Credit rating agency S&P Global Ratings says downward pressure on New Zealand's sovereign ratings could emerge if key economic metrics it tracks, especially the current account deficit, remain weak.

S&P analyst Martin Foo sees evidence in the Government's Budget of juggling competing priorities, with it trying to both ease cost-of-living pressures, and avoid fanning the flames of already high inflation.

"The Budget revises up the projected central government cash deficit for fiscal 2023-2024, year-end June 30, to 6.5% of GDP [Gross Domestic Product]. This is a big uptick from the 4.3% deficit penciled in five months ago, and 2.2% a year ago. However, we still anticipate fiscal improvement in the subsequent years as emergency spending programs are rapidly phased out," Foo says.

"Public debt is not a material constraint on the rating. We expect net general government debt to stabilize at around 30% to 35% of GDP. We base this on our measures, which include the debts of the local government sector, and which differ from the government's own fiscal indicators. This debt ratio is mid-range out of 18 sovereigns that we rate in the 'AA' category."

"Any further new spending may stoke inflation. The budget announces cost-of-living relief and investment in resilient infrastructure, with an eye to the general election in October 2023. Up to $4 billion in reprioritizations and savings will partly offset disaster recovery costs to address $5 billion of damage to public infrastructure," Foo says.

Eye on the current account deficit

He goes on to say that downward pressure on NZ's sovereign ratings could eventuate if external metrics remain weak.

"This will be especially true if, on our preferred measures, the current account deficit (CAD) remains persistently above 20% of current account receipts, after tracking at about 25% in 2022. In the fourth quarter of 2022, the CAD widened to its highest level since the 1980s."

A current account deficit reflects that the country is spending more than it's earning overseas.

"Our base case assumes a narrowing CAD over the next three years, as slowing domestic demand compresses imports and tourism inflows rebound. Cyclone Gabrielle, however, could alter this trajectory if the rebuild drives imports higher than we expect."

S&P has an 'AAA' sovereign domestic currency rating with a stable outlook on NZ. This rating assesses the country's capacity to meet obligations denominated in the NZ dollar, which almost all government debt is issued and repaid in. It has an AA+ foreign currency rating, for obligations denominated in a foreign currency, on NZ. (See more on NZ sovereign credit ratings here, and credit ratings explained here).

To maintain these very high ratings, and because of the external vulnerabilities NZ faces, the country must deliver stronger fiscal metrics than peers, S&P says. A credit rating downgrade could increase the Government's borrowing costs.

'Gobsmacking'

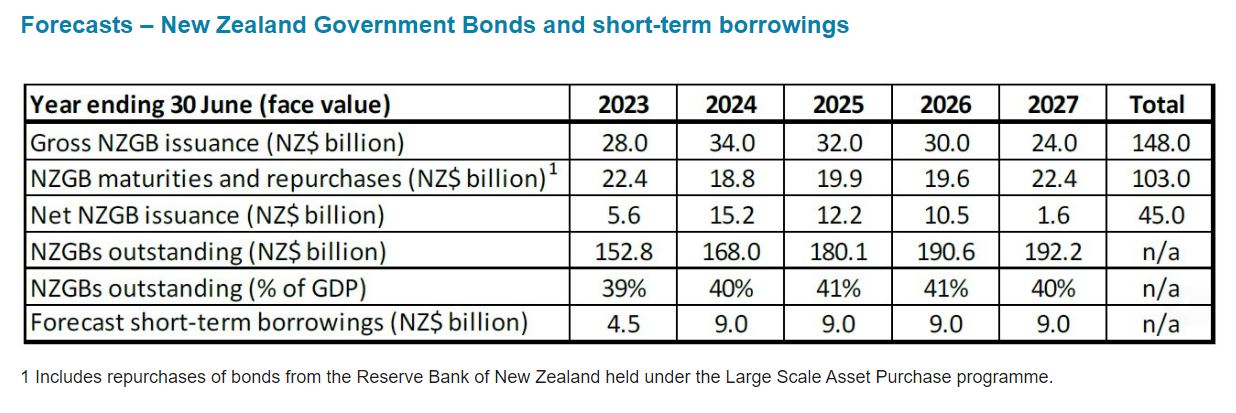

The Budget forecasts a $34 billion 2023/24 New Zealand Government Bond (NZGB) programme, up $4 billion from December's Half Year Economic and Fiscal Update. The forecast NZGB programmes for 2024/25, 2025/26, and 2026/27 have all been increased, by $2 billion, $10 billion and $4 billion respectively. Meanwhile, the forecast for the 2022/23 year is unchanged, with a $28 billion NZGB programme, NZ Debt Management (NZDM), the Treasury unit that manages government debt, says. (See table at the foot of this article).

