Heartland Group Holdings says it has signed a deal with TSB's parent the Toi Foundation to buy TSB in a deal valued at $620 million to create "a New Zealand challenger bank of scale with a regional focus" named TSB Heartland Bank.

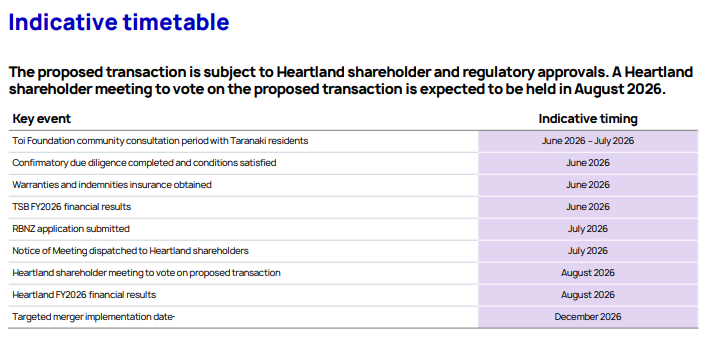

The proposed deal is subject to satisfaction of a number of conditions including community consultation by Toi Foundation with Taranaki residents, Heartland shareholder approval and New Zealand and Australian regulatory approvals.

Heartland Group Holdings says it signed a conditional merger implementation agreement with Toi Foundation and Toi Foundation Holdings on June 1 to merge Heartland Bank and TSB Bank. The Toi Foundation, formerly the TSB Community Trust, is TSB's owner and also holds 66% of Fisher Funds Management. Dividends generated by these financial institutions fund the Toi Foundation’s philanthropic work.

Under the proposed transaction, Heartland will acquire all TSB shares on issue from Toi for $620 million funded in a range of ways (see more below). Immediately following the acquisition, Heartland Bank and TSB will merge via what's being described as "a short form amalgamation" to create TSB Heartland Bank.

Heartland says the proposed merger will create a New Zealand challenger bank of scale with a regional focus, saying it will increase banking competition and choice for New Zealanders.

"It will be a full-service capable bank differentiated by its specialist product offerings, with a lower risk-weighted product portfolio," Heartland says.

Following the announcement, Heartland's shares were up more than 13% at $1.29 on the NZX in late morning Tuesday trading.

'All feedback will be considered'

Toi Foundation chairman Chris Ussher says Taranaki residents are invited to provide written feedback on the proposed TSB sale. Ussher says all feedback will be considered before the Toi Foundation's trustees make a final decision on whether to sell TSB.

Public meetings will also be held, with support required from eight of the Toi Foundation's 10 trustees to get the deal over the line, says Ussher. The Foundation is a charitable trust.

"The conditional proposal would see TSB and Heartland Bank merge to form TSB Heartland Bank, which would be a larger New Zealand challenger bank with a continued strong association with the Taranaki region, complementary products and services, and an improved long-term performance outlook," Ussher says.

If the deal goes ahead, one Toi Foundation nominee would be appointed to the Heartland Group board, and two existing TSB directors would join the TSB Heartland Bank board.

"The structure of this proposal would enable Toi Foundation to continue to support the merged bank’s strategic direction through its Heartland Group equity stake and governance role, while also freeing up capital to better support philanthropic giving in Taranaki," Ussher says.

"We fully recognise the importance of TSB in the Taranaki community and for customers all over New Zealand. The intent of the merger proposal would be to make TSB Heartland Bank a significant challenger bank that has greater scale to support its ability to compete against larger banks, is commercially strong and backed by specialist products."

"Importantly, there is an agreed intent that, if the proposal proceeds, there would be no changes to the range of current TSB customer products or services, and TSB Heartland Bank would continue to be regionally focused, with specialist teams retained in Taranaki to support future growth. TSB Heartland Bank would continue to have a close association with the Taranaki region,” Ussher says.

"In particular, the ability to increase returns from our investment portfolio will have a significant impact for people in Taranaki, especially in Toi Foundation’s key focus areas of improving the environment, enhancing child and youth wellbeing, and empowering Māori aspiration. We look forward to hearing the community’s views."

Ussher says Toi's estimated annual dividends from TSB Heartland Bank would be around $30 million, compared to the average of about $10 million from TSB over recent years. (See more from Ussher and Toi here).

Heartland Group CEO Andrew Dixson says the combined bank would increase banking competition and choice for New Zealanders.

"By bringing together Heartland Bank’s specialist product strengths with TSB’s strong funding base and everyday banking capability, we can offer more New Zealanders a better‐value alternative – with the scale to keep investing in products, technology and resilience," Dixson says.

