Evidence is growing that the housing market is heading into a significant correction as it goes into its peak selling season.

Probably the most compelling evidence is the movement in the Real Estate Institute of New Zealand's House Price Index (HPI) over the last three months.

Back in November, just seven of the 28 urban districts measures by the HPI were showing a decline.

By December that number had doubled to 14.

And January's figures were even more compelling, with 23 districts showing declines and just five showing increases..

Those are the changes are from the previous month, but perhaps even more important in the January figures was the fact that the HPI was lower than it was three months previously in 18 of the 28 districts, with nine showing increases and one district (Napier) being unchanged.

And of the nine districts showing price increases over three months, five were showing decreases from the previous month.

Clearly, there is now an easing price trend and it is gaining momentum.

The REINZ HPI is one of the most reliable measures of price movements because it is comprehensive, being based on all residential sales recorded by the REINZ.

It is also a leading indicator because its data is based on sales as they become unconditional.

While other measures such as average and median prices are also useful tools, they can be skewed by the composition of sales each month.

If a greater proportion of sales activity takes place at the top end of the market it can push up average and median prices even if prices of individual properties haven't moved and vice versa.

The HPI adjusts for changes in the composition of sales each month, to give a better indication of overall price movements.

What is not known is how far prices may fall or long the correction may last, but it's off to an impressive start.

The National HPI was down by 1.5% in January after being down just 1.0% in December.

In the critical Auckland market the regional HPI was down 2.6% in January after falling 2.3% in December.

The February and March figures will be important because they are usually the busiest months of the year, after which sales start to slow again as we head towards the quieter winter months.

But evidence, such as slowing auction sales and a greater degree of buyer caution, suggests the correction has some way to run.

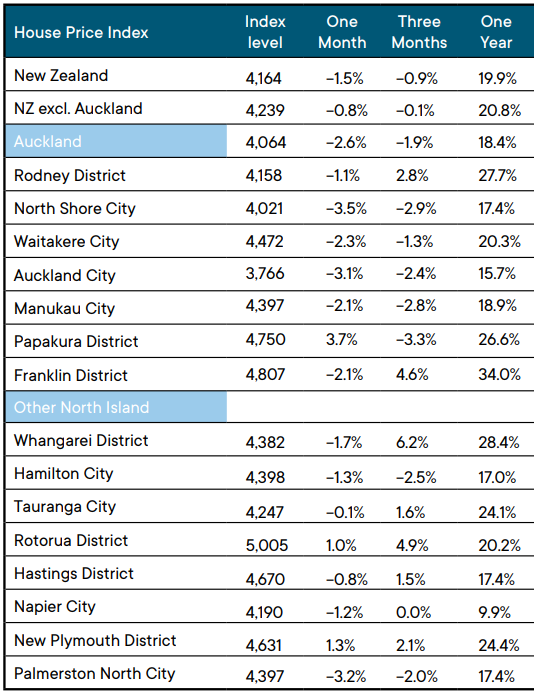

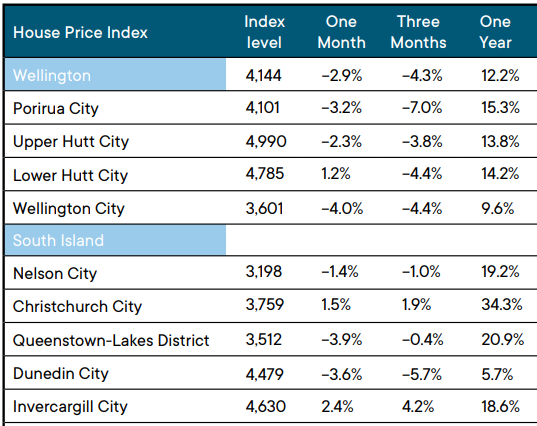

The table below shows the latest HPI figures for the main urban districts.

The comment stream on this story is now closed.

REINZ House Price Index - January 2022

183 Comments

Still room for upward valuation.

BE QUICK 🤡

Indeed. Be quick, but only if you like the smell of horse sized FOOP.

Housing market is cooling off - another soft-landing forthcoming.

TTP

LOL

No seriously.

DON'T MISS OUT!

Be quick. List now! Before interest rates rise again.

Dont be the last boomer to cash out!

there are heaps of policies that could be unwinded to save house price from decreasing by 20%.

But why?

Entitlement Mentality

It is clearly essential to unwinded policies to prevent price drops. It's what kiwis expect.

