By Alex Tarrant

Taxpayers may be in line for a NZ$337 million hit from the government's backstop agreement with insurer AMI, if the Christchurch-based insurance company is not able to raise new capital by 2015.

Insurer AMI, which is heavily exposed to the Christchurch residential property market, announced on Tuesday the cost of the earthquakes that have hit the city since September last year was likely to be about NZ$531 million above its available reinsurance. It also booked an additional NZ$229 million contingency for costs largely related to the February 22 quake. AMI financial statements showed it had gross outstanding claims from the Christchurch earthquakes of NZ$1.937 billion in total, while it had NZ$1.197 billion in reinsurance receivables.

AMI announced a NZ$705 million loss for the year to June 30, 2011, compared with a profit of NZ$33 million the previous year, chairman Kerry Nolan said. That was not a cash loss, and reflected the expected costs of the earthquakes which hit Christchurch, Nolan said.

Nolan said the company would be in need of the government's capital committment of up to NZ$500 million if it was unable to recapitalise by 2015, although work was progressing on recapitalisation plans, with AMI set to soon go to the market in search of new funding.

That would most likely be through an outside investor taking an equity stake in AMI, which would mean the company would lose its independence as a mutual. AMI had previously said it would like to remain a mutual company if possible, meaning it was fully owned by its policy holders.

Finance Minister Bill English said based on AMI's NZ$705 million loss in the year to June 30, the best current estimate of the likely cost to the government of its support package for the company was NZ$337 million. This would be booked as an impairment in the government's accounts for the year to June 30, set to be released in October.

Quake costs

"AMI has NZ$2.3 billion in assets including NZ$1.2 billion of available reinsurance receivable, its own cash and investments and the unpaid NZ$500 million of Crown capital committed to the company by the Government in April," Nolan said in a media release.

"The Government agreed to contribute the capital, if needed, to enable the company to use its own cash and investment assets of some NZ$400 million to help meet earthquake claims," he said.

“AMI continues to trade strongly. We are able to pay all normal day-to-day and earthquake claims as they are settled. We have effectively set aside NZ$760 million, which includes a large contingency, to pay earthquake claims as they are settled over the next few years and have already paid out NZ$80 million,” Nolan said.

He said several potential investors have made approaches since AMI appointed Goldman Sachs to oversee a capital restructuring by attracting a new investor as it seeks new capital.

Set to lose mutual independence

Nolan told interest.co.nz that recapitalisation talks were well advanced, with AMI set to go to the market “in the near future,” looking for an investor to join with an equitable holding in the company, rather than raising cash through a bond issue or borrowing.

However AMI had yet to resolve completely how the capital would be raised. Either way, there would need to be an injection of money from an outside source, Nolan said.

“But it isn’t hard for a mutual to raise capital, it just is a little different from a company limited by shares, because we can’t look to our members. But of course we have effectively raised capital from the government, so it can be done,” Nolan said.

“It’s fair to say it [the new capital] will be through an equitable holding rather than bonds or borrowing because of our solvency requirements under the Reserve Bank,” he said.

“At the end of the day, AMI will be owned wholly or partly, or as a majority or minority, by an outside investor.”

AMI has been New Zealand's largest mutually owned and locally owned general insurer. It has 500,000 policyholders who have effectively been its owners and will see their ownership diluted. AMI has not disclosed who might be potential buyers, but NZX-listed Tower has already expressed an interest and Australia's Suncorp Metway (which owns Vero and most of AA Insurance) and IAG, (which owns State and NZI) are potential buyers, as is the Wesfarmers' owned Lumley and QBE Insurance.

How much would be raised was up to the investors being talked to, which included both local and international investors, with some in the insurance business.

“We want to get the best price and it depends on what the investors are prepared to offer,” Nolan said.

'Might split into good and bad'

Capital raised by any recapitalisation would be used to help cover the earthquake liabilities, regardless of whether AMI separated its business into a good part and bad part, which was a likely scenario.

