The number of residential properties being auctioned by Barfoot & Thompson continues to steadily decline each week as we move further into autumn, but the overall sales rate has been remarkably stable for the last three weeks.

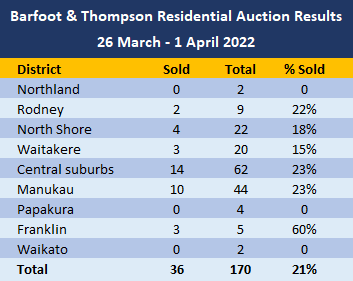

Auckland's biggest real estate agency marketed 170 residential properties for sale by auction in the week from March 26 to April 1, down from 201 the previous week and 181 the week before that.

Of the 170 properties offered last week, sales were achieved at auction on 36, giving an overall sales rate of 21%.

That was the third week in a row that the auction sales rate has been either 21% or 22%.

Around the main Auckland auctions the sales rates ranged from 15% for Waitakere properties to 23% for properties in Manukau and Auckland's central suburbs.

However none of the Papakura properties offered sold under the hammer while those in Franklin had a 60% sales rate, although the number of auctioned properties in both districts was small. - see the table below for the district-by-district sales results.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

153 Comments

The first property on the list is an 80-square-metre bungalow in Karori, Wellington, with two bedrooms, one bathroom, asking for offers above $795,000.

The home may be close to public transport, schools and shops, but it is listed at a large reduction compared to the Quotable Values (QV) estimate of $910,000

The Homes.co.nz HomesEstimate on this Parkvale Rd property in Karori sits at $950,000.

Thats -12.% with QV 0r -16% with Homes.co.nz

The second property to make the list is a four-bedroom home in Miramar, Wellington at offers above $950,000.

Despite having a separate laundry and a large dining room and kitchen, the property is listed well below its QV estimate of $1.21m.

The Homes.co.nz HomesEstimate on this Miramar property on Broadway is $1.28 million

-21% with Q.V or 25% with Homes.NZ ( this is CRASH Territory )

There are bigger reductions still in the capital. Currently advertised on Trade Me is a three-bedroom Melrose property on Dunedin Terrace inquiries above $695,000, $425,000 below the QV estimate.

-38% ( CRASH Territory )

An example is this cedar and plaster four-bedroom home on Mt Albert Rd in Mt Roskill, Auckland on the market for $865,000, $285,000 lower than the QV estimate of $1.15m.

-24% ( CRASH Territory )

7% interest rates this year Guaranteed . -30% Crash in Home Prices this year is a Certainty .

But wait, property expert Ashley Church says this is a temporary ‘confidence’ thing and the market will be humming in just a few weeks time!!!

The Church also advises that people cut their cloth and find an extra 40k gross income per annum to ride out unaffordability issues from increased debt servicing costs… if they bought on his advice that interest rates would never go up from emergency levels.

maybe The Church was caught in an Unguarded Moment?

The Church of Ashes .

Amazing play on words, what talent! Did you come up with that one all by yourself?

Hahah.... Yvil has your number.... 2022. F***ken laughing at my own weird joke

Take a Chill Pill Yvil . I also came up with that by myself. https://www.youtube.com/watch?v=WRK03q76GKU

Oh, you're still a child, I didn't realise you had the maturity of a 5 year old, I do now.

Why do you copy and paste the same comments everywhere?

I wonder the same thing. It's like listening to the Briscoes lady.

Hi nktokyo - The posts are different. I understand you may be feeling a little worried NZ may become like your country.

There are more than 8 million empty homes in rural Japan, and local governments are selling them for as little as $500 in a bid to lure residents

https://www.insider.com/japanese-government-selling-rural-homes-cheap-a…

I know. The government has a xenophobic immigration policy, which coupled with a highly educated, high-cost society has led to a critically low birthrate for decades, and here we are.

More so than Auckland, Wellington has had some significant house price corrections in the past.

I think it was 03/04 when my parents were selling their house, I think there was a slump of 10-20%

By the same token I remember watching a home Reno program in early 2000s, all Auckland. I was shocked at the time as some had bought houses 10 years or more previous and the current valuations were about the same. Totally dead. I also remember the series as it revolved around trying to up the value by more than a Reno spend. Every single one failed to increase despite the employing of lots of advicing experts. Most created a good look that no one could actually live in

I fail to believe a word you are saying red. the program you are talking about sounds like My First Home and I know they added value to the houses. Goodness me you must be feeling off-colour with a bit of the Omicron

Hi MouseHouse,

Note that in Wellington, upward price corrections have far outweighed downward price corrections over the last decade.

