two year fixed mortgages at 1.2%. One Danish bank toyed with the idea of offering mortgages with a negative interest rate this month. That means the bank pays the borrower. The average long term Danish mortgage rate is 2.6% and the average short term rate is 0.3%.

So why are New Zealanders so sure that mortgage rates can't fall much lower over the next 10 years? In late 2008 many Kiwi borrowers leapt at the chance to borrow for five years at less than 8%. Within a year many were paying huge break fees. Just imagine the break fees on a 10 year mortgage if rates fell to European levels.

Mr Key would never dream of committing himself to a policy stance for 10 years, yet was comfortable suggesting borrowers commit themselves to a mortgage for 10 years. TSB even boasted of the Prime Minister's support on its Facebook page.

The mortgage times they are a changin' and borrowers should be just as light on their feet as the Prime Minister is with his policy stances.

-------------------------------

A version of this article was first published in the Herald on Sunday. It is here with permission.

22 Comments

One Danish please! Lol.

Perhaps Kiwis have heard so many hiking messages from bank economists and so many 'historically low' media stories that they don't realise that all other developed countries are offering 1 to 4% home loans.

However, as your article discusses, as Capitalism goes through its dying throes anything could happen: we could see a huge spike in interest rates if major events / military action in the Middle East & Europe start unfolding. We could see another liquidity freeze up temporarily. We could see nationalisation of many countries assets/finances as Socialism takes over under another guise.

My take over the last 6 years has been to fix for 6 to 12 months with brief floating periods. However, if a certain strategy has been suitable for a decade, then another big change will hit.

Im now starting to think long term fix - mainly due to huge geopolitical risks ahead which will probably change all the rules. But I'm sure the banks could break a fixed deal on you if they wanted to, so really there's no insurance for the householder/borrower/consumer.

Nothing wrong with the ten year idea Bernard. It's just the price you have to question.

Interest rates can fall, the question is , 'why are they falling'?

Sweden has dropped interest rates, why

Sweden's new center-left government and its financial authorities are under huge pressure when they meet on Tuesday to tackle a mountain of household debt that is casting a long shadow over one of Europe's few economic bright spots.

"The longer we wait, the bigger the imbalances are," said Bengt Hansson, analyst at the Swedish National Board of Housing Planning and Building. "We already have a bubble, but we will avoid an even bigger bubble."

Consumers bullish

It will be hard to dissuade bullish Swedish consumers.

In Stockholm's frenzied housing market, buyers make multi-million crown offers to snap up flats they may only have seen in photographs. And cranes and scaffolding are common sights in suburbia as householders take advantage of generous tax breaks for home improvements.

http://www.marketmoving.info/swedish-housing-market-bubble-poses-huge-r…

Denmark With a debt to GDP ratio of ~ 260 % !1

Currency War Feeds Denmark’s Housing Boom

Amid Extreme Rates

http://www.bloomberg.com/news/articles/2015-02-19/extreme-negative-rate…

Nov. 21 (Bloomberg) -- Dutch architect Rien de Ruiter describes himself as a survivor after the housing-market bust that cost half of his colleagues their jobs.

http://www.bloomberg.com/news/articles/2014-11-21/euro-area-s-third-hou…

Surely a time to reflect upon the inevitable failure of corporate memory.

".....The world of finance hails the invention of the wheel over and over again, often in a slightly more unstable version. All financial innovation involves, in one form or another, the creation of debt secured in greater or lesser adequacy by real assets. This was true in one of the earliest seeming marvels: when banks discovered that they could print bank notes and issue them to borrowers in a volume in excess of the hard-money deposits in the banks’ strong rooms. The depositors could be counted upon, it was believed or hoped, not to come all at once for their money. There was no seeming limit to the debt that could thus be leveraged on a given volume of hard cash. A wonderful thing. The limit became apparent, however, when some alarming news, perhaps of the extent of the leverage itself, caused too many of the original depositors to want their money at the same time. All subsequent financial innovation has involved similar debt creation leverage against more limited assets with only modifications in the earlier design. All crises have involved debt that, in one fashion or another, has become dangerously out of scale in relation to the underlying means of payment.” John Kenneth Galbraith, "A Short History of Financial Euphoria" Read more

.... but what happens when you are paid to borrow?

So Sweden is concerned that house prices have risen 196% since 1990? Then don't come to Auckland where prices even in Glen Eden for example from 1990-2015 have increased from $100k to $500k for the same 3-brm modal house. That is a solid 400%, twice that of Sweden.

Either Auckland is a bubble, or Sweden is still cheap.......

The problem is, if interest rates ever do go up and they surely will, many mortgagors free cash-flow will evaporate in additional loan interest payments. The bubble may then pop. A serious unwinding would wipe out a lot of home-owner equity given that housing is effectively a leveraged investment.

In 1989-1991 Auckland house prices fell up to 30% - the higher they were in terms of value the harder they fell. The lower value housing did not fall much perhaps 10%. Some players would not even be aware of this historical fact. Indeed there was comment by someone in the industry only a couple of weeks ago discussing property cycles who failed to mention Auckland's most serious property value downturn in a generation.

Seems that there are a number of first world countries experiencing hyperinflation in main city real estate, against a backdrop of deflation in the broader economy including interest rates. We need to figure out what it means, where it is heading to and what the risks are.

