Insured losses from the early Monday morning earthquake felt widely around central New Zealand are likely to be "material" for some domestic insurance companies, insurance credit rating agency A.M. Best says.

A.M. Best notes IAG and Vero are the major general insurers in key affected regions, such as Kaikoura and Wellington.

"The insured losses from a series of earthquakes in New Zealand since November 14th, 2016 (local time) are likely to be material for some domestic insurance companies," A.M. Best says.

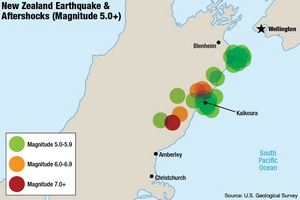

"The impact of the first quake, Magnitude 7.8 (according to GeoNet in New Zealand), whose epicenter was in Amberley, just under 100 kilometres north of Christchurch, was felt throughout the North and South Islands, followed by a tsunami which arrived about two hours later. So far, two deaths have been confirmed, together with massive building and infrastructure damage. While the impact is still developing and strong aftershocks are being felt, A.M. Best expects that the number of reported insurance claims will continue to increase. In fact, over thirty aftershocks have measured above Magnitude 5.0, mostly centered near Kaikoura, further up the Pacific Coast on the South Island. While damage does not initially appear to be as significant, the earthquakes also were felt across the Cook Strait on the North Island in Wellington, the capital of New Zealand."

A.M. Best doesn't rate IAG or Vero. It has an a- issuer credit rating with a negative outlook, and an A- financial strength rating with a negative outlook, on Tower. See A.M. Best's credit ratings detailed here. And there's information on all NZ insurer's credit ratings here.

A.M. Best says claims from the earthquakes are likely to undermine the underwriting performance of some large insurers, but adds it's too soon to determine the exact impact the earthquake will have on the financial strength of the New Zealand insurance sector as a whole.

The Insurance Council of New Zealand puts the 2015 total gross written premiums of the general insurance industry at about NZ$5.3 billion.

"As such, should insured losses from the quakes and aftershocks total hundreds of millions of dollars, this could result in a moderate impact on the gross claims experience of general insurers. IAG and Vero Insurance are the major general insurers in the affected regions, such as Kaikoura and Wellington," says A.M. Best.

At this stage the firm expects the bulk of gross claims for New Zealand insurers to stem from a combination of commercial property insurance and domestic property insurance.

"On the commercial side, in the heart of Wellington, multiple buildings in the central business district have been found to have structural damage after Monday’s 7.8 magnitude earthquake. For domestic property insurance, the Earthquake Commission has received more than 600 claims. For most insurers, reinsurance is expected to reduce the overall impact on the sector. Nevertheless, the degree of severity to which their underwriting results could be affected will vary by each insurer’s gross exposure, deductibles, retention levels, and adequacy of its reinsurance programs."

A.M. Best doesn't currently expect to take rating actions on rated insurers in the short term.

"Since the Canterbury Earthquakes in 2010-11, most general insurers in New Zealand have already moved to 'sum insured' policies for home insurance, rather than 'full replacement' covers. In addition, deductibles have generally increased for commercial insurance in recent years. Altogether, these suggest that the impact on our rated companies in relation to this event is unlikely to be as severe as the Canterbury earthquakes in 2010-11. While high uncertainty remains with regard to the ultimate insured loss, the implications for the financial strength of our rated companies with significant exposure to the affected regions will be closely monitored," A.M. Best says.

1 Comments

The losses will only be material to the extent of the excesses under those insurers reinsurance policies - assuming there is only one 'event'. While policy wordings have been changed to reduce the ambiguity over how repeat events are treated, there will no doubt still be some anxious discussions going on right now about whether the Waiau and Marlborough/Wellington earthquakes are one or two seperate events.

From experience of dealing with clients commercial claims in CHCH, the real extent of damage is not known for a long time. Initial engineering inspections pretty quickly determine structural integrity but insurance policy entitlements extend well beyond that and it will be months before the full financial cost is known.

Some of the insurers initial loss estimates circulating round the market sound pretty light. Would love to be proved wrong as reinsurers must now be looking at NZ with a jaundiced eye and that ain't good.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.