BNZ head of research Stephen Toplis notes the total bond programme has been revised upward by $20 billion over the next four years, with "a gobsmacking" $10 billion increase in 2025/26.

"There was nothing immediately apparent in the fiscal track to explain the timing of the big lift in 2025/26. It would appear this reflects two things: (1) the earlier years’ programmes are less than might otherwise have been the case thanks to the Government running down its excess cash. (2) There is some smoothing at play," Toplis says.

'NZ’s fiscal position remains solid compared with peers'

Martin Petch, Vice President at Moody’s Investors Service, another credit rating agency, says NZ's fiscal metrics have seen a moderate deterioration through the forward estimates, largely driven by the impacts of the Covid-19 pandemic, the extreme North Island weather events and the impact of high domestic and global inflation.

"We expect fiscal repair to continue, albeit slightly delayed than we earlier expected, but will be in line with its fiscal targets. Supported by its fiscal policy framework, New Zealand’s fiscal position remains solid compared with peers’ and will likely enable it to respond effectively to economic shocks," says Petch.

Moody's has Aaa local and foreign currency ratings with stable outlooks on NZ.

'Tailwinds from low unemployment & inbound migration plus an orderly property price correction'

Foo notes NZ's economic backdrop is difficult.

"Headline inflation stands at 6.7% year-on-year, well above the central bank's target band of 1% to 3%. This is in part a hangover of hefty fiscal stimulus rolled out in 2021-2022. The 500 basis points of cash rate hikes since August 2021 are slamming on the economic brakes and precipitating an orderly property price correction," says Foo.

"The economy contracted in the fourth quarter of 2022; and another weak GDP print beckons for the first quarter of 2023 after severe floods in Auckland, and Cyclone Gabrielle, New Zealand's costliest weather event this century, made landfall weeks later."

"There are, however, substantial tailwinds from low unemployment and a recent surge in inbound migration," Foo says.

Recession risks and reconstruction costs from Cyclone Gabrielle are delaying New Zealand's post-COVID fiscal repair. If a somewhat expansionary fiscal stance adds to the import bill, this could further weaken external accounts and erode headroom for the sovereign ratings on New Zealand."

*The table below comes from NZDM. (NZDM's Director Kim Martin features in this episode of the Of Interest podcast).

13 Comments

But wait... there's election bribes to come.

Oh well that inflation rogered

'Public debt is not a material constraint on the rating.'

Excellent.

This is a bunch of people who relate to the tension on the other parachute-strings, while failing to notice the ground is approaching. All good so far...

Even as the Titanic sunk some refused to accept it could be happening....

Here we go this is the first comment - we are concerned , anyone else rememeber GFC...

Don’t be concerned, they aren’t. Best option is to make sure you have options.

Ah yes, the GFC. That was the one where S&P, Moody's et. al. rated securities as investment grade just days before they became basically worthless, destroying any shred of credibility these ratings agencies may have had left.

And not for the first time, either. I simply cannot believe that people still pay any attention to these fraudsters.

It's a bit like the whole PWC debacle across the ditch. Is anyone surprised? Do people not remember Arthur Andersen? And these are only the ones who got caught.

Looking forward to the balance of trade release at 10:45am tomorrow.... Credit agencies will be quickly updating their guidance I'd say...

let's convert to electric.... oh its all imported just like fossil fuel..... I am old enough to remember the current acc could be bumpy due to a few jet imports for air NZ.... we are so far past that now its a mess

Is GR our most incompetent finance minister in a generation?

He is no where near any past Labour finance minister.... with an amateur on the tiller the foredeck crew are nervous

The most incompetent and the most sneaky by changing the way NZ government debt is measured. Tax take has increased by 55% since he took over and they have blown the lot and more than doubled the countries debt. It would be funny if Greece did it, us, not so much.

I have seen this mentioned a number of times here. Are there any good articles which explain this well?

The bailiffs of Wall Street would wish to see an austerity black budget, but Robo isn't doing it. CPI will drag on the way down. cf 1990-91 period .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.