By Andrew Coleman*

This appendix considers the extent that residential property income is taxed less than other commonly held assets. It makes the comparison with income from directly held interest-earning securities such as bank accounts, and income from interest-earning and equity securities held in KiwiSaver and other retirement income accounts. These are the most commonly held classes of assets in New Zealand.

New Zealand taxes nominal interest earnings. While the effective tax rate on nominal interest earnings is the standard income tax rate, the effective tax rate on real interest earnings is much higher than the statutory rate when the inflation rate is positive because the inflation component of nominal interest rates is taxed. This raises the effective tax rate on real interest payments by an amount (1 + π) i / ( i - π) where i is the nominal interest rate and π is the inflation rate. For instance, if the nominal interest rate were 4% and the inflation rate were 1.5%, this would increase the effective tax rate by more than 60 percent. For someone facing a 33% marginal tax rate, the effective rate on real interest income in this case would be 54%.

Income earned in most KiwiSaver accounts is taxed either at a 28 percent rate or at the appropriate PIE rate, depending on the scheme. Nominal interest income and dividend income are both taxed at these rates. In general, capital gains from investments in New Zealand and Australian shares are not taxed, but the taxation of other capital gains depends on the exact structure of the fund. Thus real income from debt securities held in KiwiSaver accounts is taxed at rates higher than statutory rates, because the inflation component of income is taxed, while real income from equity securities held in KiwiSaver accounts is likely to be taxed at rates lower than statutory rates, because capital gains are not taxed.

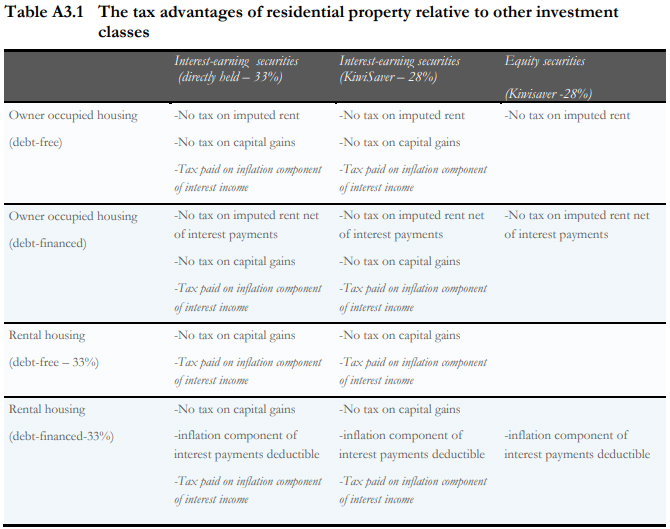

Table A2.1 indicates the major tax advantages of owner-occupied and rental property investments relative to interest-earning securities and KiwiSaver accounts. The extent of the tax advantage varies across the twelve possible comparisons, but in all but two cases (rental property investments versus equities held in KiwiSaver accounts) property is tax advantaged. These differences are discussed in detail below.

Approximately half of all owner-occupied housing is owned debt free. The tax rate on income from debt-free owner-occupied housing is lower than the tax rates on income from either debt or on KiwiSaver assets. According to the Haig-Simon definition, the income from debt-free owner-occupied housing is the implicit rent earned from the ‘housing services’ generated by the property plus any change in the real value of the property. The change in the value of the property should include the effects of depreciation. Neither of these components are currently taxed. Moreover, real income from interest-earning accounts are over-taxed in an inflationary environment. Consequently, income from owner-occupied property is taxed substantially less than income from interest earning securities, whether these are held directly or in KiwiSaver accounts. Income from owner-occupied property is also taxed less than the income from equity securities held in KiwiSaver accounts, for while both are largely exempt from capital gains taxes, dividend income is taxed but the value of imputed rent is not.

A neutral tax regime for debt-financed owner-occupied housing is similar, except the owner of the property should be taxed on the imputed rent net of real interest payments, and the holder of the debt security should pay tax on the real interest payment. Since real interest payments are not deductible, debt-financed owners of owner-occupied property are less tax advantaged than debtfree owners of owner-occupied property. Nonetheless, real capital gains are still tax exempt, and in circumstances where capital gains are large and expected to continue, debt-financed property is still likely to be tax advantaged relative to interest-earning securities.

