Here's something a bit different today.

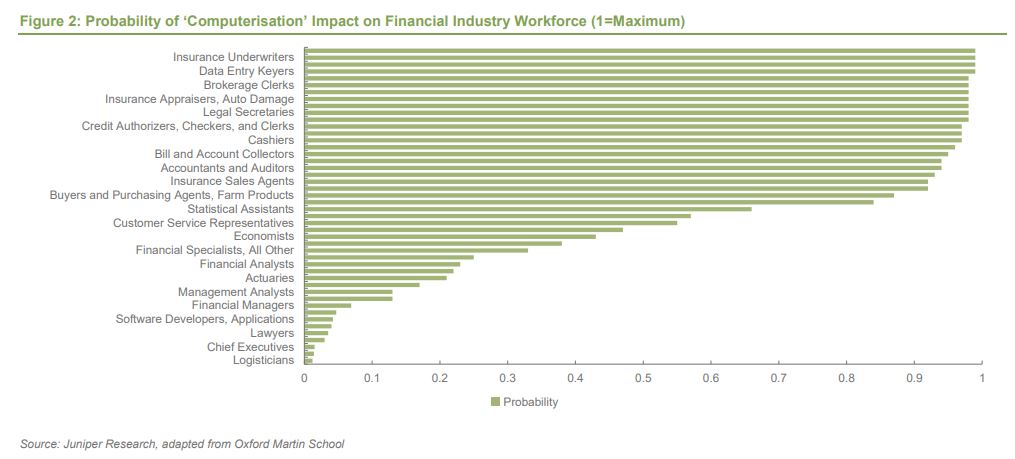

Firstly, Juniper Research estimated which jobs in the financial industry are most likely to be "replaced by sophisticated algorithms" (machines) in the automation revolution. The news is a lot better if you're a lawyer, chief executive or logistician than it is if your occupation is among the following; insurance underwriter, cashier, insurance appraiser, bill and account collector, legal secretary, accountant or auditor, and credit authorizer.

"The impact of AI-driven automation on the workforce is often discussed in terms of its implications," Juniper says. "It is certainly an accepted viewpoint that jobs that require a great deal of routine can more efficiently, in terms of cost and speed, be replaced by sophisticated algorithms."

"There are a number of such jobs extant in the financial industry today; meanwhile, the fact that much of the industry is data-driven means that the scope for automation in terms of impact is broad. Indeed, a 2013 study conducted by the Oxford Martin School at the University of Oxford calculated the probability of ‘computerisation’ impacting a range of jobs," says Juniper.

Juniper collated the data, as shown below. (If you're having trouble reading that, it can also be found in this Juniper report.

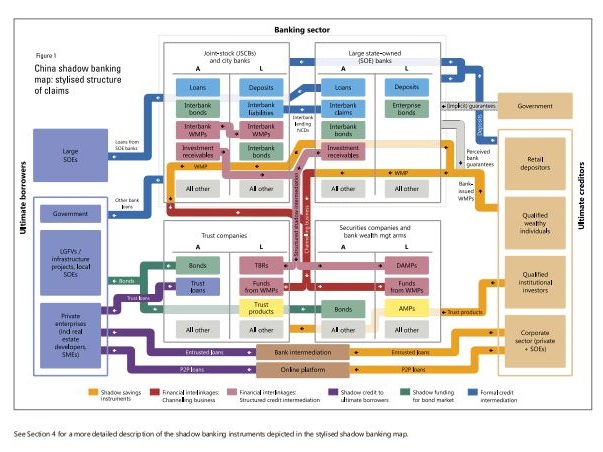

'Banks the central player within China’s shadow banking system & providers of implicit guarantees'

Off on a totally different tangent, a Bank for International Settlements (BIS) working paper has shed some much needed light, in the West at least, on the Chinese shadow banking sector. And surprise, surprise, Chinese banks are up to their necks in it.

"All types of commercial banks in China, but especially the smaller joint-stock and city commercial banks, are actively and directly involved in shadow credit intermediation. In the process, they create tight interlinkages between formal and shadow banking activities and entities. A significant share of the proceeds from bank issued WMPs [wealth management products], for instance, are channelled into trust products ('channelling business'). Further, banks hold TBRs [trust beneficiary rights] which are participation rights to the proceeds from trust products issued by a trust company," the paper, authored by Torsten Ehlers, Steven Kong and Feng Zhu, says.

"Besides their direct role, banks facilitate shadow credit in various ways. For instance, since direct loans between non-financial firms are legally not permissible, banks act as the trustee and middleman of the so-called entrusted loans between firms. The trustee bank collects the principal and interest and charges a handling fee. It either does not take credit risk in the process, or absorbs part of the credit risk through so-called entrusted rights. By distributing and intermediating a wide range of shadow banking products themselves, as well as on behalf of other entities, banks are the central player within China’s shadow banking system. In this role, banks are perceived as providers of implicit guarantees to their customers in case of defaults, even though they have no such legal obligation."

"More recently, banks have resorted to a combination of existing shadow credit instruments to reduce regulatory burdens. Through this 'structured' form of shadow credit intermediation, bank assets are reclassified into investment receivables. Banks can thereby lower non-performing loan provisions and alleviate loan-to deposit ratio constraints," Ehlers, Kong and Zhu write.

The three developed a "stylised shadow banking map" for China that aims to provide a coherent picture of its structure and the associated financial system interlinkages.

"Five key characteristics emerge. One defining feature of the shadow banking system in China is the dominant role of commercial banks, true to the adage that shadow banking in China is the 'shadow of the banks'. Moreover, it differs from shadow banking in the United States in that securitisation and market-based instruments play only a limited role. With a series of maps we show that the size and dynamics of shadow banking in China have been changing rapidly. This reveals a marked shift in the relative importance of different shadow banking activities. New and more complex 'structured' shadow credit intermediation has emerged and quickly reached a large scale, while the bond market has become highly dependent on funding channelled through wealth management products. As a result, the structure of shadow banking in China is growing more complex," the paper says.

Their map is below. If you're having trouble reading it, the BIS working paper is here.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.