Nine years on from the Canterbury earthquakes, and private insurance companies are still chasing the Earthquake Commission (EQC) for hundreds of millions of dollars related to disputes over how to apportion costs between themselves and the state insurer.

The uncertainty has hit the country’s third largest and only New Zealand-owned insurer, Tower, particularly hard.

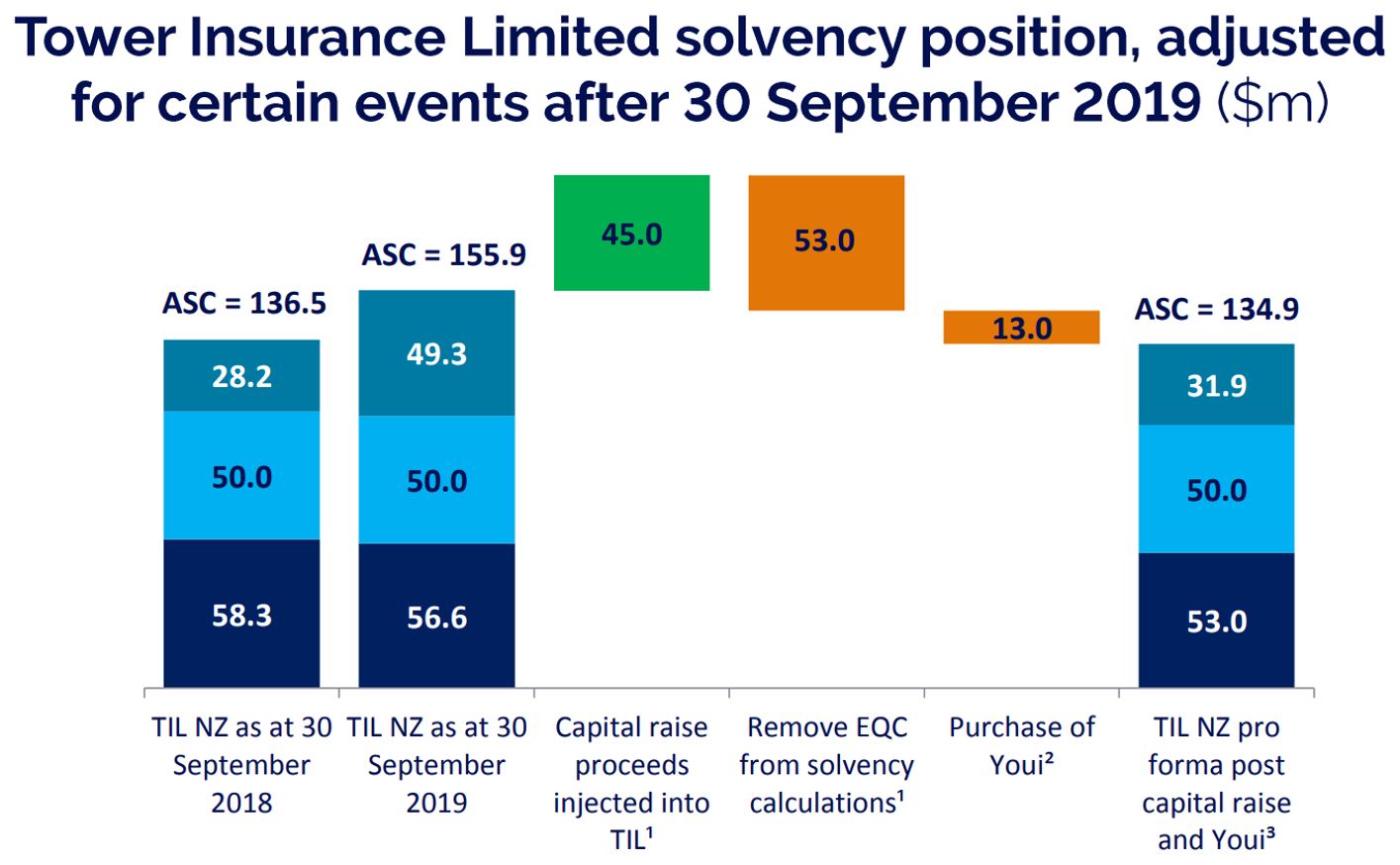

Tower on September 24 announced it needed more capital to meet the Reserve Bank’s (RBNZ) solvency requirements, as the regulator decided it couldn’t keep treating nearly $70 million of “receivables” from EQC as solvency capital, when it still hadn’t in fact received the money and might not in the future.

These receivables have for years been included in Tower's balance sheet, with the fine print explaining they represent a contested sum the insurer is confident it will retrieve.

Tower said in its 2018 financial results that it believed it was owed “significantly” more, but adopted a lower figure on actuarial advice.

In its 2019 results, released on Wednesday, it went in to a bit more detail around the dispute. It said it is going through a dispute resolution process with the EQC to try to settle matters around damage to buildings, but this could end up going to court and dragging out. It also issued proceedings against the EQC in regard to land damage.

“[T]here remains risk that any amount ultimately recovered may be less than the amount of the receivable carried in the financial statements,” it said.

