Many hopeful first home buyers in Auckland, Tauranga and the Kapiti Coast are likely facing a Catch-22 situation, where they can't scrape together enough money for a 20% deposit, but are also unlikely to be able to afford the repayments on a low equity mortgage with a smaller deposit.

Although mortgage interest rates are steadily rising, they are still at a reasonably affordable level compared to previous years.

The average two year fixed rate rose from its recent low point of 4.49% in November last year to 5.24% in May this year.

Although that's up from where it was in May last year (5.01%), it's still well below the level of May 2024 (6.74%) and a high of 9.64% set in March 2008. (Interest.co.nz's records only go back to 2002).

At the same time, housing prices have also fallen back from their recent highs.

According to the Real Estate Institute of New Zealand, the national lower quartile selling price was $600,000 in May this year. That's exactly the same as it was in February 2026, October 2025, December 2024, March 2024 and November 2023.

Essentially, prices at the bottom end of the housing market aren't going anywhere, but they are down from the record high of $670,000 set in November 2021.

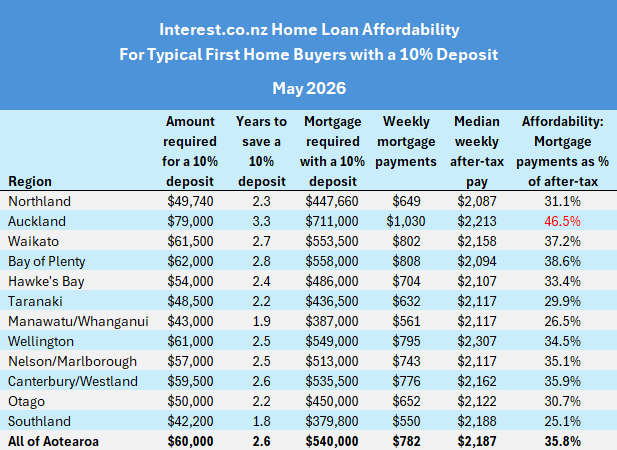

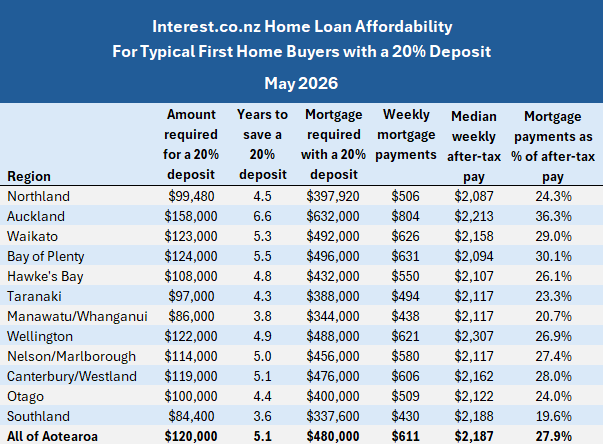

Of course lower quartile prices vary greatly at the regional level, and in May this year they ranged from $422,000 in Southland to $790,000 in Auckland.

So to buy a lower quartile-priced home with a 20% deposit, first home buyers would need to scrape up (savings, KiwiSaver, mum and dad, favourite aunty and uncle, Lotto) somewhere between $84,400 and $158,000, depending on where they wanted to live.

Getting that sort of money together is no easy feat for a young couple starting out. Interest.co.nz estimates a couple earning median rates of pay for people aged 25-29 would need to save 20% of their after-tax pay for 3.6 years to get a 20% deposit on a lower quartile-priced home in Southland, and 6.6 years for one in Auckland.

The good news for those buyers is that once they have a 20% deposit, the mortgage payments on a lower quartile-priced home should be well within affordable limits for typical first home buyers on average incomes, and that applies to all regions of the country, including Auckland.

Interest.co.nz estimates that the mortgage payments on a lower quartile-priced home in Auckland purchased with a 20% deposit would be around $804 a week, equivalent to 36.3% of the combined after tax pay of a typical first home buying couple.

That's still well below the 40%-plus threshold at which mortgage payments would be considered unaffordable.

In Southland the mortgage payments would take up just 19.6%, of a typical first home buying couple's after-tax pay and the rest of the country is somewhere in between those two figures.

Clearly, housing at the lower quartile price is affordable for typical first home buyers in all regions of the country, provided they have a 20% deposit.

But what if getting a 20% deposit together is just a mountain that's too high to climb for some first home buyers?

Banks are willing to provide mortgages to buyers with less than a 20% deposit and are actively doing so.