The tax situation for owner occupiers is complicated by local government property taxes. In 2013 local government rates totalled $4.6 billion, of which approximately 30 percent was paid by non-residential entities.42 As the value of residential property services was $29 billion, or 4.3 percent of the estimated value of property, the average rate of local property taxes was 11 percent of the value of residential property services.43 If these payments were a proxy for income tax payments, they would need to be counted when comparing the income tax paid on property income and other classes of capital income. These payments are not income taxes, however, just as tobacco taxes are not income taxes, and under the current tax regime they should not be treated as such, partly because the incidence of property taxes does not normally fall on those paying the tax.44,45 Consequently, they need not be counted when comparing taxes on different classes of capital income. Even if they were counted, income from owner-occupied property would still be taxed lower than normal rates, as the average local property tax rate is much lower than normal income tax rates.

Taxes on rental property are less than they would be under a neutral tax system for two reasons. First, real capital gains and losses are not taxed. The treatment of capital gains and losses is particularly complex, for while depreciation allowances should be incorporated into the calculation of capital gains and losses, they are not. Consequently, neither capital gains nor losses are taxed appropriately. Secondly, investors who borrow can deduct nominal interest payments rather than real interest payments from their taxable income even though the inflation component of interest payments is properly treated as a real debt repayment. This factor is sizeable: in March 2017, mortgage debt held against rental property was $67 billion.46 When the inflation rate is one percent, this means the interest deduction that is claimed by residential landlords is approximately $700 million too large, a subsidy worth over $200 million.

Investments in leased residential property are taxed lightly relative to interest-earning securities because real capital gains are not taxed, the inflation component of interest payments is deductible, and the inflation component of interest income is taxed. Investments in leased residential property are taxed lightly relative to equity investments held in KiwiSaver accounts because the inflation component of interest payments is tax deductible.

To summarise, both owner-occupied and rental property are taxed less than the two most common alternative forms of investments, interest-earning securities and KiwiSaver accounts. Debt-free owner-occupied property is particularly tax advantaged relative to interest-earning securities but is also tax advantaged relative to equity securities as imputed rent is not taxed. The tax advantage of debt-financed owner-occupied property is smaller, as mortgage payments are not deductible, but for households expecting to be debt free at some stage owner-occupied property is taxed at significantly lower rates than interest-earning securities. The tax advantages of rental property relative to interest-earning securities occur because capital gains are not taxed, and the inflation component of interest payments are incorrectly taxed. The advantage relative to equities held in KiwiSaver accounts primarily concerns the way residential landlords who borrow can deduct the inflation component of interest payments.

Notes:

42. Local Government New Zealand (2015) p19.

43. The 2013 input-output tables produced by Statistics New Zealand record the value of residential property operation as $8472 million, and the value of owner-occupied housing services as $20,7175 million. The value of the housing and utility final consumption component of GDP for the year to March 2013 was $33198 (Infos series SNE036AA.) The value of residential property in March 2013 was $672 billion (Reserve Bank of New Zealand series HC22 HHAL.QC1).

44. A government could use a property tax as a proxy for an income tax if it were difficult to tax the value of imputed rent directly. To do this they would need estimate the imputed value of rent conditional on the property value and then tax this sum at the householders’ individual income tax rate.

45. Standard theory dating back to Ricardo (1817) argues that property taxes are partially capitalised into the value of the land and thus the incidence of the tax is different to an income tax. If land is supplied inelastically, the incidence of the tax falls on the owner of the property at the time the tax is introduced, although the incidence will partially fall on the contemporaneous occupants to the extent that the supply of land is elastic. See Hilber (2017) for a discussion of the conditions where a property tax will fall on the contemporaneous occupants of residential housing.

46. This is calculated as the difference between all housing loan and housing loans borrowed by residential households, calculated from the Reserve Bank of New Zealand household balance sheet HC22.