A material amount of money in limbo

The RBNZ’s move to make Tower exclude EQC "receivables" from its solvency capital was huge. This, along with Tower’s decision to spend $13m buying Youi NZ’s 34,000 in-force policies, prompted Tower to do a $47m capital raise in October.

This came further to Tower in December 2017 putting its hat out to shareholders to raise $71m to keep its head above water.

The outstanding $70m from EQC is a material amount of money for the company.

Put in context, Tower had a market capitalisation of $304m at the time of writing. It had a solvency margin, above what's required by the RBNZ, of $49m as at September 31. In 2017, this buffer fell to $5m, prompting Tower to take out a bank loan.

Because Tower would need to pass on a portion of the $70m to its reinsurers, the RBNZ required it to remove $53m from its solvency calculations.

This means that further to its capital raise, and once the Youi deal gets regulatory approval and is settled, the company will have a comfortable solvency buffer of $32m.

Insurers want to handle claims from the get-go

The bigger picture is that the Canterbury quakes have exposed a lack of clarity in the law that still hasn’t been resolved.

The EQC’s deputy chief executive, Renée Walker, said the EQC has been working with each of the major insurers on the apportionment of costs for some time, and has a pot of funding put aside to settle disputes.

“These discussions are commercially sensitive as we are in ongoing negotiations,” she said.

Insurance Council of New Zealand chief executive, Tim Grafton, estimated the total amount sought by insurers would be in the hundreds of millions of dollars.

Neither IAG nor Vero’s financial results reveal the outstanding sum in the same way Tower’s do.

Neither company would disclose these figures on request. IAG said matters were either still before the court or subject to confidential legal proceedings, while Vero referenced commercial sensitivity.

If there was a major disaster tomorrow, the EQC and private insurers would probably still find themselves squabbling over who pays for what 10 years down the track.

Grafton reiterated that the industry’s solution is for private insurers to handle claims in accordance with their customers’ policies, passing the cost of the first $150,000 to the EQC.

The EQC and private insurers agreed to use a system like this after the 2016 Kaikoura earthquake.

Grafton said the issue otherwise is that damage to a property is assessed according to two sets of terms and conditions - that of EQC and that of the private insurer.

Law change pending further to outcome of Public Inquiry

Treasury started a review of the Earthquake Commission Act in 2015 under the National-led Government.

Further to this, the Coalition Government in March 2018 announced changes to the Act that saw the EQC cap for residential buildings extended from $100,000 to $150,000 and contents cover dropped.

Former governor general, Silvia Cartwright, was in November 2018 appointed to lead a Public Inquiry into the EQC. She has until the end of March 2020 to make recommendations.

A Treasury spokesperson said progress on its review awaits the findings of the Public Inquiry, but the Government hasn’t made any decisions on deadlines beyond March 2020.

Tower’s board chairman, Michael Stiassny, on Wednesday reiterated how the “the system remains fundamentally broken, despite some recent improvements”.

“A true step change in conduct and culture would see the industry join forces with the Government for an honest and transparent appraisal of the EQC and agreement on a sustainable future model for the agency,” Stiassny said.

“An EQC that delivers fair customer outcomes would have the single greatest impact on restoring New Zealanders’ trust in the industry.”

14 Comments

With the increasing impact of global warming, the only thing thats going to protect the insurance industry's profits is higher premiums.

With the high cost of living, the general public are already stretched. This can only mean something else has to give, and the one thing that comes to mind is the hydrauliced real estate prices the banksters facilitated.

For those who don't know, insurance companies are linked to banks. Those with low equity loans will understand this, given mortgage protection insurance is required and added into your lending rate. One can not exist without the other; effectively partners in crime.

This cosy relationship the banks and insurance companies mean this corrupt system is taking all the profit.

One solution would be to regulate these lenders behavoiur, and/or Nationalise the right to lend money; which as we are taught in early economics by Joe Bloggs was only suppose to be a medium of exchange. This approach would shut down these banksters private tax scheme, and let the market operate how it should.

"With the high cost of living, the general public are already stretched. This can only mean something else has to give, and the one thing that comes to mind is the hydrauliced real estate prices the banksters facilitated."

Yes, standards of living will go down as a result of climate change and the world economy's reaction to it.

Well Tower was in trouble before. Well and truly.Somehow a $40mill loan from the BNZ arrived like the cavalry to shore up their ratios. What was the collateral for that. The shares were propped up as needed, from the look of it, by continual day by day, inter trading between ACC & the Super fund. Somehow, veryweak litigation for $37mill or so against a reinsurer was entered on the balance sheet under current assets.

And in terms of the general subject, the issue of the “Red Zone” has not been addressed. Far from it. How many NZrs are aware if their land is EQ damaged to the point of being unoccupiable, but their house remains inhabitable, their insurance pays only the cost of repair, if any. In terms of EQC, the insurers have in fact, done rather well. Firstly in their successful claim for a cap to be paid for each event. But on the other hand, don’t think any insured have being successful against the insurers for “multi events” in the same vein. Secondly all those joint assessments with EQC which deliberately held claims under the cap. $millions now being paid by EQC because the true costs are now being revealed. And if in the meantime, the property has been sold, or because of the statute of limitations, the insurer is now no longer liable. That would have to be one of the biggest own goals in financial terms of any government ever and it is quite baffling, that the present government has not hung all that XXXL washing out, for all to see.

