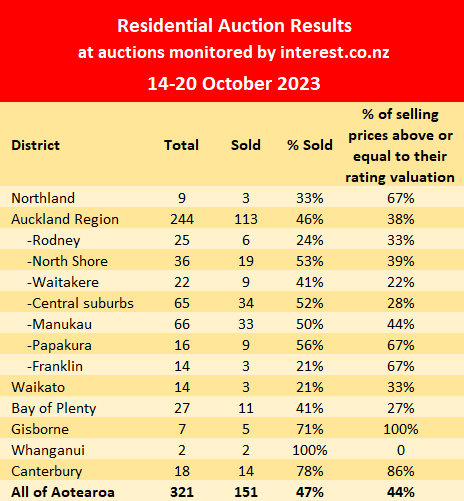

There was a slight drop in activity at the latest auctions although the number of properties going under the hammer remains elevated.

A total of 321 properties were offered at the residential property auctions monitored throughout the country by interest.co.nz in the week of 14-20 October, down from 367 the previous week.

However the previous week's auctions had the highest number of properties offered in any week this year and the latest week's auctions had the second highest of the year. That means the auction rooms are still the busiest they have been so far this year, surpassing the levels of activity back in March, which is usually the busiest time of the year.

The number of sales achieved also dipped slightly at the latest auctions, with 151 properties selling under the hammer compared to 167 the previous week.

The overall sales rate has been fairly steady for several months, usually remaining within the 40% to 50% range since early May.

The results of the last few weeks suggest a reasonable start to the spring/summer season, although things are usually a bit quieter during a short week so it may be difficult to pick a trend from next week's results.

The chart below shows the latest regional results from the auctions we monitor around the country, and details of the individual properties offered at all of the auctions we monitor, including the rating valuations and prices achieved for the properties that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

69 Comments

So the housing market is stagnant, with the potential to fall in light of HFL..

Sorry guys, HFL is now superseded by JH..

Jolly High?

Just Higher

Indeed. What is around the next corner is the much anticipated and delayed effect of the increased interest rates and rollover wave, not another boom.

The bigger picture over time = Cost of money trending up - house prices trending down.

Still can't picture it? Try adjusting for inflation and see what it looks like then.

The key/buzz word around the financial world is HFL... so that effect will start to show up in results over the next couple of months

Still can't picture it? Try adjusting for inflation and see what it looks like then.

Assume you're referencing your term deposits, Retired-Poppy.

TTP

... assuming you're factoring in net 8% interest plus insurance and rates as outgoings before passing judgement????

Life can still be good for some of us loser DGM's

Dont worry about TTP R-P, there is nothing wrong with TDs for unsophisticated investors and hopeful FHB.

.... and coming from you, I will rightfully treat that as a compliment:)

It's certainly about the FHB getting ahead - not me. TD's is an wise and patient method in achieving more equity up front don't you think?

The investment portfolio includes TDs as well as local and offshore shares, investment property. We rent a house with sea views

I wonder if a balanced portfolio should incl a couple of racing fillies.

On here, it can be anything you want it to be :)

"It's certainly about the FHB getting ahead"

Some maths for FHB to think about..

Another common line of reasoning is buy property as the mortgage erodes with inflation.

https://www.oneroof.co.nz/news/can-r...mortgage-41757

So how has that worked out in 2022?

1) House prices have fallen 15.2% in nominal terms

2) Inflation of 7%

A) November 2021

House price: 1,000,000

Mortgage (at 80% LVR): 800,000

Equity: 200,000

B) Dec 2022

i) Nominal terms

House price: 848,000 (-15.2%)

Mortgage: 800,000 (deemed to be interest only for simplicity)

Equity: 48,000 (-76%)

ii) Inflation adjusted values

House price: 792,523 (-20.7% from original price)

Mortgage: 747,664 (-7.0%)

Equity: 44,860 (-77.6% from original equity)

That fall in inflation adjusted equity value is a significant erosion of purchasing power.

Now how many of the buyers from 2020-2021 are going to be unable to hold on and be forced to realise their losses?

