New research has found within the next 15 years, thousands of homes at risk of coastal inundation will only be able to get partial insurance cover, before becoming completely uninsurable by 2050.

Research done by Belinda Storey for the Deep South National Science Challenge has identified 10,230 homes in Auckland, Wellington, Christchurch and Dunedin that are located within 1km of the coast and are in a 1-in-100-year flood zone.

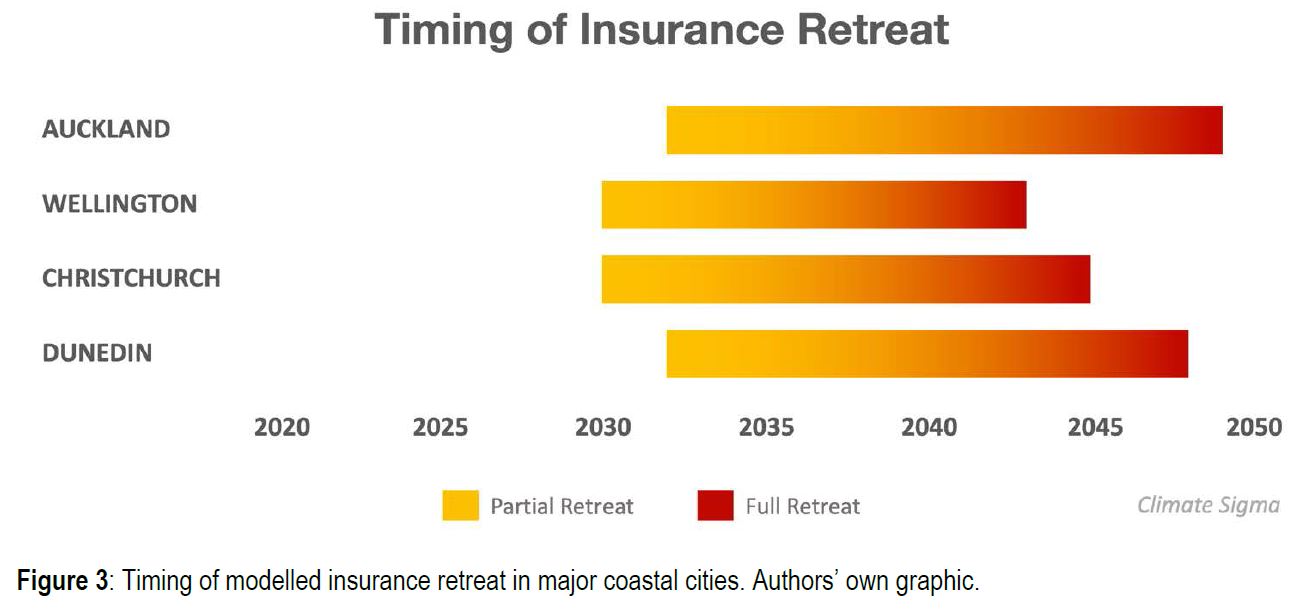

Storey found insurers would start retreating from Wellington and Christchurch in 2030, a few years before retreating from Auckland and Dunedin, because there are smaller tidal ranges in these cities, which make them more at risk of storm surges.

Storey’s research only covered these four cities. She said she took a conservative approach towards her findings.

“Insurance is a requirement for residential mortgages in New Zealand and failing to maintain insurance can trigger default,” Storey said.

“While mortgages are often granted with repayment periods of up to 30 years, insurance contracts are renewed annually. An insurer can exit a market within 12 months, while a lender may still have decades before their loans mature.

“Currently, despite rules requiring mortgagors to insure, the general absence of compliance checks means banks do not currently know whether some properties they mortgage remain insured beyond the first year of ownership.

“Once insurance is unavailable, property buyers will find it difficult to borrow money to purchase a property, and existing owners may need to make expensive modifications to their homes to prevent flood waters reaching inside.

“Insurers may be willing to continue to provide insurance to high risk areas if active differentiation between these areas and lower-risk area is widely accepted. This differentiation could include policy exclusions or very high premium prices and excesses.

“We expect particular hazards may be dropped first, for example people may still have insurance for flooding caused by excessive rain, but not insurance for damage caused by a storm surge. In some cases it may be difficult to identify a single cause of a flooding event - for example if rain water cannot drain because of a storm surge - which could result in litigation between policy holders and insurers.

