Over the past year, households have shown less inclination to hold their liquid cash balances in term deposits. The shift is especially marked for term deposits.

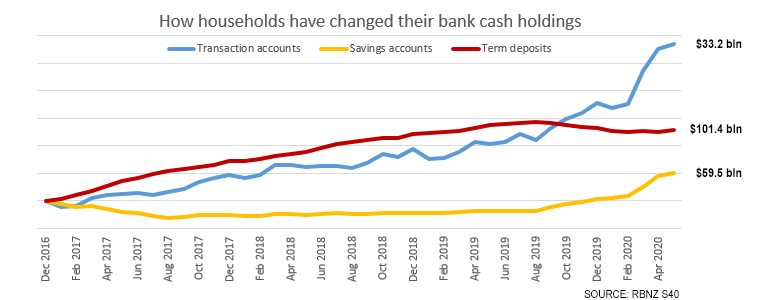

In that time they have cut their holdings invested in term deposits by -$1.4 bln and more than -$0.5 bln of that is since the start of 2020.

This comes as interest rates have been cut sharply. In May 2019 a six month TD returned 3.15% on average (3.30% as the best rate). Equivalent one year TD rates were 3.15% and 3.35% as the 'best rate'.

Now those rates have reduced to 1.90% (2.25%) as at the end of May 2020, and for one year they were 2.00% (2.30%). In June they went lower yet again.

But households have not shifted their savings away from banks. In fact, they have shifted them into lower earning accounts!

Banks haven't been hurt at all - if anything this shift has reduced their cost of funds by more than the reduction in interest rates they have carded.

Banks appear to have been a winner in this shift.

Take care interpreting this chart. Each component has been rebased to the start of 2017 to show the change since then.

In a year, an additional +$13.7 bln has flowed into total household bank accounts, +$9.0 bln of that in 2020 alone.

Transaction accounts have grown by +30% and savings account balances have grown by +14% in a year, even as term deposit balances have shrunk by -1.4%.

Household behaviour with their ready cash has clearly shifted to 'risk-off' in the past year. Interest earnings are now not much of a motivator to holding bank balances - quick access to to it for liquidity is.

Interest earnings on cash have become irrelevant in household decisions as economic and pandemic risks have risen and household balance sheets have been rebalanced for a short-term 'prepare-for-crisis' basis.

All this has come at a good time for bank margins. They aren't lending as much because loan demand isn't strong. And with competition evaporating for cash, volumes of very cheap customer funds are surging.

In the year to May 2020, bank loan books (as per C5) have risen +$20.0 bln with less than +$5.3 bln of that in 2020.

But customer deposits (as per S40) have risen +$32.5 bln with more than +$21.4 bln of than coming in 2020.

We are seeing a very large, recent shift. And it is unprecedented. As recently as February 2020 total customer deposits were 77% of total loans, a level they have been at for a very long time. Suddenly they are at 82% and that 5% change is driven by the +$20 bln rise in deposits just as lending has plateaued.

Since February, household deposits have jumped by +$9.6 bln, business (including farming) deposits are up by +$7.6 bln and even central government has raised its cash deposits in the local banking system by +$2 bln. And most of these rises are in at-call transaction and savings balances. Banks have no trouble with their Core Funding Ratio, even if the RBNZ has recently loosened this standard in an effort to get them to lend more.

Banks are being forced by their depositing customers to "borrow short", and expected by their borrowing clients to "lend long". It's a trend both bank treasurers and regulators will be watching with unease. The only funds banks can access that are 'long' - so that they can rebalance than unhealthy trend - are from foreign professional investors via the bond market. And they are only fair-weather friends.

45 Comments

For retirees, if household outgoings exceed income there are only two options. Reduce expenditure or dip into savings, ie capital. If the latter, then those funds need to stay accessible, current account not a term deposit. For the former option it would be interesting to learn whether the cancellation of health insurance policies has increased. If so that would be one indication of austerity creeping into households and long term, a lot of cases will end up on public lists rather than private hospitals and particularly if said austerity reduces heating, diet quality and socialactivities.

Of course there are some wily 94 year old's, rolling over half a mil for six months. They know whats coming unlike their children ,cashed up, watching , waiting.

US funds, where the money has gone .https://www.financialresearch.gov/money-market-funds/

RBNZ will go negative , along with the others as deflation circles the globe, and bugger thy neighbour currency wars ensue..