* Andrew Coleman is a senior lecturer in the economics department at the University of Otago. He's also principal advisor & economics lecturer at Treasury.

92 Comments

The one area where Joe Average can achieve modest wealth over a lifetime (buy a house and pay it off) is soon to be targeted for a capital gains tax?

Because, supposedly, they get an ‘income’ from living in a house that they paid for!

"The one area where Joe Average can achieve modest wealth over a lifetime (buy a house and pay it off)"

That's the problem that this paper is trying to address.

Joe Average isn't supposed to achieve wealth from the house he lives in. He's supposed to do that from his day-job ( productivity, in other words). His house is supposed to be a shelter for him and his family whilst he goes about that, and the more successful he is, the better the house is that he can live in. That the only alternative he is given for surviving on a daily basis and into his old age is 'wealth from housing' is an indictment of The System that we ( and, yes, others) have created.

It needs changing, and if not now, when? For the longer we leave it, the worse the solutions - whatever they are - will be.

(PS: Imagine what Joe could do with all the 'excess' wealth he has generated from his day-job if it didn't go into his home? Imagine if his home cost 1/10th of what it costs him today. Think of what else he could do with all that disposable income that hasn't become trapped in the roof over his head. And the response that 'his day-job doesn't pay enough to do that' just shows how out of whack the whole System has gotten!)

Bravo.

Ok, let’s extrapolate this ‘derived income’ further:

You buy an ebike to go to work - so let’s tax the derived income that you have by no longer paying bus fare or petrol.

You buy a glasshouse and extensive horticultural equipmen5 to grow your own food - so now you pay tax on the derived income from saving on buying groceries.

MB well said maybe the evening cooked dinner needs taxing as it was not bought at a restaurant !!

I don't think you're considering the price elasticity of supply. I hope the tax incentive of buying ebikes and glasshouses would encourage people to buy these as suppliers would be easily be able to increase production. Prices would be elastic therefore not inflate therefore be good for society. What we have seen from the tax advantage regarding housing comparative interest-earning securities and KiwiSaver accounts is an increase in the price of houses proving this this is inelastic so the tax advantage is being capitalized causing inter-generational wealth disadvantages. This is also layered on top of a fractional reserve banking that allows banks to lend out more than they have in reserves thus conjuring value that didn't exist cause further levels of inflation into this asset class. This newly created credit is a tax on future generations, as people are waking up to in France with yellow vest movement attempting to force bank runs. We may well have a global Henry Ford moment - "It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning" - Henry Ford.

There are many other factors (exacerbated by Govt policy) driving house prices - so the supposedly tax-advantaged citizen home buyer can’t be blamed for it all.

Other factors: high immigration rates, open foreign buying rights, restrictive land use & council restrictions, building suppliers duopoly, etc.

Why should the homeowners be punished for these factors simply because they go along for the ride ....

You've enjoyed capital gains due to the uneven tax structure caused by government. You're not a victim, the tax would just be a balanced approach. The idea is to encourage investment into something more productive. Houses would be cheaper, easier to pay off. energy could flow into a more productive economy. bw makes this pretty clear.

Agree - Whilst individuals can prosper from value gains on their house - collectively this is no basis for the wealth creation required of a nation to pay our way in the world.

It requires little intelligence to work out we as a nation can not prosper by selling our houses to each other.

So lets go further. MPs Superannuation funds, not taxed as income and not really earned so must be an accumulation of capital which should be taxed at the members marginal rate on leaving office - just as fair/unfair as owner occupied housing.

"Joe Average isn't supposed to achieve wealth from the house he lives in. He's supposed to do that from his day-job"

What a terribly poor way of thinking, that you get wealthy from your day job, no wonder so many people struggle in life with beliefs like that. A day job pays the bills but it will not make you wealthy. Owning your house and paying it off over the long time make one wealthy because it's a forced saving scheme, most of us don't have enough discipline to save by choice.

You're right. New Zealand is a peculiar economy where bricks and mortar in sleepy suburbs give us everything we need. Just lock the door and let the house do gods work. It doesn't matter what we do with our time go eat crackers for eight hours, roll around in a field. Banks create value through old houses.

