Analysis that has been featured by the World Gold Council.

By Jennifer Johnson-Calari*

For millennia, gold, and to a lesser extent silver, underpinned the value of money—at first directly through the stamping of gold coins, then indirectly with fiat currency “collateralized” by government gold holdings through guaranteed convertibility at a fixed rate.

And, throughout history, the dominant international currency has tended also to be the domestic currency of the strongest economic and geopolitical power, which had the military force and the wherewithal to provide “global public goods” – freedom of navigation, enforcement of contracts and rules of international commerce, finance and relations between states; wealth to support its currency as a store of value; and extensive global trade links underpinning the use of its currency as a means of payment.

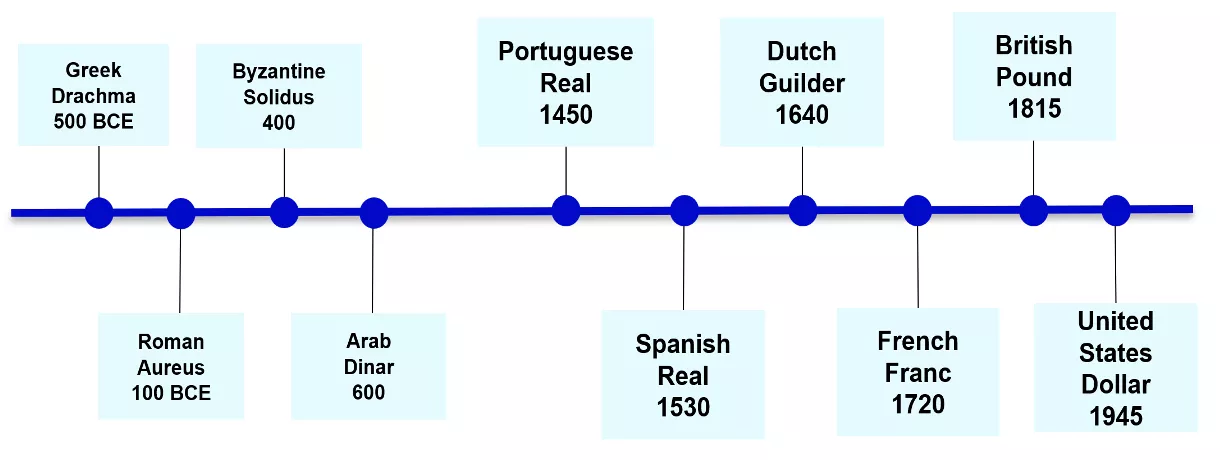

Chart 1: Rise and Fall of Global Currencies over History

The leading country typically had also a technological edge, supporting both military and economic leadership, which was often deployed to protect commercial, financial and geopolitical stability. The leading power thus offered what is known as “hegemonic stability” and generally presided over periods of peace—such as Pax Romana, Pax Brittanica and, following WWII, Pax Americana.