Let's form a working committee to discuss these proposals, go through consultation and enact some watered down politically convenient findings in three years time.

We aRe PuLLinG eVeRY LeVeR.

Those sorts of committees are only assembled for stuff that would reduce cost of living Brock. Whenever a housing price drop appears to be happening it's "ACT NOW, THINK LATER, F$#% THE CONSEQUENCES" by all and sundry (RBNZ/Finance teams/Banks regaling us of fantastic stories how everyone in NZ is going to be in negative equity/One Roof claiming the sky is falling etc).

The muppets at the RBNZ call this the "path of least regret".

Hello there fellow cynic.

Do not worry, head of central bank Mr Orr and Prime Minister of of our country Jacinda Arddn, who is commited to support and promote house price growth will act soon as they believe in `Least Regret' policy when it comes to promote housong pyramid ponzi being only economy in NZ and must for their political survival, only they have to portray to show that they are taking meadufes to help FHB but in reality it.........

To help FHB let the economy take its own course.

To help speculstors intervine as they will fall without government and rbnz support.

Do not be surprise if rbnz relaxes certain norm to distribute easy money or some other measures by rbnz or government to pump the ponzi, in which they are experts.

Pump, pump pump the housing Ponzi until it falls down under its own weight !!!

Can you please explain those policies? What I see is dilemma of who to save. Copying from my other post the conundrum faced by policy makers.

- If interest rates are raised to fight inflation then mortgage payments would increase leading to reduction in discretionary spending to pay for increased interest component of overleveraged mortgage payment thus affecting businesses and in-turn economy.

- Keeping interest rates low would increases inflation which affects 100% population leading to reduction in discretionary spending due to prices rise and to pay for fixed overleveraged mortgage thus affecting business and in-turn economy.

- Turning the immigration tap on to import workers to save costs for businesses by reducing wage demand will impact those who had planned on higher wages to pay their overleveraged mortgages.

If you try to save house prices then business and earners suffers. If you try to save earners then business and house prices suffer. And if you try to save businesses then earners and house prices suffer. Unless some miracle happens and inflation disappears.

If there is reduction in house value then major impact would be on the new entrants and that I guess won't be more than 10% of population.

The stars are aligning for something but not sure who would have to compromise.

The decision will be made for us.

Rates are going up. Salaries are stagnant. The amount we can borrow will come down.

Still only really affects marginal borrowers. Or those who are close to but have missed out cashing up.

Everyone in the country is already suffering due to the inflation pressure. House prices are an easy casuality.

Salaries aren't stagnant

Sure they are, how do you think we went from 3 x 1 persons income to 12 x 2 peoples income to buy a house ? Salaries in this country never keep up.

1. I'm talking about now, not the past

2. "Salaries in this country never keep up" is not the same as "stagnant"

3. Your comment relates more to the long-term downtrend in interest rates

OK. Not stagnant for many.

Sure haven't doubled over the past 7 years...

The government has caused enough harm with crap policies the market will fall and find its feet at a much affordable level. The one thing that would be good is to stop speculators from pumping up prices.

I cant see Nats would have done anything differently except raise the covid death rate...they would have targeted businesses the same, printed money the same...maybe less concessions for iwi...but theyre all using the same flawed song sheet that presumes people with lots of money have the right to make lots more...

They increased Government debt from $10b to $60b for a "North Atlantic Financial Crisis" and an earthquake which according to the RBNZ in 2015 had an estimated total rebuild cost of $40b, comprising of $32b for residential/commercial and $7b for infrastructure. As at 30 September 2015, insurers had paid out $26b (page 3 and page 5 of the PDF). While at the same time increasing GST and cutting income taxes.

https://www.rbnz.govt.nz/research-and-publications/reserve-bank-bulleti…

So yes, printing money would have been more or less the same with National.

True...back in the days where they also did away with democracy in Canterbury and replaced elected representatives with their own people.

Really.. The prices need to come down to be reasonable. The society fails when sometimes unreasonable things happen. Crime increases and social unrest gathers pace.

We are a small country, small well connected society, we do not need unreasonable things to happen around us.

Let's not be greedy and get things knocked down a bit so everyone can prosper at the same time.

No. They (whoever that is) will be in as much control on the way down as 'they' were on the way up.

And housing policy and markets play out over years and months. So even if regulatory changes are made it would still take time to play out.

You also assume 'they' don't want a general deflation...