If they are serious about addressing the imbalance in the housing market and distorted housing prices - cut mass immigration!!!

The population was 3.3M in 1992 its not tipping 5M, thats a 50% increase on a base of 3.3M. There has been 1 new university added in that time and a number of polytechs closed. The education deficit for the population is so huge that the only way to get doctors to service the population is to license doctors trained in Bangladesh and other third world countries to work in NZ. They need to stop immigration, increase the number of places in the NZ tertiary education system for New Zealanders, and cut the number of places in the education system for immigrants. The system is set up so that the system favours immigrants and international students over NZers at present.

TOP Policy by Gareth Morgan

Tax Advantage and money laundering what is happening in NZ :

Just saw a house listed in Bucklands beach - 8 Te Akau Crescent (probably it seems a plaster house) - which was Sold in January 2014 for $905000 and in a year time in March 2015 was sold for $1820000 (MORE THAN DOUBLE IN A YEAR) than Sold again after a year in 2016 for $2458000 (appox 3 times in two year) and now again is for sell.

What is it only experts or National party could shed a light on it.

Auckland council too is culprit for raising the CV much higher to generate revune and therby adding fuel to fire.

https://homes.co.nz/app/listings/d73ad532-fb80-4c06-8cad-cd6a91d5c01c

This has been the story throughout NZ only the percentage may have differed.

Hopefully this nonsense will stop though damage been done.

Wonder what people who argued that in NZ house price have gone up only because of house shortage/supply and NOT by speculators / money laundering have to say.

This proves how wrong National party has been and responsible for the damage.

Keep ignoring that prices rose faster under Labour, who didn't see the need for a mass building program or comprehensive CGT until they were voted out of office in 2008. Of course, it's easier to blame National for everything than actually stop and look at the facts now and then.

Hi, If any experts here, can the so called experts advise how a property worth 900000 is 2.4 million in 3 years.

Uncontrolled immigration, high numbers of incoming international students, open door foreign or foreign-related property buyers, Council land section restrictions, school zoning, high building costs due to duopolies, high tax on all other investments, etc

By renovating it alittle

Renovating a little and multiply x 3. Must be joking.

Please add foreign buyer and money laundering to the list of reasons.

Keep an eye on this property and will know.

I said "renovating alittle" not "renovating a little", alittle. Maybe its clearer to you if I say "by renovating a lot alittle"?

Must have renovated with gold and diamond for house to triple fromm 900000 to 2.4million in 3 years :)

So you're admitting that you don't know what they did with he property over these 3 years to improve it yet you pass judgement

It's easy to blame National because they had the hindsight of what happened under Labour, were elected as they campaigned on addressing it and did absolutely nothing.

Prices also rose at a greater percentage under Labour, but the magnitude of the rises under National in pure dollar terms was much greater.

Not only is it easy, it's factually accurate too.

It was national who denied that their was a housing problem and when pushed said what they believed that housing problem is a good problem - Sign of prosperity.

Not sure why you're dragging the National Party into this, they're the ones who introduced the Brightline Test to capture these without doubt.

Imagine the productive investment and rise in living standards that could be achieved if we didn't simply encourage all money into unproductive property speculation.

Shares receive exactly the same benefits as a rental investment i.e. capital gain not taxed and a borrower can deduct the inflation component of interest payments. Real property is just a safer bet.

HG,

Who borrows to buy shares? Very few,I suspect. Those without capital can and should dripfeed money into shares through KiwiSaver.

You provide no evidence to support your case that property is a safer bet and I would dispute that. I am primarily a stock market investor,but I also have an investment property,so I speak from experience.

You provided the evidence yourself. People more willing to borrow to buy real estate rather than shares indicates property is a safer bet. While shares as a group might exceed returns on property more companies go under making shares worthless than real estate whose value erodes to nothing.

No.

If a population is on average opting for one asset class over another or disproportionately weighting their portfolio towards that asset class, it is evidence of some type of distortion in the expected returns.

i.e tax distortion impacts on risk weighted returns.