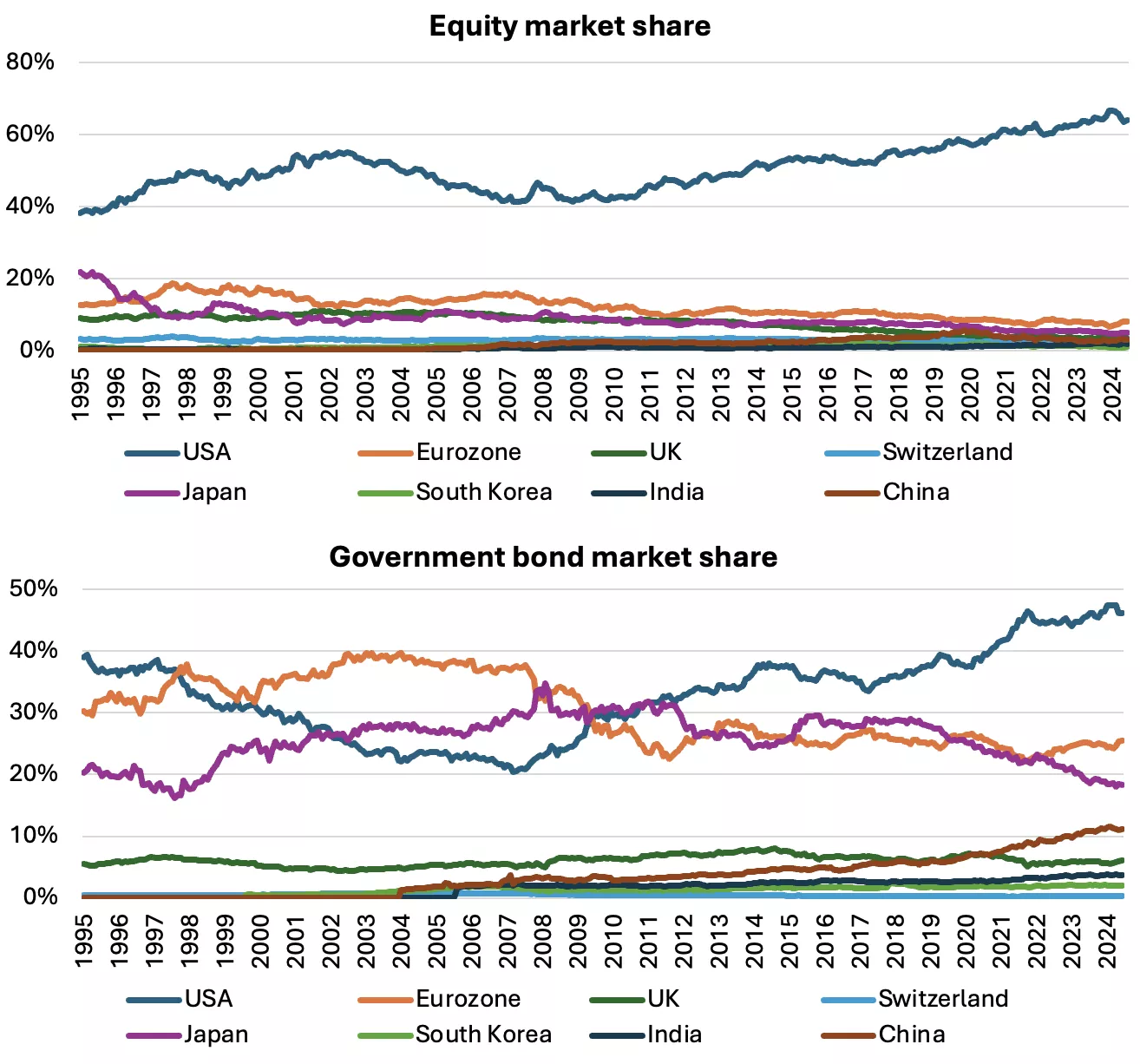

Despite external challengers and internal debt dynamics, the USD still dominates global capital markets investments and cross-border payments