“After insurance is unbundled we expect properties to quickly lose insurance for climate-related hazards.”

See Storey’s full report here.

67 Comments

Give Al and Obumer a call. They will snap them up in a heartbeat!

Maybe you should invest in these properties? Sounds like you've spotted a bargain.

Underwater has two meanings

Well you can see how much "At Risk" your AKL home will be with this handy interactive map. https://www.arcgis.com/apps/MapSeries/index.html?appid=81aa3de13b114be9…

Is there one of these for the whole country?

There's one for costal risk; Projected risk to land that may be underwater by 2050. https://coastal.climatecentral.org/map/9/176.3344/-37.6582/?theme=sea_l…

Check the algorithm used. Designed and used by the same people who predicted we would all be dead of Covid-19 by now. Note the may be, could be, might be. Make them give us a concrete date for a concrete event, so we can mock them severely when, as usual, it doesn't happen.

The good thing is that a lot of beach coastal properties are owned by wealthy or comfortable economic group who are usually older. They will spend whatever they have to so that their homes are protected. Could be to raise the piles or build stop bank or sue council.

No, they will pressure Councils to spread the cost over everyone else.

It's that kind of thinking, often enough, that got them there in the first place.

Firstly what do you mean by "got them there in the first place". Second you obviously accept there are solutions which as a left leaning climate change raver is quite a miracle. Third have those ratepayers or have they not paid most of the rates for the district so you could say they are getting some of it back pdk.

By using the phrase "left leaning climate change raver" does that identify you as a conspiracy laden right wing climate denier?

Flying high,

The science of climate change is neither Left or Right wing. It really doesn't care whether your world-view inclines you to believe in anthropgenic warming or not. Putting ever more GHGs into the atmosphere has measurable effects and consequences irrespective of your political views.

V interesting. Esp in relation to lender not knowing if prop remains insured after 1st year.

Unfortunately, taking into account NZ natural hazards and geology, its tax base is way to low for the investments needed and the electorate (like others in world) has got used to idea that it can keep wanting stuff from the State without being willing to stump up the revenue needed to pay for it. Galbraith called it "private affluence and public squalor" a long time ago. Little is changing.

Considering billions will have to be spent each year on making our coastal properties resilient to floods and inundation, we barely pay enough to fund these projects.

Worse, our councils are several steps behind on basic 3-water and transportation infrastructure, they can't possibly front up these extra costs for future-proofing coastal areas.

I'm no actuary, but surely the risk of fire will continue to decline = discount on premium for that sort of event?

Perhaps it is time for ComCom to do a competition study into our insurance market?

There are also lots of unknowns. For example much of Wellington was uplifted approximately 2 metres in the 1855 earthquake and there will be further uplifts. The Basin Reserve used to be a coastal lagoon and much of Wellington City was below sea level when Europeans arrived. New Zealand is itself a 'land uplifted high'. From my home in Canterbury I look down on the Halswell River which follows a path created by the Waimakariri River only 550 years ago. Currently, the Waimakariri River is more than 20 km away but at some time it will come back. I also look down on urban housing where the Maori used to paddle their canoes and go eeling in the 19th Century. Much of Canterbury is laid down by the forces of water disgorging shingle from the Southern Alps, and those forces continue.

KeithW

Indeed, Keith. The Christchurch earthquakes raised part of the Southshore Spit 40cm, and the Kaikoura sequence raised land 1.5m at Oaro, up to 5m at Marfell's Beach. And sand accretion all along the Pegasus Bay foreshore south of the Waimak, has kept the shore pushing out over millennia, despite a persistent SLR over that entire period. Go figure....so much for the 'within 1km of MHWS' metric used in the report.

Plus, as is usual with these types of reports, the RCP 8.5 scenario is invariably used as the worst case. That scenario requires every scrap of retrievable C on the planet to be dug up and burnt. Ain't gonna happen....the more modest RCP 4.5 causes a rise of 40cm - about the seat height of yer average dining chair. So any person of Dutch descent knows what can be done about That. More calm, less fear-mongering is needed.

Waymad

On a recent flight home from Auckland I was fascinated but not surprised to observe the silt-laden waters of the Waimakariri extending well out into Pegasus Bay. It happens whenever the norwester drops big rains in the mountains.

KeithW

You may be Interested in the recent Sand Budget Report done for the CCC. They've hidden it well, as it rather contradicts their staff's preferred agenda (which is 'You're Gonna Drown - Retreat Now'.