Hence my original post the tax effects on real estate and share investment are the same. Maybe you can explain how the tax law applies differently as between shares and real estate.

We don't have pay tax on dividends anymore?

Awesome. I'll be sure to tell my accountant next time I see him.

I will slow down for you nymad as you're struggling.

House = capital asset (not taxed)

rent = income (taxed)

share = capital asset (not taxed)

dividends = income (taxed)

Any interest on funds borrowed to buy shares or house is deductible against income (i.e. rent or dividends).

No difference in tax treatment.

House = capital asset (not taxed)

rent = income (taxed)

So you already make voluntary tax payments on your imputed rent for your primary residence?

Good on you!

It makes me wonder why you are against such a tax!

Home worth $500k imputed rent not taxed.

Renting with $500 k invested - after tax interest used to pay rent.

Renters get shafted as their accommodation is an after tax cost.

Inescapable tax bias to home owners.

But they won't fix it.

The comparison was between shares and "rental investments". Did you even read the thread or the article heading "Andrew Coleman finds that rental property investors get a sizeable tax advantage because they can deduct the inflation component of interest payments?"?

The article indicated rental proprieties receive advantages over other kiwisaver/bonds as the receive a tax free capital gain and can deduct interest on borrowed funds. I merely pointed out other non-cash assets also get these benefits (e.g. shares) therefore the focus on rental proprieties is too narrow.

Then in you come missing the point as usual.

Okay HG.

Let's review...

The thread by OP was:

"Imagine the productive investment and rise in living standards that could be achieved if we didn't simply encourage all money into unproductive property speculation."

Where did they say investment rentals only? It was you that made this distinction.

Given the fact that in general New Zealanders hold a substantial amount of their wealth in their own property, it's pointless to only consider the case of rentals and ignore the ~65% of home owning individuals.

Regardless, think of it this way.

If I purchase a $500k rental investment using equity in my primary (or other) residence (derived from capital gains), do I have the same long run tax liability if I purchase $500k of shares using cash?

No. Rental wins out.

It doesn't matter if I borrow to finance this, the tax advantage still exists in the case of the rental property because the equity in the case of the cash case has been subject to taxation, whereas the property capital gains have not.

Post purchase the tax benefits may be the same. However the during the acquisition of the capital there has been a distinct tax advantage.

The article refers to "rental properties" and the op refers to "property speculation", that's the context of the discussion and my response which refers to rental properties.

Your example is bs, any capital gain (e.g. shares or real property) can be used as equity to acquire a new asset. Furthermore, your example also assumes the cash used to acquire an asset is from a taxable income (why not cash from a realised capital gain).

Stop making everything about your deemed income crusade.

"The article refers to "rental properties" and the op refers to "property speculation", that's the context of the discussion and my response which refers to rental properties."

FYI - From the article:

To summarise, both owner-occupied and rental property are taxed less than the two most common alternative forms of investments, interest-earning securities and KiwiSaver accounts.

Also owner occupied housing is obviously also inherently speculation.

"Your example is bs, any capital gain (e.g. shares or real property) can be used as equity to acquire a new asset. Furthermore, your example also assumes the cash used to acquire an asset is from a taxable income (why not cash from a realised capital gain)."

Thank you for proving my point - share price is a function of capital appreciation and dividend yield. Thus, the overwhelming majority of share investment return (be it dividend or capital gains) will be, effectively, subject to taxation.

So, that leaves property as the main investment mechanism returning tax free gains. Thus, my point is not at all bs.

To rephrase you;

Stop trying to make this all about you fruitlessly trying to be the smartest in the room.

FYI - it really doesn't help your intention "to get paid for fact checking these pseudo experts".

1. "Also owner occupied housing is obviously also inherently speculation." That's your opinion and not in the article or in the op.

2. Shares can appreciate and provide a tax free return on sale based on potential future value. Shares can be sold for a gain without ever having received a dividend or the company ever making a profit. Show me this "effective taxation" in such a case e.g. facebook, tesla, google and most start ups.

1 - So house prices don't rise at all in real terms?

