By Rand Low*

Gold has long enjoyed a reputation as a financial “safe haven” during stormy times. But over the past few months of geopolitical chaos and market panic, the precious metal has moved more like a roller coaster than a steady ship at anchor.

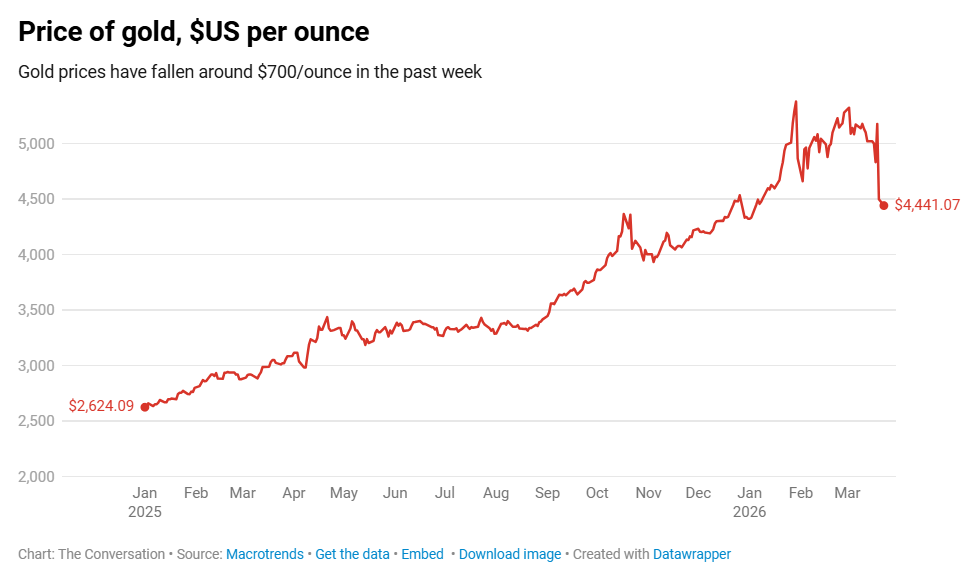

In late January, the gold price surged to an all-time high near US$5,600 per ounce – effectively double what it was a year earlier. It’s lost about 20% since then, sliding sharply while major conflict broke out in the Middle East.

To be clear, gold is still at lofty heights by historical standards, up almost 300% over the past decade. Much of this surge has been driven by “financialisation”.

Put simply, more ways of investing in gold on paper – with complex financial products called derivatives and funds that track its price – have seen a boom in speculation by institutional and retail investors.

But this year’s wild swings in price should shatter any remaining illusion that gold is always a safe haven. To understand why, we need to look at how modern financial markets work – and in particular, why an oil shock is different to other crises.

Umbrellas and storm shelters

To protect their wealth, investors often seek assets that are either “hedges” or “safe havens”.

A hedge is an investment that generally moves in the opposite direction to the rest of the market on average over a normal, long-term period.

Think of a hedge like holding an umbrella above your head every single day. You’ll stay drier than everyone else when it rains, but you’ll also block out on some of the sunshine (potential gains) when it doesn’t.

A safe haven, on the other hand, is an investment that generally moves in the opposite direction to the rest of the market only during sudden periods of extreme stress or crashes.

It’s like a storm shelter you only run to during a hurricane.

Where does gold fit?

In a 2016 research study, colleagues and I found gold had some of the qualities of a safe haven, particularly for share markets in Australia, the United States, Germany and France.

During the 2008 global financial crisis, gold was the most stable commodity among the precious metals we studied. Its price did drop, but it avoided the catastrophic losses seen in other precious metals.

It had similar safe haven qualities in 2011, when ratings agency Standard & Poor’s (S&P) downgraded the US’ AAA credit rating to AA+ for the first time in history and many global stock markets fell.

Importantly, those market shocks came out of the financial system itself (a banking system failure and a credit downgrade).

Today, the world faces something fundamentally different: a massive energy shock due to interrupted oil supplies and major damage to oil and gas facilities in the Middle East.

Why an oil shock is different

Traditional finance textbooks will tell you that when a war breaks out, inflation spikes or stock markets crash, investors typically engage in what’s called a “flight to quality” – fleeing riskier assets and moving their money somewhere seen to be safer (such as gold).

In a 2025 research paper, colleagues and I offer a more nuanced view. Crucially, we incorporated data from more recent periods of stock market turbulence, including the COVID pandemic, where gold’s safe haven properties were more muted.

We found gold is still a go-to choice for investors moving out of riskier investments. But it is not an untouchable storm shelter.

Instead of standing completely separate from the panic during a crisis, gold absorbs some of the volatility from both the stock market and energy markets, which can cause its price to fall.

Ripple effects

Why? For one, market chaos means some large investors may be forced to sell gold to cover other losses or meet financial obligations, such as margin calls (where a lender demands funds to cover the falling value of an asset).

For other large investors, the recent price rally may have created an opportunity to sell high and take profits, or rebalance their investment portfolios.

But there is also the fact gold does not have as much essential intrinsic value as something like oil. There is not much industrial demand for it compared to other commodities.

In a severe crisis, forced to chose between a commodity like oil and gold, what does global industry really need? Oil.

Rock, paper, gold

The different ways people are investing in gold is another important factor. Over several decades, gold has become increasingly “financialised”.

Now, it can be bought and sold with ease on “paper” via speculative, complex financial instruments called derivatives, or in increasingly popular exchange traded funds which track the price of gold.

With these funds, you aren’t buying gold itself. You’re buying an asset whose price is designed to track the price of gold in some way.

Today, a massive rise in speculative investment means that commodity prices depend on far more than real-world supply and demand.