Now compare to if the buyer had instead chosen to put their deposit into a bank account.

1) Equity deposit 200,000 above

1 year bank deposit interest rate at Nov 2021: 1.64% (33% tax rate is net after tax interest rate of 1.098%)

https://www.interest.co.nz/chart/investing/term-deposit-rates

Value of deposit in 1 year: 202,197

Value of deposit after inflation of 7.0%: 188,969

After one year - inflation adjusted amounts of the same initial 200,000 deposit

1) Value of deposit in bank: 188,969

2) Value of equity in house: 44,860

The house buyer's equity value is 76% below that of the amount they would have had in the bank.

For those who know the significance of this.

Here is the return on a "risk free" asset in New Zealand:

1) September 2021 price: 98.25

2) October 2023 price: 59.13

That is a price change of -39.8% from its peak price in just over 2 years.

https://markets.businessinsider.com/bonds/new_zealand-_government_ofnd-…

Add to that equities are trending down too. Losses everywhere. I'm not alone in thinking something big is going to fall over and very soon.

Yep. With every quarter, inflation has made my mortgage smaller in real terms.

Not really. The cost of living increases are balanced out by falls in house prices over the past 2 years.

Sure, over the coming year perhaps as house prices continue to edge up and inflation continues to linger around 5-6% you might have a point.

He is correct HM, but only if you are getting significant pay rises to match inflation or better.

How is he right when house prices have been falling, significantly? Doesn’t make sense.

As I said, he will be right if house prices increase over the coming year and the CPI remains high

Housemouse I am responding to RP about house prices falling in real terms. In my area, nominal prices haven't fallen for three months or so. My wages will eventually catch up with inflation. But my mortgage will not change.

"With every quarter, inflation has made my mortgage smaller in real terms"

Another common line of reasoning is buy property as the mortgage erodes with inflation. What is overlooked (or conveniently omitted by the property promoters) is the impact of inflation on the falling housing price and the real impact on the owners inflation adjusted purchasing power.

https://www.oneroof.co.nz/news/can-r...mortgage-41757

So how has that worked out in 2022?

1) House prices have fallen 15.2% in nominal terms

2) Inflation of 7%

A) November 2021

House price: 1,000,000

Mortgage (at 80% LVR): 800,000

Equity: 200,000

B) Dec 2022

i) Nominal terms

House price: 848,000 (-15.2%)

Mortgage: 800,000 (deemed to be interest only for simplicity)

Equity: 48,000 (-76%)

ii) Inflation adjusted values

House price: 792,523 (-20.7% from original price)

Mortgage: 747,664 (-7.0%)

Equity: 44,860 (-77.6% from original equity)

That fall in inflation adjusted equity value is a significant erosion of purchasing power.

Now how many of the buyers from 2020-2021 are going to be unable to hold on and be forced to realise those losses?

the auction rooms are still the busiest they have been so far this year, surpassing the levels of activity back in March, which is usually the busiest time of the year.

new trend developing? Up and up not down and down.

This guy thinks so:

Liam Dann: Is Christopher Luxon about to get lucky with soft economic landing?

https://www.nzherald.co.nz/business/liam-dann-is-luxon-about-to-get-luc…

Mssrs Luxon and Seymour please please TAKE NOTE:

Making renting more secure is better for health. Renting can make you age almost twice as fast as being unemployed according to new international research. “It’s stressful for people, it’s insecure, it’s not very affordable so it’s logical and totally reasonable to find this outcome" says study author Dr Amy Clair. She says there should be a shift towards making private renting more secure for tenants. https://www.1news.co.nz/2023/10/19/renting-can-make-you-age-faster-study/ - 19 October See also NZPIF Plan to fix the rental crisis and recommendations for more secure tenancies -https://www.nzpif.org.nz/news/view/61761

It’s a conundrum.

Way back when, the governments of the time could not supply enough state housing for all of the lower working class and the so called bottom feeders who could not afford to own. There has never been a time when housing was affordable for all, no matter how small the sums of money may seem now, many people earned an absolute pittance and lending did not exist in the form that it is today.