I know it's far fetched, but let's just imagine they do...In which case capital appreciation is a component of the return on capital.

2 - Make a list of the shares on the NZX that don't pay dividends. Then compare that to the list of companies that do.

I'll give you a hint - the overwhelming majority do.

If you are investing in non dividend yielding shares in Facebook and Google, please do tell us how your investment portfolio is taxed annually if you are a NZ tax resident.

This lost me..can anyone explain it simpler -

"Secondly, investors who borrow can deduct nominal interest payments rather than real interest payments from their taxable income even though the inflation component of interest payments is properly treated as a real debt repayments.."

Inflation over time erodes the cost of the debt to the borrower who benefits from paying a lower real amount (due to inflation) while being able to deduct a nominal amount (e.g. an amount effectively paid by inflation).

..thanks for confirming.

He very briefly mentions the issue of depreciation no longer being deductible (part of Bill English's tax grab) but doesn't mention the related issue of replacement cost. These are two separate issues. Depreciation is an accounting convention of writing off the capital cost of something over time. It is not the same as a fund for replacement of the asset. The issue of inflation in house prices is thus avoided. Which is kind of handy as it does rather appear that it is due mainly to government incompetence. Or is it government intention, get the buggers in debt so they do what they are told?

Another paper pushing the 'more tax' barrow without seeing what happens to the market or investment patterns once the loss limitation rules come into effect.

And as someone who is stuck paying back student loans, higher rents and will have to save a higher deposit to pay more for a house than any other generation in history, you can stuff your 'imputed rents' up your backside. This shortage is entirely created by vested interests and lazy political parties, and the idea that people under the age of 35 will continue to reach into their wallet to cover everyone else's ends needs to stop. We just don't have the money. We won't stay if you keep expecting us to pay everyone else's bills. On top of this, we're expected to pay for our own retirement in advance.

Meanwhile, the people who got us into this mess stamp their feet if you even suggest taking away their prized superannuation, a reward for turning a certain age. You got us into this mess; if someone has to take a haircut, then for once, it should be the people who are responsible. Or are we meant to believe the people who feathered their own nests at our expense while telling us they knew best suddenly actually know best?

Well said !

Bravo!! Comment of the year....

What will be funny to watch is the whining once the generations that caused this mess (1) cannot sell their business for top dollar as no one can afford the debt required to buy them as they are already mortgaged to the hilt, (2) cannot sell their 5 bedroom family house in the leafy suburb that a young family needs and would gain most benefit from but cannot afford due to the low wages and high house prices perpetrated by the same generation and (3) cannot get their private health insurance as all the young families subsidizing that generation quit the scheme as the costs keep getting passed inequitably through to the young not the old (ala Southern cross).

Bring back asset testing of super payments I say...as well as pushing the age to 70.

Age should be average life expectancy minus 15 (or number of your choice).

Trouble with changing super is (a) it is rather unfair to alter the rules for those already in the system and (b) the large number of immigrants like myself who get their super from a foreign country - you will end up with two classes of pensioner.

You're getting your super from another country. It's between you and said foreign country.

For those complaining about the 'rules of the system'; it sure as hell doesn't seem to stop them disadvantaging younger people when it works in their favour. Maybe people need a lesson in how cashflow works; about how the taxes they pay today pay for super for super annuitants today, and how they'll be relying on future workers, not the taxes they're paying now, to fund their government pensions.

There's always an out for one particular generation when it comes to things like this in the name of 'fairness' but there's bugger all considering of 'fairness' on the generation who has to pick up the can that's been kicked down the road because it's in the 'too hard' basket.

Very true.

Where were the rules of the system and fairness when those who have received much in their day decided they should cut free education and make the younger generations pre-pay their own retirement (twice over) so they themselves could give them a tax cut in the meantime. For some reason it's only the entitlements for the older folks that are sacred and untouchable. They're completely missing the quid pro quo nature of society.

I assume you mean free tertiary education. In my day it was 4 to 6% of school leavers going to uni. Now it is nearer 50%. So abolish the wealth of retired elderly graduates if you must but not the poor sods who spent their life digging ditches or working as nurses.