According to the Reserve Bank, 46.2% of the mortgages approved to first home buyers in April were low equity loans where the borrower had less than a 20% deposit.

So a low equity loan provides a way around the lack of a 20% deposit for many first home home buyers.

But it is not a free run, because low equity mortgages are significantly more expensive that those with a regular 20% deposit.

Interest.co.nz estimates the mortgage payments on a home purchased at Auckland's lower quartile price would increase from $804 a week with a 20% deposit to around $1030 a week with a low equity mortgage. That pushes the mortgage payments squarely into unaffordable territory for typical first home buyers.

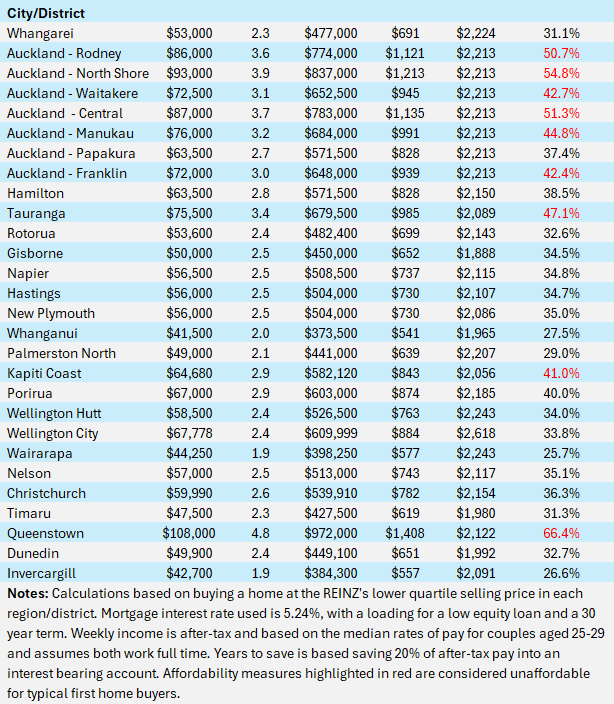

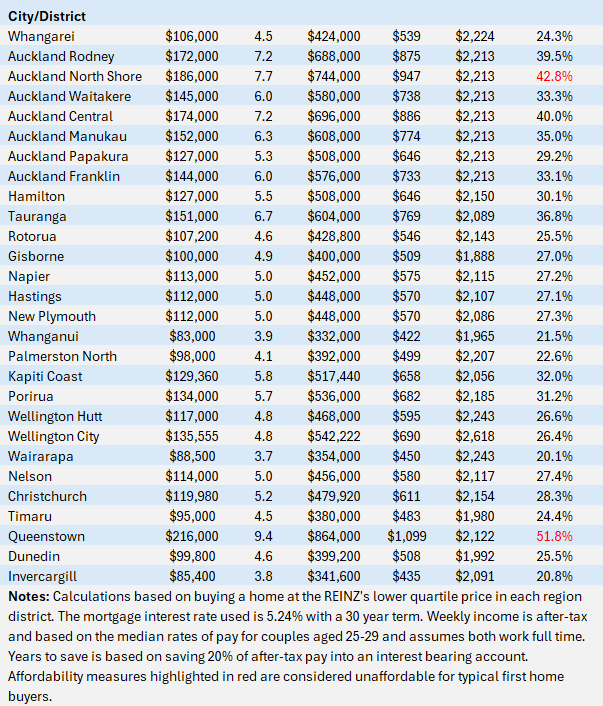

A closer look at the Auckland figures by its main urban districts shows Papakura in South Auckland is the only Auckland district where mortgage payments remain affordable for typical first home buyers with less than a 20% deposit.

That's likely to leave many first home buyers on average incomes trapped between the rock of a mountainous 20% deposit and the hard place of unaffordably high mortgage payments on low equity mortgages.

The same situation exists in Tauranga and on the Kapiti Coast.

And of course there's also Queenstown, where housing prices are so sky high they might as well be on another planet as far as first home buyers on average wages are concerned.

The tables below show the main affordability measures for first home buyers with either a 10% or 20% deposit in all major urban regions.

While there's not much good news in them for buyers in Auckland, Tauranga, Kapiti and Queenstown, homes in the rest of the country should be well within affordable limits for typical first home buyers, even if they don't have a 20% deposit.

The comment stream on this article is now closed.

24 Comments

So 28% of income in average NZ if you can get the 20% deposit. Not that crazy is it?

