Pie Funds and JUNO investing magazine are partnering to offer a low cost KiwiSaver scheme with actively managed funds.

The husband and wife duo behind the boutique fund manager and magazine, Mike and Jacqueline Taylor, are launching JUNO KiwiSaver on August 1.

The scheme’s fee structure is its main point of difference.

JUNO KiwiSaver members will be charged a set dollar amount per month depending on the size of their balance, rather than a percentage of their balance, regardless of whether they’re in a conservative, balanced or growth fund.

Furthermore, under-18s and those with KiwiSaver balances of less than $5000 won’t be charged at all.

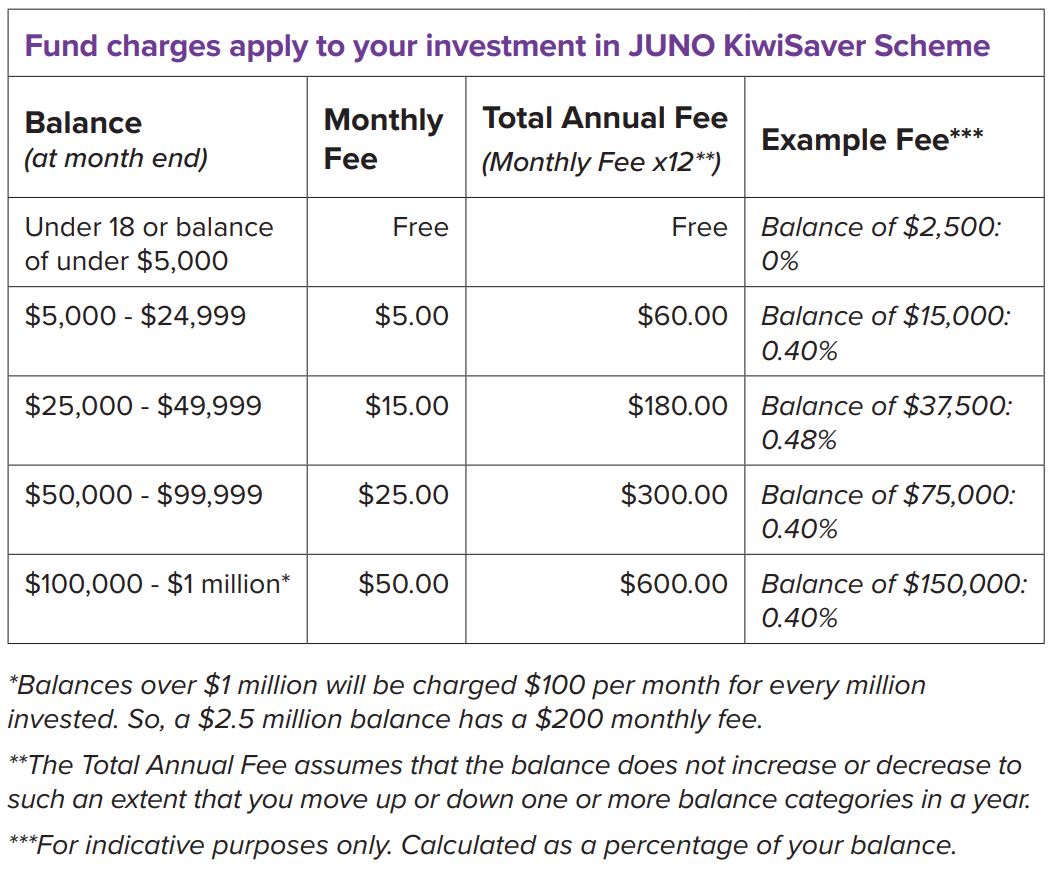

This is what JUNO KiwiSaver’s “monthly subscription” type of fee structure looks like:

The amount a member pays as a percentage of their KiwiSaver balance will depend on where they sit in the band they’re in.

For example, someone with a balance of $25,000 will pay the equivalent of 0.72% per year in fees, while someone with a balance of $49,000 will pay the equivalent of 0.37%.

