By David Chaston

The people behind payday lender Moola have now moved into car finance with a similar business model.

And that includes sky-high interest rates.

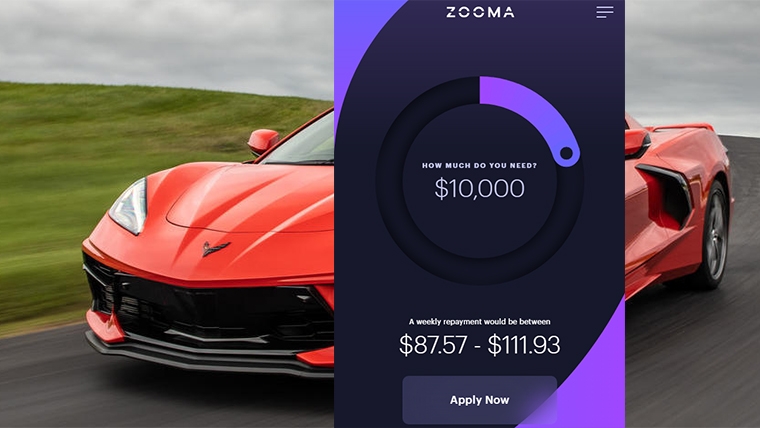

The company is seeking new capital to push harder into car finance, with a contactless, online offering aimed at millennials.

Their target is the $5.4 billion of car loan business transacted annually by non-bank lenders, using cloud-based digital-first approaches.

It recently raised a $50 mln funding line via a senior line of credit from "a syndicate of Australasian and Silicon Valley investors". At an average of $5000 per loan, this represents a new ability to fund 10,000 additional loans.

Now they want to raise another $20 mln of "additional growth capital" in the form of a Convertible Note issued by the group’s holding company NZ Fintech Group Holdings.

The offer for these Convertible Notes is that they will pay an interest rate of 12% to 15% pa paid monthly in arrears, depending on the term of three years or five years. Interest can be capitalised and compounded monthly.

They are also offering investors the option to convert to ordinary shares in the holding at year two at a pre agreed valuation, or leave it as a fixed term loan at the initial interest rate. The security for the investors is a shared GSA over the Group.

Assuming a successful Note issue, that would increase their base capacity by about another 4000 loans.

Their business model depends on borrowers focusing on the 'affordability' of the weekly payments, rather than the cost of the interest and fees included in that payment.

The "affordable repayment" is the headline feature in their app and web portals.

But fees are extensive and the interest rate range is high.

Their disclosure page reveals the interest rate is between 19.97% pa and 34.97% pa. "When we are assessing your application we take into account a number of factors including, but not limited to, your income, credit history and class of drivers licence."

The list of Fees is substantial ...

| ESTABLISHMENT FEE | $21.23 |

| Fee charged for processing, assessing and approving your finance application, this will only be charged if your application is approved. | |

| CREDIT CHECK FEE | $9.15 |

| Payable if a Credit Check is performed. | |

| LICENCE CHECK FEE | $3.15 |

| Payable if a Driver’s Licence check is performed. | |

| AUTO PLUS REPORT FEE | $13.35 |

| Payable for any checks run on vehicle information provided. | |

| PPSR REGISTRATION FEE | $15.40 |

| Fee for registration on the PPSR. | |

| TRACKER COST & INSTALLATION FEE | $400.00 |

| Payable if a Tracker is installed on your vehicle, along with the tracker cost. | |

| BROKER FEE | $499.00 |

| Payable when application has been submitted by a dealer or broker. | |

| DIRECT DEBIT FEE | $1.92 |

| Fee for each direct debit attempted. | |

| ONLINE PAYMENT FEE | $1.92 |

| Online payment method which facilitates a scheduled internet banking payment from your bank account. | |

| DEBIT CARD PAYMENT FEE | $1.92 |

| Fee for each debit card payment attempted. | |

| MANUAL PAYMENT FEE | $0.62 |

| Payable for each payment received by payment made by customer directly to our bank account rather than by direct debit or debit card. | |

| TRACKER MONTHLY FEE | $8.00 |

| Payable each month if a tracker is installed on your vehicle. | |

| EXTENSION FEE | $11.12 |

| Payable on the lender agreeing to extend the loan, or agreeing for the customer to miss a payment, or to only make a partial payment. | |

... and indicates fee income is a core part of their business model.

We ran a mystery shopping example through their calculator as follows:

Borrow: $5000

Renter in Glenfield, Auckland.

Household income of $100,000

That gave a repayment amount of $227.12 per month at a stated [minimum] 19.97% interest rate, but it did not disclose the term of the loan before asking for agreement to terms and conditions and a signature for the loan application.*

Assuming a range of terms, here is the true cost using our Real Cost of Debt calculator,

| if the term was ... | the real p.a. cost including fees is |

| 36 months | 34.8% |

| 48 months | 44.5% |

| 60 months | 48.8% |

Based on the net amount borrowed.

For the Zooma business model to work, it probably relies on customers not knowing or acting on this information. Zooma doesn't hide its fee information, but you need to look for it by clicking on the links they provide, and you need to work out what they mean.

The Zooma car loan business is an outgrowth of the Moola business where our calculator suggests the Real Cost of Debt is 52.0% pa, based on the calculator operating on their website. ($2000 for 40 weeks with a $90.32/week repayment.)

NZ Fintech director Edward Recordon says the strategy of Zooma is to "make an impact leveraging design, innovation, and technology" to connect with online prospects and get them to make a fast decision with an easy, attractive interface. The focus is all on the repayment amount without emphasising the interest or fees costs.