If a downward trend kicks in (say 3 or 4 months in a row) all you know is that no one will want to pay more than the last person.

“there are heaps of policies that could be unwinded to save house price from decreasing by 20%.”

Indeed.

But please do not discuss as it is reserved for later on maybe before the election next year. Let’s just let the market take a breather for now as life slowly goes back to normal.

As the stock photo illustrates, kiwi leaky homes don't float.

One swallow does not make a summer.

Those who understood how this works makes the most money.

Nothing like watching DGM false hopes vapourised by Autumn.

Be quick!

Do you consider autumn to start on the 1st of March or 21st of March?

What does "vaporised" mean in this context?

With the price falls in December and January, further price falls in February will certainly the summer make.

You would be a very interesting subject for a sociological study.

I'm pretty certain he's a parody at this point. Like some sort of performance art.

Just as certain like you're a 46 y.o male from the North paradoxically staying in the Southern hemisphere.

I'm 30. What's paradoxical about a northerner (referring to England - not the world) being in the southern hemisphere?

Go learn a bit on England's long and colourful history and perhaps you'll get the paradox.

🤡

On the other hand, you would had already proven Joseph Goebbels' theory by subscribing only to DGM narrative.

Please don't ever leave. You're a clown but it's quite entertaining reading your nonsense.

Well, he is occasionally quite brilliant as a troll. You have to be fair and give it to him

Interest should be giving him some of that ad revenue. He keeps me coming back for more.

The trick to being brilliant as a troll is the victims not knowing they are being trolled.

When everybody knows, you're just filling the role of village idiot.

Don't you worry chap - i've found your brother from another mother so you don't have to feel alone anymore.

Love your work CWCB - keep it coming. Belly laughs all day long

Aggregated numbers tell only ever part of the story..

Some parts of the countries property market are still going up will some have certainly eased off.. real incomes and business activity are also moving for many.. its a relativity scenario...depending on your situation and what you planning to do.. nothing definitive..

RBNZ to the rescue...

An NZ Initiative economist stated that previous RBNZ analysis on wealth effect (housing Pigou effect) from higher house prices shows a +3% impact on GDP.

On the flip side, lower house prices could potentially wipe out 6% from NZ's GDP, primarily from the household consumption part of the equation.

Higher house prices shows +3% impact on GDP? What about the real GDP? If printing money and higher house prices can simply boost GDP, then why do we even need to work? RBNZ should just keep printing money every year and we just sit at home to see GDP increases 10-20% every year. Everyone is happy, simple and easy, right? ;)

If printing money and higher house prices can simply boost GDP, then why do we even need to work

How else have we gamed an economic recovery during the pandemic without the billions in foreign dollars from tourism and education?

Path to real GDP you ask - bring more migrant workers to do work Kiwis won't do, line the pockets of our monopolies and speculators by forcing them to pay ridiculous prices for basic necessities, rinse and repeat.

Probably not many other options I think, but what I know for sure is not by injecting printed money into house market. I am not against loose monetary policy during pandemic. But while housing market has been extremely hot ever since before pandemic, it's not a rocket science to figure out the negative impacts mass QE, extra low interest rate and removal of LVR could bring to our economy without any regulation to prevent money injecting into our housing market. Now RBNZ needs to correct the mistakes that they've made during the pandemic. Of course, correction comes with price and pain. There is no such thing as a free lunch!

Funny, I recall Michael Reddell conducting a lit review and is own analysis that showed the "wealth effect" was prime reserve bunk and only shifts wealth from some to others (and often from those who would have spent it to those who won't spend as much of it).

Wealth effects used to justify pumping house prices ever higher. It is junk thinking like this that undoubtedly contributes to the staff exodus from the RBNZ under Orr's tenure.

The country cannot keep borrowing against the future to fund the consumption of the investor class.

The debts will come due, and the economy will suffer. But how much we suffer is up to the likes of Orr and co.

The market will continue to sink until we get to a place where average wage earners can afford to buy a house, how far the market tumbles will depend on inflation and interest rates as they are both on way up it could be a long way down.

if the fall does reach wage earners affordability, that would be a very long way down.

Yes I agree it will go down a long way, you just can have a society where average wage earners cannot afford a place to call home for family

A middle class of size and owning home as we know them, has only been for such a short period in history.. no reason to assume it will continue.

Switzerland is a very developed society where average workers cannot afford to buy a house, most rent.