“If we want to maximise the price, of course what the purchaser wants is certainty. Because there is, even now, no real certainty as to the magnitude of the earthquake liability, one of the options is to separate the earthquake [part] out, and offer to the market the business as usual, as it were, part of AMI Insurance,” Nolan said.

If that were the way forward, then the capital introduced to AMI would flow back to the earthquake part, or ‘bad book’ of the company.

That would mean the government’s backstop would be called upon if the amount of new capital was not enough to cover that part of the business.

However, there were other variables, such as the NZ$229 million contingency for the February quake, Nolan said.

“I’d rather not be too specific about AMI because it may not happen this way, but you could have an insurance company in this sort of position, or with large debts, which formed a subsidiary, sold the good assets, whatever they happened to be to the subsidiary, and took a debt back, so that as new capital flows into the subsidiary it is then paid back to the parent.”

Nolan said he could give an “absolutely unequivocal guarantee” that any new capital would be used to help cover costs from the earthquakes.

“One of the reasons is that the capital raised needs the consent of the Crown, and if that were not to happen, the Crown simply wouldn’t consent. So there is absolutely no doubt that all new capital will assist with the reconstruction of Christchurch,” he said.

There were other options than splitting the company two, with AMI to a degree in the hands of the successful investor, and the government.

(Updates following interview with AMI Chairman Kerry Nolan)

See the release from AMI below:

AMI Insurance says the cost of claims resulting from the Canterbury earthquakes, over and above the company’s available reinsurance, is likely to be about $531 million, in line with earlier estimates.

Announcing its results for the year to June 30, 2011, AMI says it is also providing an additional $229 million risk margin (contingency sum). Almost all of the costs relate to the February, 2011 earthquake.

The calculations of the likely cost of claims and a prudent contingency sum have been provided by an international actuarial consultancy commissioned by AMI. They take into account the recent upward revision by the Earthquake Commission of the number of house claims they expect to receive over their maximum level of cover.

“These calculations are the best estimates available, but it will be the middle of next year before the company has reliable projections based on resolution of claims to that point,” says AMI Chairman Kerry Nolan.

The calculations of net earthquake claims and the recommended contingency sum have been included in the company’s annual accounts to June 30, 2011, resulting in an after-tax loss of $705 million.

AMI has $2.3 billion in assets including $1.2 billion of available reinsurance receivable, its own cash and investments and the unpaid $500 million of Crown capital committed to the company by the Government in April. The Government agreed to contribute the capital, if needed, to enable the company to use its own cash and investment assets of some $400 million to help meet earthquake claims.

“AMI continues to trade strongly. We are able to pay all normal day-to-day and earthquake claims as they are settled,” says Mr Nolan. “We have effectively set aside $760 million, which includes a large contingency, to pay earthquake claims as they are settled over the next few years and have already paid out $80 million.”

ANNUAL RESULTS

Announcing AMI’s annual result for the year ended June 30, 2011 Mr Nolan says the company would have made a record profit but for the impact of various earthquake-related costs during the year, and the need to make provision for the future payment of earthquake claims.

Instead, AMI has recorded an after-tax loss of $705 million compared with an after-tax profit of $33 million in the previous year.

Gross written premium income of $362 million for the year compares with $341 million in the previous year.

“Almost all of the loss has been caused by claims related to the February earthquake, rated as a one in 2500 year event. This was the most damaging disaster in New Zealand’s history and, I believe, the most expensive insurance situation to occur in any country relative to GDP.

“In making provision in the accounts to June 30, 2011 for future claims, we believe we have allowed for worst-case scenarios and added an appropriate contingency sum, but only time will tell what the final figures will be.”

Mr Nolan says AMI is confident about its trading situation and expects to show a trading profit in the current financial year.

“In the meantime we are strongly focused on continuing to run a major New Zealand insurance company providing secure cover for almost 500,000 New Zealanders, and we are able to meet all valid claims.”

