OMV says its ability to increase natural gas prices, should it be allowed to buy Shell’s New Zealand assets, would be constrained by the fact these assets are reaching the end of their life.

The Austrian oil and gas giant makes this point in its merger clearance application, just published on the Commerce Commission’s website.

It argues that even though an acquisition would see it increase its market share, this share would drop off over time as the reserves of the fields it would be acquiring have nearly been depleted.

OMV expects Pohokura - New Zealand’s largest gas field - to “come off plateau” in the next year or two and “gradually decline towards its end of field life from then”. It’s proposing to increase its stake in this field from 26% to 74%.

As for the Maui field, which OMV is proposing to increase its stake in from 10% to 94%, its reserves are expected to be depleted by 2023 if no new finds are made or existing reserves enhanced. The “best case” scenario is that Maui continues to operate until its permit expires in 2036.

OMV therefore asks the ComCom to focus on different producers’ market shares of reserves, rather than production, as it weighs up its application.

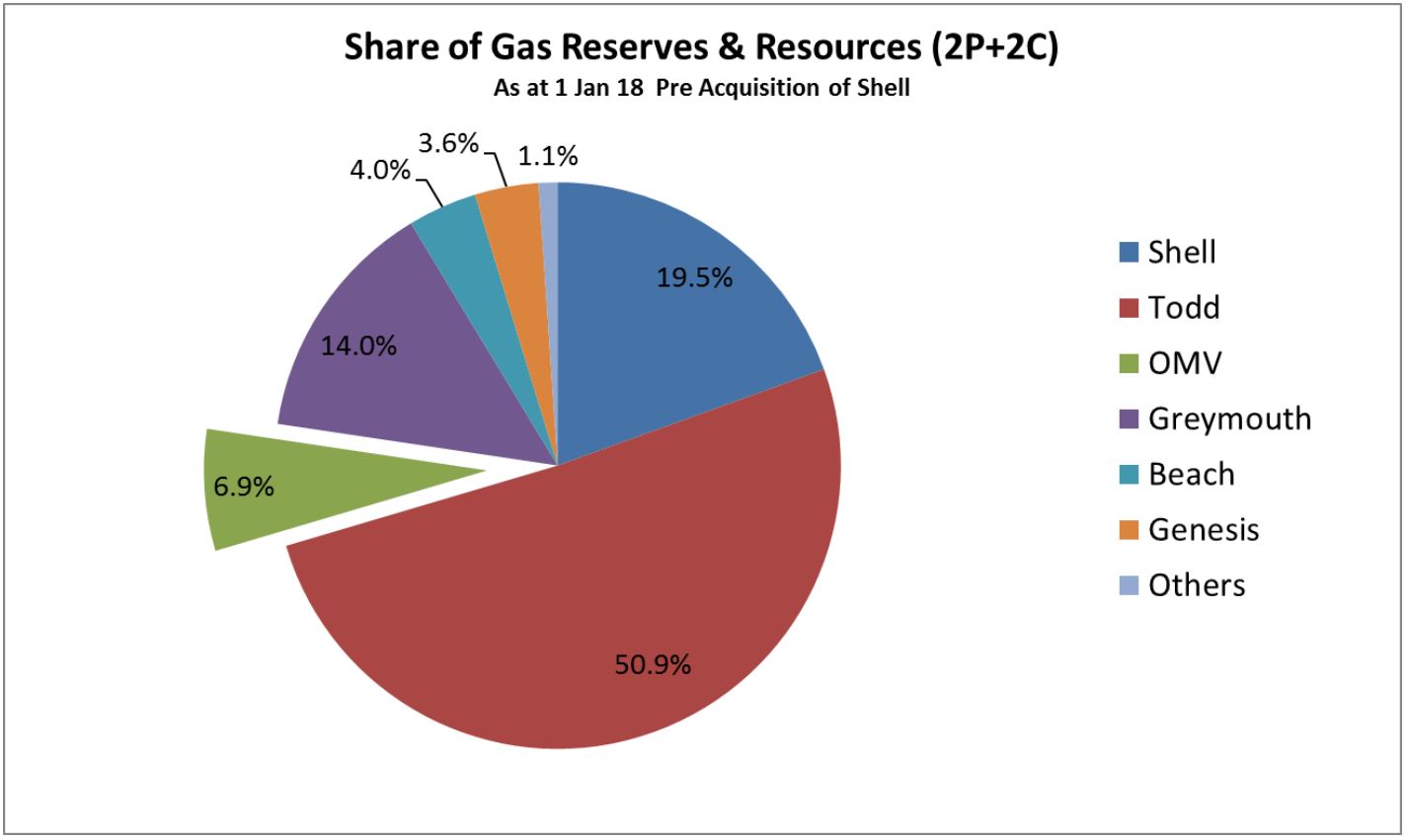

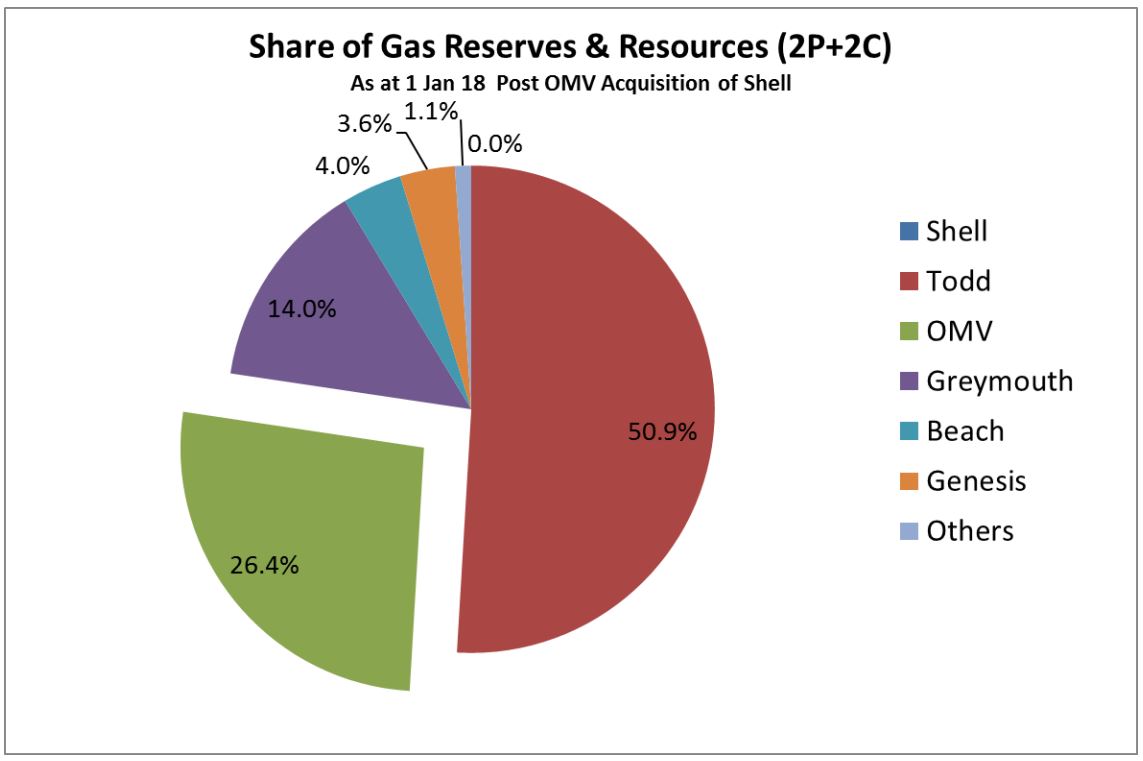

While just over 53% of all the gas produced in New Zealand (gross) in 2017 came from Pohokura and Maui, the “proven and probable” and “contingent” reserves OMV will have post-acquisition will be much lower than that of Todd.

OMV’s share will have increased to 26% from 7%, while Todd’s will be 51%.