You back cowpat :)

Yes following your advice, just waiting for the phoenix to rise again.

by Cowpat | 16th Mar 20, 8:26am

The end of the New Zealand property cult.

Trolling again printer8. Unfortunately I oversee two family funds and are often unexpectedly busy. Perhaps you should consider an alternative career than a landlord if you have idle hands. .

Printer8 don't confuse cults and prices, perhaps you should take a global view rather than a Hawkes Bay myopic

by Cowpat | 31st Dec 19, 6:34pm

Ten year extrapolation , New Zealand median house price to reach 1.175 million by end 2029, Auckland a lofty 1.75 million, NZD . ( Emphasis on the NZD ) Median rent $ 675 pw

Forecasts for 2020

1. RBNZ and RBA will both reduce the OCR. For the RBNZ , GDP remains too weak to create the type of inflation it wants, after all ,we are an economy, for so long based primarily on housing. Our big cousins .Australia and China now a drag . NZ 10 year yield sub 1.0 percent.

2. 2020 real estate sale volumes will be below those of 2019. Historically the third lowest in the past 30 years. The lower OCR will not increase sale volumes as anticipated. Home ownership rates to fall ( if Stats NZ does not further adjust its numbers. )

The gap between Auckland and New Zealand ex Auckland median prices will increase.

4. Short NZD/JPY. Long JPY

5. Some bright spark will question the RBNZ forecasts and leadership.

6. Continuing on from last year, Fletchers will continue to deliver more bad news. Once the buybacks are near end , its on the chopping block.

7. China will tread heavily on toes somewhere in Asia or Pacific.

A snippet from 2019 forecast, so you may appreciate how our funds operate, by Cowpat | 31st Dec 18, 4:2.

RBNZ will cut OCR Q3, .RBA will follow in 2019 and from 2017

by Cowpat | 1st Jan 17, 11:07pm

US 10 Y will rise to 3.00- 3.25 in 2017,(( admittedly six months early)) but with the business cycle in its late stages the rise in interest rates will ensure a recession as housing and consumption crushed by 'inflation' fade. Interest rates will again turn globally lower end 2017.. Interest rates will again turn globally lower end 2017.With multiple markets enriched by 8 years of rising asset prices, the likes of Australia and New Zealand will need to lower interest rates to maintain the illusion a little longer.and ensure those with ears stuffed with dollar notes not to hear anything different. Graham Wheeler will not seek a second term , DTI will not break sweat. The NZD will reach parity with AUD by 2Q . The USD late 2017 will be the currency to own ,

Ten year extrapolation , New Zealand median house price to reach 1.175 million by end 2029, Auckland a lofty 1.75 million, NZD . ( Emphasis on the NZD ) Median rent $ 675 pw

Care to explain your extrapolation? Do you do h'hold incomes as well?

Maybe Covid has mutated and produced a growing group of winter nutters , not concerned by household incomes

"5) The next housing boom?

John Bolton, the boss of the Squirrel mortgage broker business and peer-to-peer lender, often has interesting things to say about the housing market. And his latest article is no exception.

After a short hiatus and a 5%-10% fall in house prices, I’m going out on a limb given the current market pessimism and predicting we will stretch into what might be the last great housing boom.

I thought house prices were cooked. Now I’m convinced there is another surge coming that will see the average house price in New Zealand hit $1 million in the next ten years. Some would say that’s a no-brainer because property prices double every ten years. The outcome might be the same but the logic isn’t. Others will predictably say I’m ‘just’ a mortgage broker and talking up house prices is confirmation bias."

Cowpat

Something I learnt from you. :)

Re being a landlord: I am happy either way. My previous tenants were very happy. Quite happy to look at becoming a landlord again. So nothing for you to worry about there but yet to see the 50% falls or even bubble bursts claimed by a number so may have been sadly misled there.

Re 2029: We wait and see. Personally not into guesstimates.

Re banter: I'm happy.

Cheers :)

well...the rbnz didn't think of this?? coarse they did, they wanted cheap money to finance housing before covid (even though they were trying to reduce housing investment before they decided to try and increase it!!!!!) and now trying to inspire cheap lending to try and save the economy...Im significantly in cash transaction account . Stock market is way overpriced for coming fundamentals for now, TDs not worth my time, if I need to jump Im not going to dick with 30 days notice, that's just a bankers scam....happy to wait and take the pickings. There might be some sorry looking stock market investors out there in 3 to 6 months.