These rates are well below market averages. According to Sorted.org, the average fee across all conservative funds in the market is 1.09%, balanced funds 1.29%, and growth funds 1.47%.

JUNO KiwiSaver’s other point of difference is its investment strategy.

Speaking to interest.co.nz, Mike Taylor says it’s focussed (but not exclusively) on investing in companies that are household names, “because there’s a desire for people to know where their money’s invested”.

“We want to invest in companies that people know and understand.”

Furthermore, he says JUNO KiwiSaver funds are genuinely actively managed, with portfolios only including about 50 holdings from an equity perspective.

“If you look at the holdings of most KiwiSaver funds, you’ll tend to see there are hundreds of companies in there and the funds are very diversified. So our first point of difference is that we’re actively selecting investments and it’s relatively concentrated compared to other providers…

“If we weren’t doing that, we may as well just be an index fund. If you hold everything in the index, you are the index.

“Over the last 12 years we’ve [Pie Funds] demonstrated we can out-perform by stock picking.”

Mike Taylor founded Pie Funds in 2007. It has about $800 million under management.

He says JUNO KiwiSaver funds don’t mirror specific Pie Funds’ funds with corresponding risk profiles.

However Pie Funds’ fund managers will manage JUNO KiwiSaver’s funds. No new fund managers are being hired to take care of the KiwiSaver business.

The KiwiSaver funds will also be socially and environmentally responsible.

Jacqueline Taylor, who is also the editoral director of the JUNO magazine, points to the importance of the investor education piece.

Like many other KiwiSaver providers, JUNO KiwiSaver will offer tools investors can use to figure out their risk profile, calculate what their projected retirement savings will be and what they will have paid in fees.

Here is a copy of JUNO KiwiSaver’s product disclosure statement.

17 Comments

Good stuff, will be interesting to see how they perform.

Their low fees are definitely a selling point, but their investment strategy doesn't appeal to me personally. I have very little desire to have my funds constrained to primarily "household names" or to know specifically where my money is invested. I really just care about the return and what potion of it is going towards fees.

You defeat your own statement with doesn’t appeal & then really just care about return

Newsflash the return is all anyone is ever primarily concerned about

If they can manage my money with 50 household names I’d prefer that to investments in say Brazil in a global fund. Volatility should be lower following their strategy & a lot of time saved informing clients about the companies invested in.

I’d like to see Milford Asset open another equity fund for investments in NZ & Aus businesses like the one oversubscribed a couple yrs back

You defeat your own statement with doesn’t appeal & then really just care about return

What on earth are you talking about?

Try boy just try

Goodnight kiwi lad

Bizarre

I'm picking our friend has been on spirits

Mmmmm, pie.

The fact that a company is a "household name" doesn't make its shares a better investment by default. Downright bizarre if that was the investment strategy, but methinks it is just marketing spin. Same with the analogy to a "Netflix style" subscription service. Last time I checked, Netflix didn't invent the concept of paying for something with a monthly flat fee. Trying to be hip/contemporary...

That said, I'm definitely interested in this offering as it bridges the gap between passive and active with a low fee approach.

The Simplicity concept has merit but some of the ETFs used are awful.

"The Simplicity concept has merit but some of the ETFs used are awful"

Is that because they are moving to investing in ethical business only?

I'm mainly thinking of the Vanguard Bond ETF that is the cornerstone of their fixed interest allocation.

An index approach is poor for the fixed income universe, as the countries with the largest weightings in the index are the ones who are the most indebted!

Arguably an ethical investment approach should also exclude the direct funding of the US government, but that's another story...

:)

For those who are interested, the portfolio breakdown is here:

https://www.vanguardinvestments.com.au/adviser/adv/investments/product…

Makes me wonder whether there is a case to diversify Kiwisaver across providers. Pity this can't be done at the moment...

“Over the last 12 years we’ve [Pie Funds] demonstrated we can out-perform by stock picking.”

Oh really? I'd love to see some figures on that...

Here are Pie Funds' quarterly fund updates. You can see how the performance of its funds has tracked against the market.

None of the three I looked at go back 12 years though.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.