If “contingent” reserves are taken out of the picture, Todd’s share of “proven and probable” reserves would sit at 37%, while OMV’s will be at 28% post-merger.

Yet OMV argues Todd’s “contingent” reserves should be counted, as it’s likely they’ll be used in the near future.

“Post-acquisition OMV will continue to face strong constraints from other market participants,” OMV says.

Prices restrained by existing contracts

While OMV argues this depleting reserves situation will affect its ability to increase prices longer term, in the short term it will be constrained by the fact a “significant percentage” of gas production from Maui and Pohokura has been contracted. The expiry dates of these contracts have been redacted from the publicly available document.

“When customers do come off contract, they have the ability to switch suppliers, which acts as a constraint on price increases for natural gas,” OMV says.

“This gives large customers (and competitors) such as Methanex, Genesis, Vector and Contact countervailing buyer power.

“Importantly, when customers do come off contract, Todd and Greymouth will hold the bulk of uncommitted (ie uncontracted) gas reserves going forward from 2019.”

New oil and gas exploration ban irrelevant

OMV (which entered into its agreement with Shell in March) doesn’t make mention of the Ministry of Business, Innovation and Employment saying the ban of new offshore oil and gas exploration, announced in April, risks putting upward pressure on domestic gas prices.

It says the announcement doesn’t affect the “relevant markets in the present case since the decision does not impact on current reserves or the potential finds from current exploration permits”.