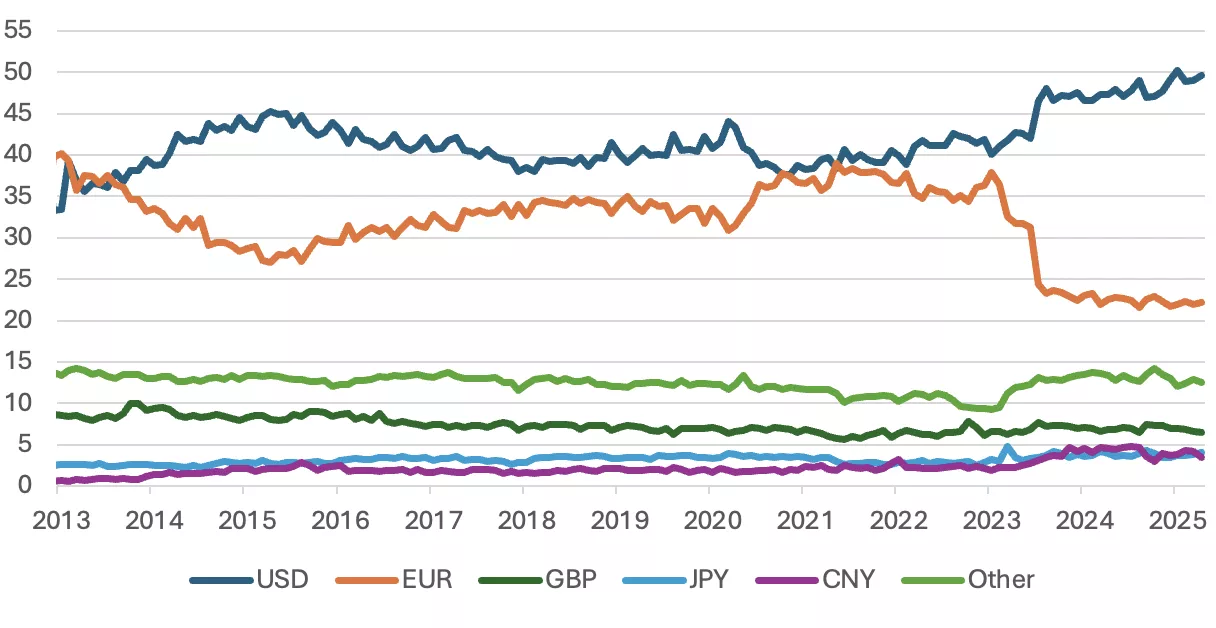

The recent backlash against the USD has arisen more for geo-political rather than economic reasons. The size and complexity of US capital markets towers over other countries with high levels of both public and private investment in USD financial assets. And, while the US share of global trade has declined, the USD still represents about half of all cross-border payments facilitated by SWIFT.

Chart 2: The US dominates global capital markets, with the divergence rising until most recently

Source: MSCI, Refinitiv, Invesco, monthly data as at 31 May 2025.

Chart 3: USD represents about half of all cross-border payments facilitated by SWIFT

Source: Society for Worldwide Interbank Financial Telecommunication, Macrobond, Invesco. Monthly data as at 07 June 2025.

The attempts to unseat the USD have been more political or opportunistic than economic in nature and no alternative to the USD yet exists. Russia responded to the suite of sanctions by not only seeking to diversify into other currencies including monetary gold but also by advocating for an alternative BRICS' currency. As this has floundered, China and other countries have continued to diversify reserves into gold as a protective measure. The ECB has taken a different approach, seeing in the recent decline of the USD an opportunity for the Euro’s role as a global currency to strengthen but faces strong headwinds.2

Supplanting the role of the USD is not imminent as the Chinese government does not necessarily want to cede control over its currencies and European national governments do not have political support to cede further control to the EC. While China is successfully ramping up the use of its currency for bi-lateral trade settlement, the use of the RMB as a global currency would entail freedom of capital flows and the running of balance of payments deficits, neither desired by the government. Europe has no such restrictions on capital flows but suffers from a fragmentation of financial markets and fiscal authority. And, while the ECB expects to launch a central bank digital currency (CBDC) in the near future, this is more likely initially to be used in intra-European trade than between two third-party countries. Finally, the BRICS currency initiative collapsed due to lack of consensus and support amongst its members.