"Consumers now exist in a digital dynamic, with COVID fast advancing a trend and preference to do everything on mobile devices," Recordon says.

This formula seems to be working with more than 400,000 loans processed already.

According to Companies Office records, Recordon is a shareholder or director in a number of other consumer finance companies including Pacific Payment Solutions Limited, Pacific Collection Systems Limited, Fincorp Collections Limited, and Secured Asset Solutions Limited, as well as NZ Fintech Group.

* For the purposes of comparison, the same loan criteria in the Marac/Heartland Bank calculator shows a monthly repayment of $172.89 for a 36 month term, $137.05 for a 48 month term, and $115.74 for a 60 month term.

28 Comments

"Their business model depends on borrowers focusing on the 'affordability' of the weekly payments..... The focus is all on the repayment amount without emphasising the..... costs."

Where have I seen that before?!

That's the whole business model of payday lenders - supposedly cheap repayments combined with astronomical interest costs all designed to "trap" the unwary. I thought Fafoi and co were passing legislation to curb this?

I guess that makes The Banks pay-day lenders with their mortgage offerings then! Just don't say it too loudly.....

The Banks offerings don't even come close - over a 30year mortgage you'll pay about 80% of the initial purchase in interest. When I got my first mortgage an honest manager said to me - the financial difference between paying a mortgage and renting is zero over the term of the mortgage, only real difference is - at the end of the mortgage you'll own the property.

Bottom feeders.....Time to legislate these kinds of pirates out of existence.

Here's the explanation of the recent legislation;

https://www.beehive.govt.nz/release/government-takes-bite-out-loan-shar…

No doubt this business has been designed to push right to the edge of what is legal.

Yeah true that Kate.. the old saying "caveat emptor" springs to mind. Imo if buyers don't do the due diligence then they really have no one else to blame but themselves - can't protect the stupid from stupidity. Remember the old ad with the $50 dollar bill - "Let's buy it!!"

The Last time Labour was in power Helen Clark and Michael Cullen time Bridgecorp Equity Corp Canterbury Finance

Wealthy usurers predating on the uneducated poor. Why do we even allow this?

Just make education free. Eventually enough people get educated that this business model ceases to work.

Education is free. Anyone can go to a library, sit down at a computer and look up how loans work.

Same with Ponzi schemes. We all know how they work, yet they're banned in general. With some notable exceptions...

Trouble is CJ, those that need educating are unlikely to make the effort to be educated. In days gone by there was an acceptance - climb a tree, fall out, break a bone, get up and learn how to climb better - those days are long gone. The world has changed - not for the better imo

I work in IT and have met some supposedly smart people who never read their mortgage contract. It's not about education, it's about awareness. I think most people only educate themselves after they get burnt once or twice.

I agree CJ.. I work in Control System Engineering - bunch of really smart people when it comes to CSE but really DUMB when it comes to lifeskills - I know tree fellers with better lifeskill smarts than half the degreed CSE engineers

what is the point of reading the mortgage contract? When it says the bank can demand immediate repayment in full for any reason at any time, what are you going to do, take your business to another bank that has the same terms?

Putting aside the fact that education is free, this would work in the neoliberal candy world where all self-regulates but unfortunately this is not how reality works, there will always be people that will need the rule of law to defend themselves against the rich and powerful.

I'd add "putting aside the general appetite for for a multimillion mortgage" - eventually this unseemly situation will self correct. The rich will still be rich, the usual interests will continue to skew public policy and the powerful will stay powerful and influential. Anyone who thinks otherwise is doomed to a lifetime of disappointment.

Loan sharks should not be welcome in polite society (or rough society, really). Somewhere between meth dealers and telemarketers in the hierarchy.

The recent CCCFA amendments state that lenders cannot charge more than twice the principal, when including fees and interest. They must be cutting it mighty fine there

The business model. as Kate points out, will take it right to the limit

A $10k loan over 5 years will incur approx. $16k in interest based on the rate including fees in this article (48%), if my math isn't wonky.

In which case the average loan balance over 5y is $5k, which means $3.2k of interest per year - 64% int rate crudely, call it 50% allowing for compounding.

There're entire businesses and industries in the country that builds around and upon WINZ clients. I know of garages that refuse to fix your car if you're not on WINZ or sell you one.

The principle of this business model is actually quite sound, if you're working you can get fired or retrenched, but if you're on WINZ, your income is guaranteed by the government. Coupled with poor credit history of most WINZ clients, businesses are right to charge a premium on their clients.

It's actually a highly profitable business model that gives what the people wants. You want equal rights to have that car to drive or fixed, these businesses can provide you what the main stream businesses can't - it's a win-win for all participants.

Equality at its best.

Very well said, when I worked for 1 of Rado's finance companys in Auckland, beneficiary's were our preferred customers, in some cases WINZ were paying us directly..

"The responsible Lending code" is great for the borrower, I've seen loans and costs and interest refunded to clients

My mate here in New Plymouth owns one of most profitable car yards in Taranaki. He told me he has suffered no downturn since covid. He said the reason was because 90% of his customers go through WINZ. His slogan. No Deposit!

If your normal bank will not loan you $5000 on a household income of $100K and your a renter, perhaps you need to be asking yourself some serious financial questions about what your doing with your money. People that need this kind of finance are the last ones that should be borrowing the money. Loans to high risk individuals with a high number of defaults, yikes. Unfortunately the government needs to step on these lenders to help save others from themselves.

"This formula seems to be working with more than 400,000 loans processed already."

Is this in NZ? Seems to be a very high number?

In the table in the article the real loan cost p/a goes up for longer loans. Usually it's the other way around with the finance rate dropping as the fees are spread over longer.

Are bank rates actually that much lower for personal loans?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.