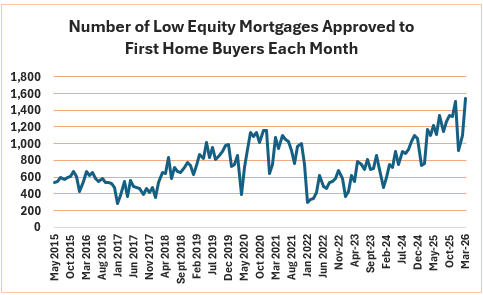

The number of first home buyers taking out low equity mortgages hit its highest point in nearly 12 years of Reserve Bank data in March.

The latest Reserve Bank (RBNZ) figures show banks approved 1537 low equity mortgages to first home buyers in March, making up 45.3% of all mortgage approvals to first home buyers in the month.

That was the most low equity mortgages approved for first home buyers in any month of the year in the RBNZ's data series which goes back to August 2014, meaning it's likely to be an all time high.

The volume of low equity loans approved to first home buyers in March was up 31% compared to March last year. Their numbers have more than trebled in the last 10 years. See the first graph below for the trend.

A low equity mortgage is one in which the value of the loan is more than 80% of a property's valuation, meaning the borrower has a lower level of equity in their property, compared to a normal mortgage which requires at least a 20% deposit.

Low equity loans are considered higher risk, because they would generally give the borrower less wriggle room to restructure their repayments should they strike financial difficulties, and the bank also has a lower level of security in the event of a default.

However, low equity loans are also more lucrative for banks because of the extra fees they charge for them due to the higher risks involved.

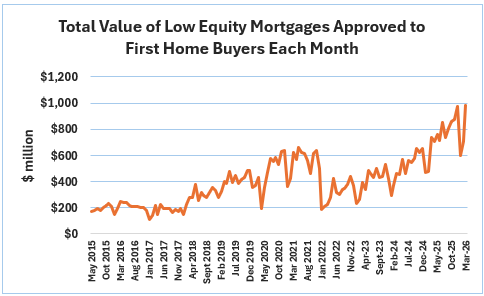

At $983 million, the total value of the low equity mortgages approved for first home buyers in March was in touching distance of $1 billion, and also likely a record high. The total value of low equity mortgages approved to first home buyers each month has increased by more than 600% in the last 10 years. See the second graph below for the trend.

On average first home buyers taking out a low equity loan tend to borrow more money than borrowers with a minimum 20% deposit. The average size of the low equity mortgages approved to first home buyers in March was $639,558. The average mortgage size for first home buyers with at least a 20% deposit was almost $100,000 less at $540,118.

The comment stream on this story is now closed.

38 Comments

What a disaster for these people. In one years time there's every chance they'll be crushed by interest rates and negative equity.

How certain is your “every chance”, if it’s a family home and your “every chance” isn’t a correct call then they have every chance that they might miss the home they really wanted.

How certain are you that they won't be able to buy the same house for 10% less next year? So missing out this year might be the greatest gift they receive.

Just as those who missed out in 2021 were relieved to find they could buy cheaper in 2022...2023...2024...2025....2026...than those who purchased in 2021.

Could well be the same that those who miss out in 2026 might find they can buy the same house for cheaper in 2027....2028....2029...

Confirmation and recency bias of the previous 3 decades would say I'm wrong....but the reality of 2021 to now would say I'm right. And yet you appear 100% certain that Palmtree is wrong in his/her opinion. Were you this confident in 2021 also that the 'be quick' team were correct and that if you didn't buy then, FHB would be locked out of the market for another 10 years - as they were claiming at the time? They turned out to be 100% wrong.

Haha settle down, at no point did I “appear 100% certain” 😂😂

You can mitigate against "crushed by interest rates" by fixing long

30yr is long and no option in our DANGERIOUS ARM style only market.

My uneducated opinion would guess anyone taking out a low equity loan would also be looking for the lowest rate on the card?

Bank greed is winning out here, which is troubling in my opinion. It's like we haven't learnt from the mistakes of the past. 20% should be the absolute minimum deposit - and not a penny less.

Bank greed is winning out here, which is troubling in my opinion.

When I see the word 'greed' in relation to housing, it frustrates me. Banks are simply trying to grow their business: keeps shareholders happy with dividends; ensure the top brass get their healthy bonuses; the foot soldiers get to keep their jobs. Apart from the top brass' bonuses, this is not really greed.

Nor is it 'greed' to want to get on the ladder before it's too late. Society - through the media and water cooler / BBQ exchanges - is telling people the same thing. I see some similarities between the general attitudes towards Aotearoa housing and those pumping the ol' rat poison (don't be left behind).

I bought my first house 20 years ago with a 15% deposit, and I'm bloody grateful the bank was so "greedy"

That's good to hear Jimbo. I do appreciate that low equity loans let more people in the door. The point I was trying to make is that once you go below 20%, the equation becomes more difficult for the FHB, and they face higher (low equity) interest rates, which makes the first few years a real battle. Additionally, there's less skin in the game for those occasions where prices can fall 20%+ (like we've seen in Wellington & Auckland in recent years), which places more strain on the FHB. It may not feel like it for the people wanting to get in to their first home, but these LVR rules are designed to protect buyers from serious economic hardship if things turn south.

Not everything revolves around you and your house you bought 20 years ago Jimbo - even though you bring it up every 3rd comment.

What happens if these FHB's buy now and prices do keep sliding? Will you be satisfied if they find themselves in negative equity? Or will you just go 'who cares, I purchased my house 20 years ago and look how well that worked out for me...'.