If you own a good 3/4brm family house in Wellington, it’s like gold. They’re often sold before they get on the open market.

TTP

The headline says "Auckland auctions", you're stating properties in Wellington. Are you saying Interest's claim that these B&T auctions are for Auckland, is wrong?

Yvil -

An example is this cedar and plaster four-bedroom home on Mt Albert Rd in Mt Roskill, Auckland on the market for $865,000, $285,000 lower than the QV estimate of $1.15m.

-24% ( CRASH Territory )

7% interest rates this year Guaranteed . -30% Crash in Home Prices this year is a Certainty .

You can't draw any conclusions when the price says "offers above". It's just BS, RE malarkey and deception. A long time ago when I had two small children and was a bit desperate for a home I saw a place advertised for offers above 260k. I really wanted it so offered 290k and didn't get it. I was sure I'd get it for that. When the agent came back urging me to offer more I couldn't bring myself to do it.

Zachary Smith - People are clearly offering less than more now that the tide has turned. So actually those price CRASH numbers in my original post are very modest.

2022, what's the point of your posts? Are you trying to support your "30% crash, sorry CRASH" by hand picking some properties that havn't sold but have higher RVs than asking price? Is that your point?

Yvil - The Media are Revealing these properties to the public, not me, but if you know of any more can you please post them. The point is to obviously show the big percentage decreases going on out there. Are these numbers making you unhappy ? we can talk about it Yvil. Do you own property ?

The "prices" in that article are all "offers above". Just not very compelling.

2022 is a crazy, lazy DGM.

Ignore her.

TTP

Tim Mordaunt and his 4 fake accounts. So predictable. Come on Yvil, make it 5.

Is that you retired-poppy... back from retirement??.?

.

Yvil, these are great examples of decisions sellers have made based on the broader market conditions they are trying to sell in. Are you saying that these sellers are uniquely reducing their expectations out of generosity and not out of reluctance and acceptance of a changing market. Is that your point?

That seems a bit fanciful.

That's not at all what I'm saying, far fetched to come to that conclusion. I'm saying what I'm saying, the article is about Auckland but 2022 comments about Wellington

Yvil -

An example is this cedar and plaster four-bedroom home on Mt Albert Rd in Mt Roskill, Auckland on the market for $865,000, $285,000 lower than the QV estimate of $1.15m.

-24% ( CRASH Territory )

7% interest rates this year Guaranteed . -30% Crash in Home Prices this year is a Certainty .

Actually I am finding it very interesting and very hopeful. Long may it continue.

Ye gods, you're like CWBW but in the other direction.

These are uncertain times. Nothing is guaranteed.

Its Guaranteed that the pendulum swings.

Your just cherry picking 2022. That house in Mt Roskill is a monoclad house, nobody will touch one with a barge pole its worth the land value +10% because it will be a demo job down the track. RV's are handed out sight unseen, the house could be a major leaker its still going to get the same RV.

It is not advertised as a "major leaker". Are your feeling sad Carlos67 ? Are your eyes major leaking ? The market is tanking, some properties are CRASHING, this is what happens when the Bubble Bursts. You cannot stop this Carlos67, its the pendulum swinging. People in denial always go through a grieving process once they can see they can no longer deny reality. Its OK Carlos67, let it out, major leak those eyes.

Mt Roskill Home for sale cheap. "just a little deferred maintenance from years of neglect, in fact if you're keen you could reclad the entire house, I am sure you could do it cheap, and by the way there isn't much road noise down here in the gully" this house is wunderbar.

A real steal.

Yvil, you don't mention anything about cities in your comment (Although 2022 did provide an Auckland example). You undermine the idea that a crash can happen and accuse 2022 of cherry picking data. If you believe these examples are "hand picked" then you believe they're not indicative of the broader market. So you're in essence saying these are just outliers and that asking prices aren't falling.