Waymad,

My reading of that report is that the mega force will be the Alpine Fault which, when it goes, will lead to major accretion both on the land and offshore. The report seems to be saying that the effect of sea level rise on the risk of fooding from the ocean will be minor. However, sea level rise will have some impact on lands adjacent to the Heathcote and Avon. Even then, sand accretion in the 30-50 year period following the Alpine Fault event may well be the bigger force on these lowland rivers.

KeithW

Indeed, Keith. Sand accretion southwards of the Waimak is of the order of 180K cubic metres/annum, which if we take the Waimak mouth the tip-of-spit distance as 18km, means that a 10m strip of beach is raised 1m/year. Of course the actual effect is more diffuse, but the shoreline is certainly accreting at what in geological terms is a rapid clip.....

.

So, to summarise, build your house on a fault line to ensure you remain insurable in the event of sea level rise. Seems legit.

waymand. Yes parts of south shore spit gained elevation in the EQs but to balance this large areas of nearby suburbs suffered significant declines and are now more flood exposed than before even when applying the previous finished floor level standards that did not factor in climate driven sea level rise. I share your cynicism about the flood alarmist zealotry at CCC, not that I think their models are wrong but because the mostly old housing stock in much of eastern ChCh will have passed its use by date before we get to ark building stage. The insurance council's Grafton is doing his usual cheshire cat act and warning insurers may begin to restrict cover in natural hazard areas but must be aware that process is already well underway. Application of punitive flood and natural hazard excesses is common in high risk areas. Anyone trying to get cover as a new client of an insurer on a Wellington vintage property will have experienced the new reality. Councils and other melodramatics urge immediate action but it is a combination of insurance, mortgage lenders, council hazard designations and the ageing process of buildings that will over time facilitate the necessary retreat from hazard exposed areas. The government lifting the EQC act cap would significantly slow down this necessary market led process.

There's a very simple check which can be made about all this: plant a solid cube of concrete every kilometre along the beach, and GPS/webcam monitor it. The once-a decade result will be, as long-term residents up and down this coast can confirm, that there's nothing much to worry about (Gaia's little excursions excepted....). But that doesn't suit the shiny asses. And, of course, all geology/tectonic effects are local, so other areas' mileage may vary.....location is everything. My own beach walk and rubbish pick-up every morning for 25 years confirm the accretion and shore extension eastwards.

It's also important to note that, even 500m back from the beach and especially adjacent to the rivers, the earthquakes acted severely on the riverine silts: liquefaction and subsidence. This was predicted 30 years ago in a Soils and Foundations report, so yet again, highly localised. Wave-packed marine sand did not suffer that fate.

Interesting point. I did have an internal chuckle that we need one natural disaster (uplift earthquakes) to save us from another people/natural disaster, sea level rise.

So will the earthquakes up lifts happen frequeny enough to outpace the sea level rise?

We can just fix up our broken stuff from.the shakes rather than run away form the sea?

'there will be further uplifts' - yes, probably some in future wellington earthquakes but unlikely to be to the same massive extent as 1855 which was a long return cycle fault, one that is thought to slip every 1600 - 3000 years. People often cite the uplifts from 1855 when predicting the likely landscape changes from the next more 'regularly' occurring Wellington fault movement but effects of that magnitude are unlikely to be repeated any time soon.

Middleman,

This is what GNS has to say.

"The last time the Wellington Fault ruptured through the Wellington region, causing a major earthquake, was around 300 - 500 years ago. Geoscientists estimate the Wellington Fault will cause a major earthquake every 500-1000 years. However other faults around the Wellington region are also active and capable of generating major earthquakes, for example the Ohariu Fault, and the Wairarapa Fault which last ruptured in 1855 causing a great earthquake that severely affected Wellington. The frequency of large earthquakes affecting the Wellington Region is therefore much higher, with an average return time of about 150 years for a very strong or extreme ground shaking quake."

Note that the 1855 earthquake was actually the Wairarapa Fault. Current evidence is that the next big Wellington quake will be another fault with the Wellington fault itself being likely. Also note that the overall 'average return time' is about 150 years and is it now 165 years since Wellington experienced a major earthquake. Also, given that the two tectonic plates are sliding over each other, and that major uplift earthquakes can originate from depth, the specific surface breaks may be consequential rather than fundamental. When she goes, she goes. A related issue is tsunami if the big break occurs offshore, which is likely.

