By David Skilling*

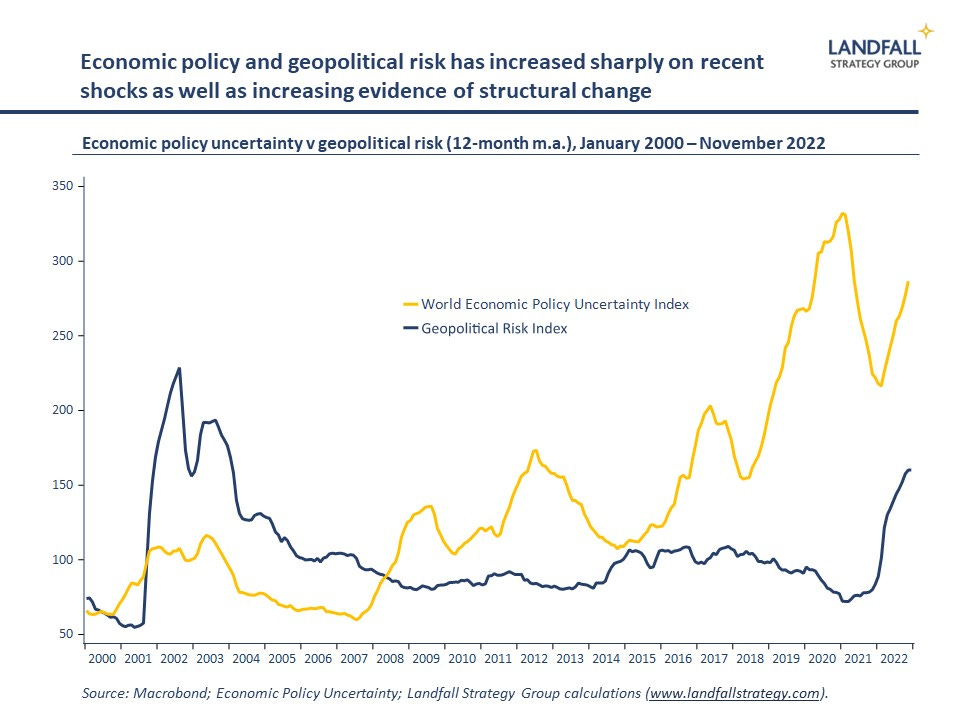

The disruptive events over the past three years – from the pandemic to the invasion of Ukraine and the structural shift of the global economy onto a wartime footing – have placed deep pressure on countries around the world.

War and other shocks illuminate the strengths and weaknesses of political systems in ways that are not apparent during normal, less turbulent conditions. Ukraine, for example, has performed remarkably under unimaginable pressure.

So at the start of the year, this note discusses how different countries have been affected by this acute stress; and how well placed they are for the economic and political regime change underway.

United States

Political polarisation in the US has weakened social cohesion and institutions, and caused decision-making gridlock. The US has been in a close race between its macro dysfunction and its micro-level innovation and dynamism.

Indeed, the US had a bad pandemic – with poor health outcomes – largely due to this political context. But over the past two years, there has been some stabilisation even if political risks remain (note this week’s chaotic House Speaker elections).

The US is now moving in a broadly bipartisan way in terms of the strategic competition with China, with big investments in industrial policy, R&D, and infrastructure to strengthen the US economy as well as a tougher military and diplomatic posture. And it has led the West’s response to Russia’s invasion of Ukraine, providing significant military and financial aid.

The US does better facing external competition than domestic challenges. Indeed, the shared purpose due to the external rivalry may moderate domestic political tensions. Whereas the pandemic exposed weaknesses, strategic competition plays to US strengths. I am becoming more structurally bullish on the US, with its financial and technological leadership positions.

However, some of these recent policies (such as the Inflation Reduction Act) interact with protectionist tendencies in the US, due to its mismanagement of international trade over the past few decades. The US will need to remain open and engaged, with strong partnerships, to compete effectively.

Europe/UK

After a characteristically slow start, the EU responded relatively well to the pandemic; high vaccination rates supported good economic and health outcomes in many countries. But the Russian invasion of Ukraine highlighted the deep complacency across much (not all) of Europe on strategic economic, political, and security exposures.

There has been an encouraging response, with European governments implementing tough sanctions on Russia and committing to invest more in areas from military capability to strategic autonomy. And this experience has reinforced a toughening stance on China (although with variation: note Germany).

However, European institutions move gradually, and Europe’s deeper integration into the global economy (compared to the US) means that decoupling comes at a high cost. Europe has a long way to go to position its economy for a wartime footing, with substantial investments and policy innovation required to build resilience and competitive strength.