Except that the average pension in Switzerland is almost double what it is here, meaning if you’ve never bought a house you can still afford to rent when you retire. Now THAT’S a developed society. you’re basically left to rot under a bridge here once you retire with no home. You call NZ a developed society? I think not.

I'm sure the rental quality is better too, as well as tenancy security and conditions.

The bulk of Swiss pensions comes from their 2nd pillar, which is similar to kiwisaver but generally with higher contributions.

Their optional 3rd pillar allows for tax incentives to save extra for retirement. Imagine if the same was done here. (I guess you could say that NZ uses property instead)

Yes I know I lived in Zurich for a while you needed to be mega rich to buy, but rent were quite low compared to wages

For our (house price) to (household income) ratio to match that of the US (4.4), NZ house prices would have to fall by over 50%.

there is a massive tax paid for living here.

People in Auckland who do not own a house are paying huge rents house prices are well out of reach for most of them even if you are earning over NZ average wage you will need 200 k deposit it has just got out of hand. The market will have too fall 50% before you could say it’s a fair market keep speculators out of market at it will find stability. People and investors who have been fooled by FOMO will incur biggest loss, but hopefully they made a heaps on way up.

If prices were to drop 30%, and wages increase 30%, this would be a 54% fall in house prices real terms.

Could be on the cards, just take 5 or 6 years with 5% movements down and up respectively.

Short term inflation and short term rates are up but the medium and long term bond market is sayin it wont last. Growth and inflation will drop off and rates will fall once again. Credit must stay affordable and keep expanding to keep the whole world afloat. Look at the BoJ they are way ahead and where the rest of the world is heading. There was massive shock and Orr when Japan started QE and since then most advanced economies have since implemented the same "crazy" policies. Inflation will drop once the supply chain clears and by then interest rates will be higher, demand for goods will drop and so the next disinflation cycle starts. Lower rates more QE and possibly even curve control.

Central banks are making shite up as they go. None of this is chartered territory. For all you know, there is just as much chance of a complete collapse of the system, as much as MMT actually working out and us living happily there after.

If prices were to drop 30%, and wages increase 30%, this would be a 54% fall in house prices real terms.

Even if prices halved they'd still only go back to where they where less than three years ago. I only hope we've got enough of a firebreak around housing to prevent a wider recession.

If prices were to drop 50% as you suggest, NZ would be in deep poop. Far too many owners would be in negative equity, this would lead to a downwards spiral that would affect everyone, (including renters)

NZ is already in deep poop and renters are already affected.

Indeed renters are already affected with overpaying for rentals.

I hope our FHB's leveraged to infinity and beyond are familiar with bankruptcy as that will be their Obi Wan as the Housing Ponzi morph's into the Housing Zombie

The Aussie liberals (?) solution proposed seems like a better approach than the current approach of enriching the wealthy and hoping for some trickle down sometime. Use a one-off payment to each adult to help address the problem - i.e. for FHB to reduce their debt, for those without a house to be recompensed for their impoverishment at the RBNZ/govt hands over the last years, and for others to help maintain spending.

As it's per adult, not per house, it doesn't unduly bail out speculators (as has been done during the last two years).

As opposed to being enslaved to Global Banking's super profit agenda via endless rent/mortgage servicing of debt...

Let the reset happen and let those that need to go bankrupt do so just like Iceland did. It only took Iceland two years to get back into Global lending favor. We could have the Govt actually do their job and mandate a no more than 3x income for investors, and 4 x income for home owners.

You are not going to hurt our Aussie Banks, give that up its not going to happen. They may make slightly less billions and have to let go a couple of thousand NZ workers but they will survive.

Mandating ITD ratios would require us to regulate the building supply industry and probably tariff the logging industry as well, Labour and sophisticated policy actions? Tui add.

Only if forced to sell

Yeah 50% would be bad. But here's hoping for at least a 20% drop. Would help bring prices a little closer to what they were a year or two ago (yes, still very high), causes some pain - but hopefully won't wipe out buyers who have purchased a home (ie. with a medium-longer term view)

And the MSM still pumping continuing increases...

https://www.oneroof.co.nz/news/40889

They think its a given that this Grey Lynn villa will sell for more than what it did in December. Agent quoted as saying there is "new vigor" in the market

Maybe they meant the Honda Vigor.

A misnomer if ever there was one

Vigor mortis ...

Media and Banking interest probably ultimately owned by Blackrock.

Also, how delusional do you have to be to think that north of $4 mil is "a really attractive price point for families." JFC.