KeithW

What ... our time scales dont align and one wont "save" us from he other. Rats. Guess we will have to run from the water and fix our shaken up stuff.

Nah, team of 5 million can do it. Some smart scientist just needs to find the fulcrum point, and at a signal from the PM, if we all jump together...

That all seems rather fiddling around the edges. Sure some isolated areas will experience an uplift in an earthquake, just as some areas will experience a downlift. Some areas are eroding and some are accreting sand.

These effects at the national level all come out in the wash. Overall Seal Level rise will swallow up the land.

Overall efect in NZ is uplift not 'downlift' as you call it. There are some parts of the world that are sinking because they are in a trough between plates, but that is not the case in NZ.

Yes, both coastal erosion and accretion ooccur, but they do not necessarily balance each other out. This is because much of the accretion comes from erosion of mountains rather than coastal erosion.

Rising sea levels have been going on for 20,000 years since the last ice age, and in that time the seas have risen well over 100 metres. The current rate is about 3 mm per year and seems to have been relatively constant for more than 100 years. But yes, it may well increase in the years ahead.

KeithW

Keith, Clearly any sane assessment would accept that temperature and CO2 have increased sharply over the last 100 years, and that probably sounds an alarm for sea expansion and rise. The 20.000 year figure does provide a nice baseline for the natural cycle part of the equation, and in fact every say 100,000 years there's an ebb and flow of sea level and CO2 (180-280ppm). The fact that we are so far outside the natural cycle now (412ppm), should sound an alarm.

Pureant'

I agree that sea levels will in all likelihood continue to increase.

I continue to look for evidence that the rate of increase is changing.

The current rate of increase - around 3mm per annum, or 30cm per 100 years - does not seem too scary. But that could change.

Regardless, there are a number of places around NZ where I would not purchase because of flood risk and/or sea level rise.

I hope that as a nation we can keep all of these issues in perspective.

KeithW

The difference is that rising sea levels are not an unknown, we have known about this for decades. Earthquakes are an unknown, because an earthquake is unpredictable. Some areas maybe higher risk, but there are still undetected faults, and anywhere in NZ can suffer from a quake. WEllington is overdue for a big earthquake for over 100 years. It may happen, it may not. Could affect house prices if a big one does occur.

Finally - this is happening. Great way to get people to give a shizzle about the climate. I guess taxpayer will pay though.

Always buy upland on bedrock!

I use a system for assessing the land of property I consider, even far inland, before I bother progressing further with agents or geotechs. I look at elevation to sea level maps, flood and hazard maps, fault maps, etc. The true beauty of the internet.

This is a perfect example of where government should do nothing and let market forces work. The managed retreat work that is going on has its eye squarely on moral hazard - the Act will have to be very careful that it doesn't lock in the government to pay out at a set price level. People who buy in risky places know, have always known that coastal property and towns next to rivers are hazardous - Edgecombe floods weren't that long ago.

House price growth that does not take into account natural hazards is a real problem. Breaker Bay in Wellington is at real risk from storm surge and sea level rise, but those houses are selling for a $million+. It would be horribly unjust for taxpayers and ratepayers to have to buy those owners out at a market price that did not reflect those hazards (i.e. they should be worth very little in 10 years). Insurers are already starting to build in risk-based pricing. As a result, homes in Northland are getting cheaper to insure and Wellington houses more expensive. This is right - why should Northland homeowners subsidise the insurance rates of Wellington home owners?

Careless government intervention in this space will create moral hazard - i.e. people will buy homes in risky areas for large amounts, secure in the knowledge that hapless ratepayers and taxpayers will cover their risk for them.

I totally support this:

"Storey said the Government should require councils to create local risk maps using this information, and to note the risk on property LIMs – and it should legally protect councils from being sued by landowners for highlighting the danger."

A lot of Councils now have this information freely available but from what I have seen nobody seems to worry. "Secure your piece of brick and tile at any cost" mentality seems to prevail with no difference in price factored in from one property in a flood zone to something not in a flood zone. There certainly is value however in not having a home in a flood zone.

You'll recall Kapiti District Council were hammered when they tried putting this info on LIMs (bad consultation was the main complaint). This has led to councils being shy about attaching the information to property title,s LIMs etc for fear of litigation.