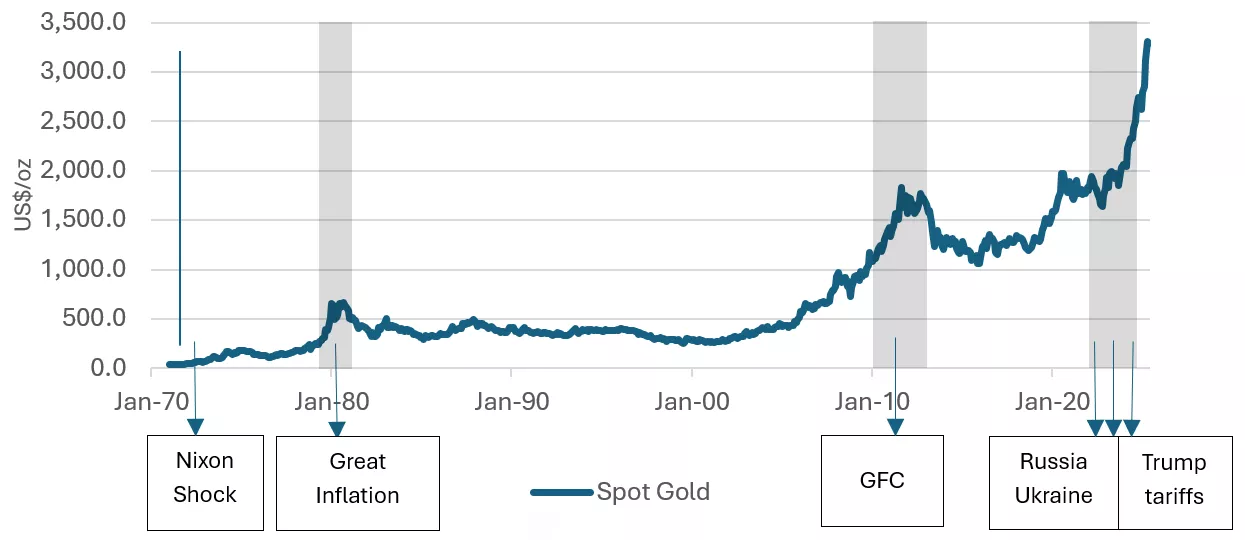

US tensions from both external and internal forces have thus been diverted to the gold market as reflected in its unprecedented rise in price since the USD was delinked from gold

The USD was, arguably, the first global currency untethered from a precious metal and held solely on the basis of trust in the issuing country. Trust in the USD was first tested in 1971, when President Nixon severed the convertibility of the USD to gold in the face of a level of foreign claims that exceeded the domestic gold stock. From 1971 to 1973, the gold price increased from $40/oz in 1971 to $108/oz as the price adjusted to underlying demand and supply variables. Since, the USD regained and until now, has retained the world’s trust based on the “full faith and credit” of the US, despite intermittent challenges and corrective actions.

Chart 4: The gold price has acted as a barometer of stress emanating from the US

The gold price run-up since 2022, however, may be signaling a pivot in the existing international monetary system and the start of a transition, albeit gradual, from a US-centric to a more multi-polar system. The recent price rise coincided with the Russia invasion of Ukraine and subsequent severing of a large part of Russia’s access to its USD and EUR foreign currency reserves, as well as to the western led financial system, including the SWIFT global payments system. Subsequently, the new Trump Administration reversed the US government’s traditional support for a free global trading system, multi-lateralism and a strong dollar, weakening the currency and contributing to demand for gold. Finally, the Administration has shown ambivalence to the US traditional role as “keeper of the peace”. These actions have spurred both central bank purchases of gold to diversify foreign currency reserves and private investor interest to protect against the risk of tariffs and, potentially, stagflation.

