Tower's share price has dropped to a record low as the insurer has released its full year results, unveiling how it plans to raise $70.8 million of additional capital.

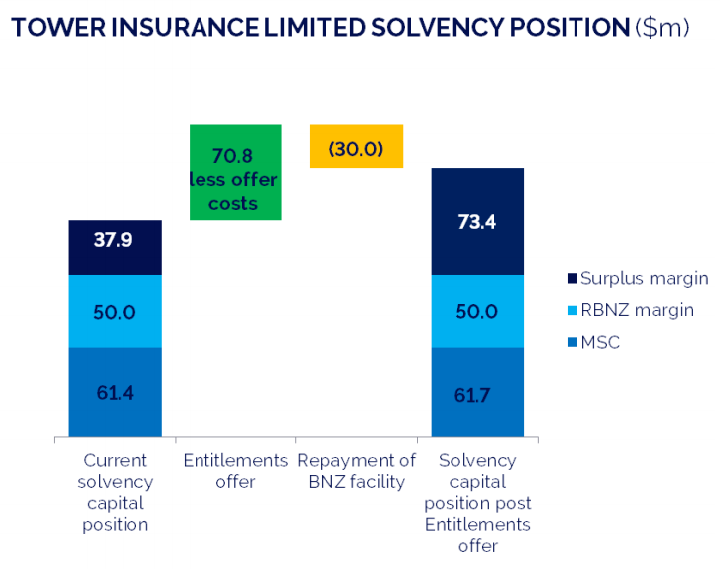

Tower hopes to “address the inherent uncertainty” it faces, repay a $30 million BNZ loan and enable more investment in the business, by making a “pro-rata renounceable entitlement offer at a ratio of 1 new share for every 1 existing share held”.

At 42 cents per share - the issue price gives investors a 45% discount on the 76 cents Tower shares were trading at before a trading halt was enforced on Monday afternoon, pending the announcement of its capital raise.

Since the halt has been lifted on Tuesday morning, Tower's share price has sunk as low as 64 cents. While it's now (at 1.30pm) back up at 68 cents, the last time it was this low was when it hit 69.5 cents after the release of the insurer's 2016 financial results.

Vero to partake in capital raise

Tower has also announced Vero will participate in its equity raise, committing to take up its full entitlement under the offer.

Vero already owns a 19.9% stake in Tower – a piece of the pie large enough to prompt the Commerce Commission to investigate potential competition issues raised by this under section 47 of the Commerce Act. While this investigation is still underway, the Commission in July declined Vero’s application to take over Tower.

Tower says if applied to its solvency position as at September 30, $70.8 million of additional capital would see it hold about three times its required minimum solvency capital (MSC) under Reserve Bank enforced rules.

The capital raise process will begin on November 21. The offer will close on December 13 with new shares allotted and trading commencing on December 20.

While Tower recognises the need for capital in the medium-term, it will also look to resume paying dividends in the 2018 financial year.

Reinsurance recoveries in dispute

In announcing a capital raise, Tower has also highlighted a number risks that could have a material impact on its business - for the better or worse.

Two of the big ones remain the $108.85 million of 20110/11 Canterbury quake recoveries in dispute with Peak Re and the Earthquake Commission (EQC).

Tower expects it will begin arbitration with Peak Re in March, with a decision expected by mid-2018. If unsuccessful, it notes it could lose all $43.75 million of the recoveries that have been recognised in the calculation of its net claims expense.

As for the dispute with EQC, Tower explains: “To date, Tower along with IAG, have issued proceedings against the EQC seeking compensation for remediation of land damage with a court hearing expected in late 2018.

“Further litigation in regards to land is expected... Based on legal advice to date Tower is confident in its position in regards to its recovery program.”

It estimates the gross amount receivable is significantly higher than the $65.1 million value its actuary put on it.

It also notes it’s accounted for the fact $17.7 million of this EQC amount is payable to reinsurers.

Bank insurance business dwindling

Among the other risks facing its business, Tower recognises: “The insurance industry is competitive, which may impact Tower’s ability to acquire and retain business.

“Concentrations of risk occur due to relationships with partners, who may choose to put their business with other insurers.

“Kiwibank domestic general insurance business will transition into runoff in April 2018.

“ASB conducted a tender process for their credit card and retail travel insurance portfolios that Tower were not successful in retaining, this relationship will cease in April 2018.

“Tower is currently participating in a competitive RFI [request for information] process with TSB to retain their domestic general insurance business and secure their retail travel insurance program.”

Furthermore, it says: “Risks exist around the implementation of Tower’s IT simplification plan which, if not successful, may result in failure to achieve desired operational performance improvements and medium term financial target.”

Tower also notes that while bids to take over the company from Vero and Fairfax Financial Holdings have been unsuccessful, there is still a chance Tower could be bought out by a third party.

Loss narrowed

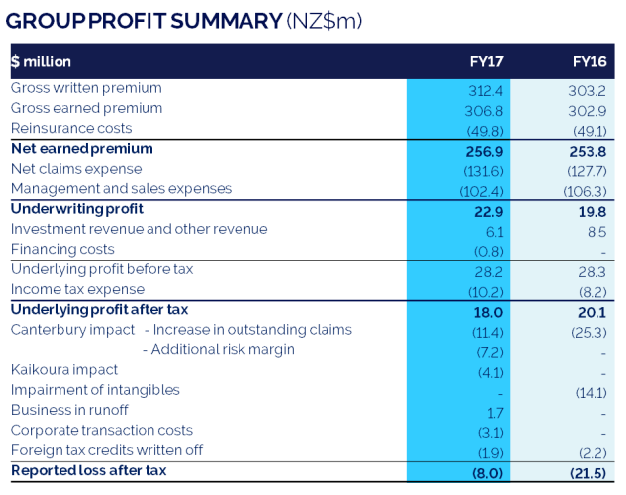

Looking at Tower’s results for the year to September 30 more broadly, it reported an $8 million loss – a $13.5 million improvement on the prior year.