All this simply bears out the notion that swimming naked is not discernible at high tide. EQC tried to be an 'assessor' after the Christchurch quake series, mainly by hiring Services - command-and-control background - types and kitting them out with iPads. Big fail. They have seen sense after the Waiau/Kaikoura sequence in 2016, simply handling the money pot and leaving assessment to the professionals. So what this is all about is the lingering aftermath of EQC's early 'assessments'.

Aye true enough, but even at high tide there can be certain concealed sharp edged rocks that can lacerate certain appendages.

Grafton proposes the ‘solution’ is for insurers to handle assessment ‘from the ground up’ but this addresses only a relatively small part of apportionment disputes. They’d still be facing a scrap with EQC and its reinsurers unless they applied sufficient resources to rapidly and properly assess damage, initially and at each major aftershock. Which they didn’t do in Christchurch and still struggled at times to do in the smaller Kaikoura event.

Insurers knew fairly quickly which properties in CHCH were most vulnerable yet in many cases sat back and waited. The intentional tactic of declaring they would not get involved until EQC put the property over cap was not driven by homeowners insurance policy conditions. Stiassny fingering a ‘fundamentally broken system’ as the root cause glosses over the insurer under resourcing and abdication of responsibility to make timely assessments which contributed just as much to this apportionment mess as EQC’s manifest operational inadequacies or challenges inherent in the EQC first loss insurer concept.

Exactly.Absolutely. And in the final paragraph of the article it is more than a bit rich, in fact it is risible, for Mr Stiassny to wax lyrical, on fair treatment of claimants and restoration of confidence. I would wager you would find, quite readily, in the Canterbury region, many hundreds of Tower EQ claimants attesting that is exactly what they did not receive from Tower.

Quite; one might have thought insurers would think twice about lobbing missiles at the sitting duck target of EQC from their shaky high ground. To give Grafton credit he adopts a more restrained tone in his position on this apportionment stoush - while delicately sidestepping key apportionment dispute aspects by emphasising the subset issues of damage assessment responsibility and the difference in conditions (between insurer policies and the EQC act) comparatively minor problem.

Both he and Stiassny are aware that NZs EQC self funded pool system operating in parallel with private insurance delivers a higher level of disaster insurance cover at a cost significantly lower than most other models in high risk zones round the world. They also know that post event wash up apportionment challenges are an unavoidable byproduct of such co-insurance models due to the complex overlapping but essential reinsurance programs that underpin all disaster insurance programs, no matter who leads the damage assessments.

Disclaimer: I think EQC was operationally substandard in CHCH. But I also have a keen ear for shattering glasshouse panes.

“Glasshouses.” Sadly, so true. We have shared comment previously. How disturbing for us all that, on the other side of the coin, became the arrival of opportunists and scavengers exploiting genuine but naive claimants, who needed to seek advice and assistance. For example, close to our family, one claimant ended up paying more for this “service” than what was received eventually towards the repair. Believe there is a current high court class action now on these grounds.

Regrettably the jackals always gather upon these big events happening. Earthquake claims are inherently disputatious compared with other types of disaster damage (harder to attribute the need to repair flood or wind damage to pre existing causes) and while removal of open ended policy cover has eliminated some of the windfall scenarios that attract the vultures, they will still fly in. On the other hand without assertive advocacy many CHCH people would not have secured their entitlements in the face of some aggressive insurer tactics. From close personal involvement in and detailed knowledge of a good number of EQ claim scenarios I am dismayed at the unjustified distress people have been forced to endure to get what their policies promised.

The government is currently threatening insurers over risk based pricing creating an uninsurable class but Woods had the perfect opportunity to deal to them with a searching enquiry yet bottled by restricting the Dame Cartwright review terms to EQC processes only. Perhaps the good burghers of CHCH paid the price for being politically quiescent leftie voters thus no local mileage for the government or maybe she is clever enough to have worked out that her leverage over the behaviour of global insurers and reinsurers in NZs tiny high risk market, is limited. As Roberston and Orr will find out in respect of the risk based pricing issue.

Yes, your penultimate sentence is the clincher, reality check indeed! The vast majority of us live in and deal with the little picture. But at the end of the day, the big picture rules.

EQC must have a huge money bin as they tax every homeowner with insurance 300dollars plus gst,there are more houses every year to add to that tax base.however they seem to prefer delay, make you go to court to get settlement.all those insurance policies should have a sunset clause and have to be settled inside a set timeframe,not still going nine years later.

They would have had a “huger” money bin if successive governments had not drawn from the fund. After the Sept event things were relatively relaxed. But the next two, things were not relaxed at all. If more money had been in the bin, perhaps thing may have stayed relaxed for a bit longer at least. Pretty obvious the punitive and pecuniary policy adopted by EQC against claimants was Treasury driven. Mr Key needed a surplus after all.

You think it's bad now just imagine another big quake in Christchurch or Wellington.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.