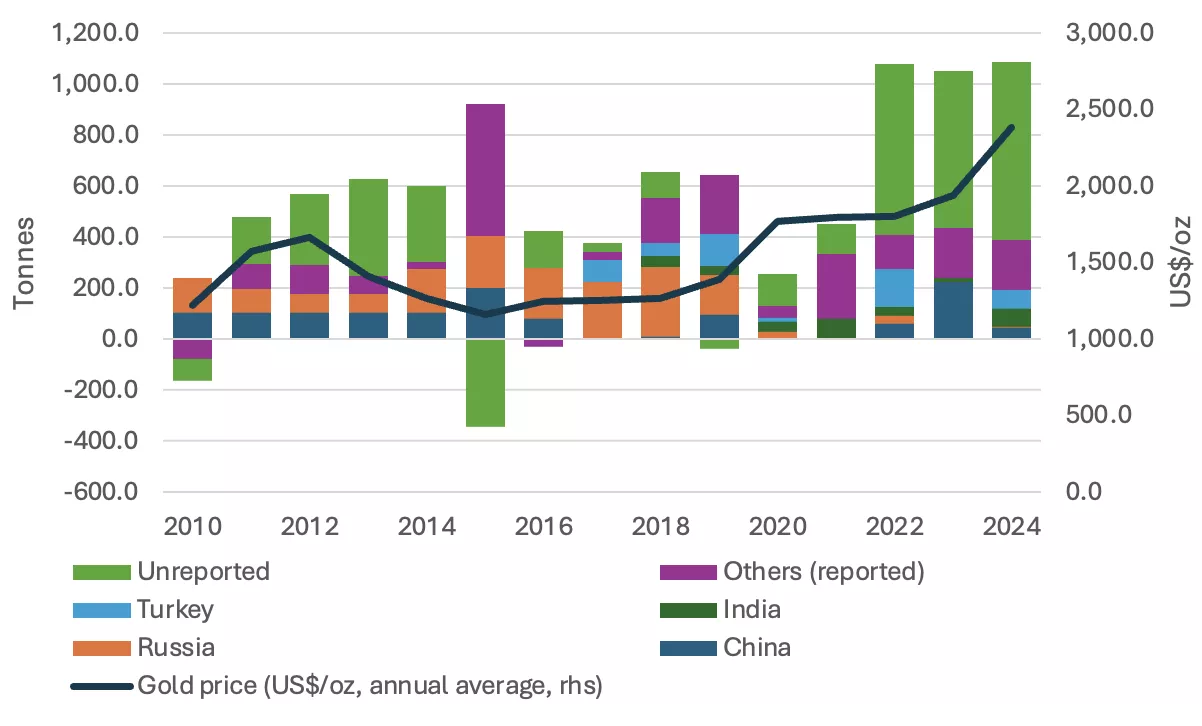

Chart 5: Emerging market central banks have sought to diversify USD foreign currency reserves by increasing purchases of gold

Source: ICE Benchmark Administration, IMF, respective central banks, World Gold Council