In the UK, the pandemic and the economic spillovers from Russia’s invasion have put further strain on a structurally weak UK economy. The UK has under-performed its peers since the global financial crisis. Indeed, the UK had the worst economic performance of any G7 country through the pandemic – as well as poor health outcomes – and has a weak economic outlook.

These external shocks have revealed policy and political deficiencies. Without significant policy change, notably around Brexit, economic improvement is unlikely. The political chaos has reduced but the UK’s ability to make the investments required to perform in a changing global context is uncertain.

China

The pandemic has highlighted the strengths and weaknesses of China’s autocratic decision-making. The rapid lockdowns constrained the costs, but zero Covid was unsustainable. And the abrupt shift to open up, with apparently little/no preparation, will generate substantial near-term economic and health costs.

China’s highly personalised decision-making process creates real risks for China – and the world; for example, on decision-making with respect to Taiwan. Some of China’s recent rhetoric and decision-making seems to have reweighted diplomacy and economics over ideology, but this could easily change.

China’s massive market gives it options in building strategic autonomy, and influencing economies and firms to support it. But it remains deeply reliant on technology and other expertise from the US, Europe, and elsewhere.

China’s economic prospects are challenged, with a contracting working age population, weak productivity performance, and structural distortions across its economy. My assessment is that its political environment will constrain China’s ability to develop as an innovative, dynamic economy. It is not clear that China will be able to overtake the US as the world’s largest economy – particularly given the tougher strategic posture of the US and Europe.

China remains a formidable competitor, but it is a much more challenging external environment for China. For example, this week China reduced its commitment to local semiconductor firms because of the absence of results from its massive support to date.

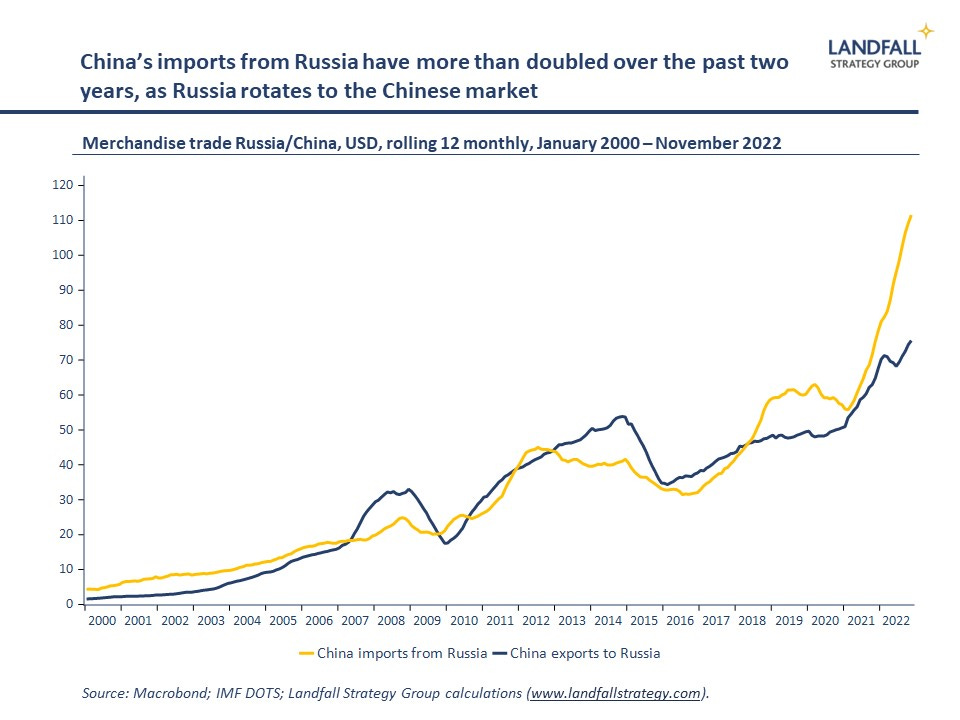

One asset is that an enfeebled Russia is becoming a client state of China, giving China readier access to energy and other commodities. This transactional relationship will skew increasingly in China’s favour.

Middle powers

Another important group of countries are the ‘middle powers’, from India and Indonesia to Saudi Arabia and Turkey. These G20 economies (and others) are acting to carve out strategic space in a more contested global environment – not aligning with the West (on issues like Ukraine) and pursuing their national interest. They do not want to choose sides.

Many of these countries have deep domestic challenges, but are taking advantage of a more fluid global environment to restructure external networks. The rebalancing in the Middle East towards China on energy and financial flows is just one example. The shift of the global economy to a wartime footing has accelerated realignments, as countries reassess the value of existing relationships. Expect these countries to become more forceful in capturing economic value, in areas from energy and commodities to global value chains, and shaping the global system.