OMV goes on to say the wholesale gas price has been declining since 2010; the proposed merger not expected to affect this trend.

Commenting on supply, it says: “While the re-estimation of the Pohokura field reserves has resulted in a reduction in overall gas reserves, this should be counteracted over time by the contingent resources coming into production.”

An acquisition would also see OMV’s share of the LPG market rise. It argues the increase would be by an immaterial amount.

OMV’s acquisition of a variety of infrastructure assets associated with the transportation and storage of petroleum assets, are also not expected to cause competition issues.

Overall, OMV says that if it didn’t agree to buy Shell’s assets, another purchaser who participated in the “competitive tender process and reached a late stage of that process”, would have.

8 Comments

http://fortune.com/2018/01/24/royal-dutch-shell-lower-oil-prices/

The withdrawal is understandable. The question is: What is Shell, Statoil - or anyone - worth below an EROEI of, say 11;1?

Jenee, if you haven't yet read it, here's some essential homework. Best link you'll read all year:

https://www.tullettprebon.com/.../1%20-%2021.01.2013%20perfect%20storm%…...

There is a bit more to it than just that IMHO. ie if you own a depleting reserve than the value of that "essential" reserve climbs. At least that is what most assumed, ie $300 a barrel? $500? no problem. The reality it is however different its only worth what ppl and economies can afford or want to pay. Then there all the addon smoke and mirrors like EVs making it even harder to see things out ahead. Finally of course we want a solution so will grasp at it no matter how farcical or tiny.

Shurely there are three elements to this proposal:

- The existence of contracts which constrain prices until the contract periods end

- The existence of competitors who can compete on price while carefully avoiding even the merest whiff of a Cartel or Duopoly

- The non-existence of reserves beyond depletion point, being as how exploration for them has been deemed Haram by Them Who Know Best

So the most likely price scenario is a plateau or thereabouts, until the contracts at #1 end, then a carefully executed but inexorable rise until the resource runs out. The price bound for the time approaching the depletion point is the price of imported gas (assuming that someone has been astute enough to get an import terminal up and running). There might even be a price hump in order to take profits to the depletion point, plus build that there Terminal.

But in the meantime, given that everything runs out in 2036 permit-wise - 18 years away - what will happen in the meantime apart from price? The example of the logging industry gives us a clue:

Assets will be immediately put on care&maintenance, and capex severely limited. Just as a logging tramway bridge was ideally designed so that it collapsed a few seconds after the very last ever bogie set traversed it, O&G assets will be sweated hard, the objective being scrap value only at depletion point, unless they are useful to the Import Terminal. The workforce, similarly, will be put on shorter and tougher contracts locally, and encouraged to look overseas for real advancement. There won't be much training or re-skilling for older staff, because they are like that tram bridge.... If Gubmints attempt to extract more moolah for reinstatement, reskilling, etc., this will immediately cause increases in product prices because assuming there is no Terminal yet in existence, there is no alternative product and producers are in the box seat, just as Russia is to Europe currently. Any whiff of rebellion and the tap gets turned off.

One does hope that folks are thinking about this - 18 years is a short enough period to get alternatives arranged especially considering the consent processes - there'll be Snails, Geckos (Geckoes??) and Dolphins galore to wade through to get anything actually built. 8-10 years for consents alone.....

One has to feel a little pity for all of those Gas-Only houses. Instant Hot water! There'll be plenty of That if the gas fields run out and no-one has thunk up and Built an Alternative....

3. in fact its very likely there is no huge reserves left and these would deplete anyway, therefore moving to renewables which is the sensible way forward and hence why the policy has been put in place.

" those Gas-Only houses" rare or non-existant if we mean mains reticulated supply ie few if any houses do not have mains electricity and a sunny roof. For the houses that do not have all three, well I have a mate who faced with a 20K+ bill to put in power to his new build put a huge solar panel and batteries in instead fpr less $s. It isnt rocket science and in fact its jobs.

Waymad - it's the energy wot underwrites real wealth, so if the 'price' is upped in a bidding-war for what remains, it will be being upped on the basis of unrepayable debt.

Which is where we are now - the global debt is unrepayable. Which raises the question of why we still value things in a system which isn't indexed to reality. Bitcoin has the same problem.

I recall Judith Collins being interviewed on TV months ago and saying we have massive gas reserves so where are the figures coming from that indicate how low the reserves are?

Is this her fantasy or a ruse?

You have to be careful with comments like 'massive'.

Brownlee was the classic re Southland Lignite - "There's x hundred years of it".

The question is always "At what rate of consumption'?

Grow your consumption exponentially, and the time shortens exponentially.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.