If you now build on a piece of land, and it is in a new flood zone, some councils will require you put this on the title, otherwise they will refuse to issue a building consent. So you have to pay a lawyer to do this. That is how they are getting around it. More and more land it seems is getting detected as flood zones from computer modeling. It is becoming a bigger and bigger problem. Would suggest buyers check things carefully, because I fear many at the moment are just buying and not checking things due to FOMO

FOMO will be replaced by AMO (actually missing out) when they lose all their equity and then some because they didn't do their diligence. Hard but fair. As someone who did that diligence my rates and taxes shouldn't pay for the FOMOs. Let the landlords by the floodzone properties!

I envision that at first Councils will bail out/try to defend with sea walls and the like then bail out all the high value waterfront residential property. What follows will be an abandonment of the working class with modest homes a 'few blocks back from the beach' or in low lying areas subject to regular flooding once the powers that be come to terms with the futility of trying to save it all at great cost of resource.

Agreed. Sea walls merely shift the erosion to a point further along the coast when they are built at all. They are also not a meaningful, long-term approach. We could always build dikes along the coast like in the Netherlands I suppose! The most efficient allocation of resources dictates no house building in flood prone areas. Abandon Dunedin South etc

15 yrs .. what a load of rubbish.

The storm and tidal encroachment is happening now at an exponential rate.

Look to Government or local councils to bale out. Well we may see a bit, but that will soon disappear because we dont have the population base to support this plus the impeding obesity/ diabetes and other mostly self inflicted health cost. The ever increasing social costs of education and police/ justice and corrections... then throw in conservation, and emissions, and add to that energy and water supplies, not to mention housing.

End of the day, very soon , its all going to come to a head.

Either we dribble a little bit here and there to keep the local voters on your side and achieve next to nothing.

Or some non career politician with social responsibility will commit political suicide by picking one or 2 , maybe 3 , hope they are the right ones long term and go with it.

There is some point that New Zealanders are going to have to stand up, rather than put their hands out, and realise climate change has been identified and talked in media and scientific community for over 50yrs now.

Then simply accept "I we really liked that place on the river flats (or built on coastal sand), but choose to ignore the last 50yrs of advice, and now have to take personal responsibility for that call"

'the storm and tidal encroachment is happening now at an exponential rate' - be interested in your evidence for this. As a lifetime observer of natural hazards in NZ I see in our media the same inundated places being cited as examples of rising sea levels that I know from a lifetime experience of flood underwriting experience have always been subject to flood, even back when our fear of the day was an imminent ice age, but seldom any new areas flooded that come as a surprise.

Interestingly enough, in this interview on RNZ, the only person advocating for coastal homeowners to be personally responsible (i.e., no government intervention) was the coastal homeowner! He's the last of the speakers in the interview and Kathryn Ryan was completely dumbfounded!

https://www.rnz.co.nz/national/programmes/ninetonoon/audio/2018770420/c…

I respect that, because he's right. People talk about the Nanny state when it comes to things like shower heads, but taking responsibility for hundreds of billions of dollars worth of houses (at current market rates - they should be worth a fifth of that, to invent a proportion) would take the ultimate Nanny state prize!

What is my million dollar Auckland house is worth once it cannot be insured? Probably the rental value for the average number of years before it is uninhabitable - guess at 15 years so it will be worth very roughly $450k max. Allow for modest maintenance and rates and time taken to accumulate that rental income then roughly $250k.

Your value estimate calculations are probably reasonable in a 'normal' market. ChCh where supply and demand are more in balance has a lively trade in as is where is houses that have no insurance on them. The game is usually to renovate and then try to get insurance but many are just superficially flossied up and rented out with the owner taking he risk it won't burn down. Likewise houses in flood management areas which carry heavy excesses if they are insurable at all. The true value of properties in Auckland cliff top, Petone liquefaction, south Dunedin etc will only be revealed once the R.E. collective madness virus fades or Dr Orr comes up with a powerful vaccine. An anecdote - I was recently asked for an opinion by a young couple on a nice ChCh house they had their eye on. 'It WILL flood' emphasised this grinch. Their bank was willing to loan on it, insurance came with a hefty excess, they believed they would take being flooded in their stride but most of all they got it at a significant discount which enabled them to get on the ladder.

The whole of Papamoa is like less than 5 meters above sea level, its one on things that kept nagging me in the back of my mind when looking for a house there. Very nice for now but in 15 years time who knows.

I cannot look at that suburb without the word "Tsunami" screaming alarm bells in my head.