I mean you were probably saying exactly the above in 2021 when others here were warning about the low equity lending then saying many of those buyers may well find themselves in negative equity in a few years time - and exactly that has happened for thousands of FHBs.

Credit availability from your favourite bank feeds directly into house price inflation.

You may enjoy the 2010 prices comming back soon then JJ?.........everyone loves reliving history, now dont we:)

For once I agree with you. 20% min would also keep many buyers out of the market and put downwards pressure on prices overall however.

Why not make it 40%, lock FHBs out completely so everyone else can enjoy cheaper prices.

That is a stupid strawman argument if ever I saw one.

Tells us one thing: there are still people looking to buy houses they can't afford.

"The latest Reserve Bank (RBNZ) figures show banks approved 1537 low equity mortgages to first home buyers in March, making up 45.3% of all mortgage approvals to first home buyers in the month."

Thought the LVR restriction was 25%?

LVR lending restrictions apply to ALL mortgage lending, not just first home buyers.

Ah...yes have reread and see the out

If rents are high enough it makes sense to try and catch a falling knife.

Well a lot of renters are prob doing the math as follows:

1) rents high

2) wages ok

3) prices already corrected

4) life moves on

5) waiting forever has a cost

Rents have been dropping and supply is relatively high (minus Greymouth due to the mining anticipation).

Yeah sure, in some regions. But rent levels are only one input. Stability, building equity, and the cost of waiting matter too

Building equity is your recency and rose tinted bias.

Equity loss and the worst side of negative equity is the reality now, since 2019.

New FRED chart shows another continuation of NZ Housing losses.

The investment world flipped a 180 in 2021 and many are still ostrich ass up and head in sand.

Renters have been winners in recent years, saving "hundreds of thousands" in losses V home buyers.

2010 prices maybe the floor in this still deflating NZ housing crash.

Not everyone views their own home as a trading chart, Gecko. Stability and life timing matter as well.

Wrong.

Most people DID look at it, as a CANNOT LOSE, trading chart.

It was awfull. Greed on steriods. Glad it ended in the crash, as as we are perhaps midway through, or just 25% in.

The ending of the foolish cheering on of housing gains, is the greatest time, to now live within.

Gecko is always loves seeing families housed and at fair prices.

Bring on the much lower, future DTIs OF 4x, and then house price stability!

Being glad some families are now seriously under water is a strange victory lap. Wanting fair prices is one thing but celebrating negative equity is another. And “midway through / 25% in” still sounds more like fortune telling than economics…

I was one of just handful of others, that WARNED of the dangers of negative equity, since 2007 (Yes 2007) as I WARN today!

- Buy todays at Still Bubble prices, at your peril.

Many called such warnings as delusional, you "could not lose" on property. History has revealed, who was in fact deluded.

I take no glee as being correct and the warning remains, offer only in the range of 2010 to 2015 prices, or walk. It is coming, simple.

If you’ve been calling danger since 2007, thats nearly two decades of warnings through one of the biggest housing runs in history.

Being wrong for 15+ years and then finding one downturn aint the same as being right on timing. And “2010–2015 prices, simple” is just another dramatic projection dressed up as certainty

Big G, I love ya…but if someone has been waiting since 2007 for a green light from uncle Gecko to buy their family home then I think that might’ve done more harm than good 😮

Completely get it from 2020/2021, it was mental…but from ‘07 is wild

There was short periods in the intervening 19 years, where property was not insanity priced and buying was possible at just High DTIs and not financial insanity DTIs.

The Delusion of the masses can span years, as we have seen.

So its gone from “walk” to “there were short periods where buying was okay.” Funny how the entry windows appear after the event

Last time it was ok to buy, at reasonable DTIs, WAS THE EARLY 2000s.

Since then it was high to insane multiples.

Buying any property, without a 7% rental yeild was risky. A gamblers dice roll.

Face it and position yourself - The biggest crash since the 1970s has begun.

Right so now we have “Only safe to buy in the early 2000s” which is a pretty a brave call from someone who appears to have spent 20 years waiting for society to collapse

Imagine missing two decades of ownership, equity gains, inflation shrinking debt, and principal paydown...then strutting in from the sidelines like a genius lol

The 7% yield rule is basically comedy as well. Which by that logic most of New Zealand should never have bought a house. Yet millions somehow housed families, built wealth, and moved on without consulting the Gecko Crayon Chart.

“The biggest crash since the 1970s” is your same old annual blockbuster: loud trailer, no release date.

Gecko Translation: “I missed the last 20 years, but this next downturn is definitely gonna be my moment”

Hey WellyPI, obvious a cloaked and forlorn property investor.

-Sorry you seem to be bag holder, without market love or return.

Like your ole mate Luxy, I don't need any market crash, to make it big. 'Im in housing already and Im sorted" - But don't feel the need to crassly crow on it.

Agree however, should alter to: Current NZ Housing Crash - "Destined to be much bigger than the 1970s housing market crash".

Release date: 2021 Bottom 2028.

(Worse case scenario is the Japan housing crash model, so 2041, if the first bottoming does not hold)

https://fred.stlouisfed.org/series/QJPN628BIS

Study and learn youngins!

“Study and learn youngins!” says the bloke posting a Japan chart like New Zealand and Japan are the same place lol.

Different demographics, different immigration, different land supply, different banking system, different zoning rules, different debt setup, different culture. Small details apparently...

So now the call is: crash began in 2021, bottoms in 2028... unless it doesnt, then maybe 2041. Strong stuff. A 20-year prediction range is basically astrology with spreadsheets.

And “Im sorted already” from someone posting daily housing doom myths is always funny. People who are genuinely sorted dont usually keep writing sequels.

Gecko translation: “My first call missed, so Ive moved the goalposts.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.