Are interest rates so low because the global economy is doing well, or because it is doing great? I don't think people are buying negative bonds because they are thinking of getting a smart-phone cheaper in the future LOL. As I have sai before, there is a lack of 'money good' collateral available, aka bankable projects. Supply and demand, lots of money (demand) nowhere to put it (supply). I'll admit I don't understand enough about your historical deflation analogy, but I can't see we are making the same 'type' of progress that you describe. We have the global consumers who are not earning more money, instead we have elites who are earning more money and want somewhere to put it. All the income growth is going to the wealthy, who have more money then they could ever spend. The measure of how brilliant and deserving of this wealth they are, is in the fact that we have them holding it at negative rates rather then using it productively. We call these elites, the producers and entreprenures, the job creators worthy of all this wealth, and are expected to be grateful that we have them.

This is not a financial riddle.

This is not a poitical riddle.

This is a type of insanity.

The insanity concerned was researched by David Dunning and Justin Kruger here.

"Unskilled and Unaware of It: How Difficulties in Recognizing One's Own Incompetence Lead to Inflated Self-Assessments". (David Dunning)

We trust these over-confident people to run our banks, local and central government.

There is a potentially dangerous flip side to low interest rates for borrowers. That is for people taking their first loan, borrowing to the max, and being just able to meet the minimum payments on a 25 or 30 year loan. The amount able to be borrowed becomes dangerously large. It's no longer enough to simply meet the interest repayments and wait for rising prices and increased salaries to inflate away the remaining debt. Instead, after 5 or 10 years, the amount of principal owing will remain high. Equity, as a percentage of the property's value, will not increase. In short, new buyers borrowing to the max will be left treading water and not getting anywhere. It will be a long journey back. Many will not make it. Some will lose their jobs, change careers, split up in their relationships, etc., etc. These things have always happened, but their impact, during a low interest-high price regime, will be more significant.

With lower interest rates, and hence larger sums that can afford to be borrowed, the solution is for banks to reduce the length of loans from 25 - 30 years to 15 - 20 years.

Low interest rates are only good for those getting towards the end of paying back their loans. For them, interest costs become insignificant, and a lot can go into repaying principal. For those starting out, it is a different matter. Beware.

Yes, agree - if buying outside of favoured Auckland areas, buyers should realise that alongside low interest rates will be: low/zero wage increases, and low/zero capital growth in house value, so no 'shrinking' of the loan and no inflation of the house value.

Maybe consider repayments on a 15 year term basis while taking a 20/25 year loan document in case of income drop.

Mortgage Belt. You need to spend sometime out of Auckland and you will be surprised to find very good incomes. Because there are very good incomes. Lower housing costs mean people have money in their pocket.

You might also factor into your equations the possibility that Auckland is in a price bubble (note I said possibility) With a much larger downside on prices than the rest of us.

Sure, agree, I enjoy those conditions too.

Auckland or not, the old normal of mortgage rates of 9%, wage rounds of 4%, and house inflation of 7% meant a homeowners mortgage shrunk quicker relative to general wage growth and increased equity.

Yes it continues to amaze me KH, people living and working in Auckland in the same jobs, for the same employer, for the same salaries, yet living in a hovel compared to their colleagues elsewhere in many parts of the country. I've lived in Auckland, nice place, and I've lived elsewhere, but Auckland just ain't that good to make up for that life style difference, and financial risk around housing.

Actually i odnt like Auckland at all....

The commute if I had to would be like London....9 years was enough.

Seems to me pythagoras is that the issue you describe is that people are paying to much for properties and borrowing hugely to do so. So vast mortages that create a lifetime of penury.

Where I disagree is that this is a potential problem. In fact it's current problem, and in fact present in Auckland for some decades. The poverty of my peers, due to property prices was something noticable to me when I spent the the year in Auckland in 1984, over thirty years ago.

My experience is that Aucklanders are significantly shot of cash in pocketl, compared to the rest of the country.

Agree about Auckland, especially the lifetime of penury for many, and also the more modern phenomenon of renting for life for those not able to get on the property ladder.

Not sure that I would agree, as a general rule, about the rest of the country having more cash. Most of small towns I've visited have not much going on ... zombie towns, to steal a phrase from Shamubeel. If you're in a profession, where pay is the same regardless of location, e.g., health (not specialist), education, police, etc., then you'll be better off out of Auckland. Not sure the small towns would be so good for builders, plumbers, electricians, small businesses, etc., unless you can use the internet to set yourself up to work from anywhere.

Here's a new label to chew over. "Zombie Suburbs"

The US allows 30 year mortgages fixes below 4%.

The US dollar will continue strength and kiwi will push down to $0.50. It won't matter if interest rates are 0% in NZ, we are heading for one almighty recession. Gold below $1000 and USD index +100.

Interesting Jram, I'd be interested in the logic to that, and more importantly, what promised land we should all try to migrate to ?

So would I.

If we do indeed go into a world wide recession then i'd expect the money to run to the USA as its "safe".

If lower rates is the new normal, how does that effect valuations of relatively high yielding assets (worked out on Net Present Value)?

Are auckland price gains simply pricing in low future interest rates, where there 4% yields is actually considered fairly good for a relatively safe asset class?

These countries with very low interest rates, what are their property yields?

NPV takes future income and discounts it by a discount rate to make up for the fact that it's recieved in the future, normally similar to inflation.

A change in the discount rate from say 3-5% to 1-2% revalues income producing assets upward (the effect being that the yeilds then reduce, as asset price increases, to a rate more appropriate for the predicted future environment.

I'm new to this valuation metric so feel free to help me out Roger Kerr.

Just how many higher yeilding assets are there left?

Looking at

a) shares they seem hughly over-valued to me.

b) property? at least x2 a bubble.

c) bonds? lots of ppl hiding in them, blood bath on exit? (if late)

d) junk bonds? oh boy look at the shale "investors"

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.