"For those complaining about the 'rules of the system'"

You're the one complaining about the "rules of the system" in your original post

Hahaha! Got 'em.

I'm not disagreeing with you that things are not right with superannuation. In fact I was not living in NZ until 2003 so I do not know how the current NZ system came into being. It certainly seems to have problems but I'm no expert. My point is when I arrived there was a system in place and I planned accordingly. A different system (say confiscation of foreign pensions - reasonable since NZ super is not available if you live abroad) and I would have planned my retirement differently. Changing your system or as you might say correcting it should be done slowly and progressively since as a retired person with medical issues the option of finding work or doing more overtime is not available.

My point about UK pension (to which I contributed to for 35 years but was changed to from 40 to 30 years for full pension and I got no refund) is only relevent because so many NZ immigrants are from the UK.

If you have a broad concept of moving wealth from the elderly to a universal child benefit then I'd support you. Vote for TOP.

If you didn't own a home and rented... and watched your savings get taxed to hell, while the home owner wasn't - you just might change your views.

I have sympathy for those (not I) being hit with this imbalance - from a fairness of tax perspective it is wrong. End of story.

Citizens who own a freehold house with no debt are no longer (so) beholden to the corporate systems which try to rule all consumers/workers/citizens. So they are quite a threat really - no longer subject to the fear/greed manipulation.

That is so very important. Our whole society is based on the idea of the voluntary cooperation of free men and women. Not on servitude.

So who could complain if say only 20% of mortgage interest is deductible

OR both rentiers and owner occupiers were allowed to deduct up to 20% of their mortgage interest paid?

The Government of whatever hue at the time would get a lot more votes from home owners than from landlords. After all even if you own 20 house units, you still get only one vote! And if you own from outside NZ you cannot vote.

In the USA homeowners get tax deductions on mortgage interest paid, rates, etc.

As an encouragement to be a homeowner?

Not so in NZ.

So why does he argue for more tax on property rather than less tax on the other asset classes?

We need to fund some serious infrastructure upgrades to just catch up with the population growth from the last 20years.

So we need to tax ourselves more to fund infrastructure from importing so many people so that we can import more people and increase taxes to fund infrastructure...

That sounds crazy.

But is effectively what is going to happen.

Then in addition the public infrastructure and enterprises will be then sold to private ‘investors’ who can resell at a profit or asset strip. It’s a win/win! Lol.

It may surprise you that even 3rd world countries have had a solution to this quandary for decades. All foreign workers pay for their work permit. I calculated mine as equivalent to annual salary for two teachers (they were not well paid). So come and work in NZ but pay for the privilege - that will pay for the physical infrastructure and the teachers and medical staff needed.

Yes, we use price as our normal way of rationing things, imperfect as it is. The imperfection is more in the way it works, that high prices are the cure for low prices. It encourages high prices when resources are scarce, thereby attracting attention and effort to solving the shortage.

The other source of imperfection is the nobbling of power and influence by special interests, whether of the red/green "I know best what's good for you" type, or the money grabbing type. This is a where competition becomes so important. Regulations favour the incumbents so the big players like them. No regulations lead to a scramble for power and influence, often a violent one.

Nope, stop the wholesale imports.. still need to pay for the infrastructure somehow.

Most of the property comming to market are those that have been bought in last year or two for fast money - speculation.

Another property that I saw was at Alexendra street, Cockle Bay that has been purched abour year and half befor for $1072000. Has a CV of $1150000 and now has an asking of appox 1.3 million but if one is following the current market will be lucky if gets a million.

Point is anyone who has bought in last few years for fast money is going to get burnt. If have holding capicity will not sell and wait for few years but if not will have to take a beating.

Picture will be clear by March /April, if the confidence that estare agents are potraying today is justified or is just a hope or a FACADE.

"Most of the property coming to market are those that have been bought in last year or two for fast money - speculation"

Can you please share the source of that information is it just your opinion?

Am just checking Trade me and for history use homesell or QV. Am looking at Buckland beach and nearby area.

Anyone can check.