The Toi Foundation says the proposed deal follows an unsolicited approach in 2024 regarding the potential sale of some or all of Toi Foundation’s shares in TSB.

How the takeover will be funded

Heartland says the $620 million price includes a $50 million pre-completion cash dividend from TSB. The deal also includes $250 million of ordinary equity issued to Toi Foundation by Heartland, being 200 million shares issued at a price of $1.25 per share, which represents a 17.5% ownership interest in Heartland post-completion of the proposed deal, plus $56 million subordinated debt issued to Toi Foundation by Heartland Bank as Reserve Bank eligible Tier 2 regulatory capital, and a $264 million vendor loan provided to Heartland by Toi Foundation.

"Material synergies will be progressively realised over a three-year period post-completion by reducing shared costs across TSB Heartland Bank," Heartland says.

"When fully realised, these synergies are expected to deliver a $34m per annum benefit to profit before tax. Material normalised earnings per share accretion in excess of 20% is expected to be generated in the first year post-completion based on full run-rate synergies, alongside an enhanced dividend per share profile."

"Recognising each bank’s long history and deep connection to regional New Zealand, the Heartland Bank and TSB brands will be reflected in the merged bank’s name and branding strategies. TSB Heartland Bank will continue to focus on helping New Zealanders to meet their banking needs. It is intended that TSB Heartland Bank will retain Heartland Bank’s existing nationwide presence, with Taranaki as a key operational hub for customer-based banking services – including maintaining a local branch network and customer-facing roles in Taranaki," says Heartland.

Credit rating focus

Heartland says it aims to complete the deal in December this year. Getting the deal over the line requires Fitch Ratings reaffirming TSB Heartland Bank will have a credit rating of at least BBB with a stable outlook, regulatory approvals, as required, from the Reserve Bank, Financial Markets Authority, Australian Prudential Regulation Authority, and Toi Foundation trustees completing a community consultation process with Taranaki residents and the trustees approving the sale of TSB's shares.

Below is Heartland's strategic rationale for the deal.

The proposed merger will create a New Zealand challenger bank of scale with a regional focus – increasing banking competition and choice for New Zealanders. By bringing together Heartland Bank’s specialist product expertise and TSB’s cost-effective funding platform and established transactional banking capabilities, TSB Heartland Bank will be a full-service capable bank differentiated by its specialist products, with a lower risk weighted product portfolio.

Should the proposed merger proceed, substantial scale benefits, value creation and material synergies are expected to be available.