Oh, well only *rich* families, obviously. I mean, people who don't have $4m are hardly even people at all, are they?

It's really only for folk who have been gifted enough money by the RBNZ and govt through previous years. Salaries are comparatively meaningless.

"I reject the premise of this data"

The alternate facts of using the year's growth to mask a considerable fall

There is no point to cheer the downward bleep, the gains that happen during labor govt are huge and will never be rolled back, the market will drop 10% to 15% and then again start going up until govt see eye-watering debt which people will not be able to serve (we are not there yet).

So the damage is done and if there is a downturn then media will cry from the rooftops and they are ritght because journos bills will be taken care by B&T not by people who read the article (very small in number).

On a million dollar dump a 10% decline is $100,000. Excellent, that's a $100,000 a FHB does not have to save. There is reason to cheer. The madness and greed may actually be dissipating.

Agreed, job well done by the Government. Obviously, this is just the start. More to come. Mission complete.

Now we can start talking about anything other than housing. What other subject can we now bang on about to express our general anti-Government feelings and our hatred of being lead by a woman?

Do you hate being led by a woman?

The rest of us just hate being led by a liar.

I just hate being lead by someone who talks to us like pre-schoolers.

Nothing worse than a smiling liar

Really ? 80% of the people on here a year ago had it in for the smiling assassin, wow how things have changed.

It's possible to hold negative views of both Key and Ardern simultaneously.

@Streetwise change your name to streetidiot, I never thought of being led by a woman. She is just a human being who possesses better qualities than many of us that's why she is PM.

I hate it because of the lies, manipulation, and deceit which have been played on kiwis by labor in the last 5 years.

I thought my post might attract irrational responses from the obtuse.

I agree as well, this is a step in the right direction.

Exactly. We are so far outside affordable measures, any downward trend is something to celebrate.

This is fantastic news for everyone. Let's hope it continues.

Will Mr Orr still maintain that they have no control over house price and is not in their mandate as have been parroting Everytime when questions were being asked about ever growing house price on weekly basis ( Still he acted overnight as soon as pandemic hit and had fear that house price may fall with full intensity) or now that house price growth has stopped or even falling will he still maintain that it is not his domain or will he come out to bat for the ponzi.

Even Labour Government will panic as in ponzi it is either up or down and their is no room for stabilization and everyone knows .............

Orr is in on the housing rort. He will pump house prices - if given the chance by the Minister of Finance.

The government review of CCCFA impact will be waaaaay slower than their passing of the rules. Then they will blame the banks.

And the banks & One Roof will blame the CCCFA...

Great article Greg, thanks for the table showing regional 1 month, 3 months & 1 year % change. Maybe it could become a regular monthly table?

It's just straight out of the REINZ report. Publicly available https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2022/Residential/202201/REINZ%20Monthly%20HPI%20Report%20-%20January%202022.pdf

Thanks realterms, (I'm aware of it but I thought it would help others who don't have access to the REINZ report)

We have been publishing this HPI table every month for well over a year now. Usually on the day after the REINZ releases its monthly sales data.

It is true that the REINZ HPI are the only property statistics worth giving credence to. The latest stats unequivocally tell us that the decline in residential property prices has started. And migration is now in negative territory.

Job done! Let's now swallow our pride, put away our impatience, and celebrate the Government for taking all the steps they could have taken to achieve what most thought would be impossible.

Would you rather have had the National party in charge?

Who is National you may well ask? Well, it's that party led by Christopher Luxon, a proclaimed Christian, who has as his mentor John Key, a former National prime minister who recently formed a residential property development company with former successful brothel and strip club owners the Chow brothers. (source: yesterday's online Herald but does not seem to appear today....too controversial for the Right Wing Rag?)

The world moves in mysterious ways.

Yes I would rather have National in charge, or even much better, Act

The bottom line preventing me voting ACT is their pro immigration policy.

I am having doubts Luxon is up to it. He started to crumble when being interrogated by Suzy Ferguson on RNZ this morning. Though she was quite rude.

She did seem to have her hackles up, but Luxon did seem to have a couple of inconsistencies in his lines. But perhaps what was laughable were his responses around Cameron Slater. Knows nothing about the guy? Ha - give me a break.