"Yvil, you don't mention anything about cities in your comment"

Yes I did:

by Yvil | 2nd Apr 22, 8:28am

The headline says "Auckland auctions", you're stating properties in Wellington. Are you saying Interest's claim that these B&T auctions are for Auckland, is wrong?

Yvil when a DGM ignores the discussion and goes on their own tangent, you know they are back pedalling.... but please excuse my stating the obvious to those seriously lacking commenters

You can do better than that. That probably won’t even get you banned again.

Wow how about that

Hi Yvil,

I’m referring to this comment specifically where you attempt to ignore real life examples of real people lowering their expectations drastically. I discuss your point regarding cities in a comment just below.

by Yvil | 2nd Apr 22, 10:19am

2022, what's the point of your posts? Are you trying to support your "30% crash, sorry CRASH" by hand picking some properties that havn't sold but have higher RVs than asking price? Is that your point?

Yvil, are you saying that property prices in this small country aren’t linked? what did we observe on the way up. Aucklanders will sell their investment properties in the regions first causing prices to fall causing Auckland property prices to adjust to the competitive affordability in the regions.

It’s the reverse halo effect. This is how property ponzi spirituality works.

At this point it'd be easier if there was a "list your market correction and interest rate predictions" page on the site, save a lot of space.

I spose for anyone under about 40, numbers going in opposite directions must seem end of the world stuff.

Most people under 40 think it's fantastic.

It'll be neither.

For most of those under 40 watching the New Zealand housing bubble implode under the weight of it's own stupidity will be nirvana.

It's not a matter of age BL, it's a matter of whether the person owns a house and how much mortgage they have on it. Mostly the only worried people will be the small minority who bought a house in 2021 with a very large mortgage.

At the other end of the ledger, there are the people who don't own a house and who are cheering on a crash, sorry CRASH, so that they can get a bargain at the expense of the poor few sods who have to sell

I'm well under 40 and have a mortgage >$1million. I hope there is a crash.

You must be in a good financial position, well done. How long have you owned said property?

I am. About 4 months. Obviously a bit miffed to have bought at the peak, but standing on the sidelines for 10 years was getting me nowhere.

The societal benefit of a significant price correction far outweighs the long-term consequences of the alternative, in my opinion.

So you're saying you stood on the sidelines for 10 years, then bought at the peak and you are now happy to lose hundreds of thousands of dollars, and possibly your house for the greater benefit. You are truly an amazing selfless person... or maybe you are just full of it ?

Yvil

Is that whats going to happen Yvil ? Are people going to lose hundreds of thousands of dollars ? And possibly lose their homes ?

Maybe he won't lose thousands as he will stay in the house for 20 years, and can afford the payments. While NZ returns to affordable housing for people less fortunate.

I remember having a discussion with a relative in 2011 or 2012 about buying a house. He was adamant that I do it ASAP, whilst I was of the opinion, even then, that the market was overpriced. Fast-forward 5 years and things are even worse: surely a correction is imminent? Then I moved overseas for work. I returned to NZ during the very early stages of the pandemic (pre-lockdown), a time when all logic suggested that the housing bubble, and it is a bubble, was ready to burst. Enter the RBNZ and our government, who made it pretty damn clear to all that they would do everything in their power to prevent what needed to happen. All the while my partner and I were looking for somewhere to buy. Our conditional offer was accepted not long after the "transient" inflation was announced. The rest is history.

Our combined income is high enough that if we ever reached the point that we lost the house then the whole country would be underwater and there would be extreme social unrest. That doesn't make me selfless, just lucky to be in the position that I am in.

Is that true Yvil? Are you saying house prices are going to "crash, sorry CRASH" buy at least 20%‽

… … . …. ……..

Wish I could say I'm well under 40. Other people can have the millions I will take the age.

Hi Yvil,

Yes, that's correct, but we were postulating about whether the cohort of under 40s will think it is fantastic.

You will find, when you think about it, that mostly people under 40 will.

Indeed. Taking the advice of charlatans such as TTP, Printer8, 🤡WBW and their ilk was an extremely risky thing to do.

There is a lot of worry ahead for some.

Not quite. There will also be a significant number who bought before 2021 but who have released equity rather than pay down their mortgage. They will also be worried.