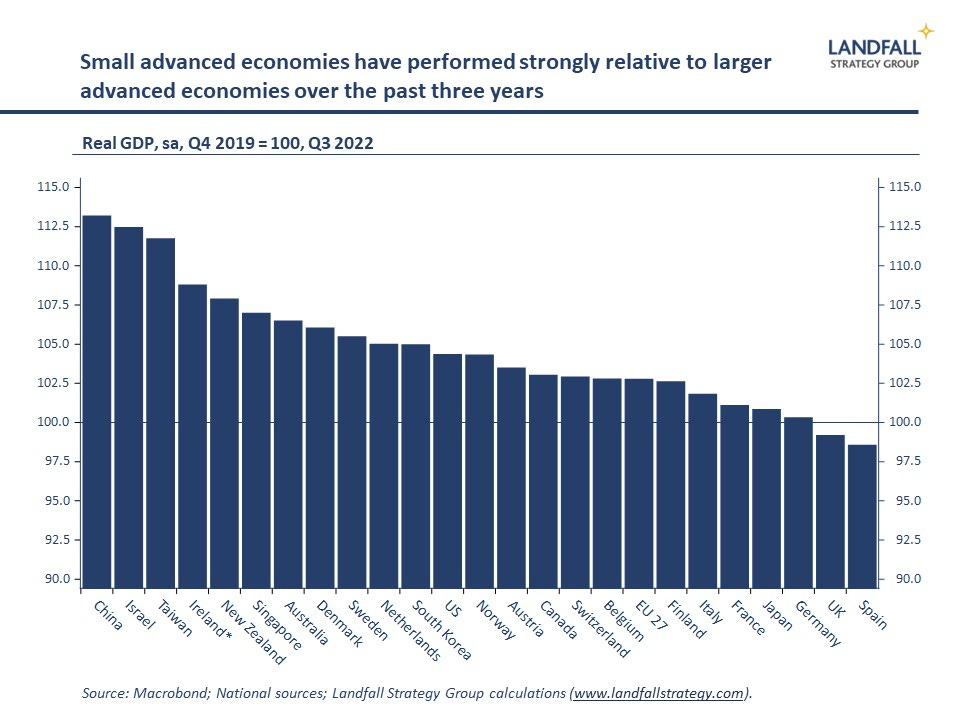

Small advanced economies

Small economies have performed well over the past few years despite (or more likely because of) their deep exposure to the global economy. They generated strong GDP growth as well as good health outcomes through Covid. And they are effectively navigating economic shocks from higher energy prices and changing patterns of globalisation.

Small advanced economies have a series of valuable assets: effective governments, social cohesion, strong skills and innovation capabilities, as well as an external orientation. There are not economies of scale in navigating regime change: as shown in the discussion above, large economies have no intrinsic advantage.

If anything, small advanced economies may out-perform as they position for this new environment rapidly and creatively. From Singapore’s strategic positioning, to the aggressive economic strategy revealed by Dubai this week, to the green energy initiatives pursued by small economies around the North Sea, there is an intensity of action.

Creative destruction

A wartime global economy is a time for serious countries. Significant, sustained changes in strategic policy settings will be required, from industrial and innovation policy to foreign policy and security.

This means that we should expect an accelerated process of creative destruction. Periods of pressure from disruptive change produce a broader distribution of outcomes; some countries (and firms) will perform, and others will struggle. The ongoing global stress tests may generate surprising results.

*David Skilling ((@dskilling) is director at economic advisory firm Landfall Strategy Group. The original is here. You can subscribe to receive David Skilling’s notes by email here.

**Get in touch (by reply email or at contact@landfallstrategy.com) if you would like to access the full paper referred to in the article above.

30 Comments

An in depth read for a Sunday morning with the year little begun. Our world is immersed in an enormous watershed moment, to put it mildly. Amongst all of that one line is clarion, “an enfeebled Russia …..” That skewing in the balance of power in that region is very open ended. China has never ever had a recognised ascendency over Russia such as it has now. Relationships that are out of balance are hard pressed to remain upright.

Take a look at Nato.

From pre pandemic to Q3,22 NZ has done quite well , according to the chart, even beating the west cousins in real gdp. Pretty strange, knowing what's happened to our economy over that time.

To be honest what you gain from being on the ground beats any numbers put out by the government.

That might depend on what ground you are on. Our household are significantly better off now than before covid so the government numbers seem valid to me.

... something Keith Woodford mentioned yesterday which is of concern for NZ is our current account deficit ... which has ballooned out ... and at a guess , I'd say that as the Reverse Bank ratchets up the OCR , the Aussie big 4 banks crank up the mortgage rates , and more Kiwi money flows out of our economy & into Australia's ...