PAYMENT OF EARTHQUAKE-RELATED CLAIMS

Mr Nolan says finalising earthquake related claims is a very complicated and time-consuming process, as policyholders have a variety of options. These depend not only on the terms of their policies, but also on Government decisions being progressively announced for each “land zone” and the need for AMI to work closely with the Earthquake Commission, Local Authorities, the Canterbury Earthquake Recovery Authority and the Government.

“Some properties have had to be assessed more than once, having been damaged in successive earthquakes. In many cases repairs have been deferred until there is more confidence that seismic activity has ceased. There is still considerable uncertainty in Canterbury.

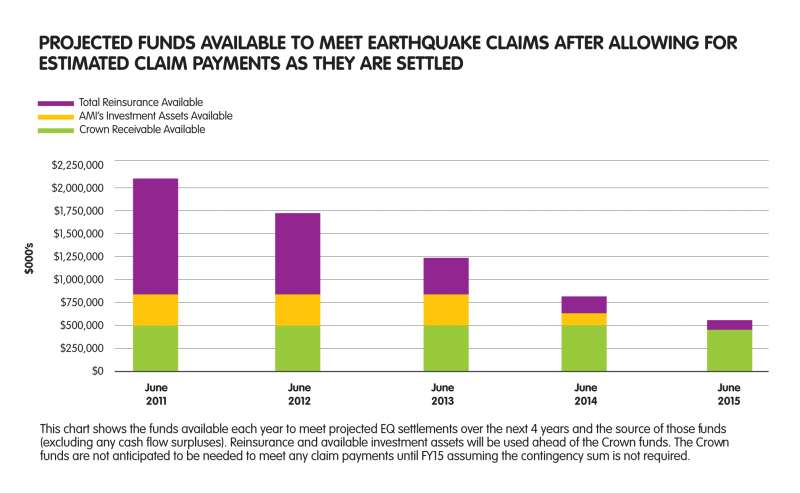

“We estimate just over one-third of claims will be paid out in the coming year, a similar amount in the June 30, 2013 year and about 20 per cent in the following year. I emphasise that all claims will be paid as they are settled.”

AMI has recruited nearly 200 people to join its dedicated Earthquake Recovery Team which is helping customers with their earthquake related claims. AMI has also engaged Arrow International to help expedite assessments of more than 7000 houses and project manage their repair or rebuild.

IMPACT OF EARTHQUAKES ON COMPANY

Mr Nolan says the growing impact of the earthquakes on the company’s resources will be felt in both the current financial year and the following two years year as the payout of claims gathers pace and the company begins to supplement the available re-insurance with its own investment assets in the year ending June 30, 2013.

“For the September 2010 earthquake claims will slightly exceed the $600 million of reinsurance available for that event. Claims related to the February earthquake are expected to exceed the $600 million of re-insurance available by a very considerable margin. Immediately after the February earthquake, the company purchased extra reinsurance of $1 billion. This meant that claims relating to the June earthquake will be very comfortably covered by our reinsurance.

“We will have more accurate projections by mid 2012, when most assessments will have been completed and enough rebuilds will be in progress to give a reality check on previous estimates of project management costs and inflation in labour and building product costs.”

RECAPITALISING THE COMPANY

AMI has established a Board Committee to oversee the capital restructuring of AMI by attracting a new investor and has appointed Goldman Sachs as advisers to help raise new capital.

“Several potential investors have already made approaches and the Board looks forward to a successful outcome. A process will be adopted which ensures that AMI’s ongoing business is ring fenced from its earthquake liabilities.

“We are grateful for the ‘Backstop’ Agreement, announced in April, for the Government to contribute $500 million in capital if needed,” said Mr Nolan. “Their strong support as we work through the process of recapitalising the company has been invaluable and is contributing greatly to the orderly resolution of the Canterbury earthquake claims.

“The Crown has already been issued with convertible preference shares in AMI enabling the company to draw down the $500 million when it is needed. The recapitalisation process the company is undertaking is expected to resolve a requirement in the Crown Support Deed for the company to have a minimum level of capital.