ACT emphasizes the benefits of immigration and like the autobahns in Germany have no stated limit. But in general ACT puts hard cash ahead of the intangible factors. For immigration these factors both +ve & -ve include reducing social cohesion, reduced incentives to train Kiwis, economic diversity bonus, low-wage rorts unfair to honest businesses, diluting Treaty guilt. A hard-headed accounting for the many costs imposed by migrants (sewers, houses, roads and light rail, medical staff & hospitals, teachers and schools, superannuation costs, judges & law courts, etc) ought to focus an ACT govt on high-paid, highly-taxed immigrants. NZ has little to worry about if the next million immigrants while paying above average income tax also build their own homes and deposit $500k for their eventual medical & superannuation benefits.

ACT are a better bet than the party I voted for because they said they would tackle immigration: Labour.

I’m willing to put my vote behind ACT next elections. Having voted labour last two elections, I have finally seen the light. A move away from both National and Labour is necessary imho.

How can she interrogate anybody,you can't understand her.Bring back Plunkett or Robinson.

Yeah, not a huge fan of Ferguson. Plunkett - no thanks!

I don't rate anyone on Radio NZ other than the mighty Kim Hill.

Indeed, how Kim Hill survives at Radio Red I will never know but bless her for attempting to keep to her fuddy duddy values.

National are all in on the housing rort.

In your ode to the current Govt you mysteriously omitted to mention that the recent unprecedented run up in property prices happened on their watch. You suggest that we should be praising them to giving us smelling salts .. after they broke our legs.

We would still have the problem under National or Act - but we would not have nearly the same size of the problem.

paashass

You are probably too young to remember but it was the Key National Government that opened the door to untrammelled mainly unskilled immigration that created the need for more housing which in turn pushed the price of houses up.

You make too many wrong assumptions - including one about my age .

You can write as much blah-blah about JK's govt as you like ( I was not a great fan either BTW ) - but the numbers do not lie; just compare house price growth under him and under JA.

The latest , unprecedented spike is on her / Orr - trying to pin it on JK via the "untrammeled immigration" is just hilarious ( we had no immigration over the last 2 years .. and yet we had the mother of all property price spikes )

passhass

Can I take a punt and call you out as an unskilled immigrant?

Ha .. you really could not have made a worse assumption - again - shows the general quality of your reckons .

I am an immigrant , with a PhD , working in a high-tech field utilizing that degree ; if that is "unskilled" to you I have to disagree..

Mic' drop....

Had you figured out how to count or replicate their index to make that your conclusion?

There're more indexes for housing than I can count. Even Wheeler had formulated one.

Just a side note, the Labour shilling is cringy.

It's "indices". Though I'm sure as an expert in both fuzzy logic and quantum mechanics you know that.

The core reason for dropping house prices is INFLATION. The RBNZ can no longer ignore inflation and has to act, (I wouldn't be surprised if they raised by 0.5% next week). Higher interest rates at a time of record high mortgages will seriously hurt. Add the higher cost of living, the end of free government money in the form of Covid subsidies (this is majorly underestimated in my view) and it's clear a lot of Kiwis are going to reduce their spending significantly. This in turn means less people at restaurants, clothing shops, other retail shops, all these businesses that have already suffered a lot in 2021 but won't get government help anymore. Quite a few of these businesses will close which, of course, means that people working there will lose their jobs. These people will stop spending altogether. I see the second half of 2022 in NZ as a real mess

Could get interesting.

One other thing people don't talk about is the opening of borders. When people are locked in house & country of course people will want more space and housing becomes a focus.

Once all these people are allowed to leave NZ, all of a sudden the daily focuse on our homes will become less intense..

Just a thought.

Well put

I know the likes of homes.co.nz is basically nonsense, but it is interesting comparing Homes.co.nz stats of "capital growth" in Auckland over the last 12 months (35ish%) to the 12 month HPI figure of 18%.. that's quite a difference

Homes.co was started, owned and run by a couple of private entrepreneurs whose sole purpose is to attract the advertising revenue on their site from both real estate agents and their vendors.

NOTE: Homes.co has recently been acquired by Trademe. There is now a direct link to Homes.co on the Trademe property site. So, you now have the option of looking up a property's estimated value on the same site i.e. Trademe. And thus you have the choice of the slightly undervaluing (Trademe) or the stratospherically high stars-in-your-eyes value (Homes.co). I have found that the respective value estimates of these two sites can be hundreds of thousand dollars apart for the same property. This situation makes a mockery of these 'value-estimating sites in general.

I have found the most reliable valuation is probably the government state owned qv.co.nz whose values sit in between Trademe and Homes.