People don't necessarily want bargains. They just want affordability aligned to salaries so they can buy a house and live in it, raise a family, have a dog and basically get on with life and not think about housing so much. That's what the property investor obsessives don't understand.

Agreed.

Yvil.

A correction of say 40% is not a crash. Its a correction.

And if it happens people will not be picking up bargains, so much as homes to grow families at prices that are more reasonably in line with salaries and long term averages.

Our current price to income ratios are off the chart and only supported via massive credit creation.

One theory is Nirvana is attained via shedding yourself of all attachments and living a life of austerity, so you may very well be right!

Boom shanka

Younger people being shat on, what’s new?

How is this mentality working out for you Northman?

Life's fine.

Pa1nter: "At this point it'd be easier if there was a "list your market correction and interest rate predictions" page on the site, save a lot of space"

Haha, great post, the comments on any housing related articles are always the most tedious

I only see you comment on housing articles. There’s plenty of non housing articles of interest on this website.

Check today's weekend briefing then

"I only see you comment on housing articles."

That is because only economy in NZ is housing - your observation is confirmation of the same.

HouseMouse

What is your point?

"Yvil: only see you comment on housing articles. There’s plenty of non housing articles of interest on this website".

Are you the controller as to what people can comment on? So what if Yvil has an interest in property, has experience and contributes sound comments. Clearly he doesn't consider himself an expert on everything . . . something you may want to think about as you really don't like be reminded of many of your pontifications.

So, the point of your post?

Cheers :)

Ah, the Master of Misrepresentation is back!

as I said before I am not going to engage with you anymore. Since you keep misrepresenting my position so significantly. Sick of it.

good bye and Good Night.

The policies of this site are designed to maximize page loads and thus ad impressions.

I don't think they will take any heed of your advice.

Let's see how leverage works both ways...

I don't get these estimated values in QV and Homes. If there is an asking price that is the value.

Do they not update the estimated value to reflect the asking price because the algorithm would then reduce the price of all the other properties in the area?

It looks as though developers, landlords and speculators are out of the market but people buying family homes are still in to some extent. Do the stronger Franklin sales also show a move out of the city as home working increases? As someone married to a Westie, Waitakere is not the place it was. Lots of Westies have headed south to Franklin.

Stronger Franklin sales? There was 3 houses sold?

Yip. That's my neck of the woods. Lifestyle properties in saught after areas do well, everything else, not so much. Plenty of recent examples of houses passed in at auction, listed with a price, price significantly reduced before eventual sale. REAs I've spoken to are either worthy of an Oscar, in serous denial, or plain stupid.

Actually Im from Franklin, its funny I've been away for many years, but its feeling a lot better nowadays, maybe just different then inner city living, and fresh eyes.

Pace of life is great with the beaches. But 3 sales out of 5 is not many, I've been watching the Waiuku area and Clarks Beach, and not much movement for houses lately. House prices here are nuts needs to drop about 20- 30% at least, hopefully continues being slow.

Perhaps Franklin was slower to go up but has peaked a little later than Auckland proper and is now heading the same way. Papakura and Waitakere seemed to dive a little earlier.

Why do people sell with B&T - are their fees cheaper? Surely seeing their auction results would be enough to put you off. Watching a few auctions of B&T and they're shocking...seems like zero care or strategy put in to sell the property, especially if you compare to other agencies. Anyone notice the same thing?

lots of people choose agents getting recent good sales done, b and t have a lot of agents. All agents negotiate to get listings most do 2%

Things fairly stable then?

Dreadful clearance rate, the standoff between buyers and sellers continues

It's the old game of who will "Blink" first

True, but I'd say it depends on which bank blinks first. When they start with even tighter lending criteria and then the odd forced sale they then reset the market.

That's not the case.

Buyers cannot afford what sellers ask, and banks will not give that money to them.

Buyers cannot blink, most of them at least.

Sellers must decide to sell now or to wait.

Waiting is a dangerous game now. In few months OCR will be even higher.

They might hope in a removal of LVR or in removal of interest deducibility, but still there are so many new houses coming in the market and so little new people.

Again, is stupidly dangerous anyways.

Wise ones are just getting the best offer, taking home what is still a good amount of plus, for now, and passing the hot potato to somebody else.

Every other time the RBNZ / governments have ridden to the rescue. Lower rates, etc.