“This Agreement gives us breathing space to seek new capital in a manner that maximises the value of the company. We are very hopeful we will be able to conclude an acceptable transaction.”

OUTLOOK

AMI believes the prospects of recapitalising the company and strengthening its balance sheet, by attracting a new investor, are positive.

In the uncertainty following the earthquakes the company says it has maintained customer numbers, and is continuing to win new business. While insurance premiums are increasing as a result of the increased cost of reinsurance, customers understand that this is inevitable due to recent catastrophic events around the world including the Canterbury earthquakes, Japan’s tsunami, Australian floods and tornadoes in the United States.

AMI has reinsurance in the current year of up to $ 1.4 billion for any major event in New Zealand.

AMI is a major insurer of homes in Canterbury, where the company originally began business in 1926.

AMI is the largest wholly New Zealand owned fire and general and personal lines insurance company. It has a current financial strength rating of A – (Excellent) from international rating agency A.M. Best Company.

The company has 73 branches, two contact centres and 21 agencies throughout New Zealand (the largest network of any insurance company), nearly 1000 staff, and around 500,000 New Zealand customers holding 1.2 million policies.

ENDS

Issued on Tuesday, September 20 by AMI Insurance.

Further information, including the Annual Report and Year in Review, is available on www.ami.co.nz ( http://www.ami.co.nz/annual-report-2011/ ).

Here is the statement from Finance Minister Bill English:

The Government is standing behind its support agreement for AMI Insurance policyholders, as Treasury continues to work closely with the company on recapitalisation options, Finance Minister Bill English says.

Commenting on AMI’s annual results announced this morning, he says the Government has not been called on to pay any money under the support agreement.

“AMI is using its own capital reserves and reinsurance to pay claims from the Canterbury earthquakes as they come due,” Mr English says.

“When we put the AMI policyholder support agreement in place back in April, AMI started a programme to raise fresh capital.

“The Treasury has been working closely with the AMI board on securing new private capital for the company.”

In April, the Government announced a backup financial support package to give AMI policyholders certainty and to ensure an orderly rebuild of Christchurch in the aftermath of devastating earthquakes in September and February.

The support package will be called on only as a last resort if AMI’s own reserves have been exhausted – unless the Government believes it is in the public interest to take control sooner.

If called on, the package would involve the Government investing up to $500 million of equity in AMI, with the right to take ownership and assume control of the company if needed.

The ultimate cost to the Government will depend on the final cost of AMI’s claims, which remain uncertain, and the outcome of AMI’s recapitalisation process, which is still underway.

However, based on the $705 million annual loss reported by AMI today, the best current estimate of the likely cost of the Government’s support package is $337 million.

This will be reflected as an impairment for that amount in the Government’s annual accounts for the year to 30 June, to be published next month.

“AMI Insurance has set aside a large amount of money in anticipation of future claims from the Canterbury earthquakes, which is the prudent thing to do,” Mr English says. “In addition, reinsurers continue to support AMI, with $1.4 billion of reinsurance in place to cover any further disasters in the 2011/12 year.

“The company’s underlying business and earnings - without the impact of the earthquakes and the need to provision for them - remain strong.”

20 Comments

Is AMI the only insurer who screwed up , and needs a tax-payer bail-out .. .. are there others ?

...... are they " too big to fail " ... .. else why are they getting a special favour , a life-line , courtesy of the tax-payers of NZ ?

Why doesn't the government just nationalise AMI , and sack the board of directors ( no bonuses , gentlemen ) ... .. because these guys appear to be seriously incompetent ?

....... does anyone on the board of AMI actually have a background in the insurance industry ?

If other " too-big-to-fail " companies , such as Fonterra , or Fletcher Building get into trouble ... if they bugger-up ( at no fault of the tax-payer ) will the government step in and bail them out too ?

Nationalise the taxpayer !!!

Nationalisation is what Labour might call it - National prefer the word "support".

Same difference to me.

“The company’s underlying business and earnings - without the impact of the earthquakes and the need to provision for them - remain strong.”

