The Ministry of Justice is proposing banks stump up the lion's share of levies to be paid by those supervised under the Anti-Money Laundering and Countering Financing of Terrorism Act (AML/CFT Act).

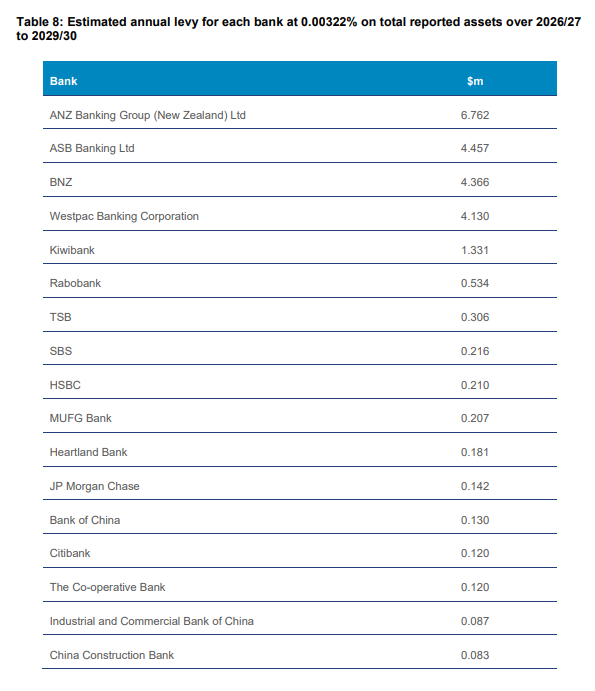

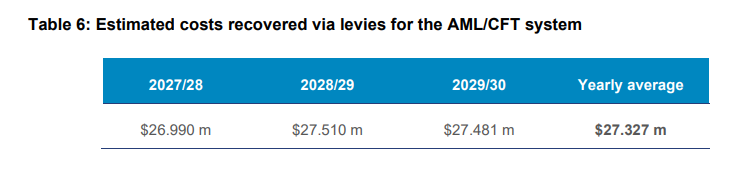

In a consultation document, the Ministry suggests banks pay 85% of $27.327 million, or about $23.228 million a year, of the proposed levies to help fund the AML/CFT system. This would see ANZ New Zealand, the country's biggest bank, pay $6.762 million, ASB, BNZ and Westpac NZ more than $4 million each, Kiwibank $1.3 million, and smaller banks significantly less.

Plans for the levies come after Associate Justice Minister Nicole McKee announced a shake-up to AML/CFT Act oversight in 2024, including plans to introduce levies on reporting entities.

The costs proposed to be met by levies include AML/CFT statutory functions of government agencies. The proposal is a hybrid model and not a full cost recovery model, meaning there would also be some Crown funding.

"We propose that most of the [levy] costs be recovered from banks, for equity and efficiency reasons," the consultation paper says.

"In particular, the Ministry has applied the principal that from an equity perspective risk exacerbators should pay their portion of costs. The [AML/CFT] National Risk Assessment [NRA] also states that the banking sector remains the highest risk. The NRA states that over $58 trillion of financial transactions are processed through the banks. Well over 90 percent of monetary transactions include the banking system. Even where other regulated entities (such as real estate agents and lawyers) are engaged in transactions, banks are almost always involved. As most payments go through banks there is a nexus between all other money laundering and banks."

"Due to the risks that banks pose to the system, their supervision costs will increase over time. The work programme includes an increase to regular offsite and onsite supervision of the five major banks due to their materiality in the financial system. Also, they would likely consume a large proportion of the intelligence resources produced by the [Police] Financial Intelligence Unit [FIU]," the Ministry says.

It's proposing using the value of bank assets to determine the levy paid by individual banks.

"The value of reported bank assets will determine each bank’s levy contribution, based on a bank’s most recent full year disclosure statement at the time the levy is set. Banks with less than $1.5 billion in reported assets would be exempt from the levy."

The Ministry proposes setting out a band in the regulations with the exact levy rate for banks published in a notice.

"The band would be between 0.001% and 0.005% of reported bank assets. The rationale for a band is to provide flexibility when setting the levy rates to account for fluctuations in the value of assets. Using the Reserve Bank of New Zealand’s Bank Financial Strength Dashboard, and bank disclosure statements for total assets, we estimate that a levy of 0.00322% of reported bank assets raises approximately $23.380 million a year. The estimated levy rate for each bank is set out in Table 8 [see below]."

"As of January 2026, we estimate the levy would cost just over 0.2% of banks’ cumulative pre-tax profits. Each bank will decide whether to absorb costs or pass them to their customers via fees and charges. However, we expect that this would be negatable given the size of the sector," the Ministry says.

It notes a similar levy has been implemented in Australia "without noticeable impact on consumers."

"In late 2028, all deposit takers will be regulated under the Deposit Takers Act 2023. This will remove the distinction between a bank and a non-bank deposit taker (NBDT). Proposals for the levy period exclude NBDTs. The exclusion of NBDTs from the levy will be reconsidered in 2028, alongside an assessment of risks to the AML/CFT system. However, the proposed $1.5 billion threshold should exclude current NBDTs," the Ministry says.

The Anti-Money Laundering and Countering Financing of Terrorism (Supervisor, Levy, and Other Matters) Amendment Bill, which is currently being considered by Parliament, proposes levies should meet a portion or all the costs incurred by the Ministry, the Department of Internal Affairs which is to become the sole AML/CFT supervisor from July with the Reserve Bank and Financial Markets Authority losing their roles, and the Police FIU in fulfilling their requirements under the AML/CFT Act.

The levy proposals anticipate the Bill being passed in 2026, with the Government to decide the final form of the levy, which will be included in regulations and anticipated to take effect during the the second half of 2026, albeit the collection of levies would commence from July 2027.

The Ministry notes its 2022 statutory review and the Financial Action Task Force's most recent Mutual Evaluation Report for New Zealand, in 2021, concluded the AML/CFT system "was not sufficiently resourced to deliver its functions."

"Insufficient resourcing was impacting how responsive the AML/CFT system is to the needs of the industry. The statutory review found that: … insufficient resource levels, along with an absence of mechanisms to ensure appropriate resource allocation across the regime, is likely contributing to the operation of the Act not being sufficiently risk based...The net outcome... is that the regime is not as effective as it could be, and it is harder (and likely more expensive) than it needs to be for businesses to comply with the Act. Ultimately this undermines efforts from businesses to detect and deter money laundering and terrorism financing."

"The levy will fund activities that would benefit reporting entities," the Ministry says.

Written submissions are due by 5.00pm on Friday 10 April 2026.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

5 Comments

The banks customers will ultimately pay for our countrys' kowtowing to the USAs incessant attempts to tax US citizens on their global income.

Just do it, drop in the bucket. Don't let them scare you that costs will go up.

Yeah make the banks pay for free card transactions, free cash withdrawal’s (twice a day in the middle of nowhere), anti money laundering, etc. I’m sure they’ll just do it out of the goodness of their heart.

Alternatively Ceo and directors compulsory 6 months in jail

Who will pay the levies on behalf of the crypto industry?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.