Provisions for the Canterbury quakes had an $11.4 million impact, the November 2016 Kaikoura quake a $4.1 million impact, “corporate transaction activity” a $3.1 million impact and an additional risk margin for Canterbury a $7.2 million impact.

Tower says “given the complexity of the Canterbury claims situation and the ongoing uncertainty in finalising these”; it will create an additional risk margin of $10 million over the provision recommended by its actuary.

Premium hikes

Like its two main competitors, IAG and Suncorp, Tower says it’s increasing premiums to at least offset a spike in claims costs – particularly in the motor sector.

It has reviewed its pricing and made “targeted rate changes” across all its New Zealand portfolios. It has also made changes to excesses.

Tower’s 'business as usual' claims expense therefore only increased by 0.2% to $124.2 million, while its gross written premium increased by 3% to $312.4 million.

As well as premium increases, Tower added 12,441 policies to its core New Zealand book and improved its retention rate.

8 Comments

"At 42 cents per share - the issue price gives investors a 45% discount"

And they're still trading at 68 cents?

Now I know that there has to be enough of a trade discount to attract any capital raising.... but 45%?!

In essence, Tower - is gone, and it's just a matter of when and how Vero takes over. Perhaps a collapse a la Myers in Australia, might provoke such a move? If so, 42 cents will look expensive.....and 68 cents, look like foolhardiness ...

A better investment would have been in the White Star Line just as the Titanic set sail from Southampton. Anybody who has level one understanding of a balance sheet knows that this outfit is a doomed dud. But then government agencies, ACC, NZ Super could still prop this up at taxpayers risk as has already been heavily committed. Good money after bad. Still it is no longer corporate lackey National in power. Perhaps now there will be some political reality and accountability.

If Tower has booked the $47.4m (net of reinsurer recovery) it says EQC owes it, this legal action is something investors will be interested in. It is said to be in respect of land damage; presumably cases where Tower paid additional costs for stronger foundations to address land conditions or to raise damaged or rebuilt houses where land sunk, thus allowing EQC to avoid its obligation to pay for fixing the land.

EQCs thresholds for determining if damage has occurred are not defined by tougher city council imposed post EQ rules for stronger and more expensive foundations in areas of the city with poor land. The bearing capacity of much of this land was already poor before the quakes.

Should EQC be liable for the cost of addressing those rule changes? It will no doubt argue it is not, except where there has been earthquake caused deterioration in the land. And even then, the amount claimable under the EQC act will usually fall short (sometimes considerably) of the additional costs of stronger foundations.

Tower would presumably need to overturn EQCs position on both how the EQC Act applies and also the amount it is liable for in respect of land damage. Given the potential knock on effect to the Crowns CHCH EQC exposure for land damage if Tower were successful, this is likely to be a strongly argued case.

Just on a side note if Tower is to succeed against EQC they will need in my opinion, a much better legal representation than that what was on show in the CHCH high court last week.

Tower would need to have made two actuarial assumptions if it has included this EQC ‘recovery’ for land damage in its P& L.

The first is that the action will succeed ; in my opinion this would be a longish shot given the exhaustive process EQC went through to test the (limited) circumstances under which it is liable and that its position has not been overturned by court action (although granted there are practical barriers to individuals doing this).

The second is the quantum recoverable for each claim, where Tower will have a tough job showing how much additional repair cost should be attributed to EQ caused damage to land and distinguishing this from the amount driven by the significantly tougher council rules for building on poor land in CHCH. Insurance policies cover the additional costs required to comply with changes to LA imposed design rules.

Agreed Middleman there are a number of long shots involved here, and too boot, being fired from fairly shaky ground. For instance the Peak Re reinsurance under litigation, recall about $47 mill. Given the extremely uncertain outcome of that, are you or anybody else out there able to offer any explanation as to how that particular transaction can entered on Tower’s balance sheet as a current asset??

I've not seen any details of the case so can only speculate about the basis of the legal action. I would make two guesses:

First, event allocation. i.e. how much of the damage to a property should be allocated to a particular event. The Feb quake reserve exceeded the total amount of reinsurance cover but the earlier and later events probably didn't. So an incentive exists to allocate damage to the events where RI cover is not exhausted.

Unless you have pre and post damage surveys for each event that identify the progressive sequence of damage through physical observation made at the time, you are then forced to back engineer the likely sequence after the event and allocate accordingly.This is a complex theoretical exercise that is open to challenge.

The second guess is around the reinstatement clause in reinsurance policies. This typically is based on the elapsing of an agreed period of time before fresh cover is available. In CHCH where major shakes followed each other closely, these time periods become critical.

There are also a number of other scenarios that could be in dispute. RI policies have substantial excesses that are triggered for each new event and these could be in play here. RI arrangements are also typically arranged in layers, some of which have complementary 'step down' towers that under specific circumstances bolster base layers of cover. Perhaps there is disagreement on the extent to which these towers were available.

There are a number of possible explanations but all will presumably be revealed to long suffering shareholders in due course - who will make their own judgements on the extent to which these 'recoveries' should have been included in Towers balance sheet. Meantime - to address your query - it is only Tower directors who can make the judgement call on the extent to which they book this recovery cash as only they are privy to all the info. Presumably they have taken legal advice on the likely outcome of litigation.

Tks & fair comment, of course the auditors would have to be reasonably comfortable with that call as well, one supposes, and then there is Treasury and where & how that sits exactly, when calculating the requisite ratios.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.