The solutions provided ever since have always been to encourage private investment into the rental sector and to make it do the lion’s share of rental housing supply. The consequences of this over time keep resulting in a bigger version of the same problem that was trying to be solved in the first place. The lower cannot afford a house and the upper can afford many. The middle meanwhile commits their working life to home ownership, getting strung along with the carrot of striving to get ahead while their goals continue to remain only just out of reach.

House price’s in New Zealand are way above what average wage couples can afford from scratch, now a million dollar mortgage is at 8.5% on variable rates, cost $1800 per week for 30 years

That's right, with every loan that rolls over, there are folks that are going to be pressured to give up ownership, as it'll be unsustainable at these rates..

When were house prices last 'affordable' for an average wage couple?

1960's to 1980's. To some degree 1990's.

We knew people who earned $50 per week and houses cost 20k. They had to rent

There are now people who earn min wage ~$900pw (18x your example), and the average house is ~900k (45x your example)

Not sure what your point is? That affordability is far worse now? Which was NZDans point…

Seems to me that a prerequisite to having property acumen is being shite at math.

But houses had to be cheap as everyone wanted to leave the country.

IPhones cost 2k, the same as a dining table and chairs in those days. All the household items were a ridiculous amount

The hubby would be the sole income earner in those discriminatory and sexist times.

Now things are so good the whole world wants to join us. NZ migration gain of 120k, nearly the size of Hamilton, Aust net migration 600k, probably the size of Canberra.

"You will be happy with house prices at 15 - 20 x the median wage (instead of 3 - 4 x) and be grateful for cheap furniture and televisions".

Anecdotes can be found everywhere. Maybe your friends didn't work hard enough?

Dated 28 November 1975, which was the day before the election that saw Rob Muldoon become Prime Minister, the properties for sale were largely priced in a range between the early $20,000s and the early $50,000s. An average income at the time was about $125 a week.

https://www.stuff.co.nz/life-style/homed/real-estate/124420300/snapshot…

Nifty it was last "Affordable" when only one person had to work. Even in my 20's the bank wouldn't lend me enough to buy an apartment in the city. Housing will never be as cheap as it was in the 1970's, you just have to move on, it is what it is.

re ... "When were house prices last 'affordable' for an average wage couple?"

Way back in the 70s.

The problem was though, it was near impossible to get a mortgage from a bank.

No credit = few house purchases = no house price appreciation = stagnant rents = no need for both partners to work

I remember my dad (well paid medical professional) got a small bank mortgage, then 2nd non-bank mortgage and then two loans from solicitors to buy a $40k house which was 2? or 3? times income. Oddly, the interest rate spread between all 4 loans was only about 2%. Pretty sure Housing Corporation was in there too somewhere but not sure if they were part of the final mix.

Any reason your well paid father didn't just save a little harder? This whole 2 mortgages and 2 separate loans to buy a house at 3 - 4 times ones salary is quite bizarre, sounds like a frivolous entitlement mentality. "Why should I have to save for a house?". I'd be quite embarrassed to make that admission when you look at the numbers.

Wow. How old are you?

LOL this was totally normal Nzdan, my parents did exactly the same, the bank did not lend you enough back then so they had a "2nd Mortgage" with a solicitor at a crazy interest rate. Waiting to buy would have been stupid in hindsight, house prices took off. They bought a house that the builder folded on and had to sell it unfinished and it cost $17K in about 1975. That exact same house is now $1.43M.

Zwifter, house prices actually held constant from 1974 to 1980, while prices for everything else increased around them.

It was in 1986 that I lent $20K through a Solicitor to a business @22.5% pa. Crippling interest rates seemed to be the norm back then.....

People were taking out second mortgages all over the show. There were those who were on (if I recall correctly) Housing Corp loans fixed on 2-4% and were creaming it. I know of one couple who were "encouraged" to pay theirs off lump sum as it was costing the state dearly. They didn't and took it to full term.

The following link shows what happened in the 70s when borrowing rates took off and house prices failed to fire.

Remember the last time house prices crashed 40%? - Greater Auckland

Is history repeating?