Out of interest, what would a resident there do if there was a tsunami alert?

Drown in their car in a traffic jam.

According to the Stuff article on this issue, risky developments are still taking place. If there is a perception that the taxpayer will rescue people from the consequences of these actions, there is moral hazard - the developments are effectively risk-free. I favour a miserly support only, which in reality is all the country can afford.

In the Stuff article: The Insurance Council’s Tim Grafton said NZ "should not be allowing new development in risky areas –something that is still happening in several parts of the country."

https://www.stuff.co.nz/environment/climate-news/123560377/homes-to-sta…

It has been obvious for many decades that low lying properties are at risk of this. WE have known about the ozone hole since the mid 80's. It is why I never purchased a property near the sea, because I knew that over time it could be a problem with insurance.. So it was not an unknown.

But you missed out on 40 years of nice coastal living?

Isn't that what cars, caravans, mobile homes and holidays are for?

I said living, not visiting. Not to mention the capital gains

Because of the hole in the Ozone Layer? Why?

I think if councils are going to continue to allow subdivision, sales and building in flood and inundation prone areas they need to restrict building approvals to homes of the relocatable variety. Insurers would be able to insure the relocatable portion of the home continuously even if the land owner had to move and forfeit the land at their own cost.

Councils already have s72 of the Building Act to indemnify themselves against liability when granting BCs in areas subject to a hazard;

https://www.kapiticoast.govt.nz/media/34459/form-570-building-consents-…

So the problem with that is not too difficult for Councils.

When it starts to get tricky is determining what the triggers are (i.e., under what circumstances) a Council would no longer repair/defend a public road that provides a sole access to privately held assets (be they residential or commercial). And in the event such a trigger is breached, whether Council's will permit the owners of those assets to attempt to defend access at their own cost. In the Wellington Region for example, Google the suburb, Eastbourne.

I use it as a case study for a discussion exercise titled:

Who should pay to keep the access road to Eastbourne, Lower Hutt open?

- There is only one way in and out of Eastbourne, a suburb of Lower Hutt City. This access is via a coastal road.

- Eastbourne has a population of 4,665 out of Lower Hutt’s total population of 105,900.

- In Eastbourne, 43.6% of people aged 15 years and over held a bachelor's degree or higher, compared with 21.1% for Lower Hutt City as a whole.

- In Eastbourne, 44.1% of people aged 15 years and over have an annual income of more than $50,000, compared with 29.8% for Lower Hutt City as a whole.

- In Eastbourne, 82.2% of households own the dwelling they live in, compared with 66.2% for Lower Hutt City as a whole.

- In 2017, the median sell price for properties in Eastbourne was $750,000, compared with $520,000 for Lower Hutt City as a whole.

This is a climate adaptation scenario that will play out all across NZ.

Preceding to all these todays climate change action, was couple weeks back being warned by the head of RBNZ.

By putting into govt agenda, after the Covid crisis, there's a new pathway by the RBNZ for printing more money, QEs towards climate change action, the usual beneficiary is already known, the big developer & large insurance companies that covering for the immediate coastal erosion, this bail out is for the re-location to inward lands.

Buy in Kaikoura, earthquakes are raising the land there, or is it the sea level getting lower?

Ten years from now coincides with the infamous "Agenda 2030".

Wr have been told for 30 or more years that various parts of the world be under water by dates long past but the Maldives and all the other "doomed" locations are still exactly as they were - high and dry.

So this means people don't have to worry at all about getting paid out by insurance companies until then?

Great, I can sleep soundly at night now.

This is yet another demonstration of the sheer idiocy of the neoliberal model that socialises losses and privatises profits. Until the early 1980s insurance was provided by mutuals or the very wealthy. In both cases risk was shared so that the high risk was subsidised by the lower risk, but as all were owners, all benefitted.

When equity ownership was allowed, the owners were only interested in the profits they could make. Profits that are maximised when losses and higher risks are removed from the portfolio. So in the end, higher risks are removed, and the only risks left in a portfolio are random event risks. What you have then is effectively gambling against random odds - and the insurer is the house - and the house always wins.

government and the rest of society are then left to pick up the costs of the uninsurable, socialisation of losses, privatisation of profits.

Maybe its time to ban equity owned insurers or regulate them for what they are - gambling providers.

Have one mutually owned insurer - maybe the government, and then the profits and losses accrue equally to society.

Insurers will always look to minimise losses while they have an equity model.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.