China’s export engine remains remarkably powerful. The country ended 2025 with the world’s largest-ever merchandise-trade surplus—US$1.2 trillion—underscoring its enduring industrial competitiveness. But that money is not going where it used to go.

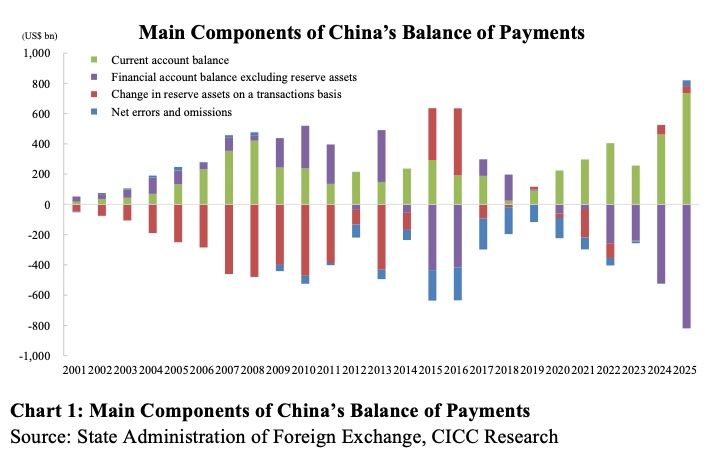

To be sure, that $1.2 trillion figure, which comes from customs data, is somewhat misleading. The balance of payments (BoP)—which records transactions between residents and non-residents of a country—shows a slightly smaller surplus of around $1.1 trillion.

The money available for recycling is smaller still. While China boasts a huge surplus in trade in goods, it runs a significant services deficit—$238 billion in 2025, including nearly $199 billion in outbound tourism spending. China also runs a primary income deficit of $110 billion, reflecting profits and dividends paid to foreign investors in China. The country’s current-account surplus for 2025 thus amounted to $735 billion—a record-breaking figure, to be sure, but much smaller than the headline-grabbing goods surplus.

But it is the way such capital is used that tells us the most about China’s economic trajectory. In the early 2000s, this was a straightforward process. The People’s Bank of China (PBOC) would intervene to absorb foreign exchange, which it channeled into official reserves, to be invested in US Treasuries and other sovereign assets. In 2002–11, China’s foreign-exchange reserves increased by nearly US$300 billion annually.

Things changed around 2012, following the end of the Compulsory Foreign Exchange Settlement and Sales System, which had required domestic institutions and residents to sell all their forex income to designated state banks. As Chinese companies gained the freedom to retain their foreign earnings, the link between trade surpluses and reserve accumulation was loosened, though the PBOC retained ample reserves.

Around 2015, expectations of renminbi depreciation prompted firms and investors to adjust their forex positions: companies accumulated dollar deposits, repaid foreign-currency liabilities, and shifted funds offshore. In other words, instead of being converted into domestic foreign-exchange receipts, the surplus was increasingly held as foreign-currency assets.

After the COVID-19 pandemic, however, another shift took place, reflecting China’s continued financial opening. The private sector is still taking the lead in recycling the surplus, but it is no longer operating out of fear. The renminbi is now stable and has even appreciated against the dollar. Instead, investors and firms are searching for yield, largely through portfolio investment in bonds and equities.

The sum of a country’s international transactions—the so-called BoP identity—must be zero, which implies that if the current-account surplus is no longer absorbed by the PBOC through reserve accumulation, it must be matched by an increase in foreign assets or a reduction in foreign liabilities, leaving aside errors and omissions. China’s non-reserve financial account recorded a deficit of about $820 billion last year, broadly mirroring the current-account surplus.

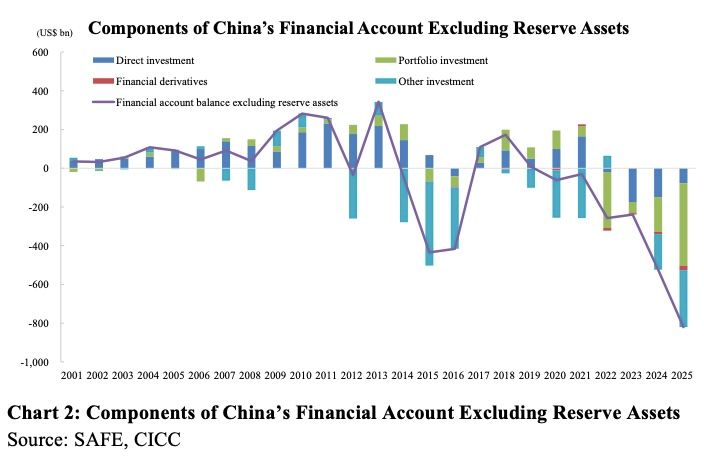

Portfolio investment—especially through the Qualified Domestic Institutional Investor program and Stock Connect—was the largest component of the financial account, totaling for more than half the deficit. Net outflows through this channel reached $426 billion in 2025, with mainland investors adding roughly $208 billion to their overseas equity portfolios and US$153 billion to their foreign debt portfolios.

While some portfolio investment is taking place within China, a much larger share of equity flows went to Hong Kong. Southbound flows through the Stock Connect scheme reached HK$1.4 trillion ($178.6 billion) last year, up 74%. This broadly matches the equity outflows recorded in China’s BoP data.

Chinese companies are also increasing their direct investment abroad, which rose by $140 billion last year. Although net outflows in this category amounted to only US$77 billion in 2025, direct investment remains an important outlet for surplus capital as Chinese firms expand overseas.

What do these data tell us about China’s economic trajectory? More of the country’s trade surplus is now showing up as foreign-exchange receipts, and the proceeds are being recycled through market-based channels, rather than official reserves. As China’s manufacturing sector becomes increasingly competitive and generates larger external surpluses, more capital is likely to seek offshore assets.

Hong Kong—with its deep equity market, strong financial infrastructure, and Stock Connect link with mainland investors—is well placed to absorb a meaningful share of these flows. Already, it is playing a more constructive intermediary role than ever before. This will advance China’s strategic goal of developing offshore renminbi markets and deepening cross-border financial integration.

These developments create new considerations for market participants. Flows driven by private portfolio decisions could be more responsive to market conditions—including yield differentials, exchange-rate expectations, and global risk appetite—than flows managed through official reserves.

The question used to be whether China’s surplus would become foreign-exchange reserves, traditional US assets, or bank deposits. The answer is now clear: China’s surplus is being recycled primarily through portfolio investment, cross-border banking flows, and Hong Kong’s capital markets, indicating China’s progress on financial deepening and underscoring markets’ increasingly central role in shaping the economy.

Miao Yanliang, a former chief economist for China’s State Administration of Foreign Exchange, is Senior Managing Director and Chief Strategist at China International Capital Corporation.This content is © Project Syndicate, 2026, and is here with permission.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.