I suspect most insurance company's earnings would also look 'strong' if you took out their need to meet claims.

How do you recapitalise a company with $337 million of negative equity?

Bill, how is that track to surplus looking?

More gun fire- before guns fire.

This piece makes more sense than the way it has been reported on the Stuff site but it is still a bit confusing. I think it all means that AMI have enough reserves and reinsurance to meet the claims they have plus a chunky contingency but that wont leave them solvent enough to keep trading as an insurer as they wont meet the prudentail requirements without the governments 500 mil backstop. I think it also means that, with all current information the Government is taking a 337 million contingency into its 2011 final accounts ( ie added to the deficit) rather than the 500 million of the guarantee.

I dont think it means Bill has had to write out a cheque yet and probably wont have to if AMI can recapitalise or is sold to Tower .

Given the understandable problems with insurance in Christchurch ( any sensible insurer wants the ground to stop shaking before they accept any more risk ) and that this problem may stymie the CHCH rebuild for months or years maybe the Government should write out the 337 mil cheque, take over the company as it is allowed to do under the terms of the guarantee and use AMI as the vehicle to get CHCH moving again. It is a Canterbury company after all.

Earthquakes being unpredictable there is probably ( sort of an insurance term ) not significantly more real risk of another damaging shake in Christchurch than there is anywhere else in the country.

I think you are dreaming. AMI says it needs to find $760 million (being $531 million + $229 million).

AMI Insurance says the cost of claims resulting from the Canterbury earthquakes, over and above the company’s available reinsurance, is likely to be about $531 million.

AMI says it is also providing an additional $229 million risk margin (contingency sum).

From its tangible assets being: its own cash and investment assets of some $400 million

So AMI is in no way solvent without the governments $500 million, and possibly not even with it if their current contingency proves inadequate.

So its probably time the board retired, with suitable renumeration of course, enough to retire in comfort and live out their remaining days to the standard they have become accustomed, close to a golf course and airport so they can spend all the air miles accumulated over the years attending board meetings.

It's highly unlikely that AMI have nailed down final costs.

Most insurers haved even opened the files on the majority of their claims. Many big claims will still be stuck in EQC limbo too.

AMI has surely benefitted from EQC picking up multiple insurance claims. It seems a simple calulation, that if AMI insurer a third of properties (albeit the cheaper ones) then at a minimum 30,000 are overcap, so if AMI gets away with 10,000 at an average of $60,000 they will be doing well. Add in all the "small" non EQC covered claims, and contents claims then there might be 40,000 claims at $10,000, so about $1b is probably somewhere near the money.

Hence AMI might survive, however if the multiple claims not been paid by EQC, then AMI could easily have been on the hook for $1.5b plus, wiping out all of their capital.

I note that AMI has been particularly tardy in making payments. My sister with a damaged drive had agreed to cash settle many months ago, yet still no money has turned up, it seems insurance companies like to promise the earth then when it comes to showing the cash either reneg, stuff about or just make it generally difficult.

Im in the same boat as your sister Chris J (not with AMi though), rushed around gettting all quotes etc..sitting on someones desk has been for months, EQC was done and dusted ages ago, but stuck with insurance company, I honestly believe they will string this out (paying) for at least 5-6 years if not longer.

in other words, AMI are MIA

Confusing as I said. The statements say available reinsurance of 1.2 billion and allowance for claims in excess of this of 531 million which is 1.731 billion in total claims and a lot more than Chris' back of the envelope calculation.

It is also claimed total assets of 2.3 billion including 500 mill from crown and 1.2 billion in reinsurance which leaves 600 million of which 400 is cash and investments. Maybe the other 200 mill is buildings and other hard assets and maybe some intangibles which wont be easily converted to cash to pay claims. Also not clear if the 80 mill already paid out is included in the 1.731 billion provision for total claims.

Presume someone knows.

I see in the Press today they saying may take up to 4 years to pay out........lets double that to be realistic...and lets hope there is no more sizeable shakes that cause damage or may as well kiss that claim goodbye for at least 10 years. The Nats were banking on this rebuild for their growth forecasts...Yeah right

It hardly seems like "insurance" if an insurer takes 10 or even just 4 years to settle a claim.

