Improvements in home loan affordability over the last 18 months appear to have come to an abrupt end in February.

The sudden deterioration in affordability occurred due to a combination of steadily rising mortgage interest rates and a jump in prices at the bottom of the market.

The average two year fixed mortgage rate has been rising since it hit a cyclical low of 4.49% in November last year, increasing to 4.72% in December, 4.74% in January and then 4.87% in February.

That was accompanied by a jump in the Real Estate Institute of New Zealand's lower quartile selling price to $600,000 in February, which reversed a sharp fall to $583,000 in January.

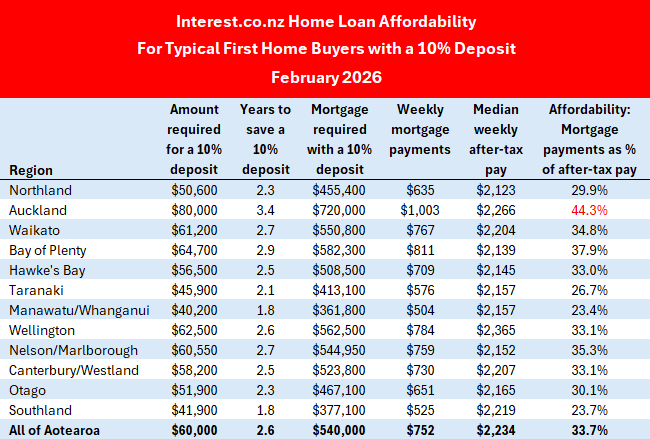

That combination of higher prices and higher interest rates pushed the mortgage payments on a lower quartile-priced home up to $752 a week in February, assuming the home was purchased with a 10% deposit, up an extra $32 a week compared to January.

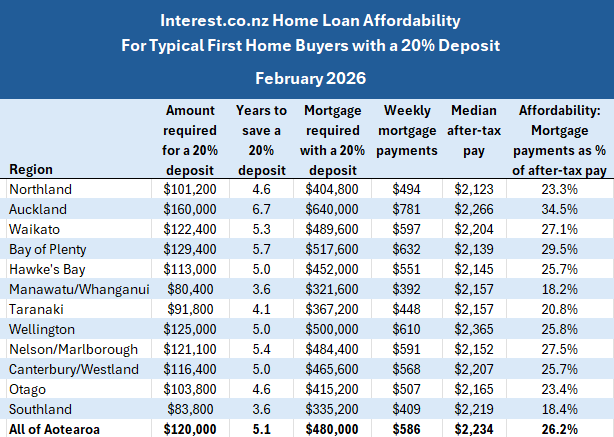

For buyers with a 20% deposit the mortgage payments would have increased to $586 a week, up an extra $26 a week compared to January.

However, it is important to note the recent rises in both lower quartile prices and mortgage interest rates have only taken them back to where they were late last year, and that housing remains well within affordable limits for typical first home buyers on average incomes in most parts of the country.

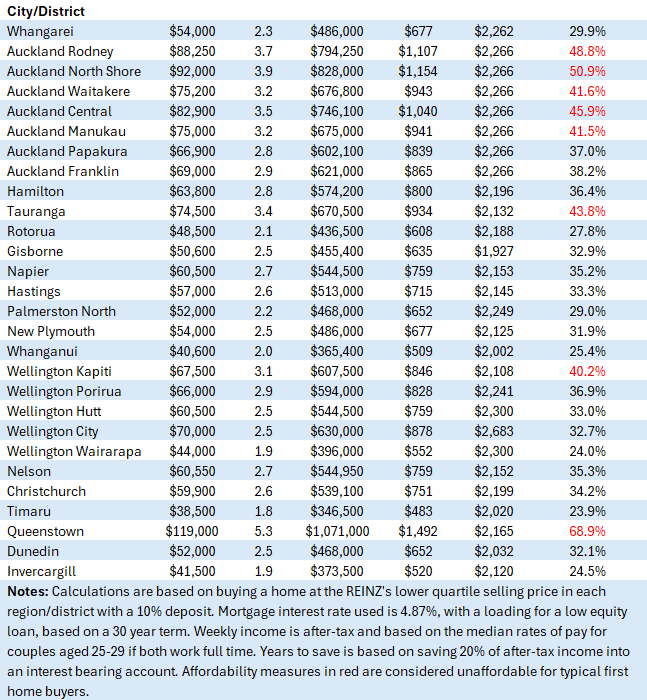

That said, they will likely need a higher than average income in most parts of Auckland if they have less than a 20% deposit. And home ownership in Queenstown remains well out of reach for all but the already wealthy or the highly paid.