FYI, Figure 4 on page 5 shows both inflation adjusted house prices and nominal house prices.

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/publications/…

Winners turn problems into opportunities……

And then the various losers here criticise the winners for succeeding.

TTP

Surely you weren't keeping a straight face when you typed this.

LMFAO😂

Retired Poppy - What helped you build the confidence to buy a house in 1997? What was the motivation? Surely the world must of looked like it was collapsing back then aswell.... the Asian Financial Crisis was just hitting...

We found the house we wanted, made a lowball cash offer at 18K below asking and they accepted.

Nice. Sure that $18k looks pretty irrelevant now but you got the home you wanted and have been there ever since. Similar to what people are doing now...buying well. Good on them.

I think Autumn 2024 is when even better value will start to appear and lowball offers will yield some chunky discounts. If I'm proven wrong, no doubt I will be crucified on here and branded a loser - LOL!

1997, the top of the cycle

LMFAO

You're wrong. As Nifty1 pointed out it was indeed the onset of the Asian Financial Crisis and things were looking pretty bad. Real house prices fell, not by a lot but sales volumes were certainly down. We got our bargain and all equity and that's what mattered.

If you had taken the time to look at CN-new graph above, perhaps you'd have been better informed.

Returns for the last month.

Ryman Healthcare -11.47

Oceania -5.33

Summerset -2.40

Ouch......hardly pointing to an imminent recovery now, is it?

Answer this

For a holder in any of these stocks, is it time to sell or buy more and stick in the bottom draw

Psst, many shareholders are sitting on huge equity gains.

"the 70s when borrowing rates took off"

FYI,

https://teara.govt.nz/en/graph/23100/interest-rates-1966-2008

70s house is not today's house. it'll be ilegal to build a house using 70s standard today.

Using solid heart rimu, redwood and matai? Thicker boards unlike today?

When I read that comment I looked around my 1920's Villa and recalled opening up the wall between the kitchen and dining room. Who needs GIB as a bracing element when all your walls are lined with sarking boards.

It will probably be affordable for average wage earners again we are already down 20% from highs, another 25% down and with inflation should just about do in around 2 years.

Mate...You're dreaming.

Nifty1 You said that before the last 20% crash or around 33% with inflation adjustments. It’s not a dream the next phase down will hit hard and fast as people refinance on to much higher rates million dollar mortgage from 900 per week to 1800 per week you are dreaming and naive if you don’t understand the effects of this on house price’s.

It's life Jim, but not as we know it.

It's life Jim, but not as we know it.

In a world awash with stories of hell-fire and brimstone, some get sucked into a vortex of negative thinking. They're the real losers......

Others prosper and thrive. 👍

TTP

....yes indeed, they do.

Way back in 2008 when we had 4% inflation the OCR was over 8%. We now have CPI at 5.6% and OCR 5.5%. and many seem to think its all downhill for interest rates. My guess is that its higher for much longer and stagnant house prices. I wouldn't expect Orr to do the National government any favours.

Yep. Which begs the question as to why the OCR isn’t higher.

The answer, of course, is pretty obvious.

We should have 10% if not higher mortgage rates. Time for some sacrifices.

HFL is a con, led by banks. It equates to HIGHER profits for banks for LONGER.

Bank economists have become sales people for banks (with a very few notable exceptions). Actually, come to think of it, they probably always were.

Take great care from where you get your forward looking financial advice. And take great care when reporting what charlatans economists are to differentiate between bank-economists and non-bank economists.

How does this relate to auction sales? Well, let's revisit what is "affordable" in early/middle '24 when HFL is recognised as the nonsense it is.

They are indeed businesses focused on exporting profit to their larger shareholders offshore. So yes, make up your own mind. Think about the risks of excessive debt unsupported by income (speculation). As long as debt is almost risk free the people that can access it have a massive exploitation advantage over those who cannot. Accordingly debt should not be free or close to it.

Banks now have been regulated into factoring in borrowers incomes. One notes that was not self regulated, they were forced into it by legislation. Something about directors being personally liable....

I cannot see national totally repealing CCCFA, tho they may tinker a bit.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.