The other sites in this field are Oneroof.co and Realestate.co, both of which require you to 'log in' for their estimates. This is obviously a ploy to pass on your contact details to real estate agents.

Coincidentally, yet another house price estimate site was announced on TV 3s "The Project" tonight. It's called HousePrice.co.nz. They built up the company on TV but at the end of the day this company just wants you to 'sign in' so they can pass on your contact details as a possible vendor to a property valuation expert (read real estate agent) who purports to give you the real value of your house. Remember it's the vendor who pays the agent, not the purchaser. This site is no different from One Roof or Realestate.co.nz. They must think vendors are stupid.

Apparently, Trade Me are upset at this new company encroaching on their turf. I don't see why they would be but then again they have just acquired Home.co (presumably at a price) so they are probably upset at seeing another competitor freely entering this market just when the market is slowing.

Personally, I still think the state site (qv.co.nz) is the most accurate site. They freely give you a valuation for any property with no strings attached but can also offer something approaching a written appraisal at a very reasonable price.

(I have been closely following these sites for some time and comparing their estimates with actual sales prices.)

.

Creating even more room for upward valuation

Be .....

FOOPed in your pants...

Help me here. Fear of... O ... P ... or something else entirely. 2nd time I've seen FOOP today. Still no idea.

Fear of over paying.

Martin North from DFA did an interesting piece about a year ago on his analysis of the effect of the availability of credit on price. His sensitivity analysis showed it outweighing other price factors substantially.

The CCCFA and Interest rates going up will reduce the availability of credit and therefore house prices will go down by this logic.

A crash is not impossible but could be slowed by reversing some of the credit restrictions again. I think a crash would require a surplus on the supply side and there will be a natural control factor there caused by peoples existing equity position. Only the desperate (estate and divorcing couples) will sell below their equity positions.

You do realise he had a stellar record of predicting property crash right?

Yes you are quite right I should have ignored his analysis of the data. Or do you have something useful to add?

The corolation between credit availability and house prices/other factors is quite interesting.

The last 10 years have seen debates rage re migration, supply, Covid etc, but when you isolate the data and put in on a graph, the only tight corolation over the past 20 years is credit growth.

Mr North calls this out, says when credit slumps so will housing. But he's not in control of setting interest rates.

It’s interesting. The majority of people I speak to (NZers), still believe that property cannot and will not come down. Apparently the influx of immigrants will save the day and drive prices higher. Either I am deluded, or they are. I guess the next few months will decide that.

I’m picking 2-3% slide per month until inflation is brought under control.

Many spent to much time at school learning Te Reo instead of time learning Te Maths.

Brock where is your Aroha?

Comrade, your comments are not very kind. I am reporting you to the authorities. Who will spray water on you.

Its called fuzzy logic in quantum mechanics and it's application in computing has the potential to change the world.

You are right when you see anything with a negative sign but wrong at the same time to consider the positive one right next to it. The same applies to the people whom you speak to who were wrong because they didn't see the negative number you had in your mind but are right when the valuators confirmed that their properties has risen in value.

There you have it, it's quantum.

There's still room for upward valuation.

Fuzzy logic has nothing to do with quantum mechanics. Your ramblings only make sense to those with unsound minds.

Yes it does.

https://link.springer.com/chapter/10.1007/978-3-540-93802-6_20

Perhaps you'll find a better paying IT job if you upgrade yourself to be as good as my Indian computer boy.

So besides exposing that you know very little about computer science or mathematics, you now want to reveal that you also can't read? At least beyond the title of what you desperately tried to find on Google.

You'd think that somebody of your advanced years would have learned by now that when you find yourself in a hole, the first thing to do is stop digging.

Not just you proved my point but funny at that.

🤡🤡🤡

CWBW now over 28000 house for sale on trademe why would you need a computer boy when you work off a phone.by the way your job titles just confirms you are a one man band and you live in a fantasy world and your main worker would be Siri.

I thought fuzzy logic died in the 80s along with permanent waves

Soooo the reason why globally increasing rates won't pull nz property prices down is because.

A) quantum physics

B) your Indian computer boy

Bahahahah - thank you for a wonderful day CWBW

Yeah the cognitive dissonance between the data and the opinion is interesting, how far the slide will go is even more interesting, I am picking a steeper fall through winter as the tipping point becomes too obvious to sweep under the carpet and people go full FONGO on it.

It's hilarious how on edge people get over the slightest decrease...

The only ones on edge are the dreamers.