Interests rates are now so low its a waste of time having the money on a TD and in a regular account you can very quickly withdraw that few thousand if things start to look ugly. The banks are in total control of what people do with their money, if you offer crap term deposit rates then people will diversify into riskier options and just plain pull the money out and put it under the mattress or in a safe.

Having any sort of cash is instant minus. I think that's the reason the real estate price is holding up. and stock market is strong even with poor outlook for companies. With real estate doom to fall, money will pour into the stock market.

Yes, I am one of those who have shifted funds from term deposits into transaction accounts.

The reality is that return on term deposits even at 1.9% less a third tax is is barely 1.2% return - it is neither here nor there. The return is especially not worth locking funds up for a year or having to give 31 days notice with penalties for early break.

Just cashed up, sitting in neutral, waiting, watching out for options.

Agreed. I'm not rolling over TDs now. Just putting them into transaction accts and using it up.

Might as well, the Greens might end up with the balance of power with the Labour ineptitudes, NZ First being such a mixed bag, National with its links to China reconfirmed etc. Oh and I am not forgetting that Labour has China links too. So there is no clear standout.

@printer8 ...me too .

I adopted a cash position almost 2 years ago when share prices got to levels that made no sense to me , disconnected from actual fair value , and in anticipation of the reversal of QE (silly me ! )

I kind of knew there was trouble on the horizon after such a good run in asset prices, and although I had no clue what or when it was going to happen , the casino was looking dangerous , and it was time to exit

I did not imagine a dead bat that someone planned to eat , would bring about such a catastrophe .

Yes term deposits of less than 100k are now not worth bothering about. Yes you might as well have it on call.

The most interesting thing to note is that collectively banks' balance sheets have shrunk ~$9.6 billion, according to the latest data release, despite significant so called "money printing" undertaken by the RBNZ.

Kauri issuance rebounded in May-June as more than NZ$2.6 billion (US$1.7 billion) priced, including a rare 10-year transaction of record volume for the tenor. Technical demand drivers are at play but intermediaries suggest positive conditions could remain even as a supply gap closes in the second half of 2020. Link

This data suggests NZ banks undertook a series hedged USD foreign borrowing deals. They might be rollover refunding operations, but it would seem the duration of this funding mechanism has been extended.

What exactly is the average interest earned by customers on those Savings account ?

Some of them may flee elsewhere if the stock market keeps performing well...

Can the Government mop up some of these savings account balances by offering a slightly more attractive bond issue ? Say 3% for a 5 year bond ? That would help the Government, right ?

I thought RBNZ/Treasury are pushing rates down, not up? Wouldn't this be the opposite?

Yep. 0.75 for a 4 yr kiwibond is not very enticing were it not for the fact that the gap between it and the banks TD rates is steadily decreasing.

Plus, 0.75 is better than the "saver" transaction accounts nowdays.

What would be the interest spread for the Banks ? Any estimate available. 2% or less ?

"Banks are being forced by their depositing customers to "borrow short", and expected by their borrowing clients to "lend long"

Which is fine IF interest rates don't rise.

But it's more than the cost of money that we are talking about here - its access to it ( both from a short term lender's redemption and long term borrower's commitment point of view).

Somewhere around here neither borrower nor lender immediately cares what the price is.

Interest rates may very well go lower, but that isn't important any longer. Access to capital is.

2.99% fixed term borrowing for 5 years, or 0.99% lending for 5 days? The price is less relevant than the access to liquidity

This appears to have similarities to the theoretical 'liquidity trap'. Where dropping rates further has no additional 'stimulus' in terms of encouraging lending and investment. People instead save because as you say the preference is to liquidity, not return. Hence they'll leave savings in a zero real return savings account (or is that even negative now in real terms?) over the ability to set up a short duration term deposit.

We're sticking with our TD's for now. We're lucky we don't need access to it - we hope. The returns are appalling but in today's market madness, not losing it is a consideration. If the banks go, then we'll all go. C'est la vie!

Why not, even if it’s just worth a couple of meals out, that is still something you might not do, if otherwise.

Looks like the start of the liquidity trap to me. Central banks drop rates to encourage 'investment' but people worry about the outlook of the economy so instead increase their rate of saving.

It might work if they hadn't spent the last decade making life precarious for too many New Zealanders. Blowing asset bubbles has negative consequences for younger generations.