So you've based your opinion on a few sales you have hand picked. I will know not to take your posts seriously from now on.

Regarding your comment alittle - I noted the same thing in my neighbourhood at 128 Cyril French Drive in Flat Bush, Manukau. CV$1,030,000 - Trade Me's property estimate $1,030,000 (which is about right) - Sold for $2,000,000?

https://www.trademe.co.nz/property/insights/address/Auckland/Flat-Bush/…

Not listed on any Real Estate Agent websites, must have had a buyer already lined up. Probably last of the foreign buyers clearing the gates.

Wow the new owner was either, robbed, or something else was going on.

Great to see some intelligent and factual analysis of an issue - a rare event in many cases in NZ today.

Congratulations to Andrew. Well done.

I really take exception to this twisted thinking: "Debt-free owner-occupied property is particularly tax advantaged relative to interest-earning securities but is also tax advantaged relative to equity securities as imputed rent is not taxed". What planet is this guy on?

Are you an economist?

A tax consultant, perhaps?

Either way it doesn't really matter whether or not you agree, or not. It is a fact that owner occupied property enjoys a tax advantage over other forms of capital investment.

Those who deny it highlight either incompetence in understanding the argument, or a willful ignorance to the issue.

That's what i take exception to.

But we keep being told that the family home is not an investment right?

We are told that it should be a place to live, not a place to speculate on capital gains.

But then we are told if we pay it off, we have an asset that needs to be taxed.

And what about other assets? If I own my car freehold, should I pay tax on that benefit?

Who says the family home is not an investment?

Only home owners who don't want to pay tax. Ironically though, they are more than happy to realise increases in it's value.

Economists have the view that the family home (or any home) is a decision to allocate capital. However, the allocation of this capital is not taxed at the same rate as other capital investment decisions. This is the root of the tax distortion.

Advocacy isn't for taxation when the asset is paid off. It is taxation for the derived utility of the asset for the duration of ownership.

Essentially the distortion incentivises capital allocation in property. Future tax proposals that exempt the family home will further distort this further. The result will be even more intensive capital investment in the 'family home' by way of 'McMansioning', renovation, land amalgamation.

bw says it's not an investment in his post way above and the 30 people who gave him thumbs ups

Interesting.

Haven't you always complained that the number of likes is not correlated with the value of the comment?

For good order sake- you have misunderstood the meaning of my original post. The Family Home is the application of the rewards of effort derived from your 'day job'. In that regard, it is an investment, and the better you are at your day-job, the better the home that you can afford to buy.

Further, (and I accept I am in the minority with this), Implied Rent ( owning one's own home and living in it; renting it to oneself, in other words) should be taxed just as any income is - realised or implied.

Don't forget the missus and that forgone prostitution cost you are avoiding for tax purposes. You sly devil;P

Exactly how do those hide tax obligations?

As far as I know, neither are assets.

Of course it is an investment. It provides a return and thus needs taxing. If you didn't own you would pay rent - out of tax paid earnings.

While I understand some may not want the home taxed filled, there is no argument it is a tax hole that is unfair on non home owners.

So try and define your views more clearly i.e is it you don't understand tax or you just don'y want the home taxed?

The whole issue has been created by poor immigration policies - to many people mean to much demand for housing. To much demand for housing means house prices are too high. House prices being too high means people have made money from housing which means taxing houses!

I honestly do not care about tax advantages or disadvantages of owning property. Whatever. What is irritating to me is the thought that there is a huge store of economical potential in NZ that is left untapped because all the money is driven into property. Where exactly the reverse is true. Lack of actual economic potential has resulted in a cult-type obsession with property beyond anything reasonable (as evident by crazy land prices and construction costs). No amount of tax incentive or disincentive can change this underlying current.

At best, if this policy is successful it will drive the house prices down (a positive for many no doubt), but any such benefits are short lived as the underlying characteristics of NZ economy remain unchanged as this policy has absolutely nothing to do with NZ economic potential.

Going to be interesting between everything the government is doing (healthy homes, ring fencing, CGT) to fix imbalances, will this have a large impact on foreign holders of property?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.