Indeed. Its who can borrow the money vs want. The bubble is built on false promises of cheap debt from the low rate parachute of the last ten years. Times a changing. Inflation exploding and no options left unless we go to -5% rates.

Reset is back towards pricing of 10 years ago.

I stocked up on Popcorn at 2%...

What a shocker.

Stable around 21% also stable around 79% did not sale. Not looking good for housing market the sale is on discounts for all.

.

Thats enough out of you chebbo !

The headline "Barfoot & Thompson's auction sales rate steady at 21%-22% for the last three weeks" is like saying that government's child is finally steady with his result as has been constantly failing badly for last three years.

OR

The headline could be " Barfoot & Thompson' auction sale result constantly failing for last three years - trend seems to be disaster"

You can smell the paper cap gains evaporating. Spec crowd is torn between hitting the ejector seat and paying income tax, or waiting the mandatory 10 years for free gains while riding out the pressure of increasing interest rates.

Which will be the biggest looser?

There are parties that have a policy of taxation on unrealised capital gains. How would this work in today’s market? Who decides what equity remains as prices fall?

Interesting, would one then also get a tax refund for capital losses, i.e. when house values reduce, like in general tax law?

Impossible to fairly estimate unrealised capital as the policy itself directly affects this.

Your post is a bit contradictory, if there is no capital gain, then there is no tax to pay.

There can still be capital gain over the purchase price, it is just being eroded over time. TOPs policy is to tax home owners on the difference between the council CV and the money owed to the bank on an ongoing basis, not at sale. In a rapidly falling market, homeowners would be taxed on equity that no longer exists.

That TOP policy seems too stupid to be taken seriously.

https://www.top.org.nz/property_tax

Here is the policy. It seems to be based on an assumption that property always increases in value and that first home owners somehow benefit from unrealised capital gain.

So the 'good' spin on this is when you are at the bottom of the barrel you can't fall further, therefore is stable.

Desperation starting to show in the housing market.. 3 consecutive weeks of approximately 80% failure rate is putting pressure on existing/ new houses coming onto the market..

Reminded of and 80s song.

Hold tight

Wait 'til the party's over

Hold tight

We're in for nasty weather

There has got to be a way

Burning down the house

stop with it dude you're sounding like a talking head

Which part of that song touched your sensitive side?

How many houses have you got to offload?

Woosh...

Talking Heads is indeed the band.

Ooo I liked

"What about the time?

You were rollin' over

Fall on your face

You must be having fun

Walk lightly

Think of a time

You'd best believe

This thing is real"

Same artist.

It looks like trademe has stopped to report the number of property in the market.

(Showing 32,000+ results)

Homes & Real Estate For Sale | Trade Me Property

Is there an other way to see the total ?

32759

add up the subtotals

Has anyone emailed Trade Me why they will not report numbers past 32K ?

There has been reports in Australia that Corlogic has not been able to give out numbers on the decrease in Values in some cities. Apparently they are having some type of malfunction. Yet it seemed to be working fine on the way up, oh well, maybe these things happen.

Pretty sure the had a tech limitation to only return 32k results at once. This happened back in the GFC as well.

16 bit integer only allows for +32k.

Nobody is using a 16 bit integer for anything in 2022.

I wouldn’t rule it out, having met new dev hires there who were …alarmed by what they saw.

TradeMe are still listing North Shore as North Shore City - i mean how long has the Supercity been a thing?!

The Trademe price bands for Resi property goes to 10M but for commercial property, farms etc they have a maximum of 2M. 2M does not buy much yet you cannot search separately for commercial property above that level. That might have been ok when TradeMe was just starting out 20 years ago

You're right, it's probably just the default SQL row limit setting of 32000.

And to think 22 years ago those old computers seemed to get through Y2K. Im sure a calculator from the 2 Dollar Shop could get past 32K.

Glitch in the matrix

Think Ray White were 190 something at about 40% clearance rate. Old BT have never been known for strong auctions in a slowing market, I'm guessing Harcourts are similar to Ray White? Be interested to see the comparison between them all

Seems crazy that anyone would go with Barfoot over Ray White if Ray White has double the auction success rate in the same market. What do you put that down to?