This whole macro financial situation reminds me of a game of poker and nobody is willing to fold - but someone is going to lose. A lot of poker faces going on between government, central banks, retail banks, business and households.

Will it be the debt holders or will it be the equity holders that lose out? Or will it be those holding cash and not willing to invest in inflation protected investments? Intriguing times...

The winners will be those that have either inside knowledge or, those who extricate themselves from the system entirely by converting fiat money into something more tangible.

From the reserve bank

Reductions to the OCR to the effective lower bound (the point at which further OCR cuts become ineffective), which may be below zero. The Reserve Bank could consider changes to the cash system to mitigate cash hoarding if lower deposit rates led to significant hoarding.

OK that's the reserve bank basically admiting cash hoarding will not be tolerated. Cash ban is coming..

PK that is beyond my senior comprehension. What measures will the RB introduce to prevent cash hoarding and what should one do prudently, in anticipation of that?

(From the same speech re Cash Quarantining from a couple of months back. It looks like they went with LASP first up)

https://www.rbnz.govt.nz/research-and-publications/speeches/2020/speech…

"The unanticipated outcomes – such as markets functioning differently, asset prices being impacted, and government balance sheets being inflated and exposed to other risks – are understood. But, these outcomes can become more significant the longer interest rates remain so unprecedentedly low."

Foxglove

Physical cash will be banned to allow negative rates to work. Trap people in the banking system so you are forced to spend money or pay 5k a year for the bank to hold your savings.

The IMF 2017 working paper states banning physical cash will allow negative rates to work more effectively so hoarding does not occur. Also the paper suggested having serial number lotteries where notes starting with a digit are declared null and void.

What to do? I do not know. Buy a house or a car. Gold or food.

Yes will be buying a house. Got the feeling I need to diversify and fast.You cannot ban cash, what you really mean as New Zealand will be forced to go to a digital currency and cash will become obsolete. You will have X amount of time to redeem it at the banks and then it will be worthless just the same as for those that can remember the old $1 and $2 notes and small denomination coins.

That will definitely start a revolution and fights on the streets. Is the Army ready ?

Central bankers won't be able to go out to restaurants and enjoy a meal in peace, one would imagine.

These all appear to be completely mad policies to keep a broken system limping along until the next financial disaster - what a daft world we live in....

CroakingCassandra ex-RBNZ guru has explained

(a) Negative Interest rates will only apply to Retail Bank settlement accounts

(b) Retail Banks might try and pass the costs onto account holdings of greater than $100,000

(c) Retail Bank charges on large account holdings incentvises a move to cash

(d) Banks will limit cash withdrawals to $10,000 to prevent cash hoarding

PK I made this comment on the weekend news @9am as a reply to Andrewj.

It is hopefully not what lies in our future.

---

AJ are they, the CBs, destroying the world as we know it or do "they" want total control as in 1984.

Here's George Gammon with his theory and I sincerely hope he's totally wrong.

The Real Reason They Want To BAN CASH!

https://youtu.be/o48-_fY58jg

For most people term deposits become a waste of time when they drop below about 2.5 %. We are now 1.7 and Aussie 0.9

Interest rates on USD stablecoins have been slashed.

https://decrypt.co/31011/coinbase-slashes-usdc-stablecoin-rewards-inter…

Am I the only one who sees the scale used in this graph as ridiculously misleading???!!! If you showed the same graph in actual numbers (heaven forbid) we'd get a more reasonable representation of what's going on.

The postscript acknowledges that?

"Take care interpreting this chart. Each component has been rebased to the start of 2017 to show the change since then."

Acknowledged, but its one of the most misleading charts I have ever seen.

Could be that the move to transaction and on call accounts has another dimension to it. That Bank Customers have also become wary of the banks but can’t find any better alternative. Just a hint of weakness at one bank or another may create a nightmare for the Reserve Bank.

This is why it is good the government is acquiring debt - they need to spend more. More income transfers for those who would struggle to acquire debt. Moral hazard is negligible in aggregate.

"loan demand isn't strong ' .......Of course not , I am sure any prudent human is waiting to see how this mess is going to unfold before committing themselves to 5, 10 , 20 or 30 year debt .

And I get the sense that there is an anticipation among folk that prices off things are going to fall , in other words , consumers have a delfationary mindset .

And why not ?

You might as well hold back on that non-essential purchase and see what happens , after all you have nothing to lose by doing nothing

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.