I feel like if you cannot afford a 20% deposit then you likely cannot afford the home. The factors preventing you from saving are going to impact your ability to repay. Less than 20% equity is a huge risk in house price fluctuations like 2020 to now. I wonder why more first home buyers do not look outside of the big cities for a cheaper investment property to get them started? Or just invest their deposit properly in a fund so that their returns outpace inflation and interest rate fluctuations.

Sounds good to buy an investment property in a cheaper area.

However, currently the market wouldn’t support this. The ‘Mum and Dad’ model of property investment will involve not only negative gearing but also capital loss being likely.

Also, from experience of others, buying an investment property in another city is fraught with issues. Minor maintenance problems which one needs to attend to (such as replacing a tap washer) becomes an expensive tradie cost. Also one needs to be handy to deal with issues with tenants personally and quickly - it is far preferable to interact personally, and if you live in another city then the tenant is more likely to be more contemptuous. As for property mangers - there goes 10% of the rent coming in (plus a surcharge on any work carried out by tradies) and profit margins have rarely been that high even in the best of times.

My ‘Mum and Dad’ grew up in a world where you could buy a house on one salary while mum raised the kids?

is this the mum and dad you refer to?

I bought my first home 20 years ago with 15%. Never missed a payment.

Aussie Minister for Social Services Tanya Pilbersek has been saying their goal is not for house prices to fall, but for the prices to grown at a slower rate, while ensuring prices are affordable for FHBers by stumping up on all kinds of grants.

I think Tanya trumped Jacinda on this. Jacinda could only claim she wanted house prices not to fall, but also wanted them to be more affordable.

We're not particularly well served by our top brass when they try to be everything to everybody.

So weird though that the expectation is that the market will only go in one direction.

All pollies but especially those on the right worship at the altar of the market and boast about their business and commercial credentials.

An asset class that only ever increases is not being fairly subject to market forces. It's crony capitalism.

For sure. What you have described is essentially bundled under the term 'Ponzinomics'.

Speaking of Ponzinomics

https://www.afr.com/property/residential/downturn-is-deepening-sydney-p…

It's been the Coalition that has implemented policies that have bought prices down and made housing more affordable.

Interest.co's info. on what has happened with the median multiple clearly shows this.

It was mainly high interest rates that caused it. And supply, but that was mainly under labour.

Or did I miss some sarcasm?

And yet in jurisdictions with affordable housing policies, those same 'high' interest rates had very little effect.

And it never does where policy allows supply to equal demand.

Prices aren't "brought down" so much as buyers just aren't frothing at the mouth as much to max out their debt.

The froth has been coming off for a number of years due to a number of policies/events/culture shifts, takes a while for many of us to catch on to the trend though.

Prices have fallen in nominal terms because the policies that support non value added speculative gains have been removed.

The very fact of offering grants pushes up prices resulting in a negative sum gain within one build cycle.

Aussie Labor is following the very same disastrous housing policies NZ Labour did, and getting the very same disastrous results.

Aussie is nows only second to Hong Kong in housing unaffordability.

Aussie bank stocks are all relatively sober in the past 12 months - flat to negative. Even over 5 years, they're barely matching inflation.

I'm not talking about the suppressed inflation figs that bank economists refer to. I'm talking relatively to more extreme inflation benchmarks like money supply growth + 1-2ppts.

Not sure what inflation has to do with my reply on grants.

My point is you cannot subsidize housing into affordability in jurisdictions with restrictive housing policies.

In fact the reverse happens ie it only make housing more expensive

Aussie is now only second to Hong Kong in housing unaffordability.

I would say get popcorn, but I ate so much pop corn during the live KPMG senate inquiry that I am sick of it short term

Australia has a few more strings to pull but it is only going to delay, slightly, the inevitable bust.

The wave has crested already..... You could blame the CGT changes but IMHO the market was already stretched too far. China slowdown is also impacting Aussie mineral sector also, sure iron ore off lows but still a long way off peaks

This is assuming 40% or less is affordable, where in other OECD countries the sum of all of your loans shouldn't exceed 30/33%.

Yes, we used to be like that but they changed the definition to fool people into thinking it was just as affordable as in the past.

A typically (for the OECD) irrelevant measure, as it ignores interest rates.

I bought my first home in 1978 on a factory workers wage. 20% deposit, 2 mortgages + solicitors loan - cheapest mge interest 15%. Servicing it took >50% of my primary fulltime net income (I had 2 additional part time jobs).

Income tax rates went to 67% & I recall paying 50c/$ > $100/wk

Right now interest rates are lower in most OECD countries than in NZ, which reinforces my point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.