Just looking at the Ray White results, the 41% are national results with 74 passed in and 51 sold under the hammer which is 41%. Although there were 38 changed to deadline treaty. That seems an extraordinary high number of people who where intending to go to auction but then changed to deadline treaty. Is it likely that these didn’t go to auction because nobody registered for the auctions? Hopefully someone from the industry can clarify.

Yea if you look Harcourts and others are stronger. Barfoot have never impressed me. Same BS lines we are the biggest and have all the buyers haha. You mean trade me has and you answer the phone. Still, I'm not seeing this "crash" that some extreme keyboard warriors are talking of. Slow Dow 100%, falling market over the next 3 months or so.... Most likely. Either way all the crap talk on here means absolutely nothing, market will do what it always has and always will.

Actually you are not wrong, but I feel that you don't understand what you are referring to.

The market will just work his way, right.

It will exceed to the left or to the right, to the top or to the bottom, finding and losing equilibrium points again and again and again.

Govts and banks don't like free market so they try to control it, usually failing, and making it even more excessive.

Markets are what is needed in conditions of scarce resources and virtually infinite needs, so that the correct distribution is "eventually" found. It works by encouraging the production of the scarce good, or finding alternatives, so that (again "eventually") resources are less scarce and needs are less infinite.

Home used to be scarce and money used to be abundant.

Now the inverse is happening.

I am not sure why you and some other guys play with the semantic of what a crash is. I don't like meaningless labels.

My prediction is at least -36.5% in real terms circa from the top by June 2023 (you can write it down and claim how stupid I was if I am wrong)

I will be definitely right or wrong, with no ambiguities, and my bet is crystal clear.

You can call it a crash, a correction, an error of the gods, whatever.

Give me your prediction and call it how you prefer.

you can write it down and claim how stupid I was if I am wrong

No there is little point writing it down and bringing it up later, I will just tell you now that you are stoopid.

Almost all your replies to any comments you don't agree with are very personal attacks. I wonder how old are you.

Anyways, for your info, at the end of every news, before the comments section, there is this:

"Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here."

Should I expect to don't see you around anymore? at least with that nickname?

Those with excessive debt against the housing market are a bit on edge lucenera. They don't mean to be nasty but their amygdala's have been hijacked by the risk they are presented with, that their 'precious' market might not go to infinity, and as a result they're in fight/flight mode as they consider the potential consequences. There is also a lot of pride/ego involved in property and property investment. People thinking they are superior to others because they own x,y,z or have been right in the past with debt speculation.

But the tide might be turning and this is causing those carrying risk to get very nervous and they move into fight/flight mode as they attempt to protect their precious egos and pride wrt the property market/property investment. Its impossible to reason with people in fight/flight as they are using the limbic system (lower order) as opposed to the higher reasoning/prefrontal cortex (higher order).

When people get nasty its the limbic system talking not the prefrontal cortex so have to be excused. Its hard when you try to lead people to use the higher parts of the brain but they want to continue to drag the discussion down to emotional triggers (limbic system thinking). At that point you just have to leave them alone to calm down and if they don't, don't engage with them.

Also its possible to tell when you are dealing with a psychopath (again not worth engaging) because they have no compassion/empathy toward/on topics that impact the well being of others....so if you post something about how the disfunctional property market is impacting the well being of society and certain individuals attack that, that they couldn't give a damn because its at odds with their own self interested property portfolio, you realise that you are dealing with a personality that would score high on psychopathic personality traits (the self is more important than the other).

Paradoxically if this post gets attacked with an emotional response, it will be by somebody whose limbic system has been triggered by the content of this post (lol). Anybody's limbic system out there getting all fired up?

Good books to read on these topics are by authors Danial Goleman, Daniel Kahneman and Thomas Erikson...and these are very much related to understand how people think, make decisions and interact with others. Great if you want a better understanding of behavioural finance/psychology.

You made my day :D

In general I liked your equanimity in many of past comments, so not too surprised.

I must admit there are few things that hit me (aka push my buttons) and I am tempted to reply in ways I would not be proud of.

I have my ideas and my ideals. I'd love to see a world where people don't have to fight for basic needs.

Some peps call that communism, but they are wrong. It's progress.

There are my hopes: a better word.

There are my opinions: the housing market will go down 36.5% in real terms in the next 18 months because bla bla bla (I already explained in another place why I think that number)

There are facts: the housing market is disproportionately priced.