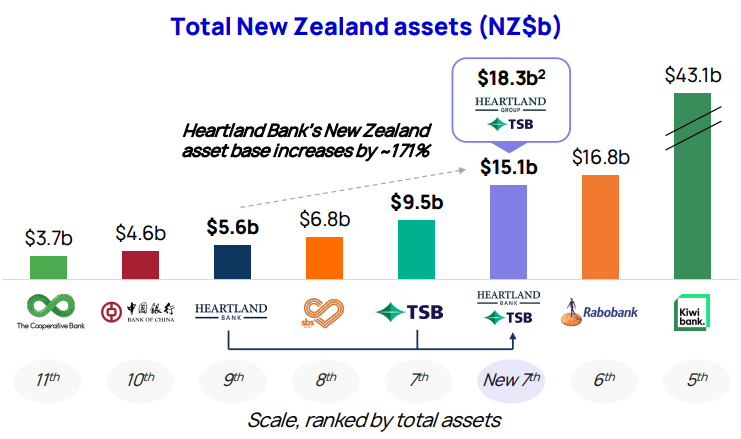

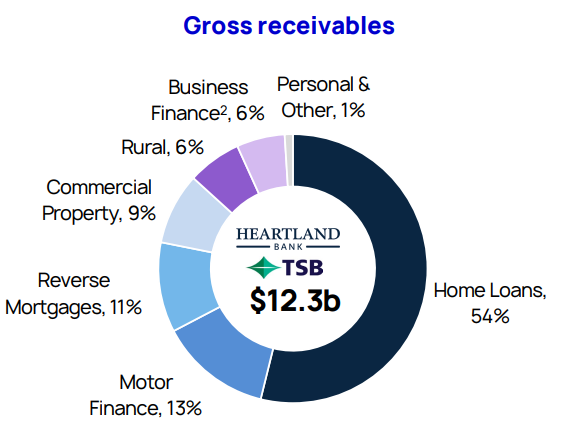

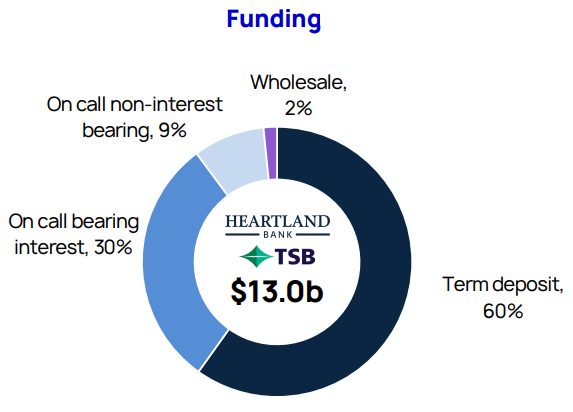

TSB Heartland Bank will become New Zealand’s seventh largest bank, with approximately $15 billion in total New Zealand assets (a 171% increase in Heartland’s New Zealand asset base). With a materially increased scale and diversified product set, it will have an enhanced ability to serve customers throughout their financial lifecycle, support a productive economy, and deliver improved financial returns. In addition, the proposed merger may support an uplift in the merged bank’s long term credit rating compared with Heartland Bank, reflecting TSB Heartland Bank’s strengthened asset quality and lower risk-weighted product profile.

Heartland’s specialist product focus across New Zealand and Australia will be retained and enhanced by the addition of full-service banking capabilities in New Zealand. As the NZX/ASX listed parent company of a larger, optimised New Zealand banking business, Heartland will have the ability to deploy capital more effectively across the group, and have the scale required to deliver an improved cost-to-income ratio through greater operating leverage.

Material synergies are estimated through cost efficiencies associated with bringing the two banks together by reducing duplication in activities, processes and shared business overheads. It is anticipated that these synergies will be progressively realised over a three-year period post-completion of the proposed merger. When fully realised, these synergies are expected to deliver an ongoing ~$34 million p.a. benefit to profit before tax.

There is also potential for further upside from funding and liquidity synergies, in addition to the ability to leverage Heartland’s investment in current and future technology programmes. Work remains ongoing in relation to technology integration costs and potential technology synergies. However, these are not expected to materially impact the proposed transaction’s financial outcomes. Total one‑off integration costs of approximately $34 million are expected to be incurred over a three-year period post-completion as synergies are realised.

The charts and table below come from Heartland.

See the Heartland announcement here, and Heartland's investor presentation here. And Toi's announcement is here.

9 Comments

wow did not see that coming.

Isn't this what Kiwibank should do? Then SBS and Coop?

"TSB Heartland Bank" seems like a mouthful.

Wonder if it's just a transition name before dropping the TSB

If their core market is the provinces, then Heartland is best on its own. But as you say, maybe they'll do an ANZ and keep the TSB name until they quietly drop it.

Similar strategy to their business in Australia I guess. Over there they bought Challenger Bank to access cheaper retail funding for the real profit engine of reverse mortgages and other specialist lending.

Building a nice business of good scale on both sides of the Tasman - I'm a happy shareholder.

Share price is up nearly 10% this morning so the market likes it too.

To me, this is an unnatural banking alignment. The deal if it proceeds, will present unique strategic and financial challenges.

Quite correct Midnight Singer.

This is a slam dunk KiwiBank purchase. I would think they were at least asked / invited to the party?

Gareth - this would be of value to readers / members for a deeper review.

HB - like many / most banks, built mostly on a history of aquisition. (MARAC, Southern Cross Building Society, CBS Canterbury then PGG Wrightson Finance

HB has a far more questionable background, loss write offs/ downs, Credit quality, Underwriting standards.

1. The culture and talent will be quite different.

2. The ultimate ownership structure of the NZX and ASX entities (NZ and Oz) is opaque [ yes, which large bank isn't?] - I thought with some involvement of Carribean companies? Probably goes against the grain of TSB ownership.

3. Term Deposits holders in TSB now have to think hard. Even with Depositor Compensation Scheme (DCS).

4. TSB had to navigate away from legacy computer and software issues and that required far more capital and subsequent cost-cutting than anticipated. Does HB have good digital systems? Who will be upgrading legacy systems here?

5. The pricing structure and Relationship Management technique is likely to be quite different.

6. If the deal is struck down by Taranaki residents and the Trustees will have a very interesting decision to make with some legal ramifications - then maybe KB are in with a look?

7. Some questions to the Minister of Finance, Chairman KB and CEO KB.

8. Capital working they way it should, or, perhaps better that KB should be growing?

9. Be interesting to get / ask for Richard Werner opinion?

HB uses Westpac to clear vs TSB having their own bank code, potential cost savings for a joint bank here.

There will be some cultural challenges, perhaps by taking the best from both worlds. I think its clear HB are probably more the risk takers.

Didn't TSB get pinged by FMA for some problems with their software a few years ago?

show me a bank that hasn't

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.