Finally, the economic landscape in February was very different to that which is emerging in March, with the market being dominated by the twin themes of volatility and uncertainty over the last few weeks.

Consequently, it may well be the affordability picture that emerges at the end of March is quite different to the one we saw at the end of February.

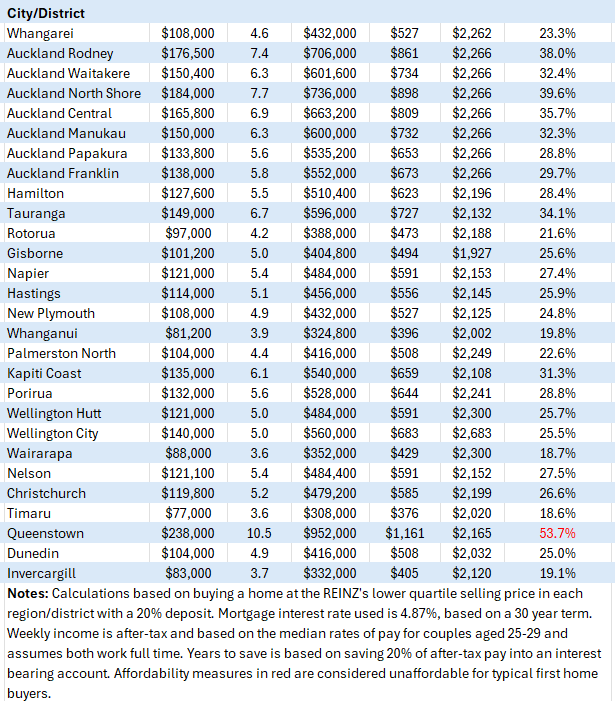

The tables below show the main measures of affordability for all of the main urban districts throughout the country, for buyers with either a 10% or 20% deposit.

The comment stream on this article is now closed.

12 Comments

If you've got the 20% deposit its only $586 a week, which is about what you'd pay in rent. Is housing really overpriced?

$586, + rates + insurance.

+ $200/ week extra if mortgage rates jump up a couple of percent. I guess it all depends on your income and other outgoings (kids, student loan).

Given the massive recession that is about to hit, who knows where things are headed.

Our house insurance is $180 / month, and I'd estimate rates at about $300 a month (based on our rates for a house that is above entry level). So that is another $110 a week for both. Then there is also maintenance.

But the flip side is that in 30 years you own something.

I'd be about~$138 a week in rates, water and insurance before touching the mortgage. Rates and insurance are on the up year on year above inflation as well so that will keep escalating. I count myself lucky to have a relatively secure job, but if AI continues to creep and remove jobs from the market, and a recession comes from increased fuel prices in the medium term, then I wonder how long the banks will look the other way this time before calling it in for mortgages in arrears.

If only affordability were like buying a pair of shoes and not a 30 year commitment till mort, to a future of chaotic black swan events that might have you on a park bench?

Pretty much like rent isn't it. If you can't afford it you're out on the street...

Maybe. But if the oil prices rises cause significant inflation then mortgage holders will get interest rate rises at the same time as a potential recession.

Yip and the collective renting pool won't be getting a significant pay rise (unless inflaiton really has got its teeth into the economy) so its not like they have the extra discretionary income to offset the landlords losses from increased interest expense.

Ah but they will have a large supply of options to choose from in the rental pool which favours them in the coming times.

Pretty much like rent isn't it. If you can't afford it you're out on the street...

Not really. For mortgage holders they have options to bide some time with the banks or lower costs (Interest Only) before they have to calling the mortgage and sell up, then putting the inhabitants on the street. Renters can be booted easier, however if they squat then it takes time to get them out forcefully.

Not really, if you're an evicted renter the bank's not going to be chasing you for the unpaid cash after foreclosure.

The last hope for sellers is stretched further away. What to do...?

Lower the price.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.