I don't find any of those offensive for any normal person.

So yeah, I guess you are right, I am offending non normal people

Actually the longer and more garbled the post, there is a higher degree of desperation to persuade others. And your garbled verbage fit that bill IO

What a tool.....i mean troll

Very touchy easily rattled haha

Good point Luc, I actually agree a crash doesn't have an actual number attached. This market change seems to of gained the attention of some extremely how would you say passionate people with potentially little experience past the last 3 years.

It is a pretty hot topic and I see why people get passionate.

You are too. As I am.

But we can still discuss on civil terms :)

You might see something that I don't see... or I could instead.

In terms of crash, specifically, or correction, or other terms: is just about how much and by when and for how long.

Numbers, even far fetched numbers, are less vague than labels (that everybody can read however they want)

Very true Luc, what I'm saying is that this forum has a group of people with extremely arrogant views. They make claims like it will happen 100%fact etc, it's just a laugh. I believe the market will slow as it is and drop x amount. I then believe it will go up again, all be it in a more controlled manner. To be honest, in my opinion I think by December we will be in positive territory but that's more of a hunch based on different things. All the best.

You don't need to be in the industry, if you have zero bidders registered for your auction then there is no point running the auction. There must be a lot of tyre kickers about because I'm seeing auctions still running and houses without even an opening bid so there must be at least one registered bidder in the room. Very quick to fill out the bit of paper to register, you just then have to wonder how many then don't even show up.

I was being facetious. It’s a terrible result for Ray White if no one even registers for 20% their Auctions.

Maybe people don’t want to bid when they’re the only one in the room as it’s a strong indicator that the asking price is too high.

You don't know what the asking price is, its called the reserve. You can open the bidding at anything you want, be it hundreds of thousands below what its worth. Auctions are a gamble you don't know really how desperate the vendors are to sell or not and you never hear the real reason they are selling either because it may put the sellers in a very weak negotiating position. At the end of the day you bid to what you want to pay and you have to be prepared to just walk away.

Generally you can't open the bidding at anything you want - which is why so many get turned in without a bid. The auctioneer won't accept bids below a certain level.

But agree with the last statement. First rule of auctions - calculate your upper limit and never ever bid above that under any circumstances. If you have an emotional investment in the property, build that into your upper limit...never decide that on the fly.

Second rule of auctions - never bid against yourself. Amazing how many people do that.

Vendor bids are never really an issue as long as you still in your price window. You just stop early and hit the negotiation phase. If your cashed up at an auction and not in a panic to buy a house it puts you in a strong position.

I live in a north island regional capital. One thing I have noticed is that the higher priced homes in the $2 to 3 million range are not selling. Some now have fixed prices. There must be some very frustrated vendors and agents out there. I have also noticed some agents are swapping to new agencies. This happens when the market reverses.

P&I

about $220k to service the mortgage @ 7%........ouch

Over four grand a week...

Six grand before tax a week...

maybe one reason they aren’t selling.... and seven percent is now looking likely....dare not think of 8,9,10%

wipeout time

Yes those other numbers are actually going to happen. But as a Mystic once told me, people can only handle information and revelation 1 level above themselves, and that is on a good day. Banks are selling 6% mortgages, so only some people will be able to handle the belief that 7% is going to happen. Anything above that and the people will fight you to the death. So its just 1 level at a time.

Hopefully the end of the dreaded auction as the preferred method to stoke the market with irrational behaviour in pressure pot situations fuelled by massive bank lending, fomo & boomer wealth.....given they are early investors in the great nz ponzi scheme. Watch RB & key ponzi stake holders in Welly try to prop the market up in the next few years while inflation screws the rest.

Is it just me, or are there any investors here that are excited about the market downturn?

It's amazing, good properties I would have bought yesterday are now cheaper today! Same reason Buffet loves when the stockmarket goes down.

If you're in it for the long term and believe in land scarcity.. then a dropping market is an investors wet dream.

Remember folks, you make your money when you buy, not when you sell.

Of course it is. IMO we are in the "denial" phase based of the bubble model. All the opportunity happens at the end of the "fear" and "capitulation" phases and the "return to mean". There is still a long ways to go.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.