Because global investors now hold gold derivatives and conventional stocks at the same time, the risk of exposure to common market shocks has drastically increased.![]()

*Rand Low, Associate Professor of Quantitative Finance, Bond University.

This article is republished from The Conversation under a Creative Commons license. Read the original article.

13 Comments

Because global investors now hold gold derivatives and conventional stocks at the same time, the risk of exposure to common market shocks has drastically increased.

Every asset class on the planet has been financialized beyond recognition. So it is possibly true that gold is not a safe haven because its price can be manipulated by the financial complex. Well we know that beyond a doubt.

That being said, Anglosphere currencies probably have the least volatility among the asset classes - most of the time. That doesn't necessarily make cash a safe haven if the hidden loss of purchasing power through inflation is running at 7-8% pa.

A good article, thank you Rand Low. You make a pertinent point when you state:

Because global investors now hold gold derivatives and conventional stocks at the same time, the risk of exposure to common market shocks has drastically increased.

"Paper" metals are indeed behaving more like securities and detaching themselves form long-term holdings of physical metals. Margin calls and stop losses can be triggered, leading to much larger downswings than with physical metals.

Whilst I have no idea where the price of Gold will be tomorrow, next week or in a month's time, I believe that Gold will significantly rise in value over the medium to long because:

1) Governments are crushed by immense debt which cannot be repaid, their only way to deal with this immense debt is to devalue their fiat currency, hence Gold will rise in fiat terms.

2) Wars are expensive and governments don't have any money left to pay for arms, munitions etc... They will therefore resume QE (mostly likely under a different fancy name) but they will print immense amounts of currency, this will accelerate fiat's demise and intensify point 1 above

3) The closure of Hormuz is very inflationary, and it will stifle growth at the same time, worldwide. Central Banks are going to be in a terrible bind with the upcoming stagflation, they should raise interest rates, but they won't be able to because of the huge debt would bankrupt countries. Volker could raise interest rates to 20% because debt to GDP was 60%, it is now more than double. This will lead to negative REAL interest rates, (where inflation is higher than interest rates). In this environment money flows out of bonds, stock markets and bank deposits and into precious metals

Global long-term bond funds saw about 4.7 billion dollars of net outflows last week, the second‑largest weekly outflow on record, exceeded only by a roughly 6.8 billion‑dollar outflow during the 2020 Covid pandemic [https://www.binance.com/en/square/post/306892219296513].

Gold experienced a sharp selloff during the same “dash for cash” episode that drove heavy outflows and dysfunction in long‑term bond markets in March 2020.

Bonds and Gold are very liquid which explains the selloff in urgent need for funds to plug other holes.

Perhaps some economies are being forced to 'trade gold for oil' as the oil price has risen beyond normal reach.

You could certainly argue that oil is cheap when priced in Gold.

Perhaps some economies are being forced to 'trade gold for oil' as the oil price has risen beyond normal reach

Yes. The Turkish central bank has reportedly sold about 58 tonnes of gold in the past two weeks, cutting reserves to roughly a seven‑year low around 513 tonnes. The stated motive is defending the lira and funding a higher oil import bill as crude prices spike with the Iran war.

Russia began selling part of its gold reserves in 2025 to help finance war expenditures, and that liquidation has continued into early 2026, taking its holdings to about a four‑year low.

Most other central banks remain net buyers or flat.

The conspiracy theorist camp will point to the Western financial complex over central banks.

A per GPT-5 mini...

Using July 15, 2008 peak gold was $988.75/oz.

Live gold spot today (Mar 31, 2026) = $4,560.75/oz.

Calculation:

- Gold per barrel = 150 ÷ 988.75 = 0.1517 oz

- Equivalent today = 0.1517 × 4,560.75 = $692.17

Result: $150/barrel (priced in gold on July 15, 2008) would have to be ~ $692.17/barrel on March 31, 2026.

............................................

The one thing I do know is that we cannot come to terms with any of these trends using fiat monopoly paper tokens as a benchmark.

Things become even more confusing given that the spot gold and silver paper prices are not market supply/demand driven. Rather they are synthetic paper prices where entities that don't own physical sell paper contracts to those who... wait for it... don't want to own physical.

This entire plutocratic-driven shit-show becomes even murkier if you try to factor in the manipulated CPI numbers that hide the true inflation rate, just to try to keep the Western fiat Ponzi alive, the can kicked down the road, and the wool pulled over Mainstreet's eyes.

This is why the physical pricing of G & S, and the bullion itself, is moving East at a great rate of knots.

Meanwhile, TOOFOO is doing a splendid job of setting fire to the entire casino, at a rate... "nobody has even seen before... not even close".

Col

Always worth having a bit of the shiny stuff

“Safe-havens are now select commodities (oil and agriculture), cash, inflation-linked bonds, and some foreign currencies – not the typical basket you normally expect,”

Yes. I bought Betashares Global Agriculture Companies Currency Hedged ETF (ASX: FOOD) around 2020. Performed miserably against gold / silver over the same time period, but has delivered strong recent performance, with mid‑teens to high‑30s returns over the last year. Fertilizers & agricultural chemicals make up 26.6% of the fund.

Gold and silver proxies up strongly on ASX today.

Bank shares not so much today, I can see the S&P500 possibly squeezing to 6800, before another down leg.

Dangerous times to hold large positions.

Crusaders 13+ multied with Chiefs by 7.5 is 50% ... seems reasonable.

If one offered investors a fat tail put option that never decays or expires, costs about -1% pa to carry, has no counter party risk & no chance of ever becoming worthless, there would be a line out the door. But when one explains that this option is physical gold… no interest. – S. Mikhailovich

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.