10 years is the time it would normally take to pay off a house. The loss of income for that time is unthinkable.

Government needs to (and should have immediately) taken action to define what is a reasonable time to settle an insurance claim. Legislation needs to be in place to penalise insurance companies that dilly dally. Most contracts have penalty clauses, why is it not mandatory for insurance policies to have penalty clauses?

Even the mere threat of introducing such clauses would spur insurers along.

Why doesn't Gerry just get on with it and stop pandering??

Bernard, in regards total AMI claims.

I haven't looked at the numbers reports thoroughly, but just as a back of the envelope calculation:

AMI say they have a total of 33,000 claims, including 4,000 total rebuilds and 3,000 overcap major repairs. (Reported in today's Press).

Now even if the average rebuild was $350,000 (that's high as AMI generally insured cheaper homes), then assuming EQC pick up an average of $150,000 (which is a low estimate given multiple payment obligations) then AMI has a maximum $800m liability, a low end estimate might be ($300k build cost, $180k EQC) hence a minimum $480m liability.

Say the average of the repairs was $250,000 (again a high estimate) and the average EQC $130,000 (again a low estimate) then AMI has another maximum $360m liability. A low end estimate might be ($200k repair, $160k EQC) hence a minimum $120m liability.

Now the remaining 26,000 claims (non eqc coverage plus excess chattels, cars etc) can't average more than $20,000, but may well only average $10,000 so that's $260m minimum to $520m maximum.

Total that up and we get (based on AMI's estimate of claim numbers) a minimum liability of $860m and a maximum liability of $1.68b.

Now this is assuming that they had no commercial policies at all. My personal view (based entirely on the number of claims AMI currently purport to have, and the fact that the average ChCh house is under 150m2 and that AMI insured mainly cheaper properties, is that $1-1.3B would cover most of AMI's claims.

But how does the Government come up with over $2b as the likely cost to AMI?

Has AMI got the total numbers of claims wrong? Does the Government know something AMI doesn't (like they are about to through a lot more overcap EQC claims their way?) Or is it just like everything we've heard from the Government so far about the earthquakes, more proof that they don't know what they are doing?

Chris_J,

Your calculations are only considering damage on a 1 event basis. For insurance purposes, incremental damage needs to be attributable to singular events. This adds in many more complexities around reinsurance arrangements

Chris_J,

Your calculations are only considering damage on a 1 event basis. For insurance purposes, incremental damage needs to be attributable to singular events. This adds in many more complexities around reinsurance arrangements

Whatever way you look at this there has been a giant cockup. The trouble with mutual structures is the total lack of accountabilities. It breeds incompentence! How can an insurer get their sums so wrong. They have now admitted to claims of around $1.2b to 1.5b and a shortfall of at least $340m.

We the poor tax payers are the ones having to front up for these amounts.

Who is going to take responsibility for making such a catastrophic error of judgement.

1. John Balmforth - CEO?

2. The Board and Kerry Nolan the Chairman?

As a policyholder and a taxpayer I want to see some people putting their hands up here and falling on their sword.

What a mess!

Interesting. The juicy bit for me is that AMI are still trading when even after the capital injection they are under the Minimum Solvency Capital standard.

So in effect the either the new Insurance regulations are being interpreted by the Reserve Banks in a rather interesting way. Or the government is effectively offering AMI a further captial life line, and AMI is taking it, without having to pay for it. Most insurers would kill to only have to return $15million on a govt backed $500 million captial call.

My gut feeling is AMI is unlikely to succeed in raising the captial. Even in 2010 (a good year) they only made cirica 30 million profit. I can't see anyone investing 500 million (probably more like 600 million) for a 30 million pa return.

They seem to be playing up that they are in a ok cashflow situation. But that in effect turns AMI into a very "interesting business model", and once the captial is returned to the crown, they are back below the MSC.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.