Those who already bought doesn't care about meaningless seasonal volatility.

CWBW after a while of seasonal drops and people are in negative equity this will put people a bit on edge. Maybe you could start up a counselling service for all the people in huge financial trouble after listening to you and your sole trader business.

Jokes aside, we did receive presents from our buyers over the last Christmas for selling them their current beloved home.

On the other hand we received nothing from renters. Goes a long way and speaks volumes about the renters' mentality.

CWBW,Perhaps the renters couldn't afford to buy you a present,probably used the money for frivolous things like food for the kids...selfish b*stards...

Did you give Christmas presents to the renters?

Yes, every one gets a bottle except the the Muslim whom we substitute it with a large box of premium dates.

See, we are nice people.

I wouldn’t stay around for to long as them buyers will soon be loosing deposit and be in negative equity so might need gift back.

I personally wouldn't expect anything from the renters except the rent paid on time and the place kept tidy.

What did you give them?

He gave them a roof over their head, he is doings God's work without any thanks...

Wow, such disdain for your customers.

That's like thanking the supermarket for feeding you

So the prices drop by 10%, would you be happy?

How far a drop do you think its fair

Then imagine once you are in the ladder, how much increase would you like?

Until the majority of the working people of NZ can afford a home. Sound about right John?

New Zealand total mortgage debt is 327 billion as of Dec 2021. Add a measly 1% rate increase on that and you get 3.2 billion. That is 3.2 billion of potential spending that is removed from the system at the same time that inflation is running at 5% plus. Average Household is paying another $20 per week for food and $15 for gas than they were last year. Same food and same gas. Just costs more. Young Auckland family that has just refixed a 500k mortgage off a 2020 rate is probably at least combined 7k worse off net than than they were last year. So they would need a pre tax 10k salary increase just to stand still.

Not much on market in Auckland for young family under a million how long have they been in house.if they have 500k equity just sell go and rent will be able to buy back house for half price in one or two years.

And whose mistake is that?

If people have been unintelligent in spreading themselves very thin and not thinking about the future, then pay the consequences.

There is no pill for stupidity in the market.

It's funny, people on here wishing misery for home owners, speculators, investors and first home buyers. I own 2 properties and have taken a page out of Warren Buffet's book...

Buffet: "I love when the sharemarket drops, companies that I was going to buy anyway just became cheaper".

The outtake here is there will be solid opportunities for the shrude buyers in a declining market. If accumulation is your goal, this is great news.

I for one will be ready to pounce on more good properties when the prices come down.

Hey diyguy

hope the bank is as confident in your plan when that time comes!

My point is, if you never plan to sell (or at least not for a few decades) and only accumulate.. then a drop is ideal. Easier to buy more properties, better yield etc.

Greedy much?

None has ever been able to spend all they store. It either rots or rats eat it.

But yeah we all do like to accommodate for that day. But never realize that the day it today itself. No one knows the future.

I have no idea what you're trying to say. Suggest not trying to communicate through metaphors.

What you're suggesting is simple investment logic. When you're in the accumulation phase, better for prices to be low so you can acquire more assets. Sensible.

The likely difference between shares and houses is leverage. Generally a 50% fall in shares means your portfolio halves in value. A 50% fall in property prices might mean your portfolio going to zero or lower, making it difficult to keep buying. So great in theory, but if you have large mortgages already, very difficult in practice.

NZ's real estate bubble is perilously close to popping in the wake of the pandemic.

Imhao the world is on the brink of an economic bust, and financial asset bubbles need to and will come down to reality.

Your house could go down by a lot more than you think.

Welcome to La La land. Let the party go on. Published asking prices should keep the housing ponzii going. But keep the lid on actual asking prices which may be way lower

https://www.stuff.co.nz/business/industries/127775543/trade-me-sends-wa…

As a property valuer, I welcome this turn in the market, although it is long overdue. Unfortunately successive governments have indeed manipulated conditions to keep the market moving upwards, and have shown no concern for affordability issues confronting an ever growing number of potential buyers. I cannot see myself voting for National or Labour again as they have betrayed hard working kiwis. I purchased my first home with 20% deposit at the age of 21, on a modest office workers salary at the time. The property was 5 times my annual salary. That same property is now 12 times my current valuer salary. Sadly NZ is not the place for low income workers to live any more and it could have been prevented. The market needs to fall more than 40% to begin to start looking affordable again, but of course the Govt wont let that happen

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.