Heartland Bank CEO Jeff Greenslade has put the spotlight on the demise of the traditional bank branch in his speech to the bank's annual meeting.

Greenslade also reiterated Heartland's forecast for June 2018 year net profit after tax of between $65 million and $68 million, an increase of up to 12% from $60.8 million in the June 2017 year.

Speaking much more frankly about the future of bank branches than bank bosses whose banks have big branch networks do, Greenslade told shareholders the bricks and mortar approach to banking is "showing signs of obsolescence." Heartland has just six branches in Takapuna on Auckland's North Shore, Hamilton, Tauranga, Wellington, Riccarton in Christchurch, and Ashburton.

Greenslade said Heartland will continue expanding its digital analytics and platforms, which he described as the pathway to lower marginal costs and scalable reach.

"While some understandably lament the decline of branch banking, the bricks and mortar approach is not something we can compete in and is showing signs of obsolescence," said Greenslade.

"We do not have branches in a conventional sense any more. This has not impacted on our all-important deposit raising needs. Our customers are busy, live remotely or are unwilling to fight the traffic to go to a bank. With digital platforms, Heartland can get to every New Zealander at a lower marginal cost. For example, we regularly get up to 1,000 potential customers visiting our deposit platform each week and 600 visiting our SME [small and medium-sized enterprise] working capital platform compared to the 20 to 40 customers per week that used to visit some of our branches. Digital allows a small bank to operate with the similar scale of larger banks and to offer speed as a point of difference," said Greenslade.

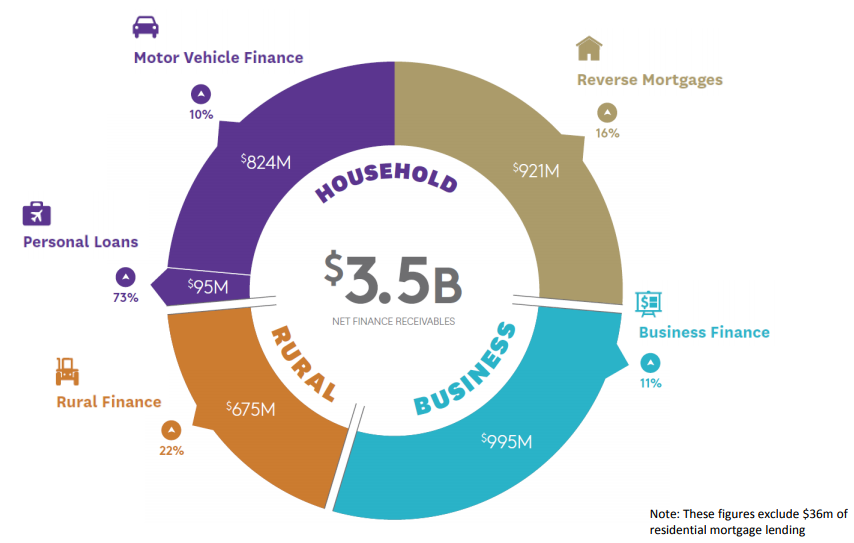

He pointed to Heartland's digital services offering livestock finance, personal loans, SME working capital finance and deposits, noting "significant opportunity" to build on these.

"We aim to have one of the world’s first end-to-end deposit platforms. For small business finance, we have the largest SME platform in New Zealand and our aim is to have one of the largest in Australasia. We will continue to provide telephone or in-person based services, but our objective is to have the majority of our products initiated or sold online."

Formed through the merger of Marac Finance, CBS Canterbury and the Southern Cross Building Society in January 2011, Heartland gained banking registration from the Reserve Bank in December 2012. Heartland targets niche markets such as reverse mortgages, vehicle lending and livestock finance where bigger banks are not aggressively competing.

Greenslade said Heartland's aim is to shift origination, or how it acquires customers, as much as possible onto digital platforms.

"People will remain a key part of our customer interaction, but will be positioned to where we can best add value," said Greenslade.

"This strategy is in contrast to many other banks operating in New Zealand which tend to operate a 'one-stop shop.' They offer a suite of products hoping to use one to entice customers to buy more, this is otherwise known as cross-selling. Pricing often plays a major part in this, as does physical distribution; two areas where we have no competitive advantage."

"This traditional model is increasingly coming under pressure from disruptors who offer simpler single lines of services or products that can be accessed quickly. This is responding to a growing customer preference for clarity and speed. Put simply, people of all ages and demographics are becoming less inclined to stand in queues. Less inclined to be cross-sold to, they just want what they want and preferably now. It is the demands of this segment of the market that we wish to target, whether it be in the business, household or rural sectors," Greenslade added.

The least expensive way to do this, Greenslade said, is through digital distribution or through intermediaries.

"We have used intermediaries successfully in the past, whether motor dealers or the Harmoney [peer-to-peer lending] platform, but the future direction will be increasingly based on digital distribution," said Greenslade.

Part of this digital strategy, he added, is harnessing data to identify risks and opportunities.

"We are investing in analytical tools to provide streamlined credit decision making with the capability to create more predictable outcomes. Similarly, we are developing means to anticipate customer needs. Traditionally, the financial industry has been built on the assumption that we, the bank will give you what we’ve got when you come to us. Ultimately we must be able to tell our customers what they need before they know it. If we wait for our customers to come to us, it is too late."

Heartland is currently looking to raise about $59 million of capital to support lending growth. The capital raise is being done via a pro rata rights offer giving eligible shareholders the chance to increase the number of Heartland shares they hold at a discounted price. (There's more detail here). On Tuesday afternoon Heartland's shares were down 1.52% at $1.94.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.