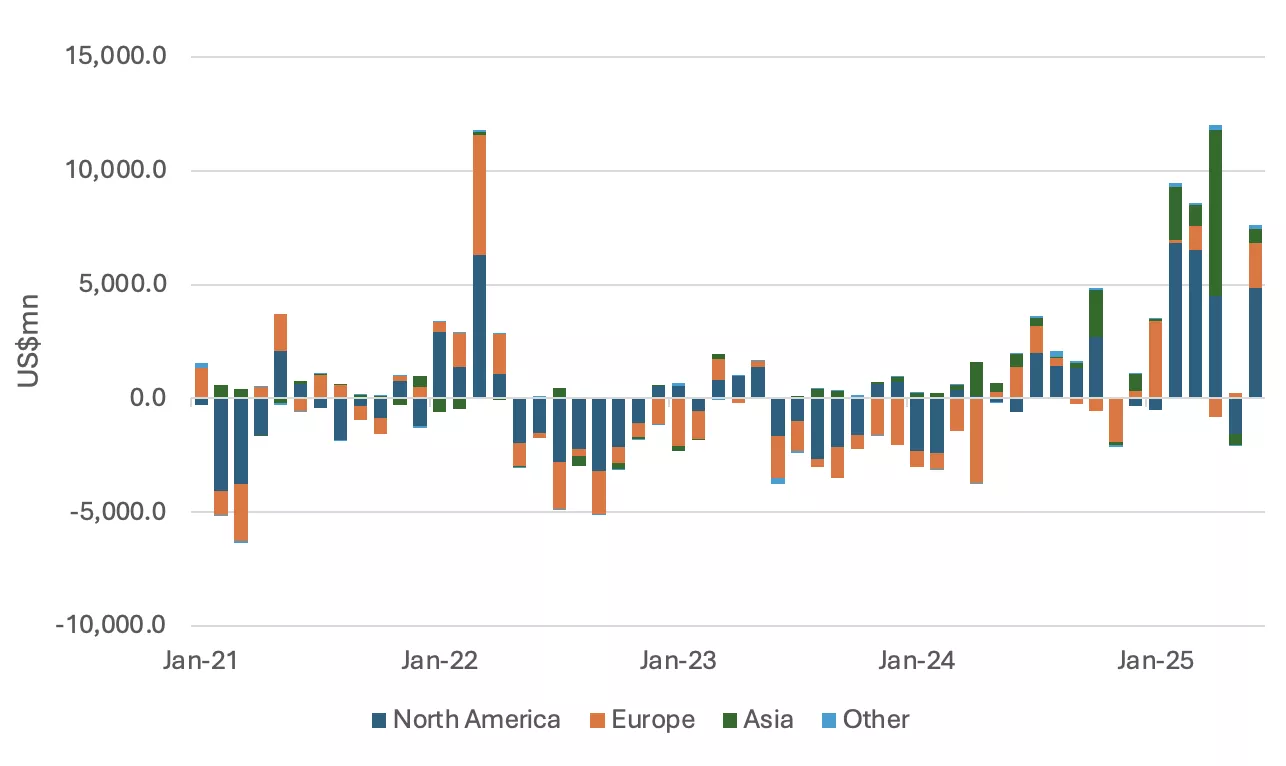

Private investment demand for gold has also increased, partly due to concerns that a global increase in tariff barriers could lead to “stagflation”-- an economic scenario in which gold vastly outperformed other financial asset classes over the past half-century. Demand for gold Exchange Traded Funds (ETFs) spiked following Trump’s “Liberation Day” announcement on April 6th and has remained largely sustained throughout July, with a net outflow in May coinciding with the announcement of a China-US “entente”, which has yet to come to fruition in concrete terms.

Chart 6: Net investment in gold ETFs spiked following the “Liberation Day” tariff announcements

The price of gold is likely to continue to be supported by geo-political concerns over the USD and the Trump Administration’s policies

The recent run-up in the price of gold has coincided with deteriorating trust in the US due to its deployment of sanctions and, more recently, access to markets to further domestic policy objectives. As part of the Administration’s policy of “America First”, the Administration is also walking away from its commitments under various international treaties created in large part by the US in the post WWII period. Despite the Administration’s erratic modulation of its more extreme statements, trust has been eroded simply by a lack of policy predictability.

At the same time, there is no credible challenger or contender who is able to provide the world with a currency with the depth and quality of markets to replace the USD. The recent run-up in the price of gold is likely signaling the start of a transition from a hegemonic to a more multi-polar system but a transition that is likely to occur only gradually and in stages. While the size of the US economy exceeded that of Great Britain in the late 19th century, the USD only emerged as the world’s preeminent currency fifty years later. During this transition and period of uncertainty, the demand for gold is likely to remain buoyant as it reassumes its historic role as a safe store of value and nobody’s liability.

Footnotes

1This post is an abbreviated summary of Arnab Das and Jennifer Johnson-Calari, “The Canary in the Goldmine: What the Price of Gold Reveals about the Role of the USD and the International Monetary System, Institute of International Affairs, Rome, July 2025. See https://www.iai.it/en/pubblicazioni/c03/canary-gold-mine

2Christine LaGarde, “This is Europe’s Global Euro Moment”, Financial Times, June 16, 2025.

This article is a re-post from here.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here.

Comparative pricing

You can find our independent comparative pricing for bullion and coins in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

2 Comments

Unfortunately gold as a medium of exchange is entirely impractical and so ultimately some form of ledger linked to a currency must be the result....and a ledger that enjoys the support of a power that has the wherewithal to enforce its will (i.e. not an independent crypto, a la bitcoin).

Or perhaps a fragmented world with regional hegemons....which appears much like Project 2025...ouch.

The article seems fair, increasingly the biggest threat to the USD are the actions of the US themselves. Increasing levels of govt debt and their increasing use of sanctions as financial warfare etc.

However like most USD articles, there is no discussion of precious metals price management by bullion banks. The demand for physical metal by central banks since 2022 makes it harder to control the price.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.