GBH,

You have been a vocal critic of MFB-rightly so, but looking at their latest figures intrigues me. As shown in the last report, they now have some $5.9m in cash, while bank borrowing is down from $15.86m to $3.4m. Their EPS went from $0.01c to $0.08c.

the current share price of just $0.40 makes it an interesting proposition. Worth a small punt?

the current share price of just $0.40 makes it an interesting proposition. Worth a small punt?

Be my guest. For me, I would never invest in such a business as I feel that it's not scalable in a meaningful sense. I think that these kind of business propositions in a country with relatively low urban density and high cost structures are not worth the effort.

Reductions in net spendable incomes will change the fortunes of this type of company being a nice to have rather than a must have.

For a country with the 5th highest GDP per capita, our economic disparities are shocking. This will be our undoing.

Question is why is GDP per capita relatively high. Is it because of our productive output compared to Israel, Taiwan and even low-rankers such as Japan?

It's only the last 3 years, no?

Surely if we look at the ranking of countries in the chart, it overlays pretty well with "which countries got disrupted least by covid over 2020-2021".

Your probably right. Go back 2020 and we rank 22nd.

What is worse, it confirms that we we grossly over compensated for covid and our high ranking is on the back of our government borrowing far more money than we needed to.

Borrowed far more than needed to. Understandably the powers that be were worried about NZ’s health services. We all were and still are. The borrowing was overblown and matched by the indiscriminate spending. $ millions on a monolithic headquarters for MoH in Wellington when overwhelmed frontline services & staffing were screaming out for support and assistance.

Not much of an optimist, huh.

Particularly in the early days, the government actually made some pretty decent decisions around keeping many of our export oriented industry going in spite of the lockdowns. This allowed for a greater degree of economic continuity and less social welfare spend.

Hard to do too much better without an unreasonable level of hindsight.

Particularly in the early days, the government actually made some pretty decent decisions around keeping many of our export oriented industry going in spite of the lockdowns.

Got any specific examples? The tourism and education export industries were more or less shelved. I very much doubt the govt was instrumental in driving the export of milk powder and kiwifruit.

March and April are a pivotal harvest time in horticulture and viticulture. It's worth several billion dollars in exports annually. At that time in 2020, some fairly significant work went into allowing the harvest and processing to continue despite lockdowns, including the setting up of isolated work camps using furloughed campervans, and segregation of work shifts.

All happened pretty quickly, it's almost like we make our best decisions under urgency deferring largely to current best practice.

At that time in 2020, some fairly significant work went into allowing the harvest and processing to continue despite lockdowns

OK. Do you know anywhere in the world where harvesting and processing was banned in 2020 because of Covid lockdowns?

No, but I know of plenty of places where harvests didn't happen due to covid mismanagement, with everyone either sick or locked at home.

Fair comment - Plan A good Plan B non existent.

Surely if we look at the ranking of countries in the chart, it overlays pretty well with "which countries got disrupted least by covid over 2020-2021".

Nope. China has arguably been the most disrupted by Covid.

For a country with the 5th highest GDP per capita, our economic disparities are shocking. This will be our undoing.

There is nothing to indicate that the chart shows GDP per capita. Rather it shows the relative change of GDP between Q4/2009 (100) and Q3/2022.

Does switching from Labour to National count as regime change?

.. no , it counts as switching the Jacindamania blinkers off , and opening your eyes to the reality of Struggle Street , NZ ...

Since when have gnats changed anything? Imagination has never been their strong point.

The figures quoted above are smoke & mirrors as usual so take with a grain of salt. They are basically relative graphs. The reality is much worse the closer you get to ground zero.

We're somewhere in the upper middle of the working age population in NZ. At our age that is to be expected. On some measures we make it into the top 10% but again, been in it & at it for 40 years now, so we'd be concerned if we weren't.

To all you younger ones out there [& that's most of you] keep your heads down & focus on doing a good job. Whether at home, in the work place or out amongst the community, become someone who earns respect. That way you'll get to the top of the tree eventually.

Agree Wrong John, as for every previous generation it's a matter of knuckling down and getting on with whatever you are doing.

And never give up.

This is great but you're ignoring objective statistic reality that knuckling down and getting on with it only gets you to a point.

Much easier to make hay while the sun shines at 4x household incomes for houses than it is at 9x or 10x.

Not to mention that previous periods of high inflation have come with greater wage inflation to help make debt affordable, whereas we seem doomed to endure the high inflation and the drop in real incomes because someone's worried about a 'wage-price spiral' that ignores the fact that wage increases are a response to higher prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.