By David Hargreaves

ANZ NZ doesn't look as though it is going to have too many problems selling its UDC Finance arm, even though the bank's remaining coy about the prospect of a sale.

A spokesperson for ANZ NZ said yesterday that as part of ANZ’s strategy to review our focus on where it allocates capital and resources, "we explore various strategic options from time to time, although this does not mean they will be sold".

"However it remains very preliminary and no decisions have been made. It’s business as usual for UDC staff, customers and investors. If ANZ was to make a decision regarding a potential sale of UDC Finance, we would inform staff, customers and investors immediately."

The Australian Financial Review reported earlier this week that ANZ has had investment bank Deutsche Bank testing interest in the unit, introducing the business to private equity and other potential buyers in recent weeks.

If UDC is sold this will be a continuation of the enormous shake-up going on in the finance company sector in the past 12 months.

New Zealand's biggest consumer finance company, GE Money, was sold earlier last year as part of a massive deal valued at A$8.2 billion to a consortium comprising of global investors Värde Partners, private equity group KKR, and Deutsche Bank.

Then the Australian financial services company Flexigroup bought Fisher & Paykel Finance late last year.

Just as an early guide, if UDC were to be sold on a similar kind of valuation basis to F&P - which was 9.9x cash earnings before any merger synergies, then the price would likely be at least $600 million or so, though early market estimates have suggested as much as $700 million.

And while the ANZ is being non-commital about a sale prospect, offloading UDC would certainly fit with its recent strategy in the light of the sale of its Esanda car dealer finance business to Macquarie Group last year. Early last year when stories of the planned sale of the Esanda assets emerged ANZ NZ at that stage said it had no plans to follow suit with UDC Finance. Clearly that has changed.

Private equity groups have quickly emerged as market favourites to be successful bidders, but Heartland Bank has been quick to raise it's hand as a potential buyer and even TSB Bank's reportedly not ruling out having a go. It's also been speculated that the ANZ could even float off UDC on the stock market.

The emergence of Heartland, a fairly similar-sized business, is interesting

What are the various potential bidders looking at buying?

UDC's been around since 1937 and boasts a strong AA- credit rating - but that does of course reflect the support of ANZ. Depending on who bought the business its rating would likely drop, which potentially would have an impact on profitability.

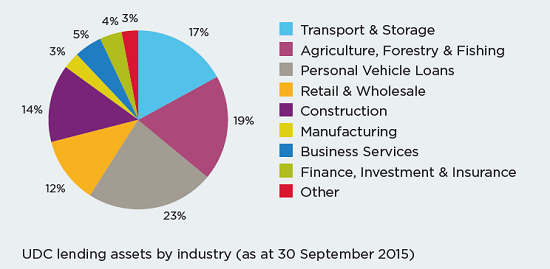

In UDC's own words: "Our main expertise is in providing asset-based finance to New Zealand businesses for purchasing plant, vehicles and equipment, helping them to grow and prosper. We do not rely on land or buildings as security, and we steer well clear of speculative property developments."

As reported by interest.co.nz's Gareth Vaughan at the time UDC's September year results featured record annual net profit after tax of $57.05 million, up $5.5 million, or 10.7% year-on-year from the company's previous record annual profit.

The annual results showed operating income up 6.3% to just over $122 million and operating expenses up 3.1% to $32.3 million. Net interest income rose 5.4% to $116.24 million, and UDC's credit impairment charge fell 11.1% to $10.4 million.

UDC's total provision for credit impairment was almost 1% lower at September 30 from a year earlier at $31.5 million. Gross lending rose almost $89 million year-on-year, or 3.7%, to $2.517 billion. UDC's assets over 90 days past due were 23% higher at $6.4 million, and its net individually impaired assets were almost 5% higher at $9.2 million.

UDC said at the time that the new financial year to date - October and November, had continued strongly with more than $100 million of new lending per month over recent months. Key growth areas were motor vehicles, construction and road freight.

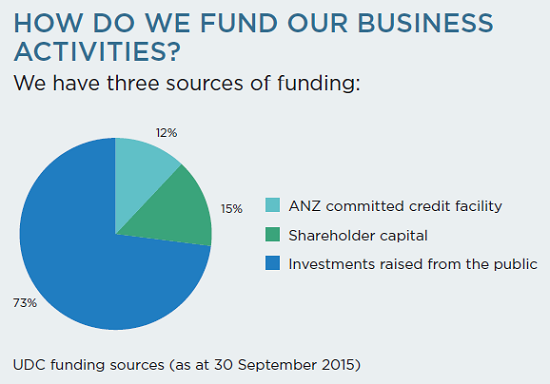

On the funding side UDC's debenture book grew a shade under $167 million in the September year, or 10.6%, to $1.736 billion. The company said the reinvestment rate was over 60%, similar to the previous year. UDC also has an $800 million credit facility from ANZ, which was $280 million drawn down at September 30, down from $395 million a year earlier.

The company's regulatory capital ratio was unchanged year-on-year at September 30 at 16.2% versus the 8% required minimum.

For the September year UDC paid ANZ an ordinary dividend of $33 million, or 63 cents per share, up almost a third from $25 million, or 48 cents a share, last year.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.