By Bernard Hickey

Fairfax Media has released the 257 page prospectus for its float of Trade Me on the New Zealand stock market to the Companies Office this afternoon.

It shows New Zealand's biggest online retailer forecasting 12% revenue growth next year, 10% profit growth and a 5.1% cash dividend.

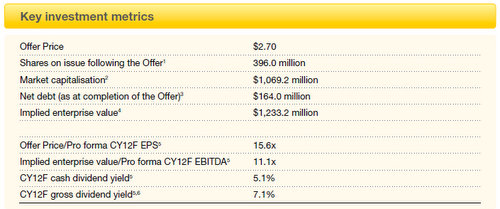

Fairfax Media is selling 134.6 million shares at NZ$2.70 a share to raise NZ$363.5 million, including the sale of up to 7.6% of the company to Trade Me and Fairfax staff, Fairfax shareholders and very active Trade Me members.

Of the 30% of Trade Me up for sale in the float, more than half the shares will go to retail investors through New Zealand brokers.

The prospectus also details issue expenses of NZ$11.8 million to be paid to brokers, including fees of 2.5% to the underwriter UBS, and up to 1.5% to brokers, co-lead managers and co managers (Craigs Investment Partners, Goldman Sachs, First NZ Capital, Forsyth Barr, Direct Broking and ASB Securities)

Fairfax Media will retain 66% of the shares after the initial public offering (IPO) or float of the shares on the NZX.

There are 118.8 million shares issued to institutions (fund managers) directly and to retail investors indirectly through brokers, including co lead managers Craigs Investment Partners, Goldman Sachs, First NZ Capital and Forsyth Barr and Co managers Direct Broking and ASB Securities.

There was no breakdown immediately available showing how much would go to institutions and how much to retail investors. There are 15.5 million shares allocated to Trade Me and Fairfax employees, and to 28,000 eligible Trade Me members, who will be notified by email within the next day.

The prospectus shows Fairfax Media opens the offer on November 17 and closes it on December 6, before starting trading on December 13.

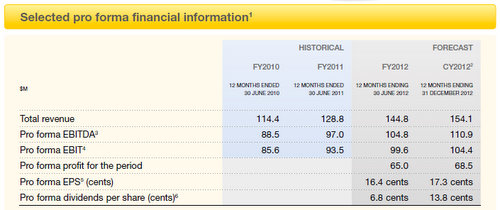

The prospectus includes forecasts for pro-forma earnings per share of 17.3 cents per share in calender 2012, up from 16.4 cents per share in the year to June 30, 2012.

It also forecasts dividends of 13.8 cents per share in calendar 2012, up from 6.8 cents in the year to June 30.

This implies a cash dividend yield to the offer price of 5.1% and a gross dividend yield (after imputation credits at a company tax rate of 28%) of 7.1%.

Trade Me said it planned to pay out 80% of its profits at 6 monthly intervals, "subject to its outlook and liquidity requirements."

The forecast points to an implied market capitalisation at the offer price of NZ$1.069 billion and total revenues of NZ$154.1 million in calendar 2012, up from NZ$144.8 million in the year to June 30, 3012 and an historical NZ$128.8 million in the year to June 30, 2011.

The directors will be Trade Me founder and Fairfax Media director Sam Morgan, former Fairfax Media CEO David Kirk, Fairfax Media General Counsel Gail Hambly, Fairfax Media CEO Greg Hywood and independent director and former KPMG partner Joanna Perry.

Trade Me elegible members would be included in the 'Priority' offer of 15.5 million shares to Trade Me and Fairfax NZ employees, as well as Fairfax shareholders.

These members include:

The Trade Me Member Offer is made to Eligible Trade Me Members, being either:

• enabled members of Trade Me’s online business website with a feedback rating of at least 500 as at 28 October 2011; or

• enabled members of the Top Seller Programme as at 28 October 2011; or

• enabled members who have qualified twice for the Top Seller Programme in the period between 28 June 2011 and 28 October 2011.

Trade Me will have NZ$166 million of debt once restructured and floated. The loan is from Commonwealth Bank of Australia from a total unsecured facility of NZ$200 million.

The covenants on the loan include that the debt must not be more than 2.5 times EBITDA and that EBITDA must be at least 3.25 times Trade Me's net interest payments. The prospectus lists goodwill at a value of NZ$721.6 million.

The float is being underwritten by UBS NZ and Trade Me's ticker will be "TME"

Trade Me's non executive Chairman David Kirk said the float was a great “next step” for Trade Me.

“The website Sam Morgan started back in 1999 has evolved to become the leading online marketplace and classified advertising business in New Zealand, but more important than that it’s firmly established as a liked and trusted Kiwi brand. This IPO is going to give Trade Me’s community of 2.8 million members an opportunity to own a slice of a website they know and use," Kirk said.

'Financial flexibility'

Kirk said Trade Me would have increased access to capital and more financial flexibility once listed.

Trade Me CEO Jon Macdonald said he was looking forward to leading the new publicly listed Trade Me.

“The one thing about this business is that it is constantly changing, and this is another exciting step in Trade Me’s evolution. However, it’s important to point out that the way Trade Me works, and our focus on providing a safe and trusted marketplace for Kiwis to buy and sell will remain the same," he said.

Trade Me expects to achieve earnings before interest, tax, depreciation and amortisation (EBITDA) of NZ$110.9 million in calendar 2012, which would be up 10% from the current year.

Fairfax Media said in a statement to the Australian Stock Exchange about 30% of the 118.8 million available after the priority offer have already been allocated to institutional investors and brokers after a 'bookbuild' process whereby UBS guaged interest from fund managers.

It said about 75% of the shares allocated in the bookbuild had been allocated to New Zealand institutions and brokers.

There is no general offer so any 'Mum and Dad' retail investors will have to buy through of of the co-managers or co-lead managers.

'Defamation action'

Page 111 of the prospectus (pending proceedings) detailed a legal action by Joe Karam, the former lawyer for David Bain, alleging defamatory were published on Trade Me forums by Trade Me members.

"It is alleged that that Trade Me is the publisher of those statements and may be held liable accordingly," the prospectus said.

Court hearings are expected in 2012 unless the matter is settled before then. Trade Me said "any damages would be at the discretion of the court."

There is more information at at ipo.trademe.co.nz

(Updated with more detail from prospectus, news release, including fees, more than half banker for loan and Karam defamation action)

Disclosure: Interest.co.nz has a business relationship with Trade Me. Advertising on Interest.co.nz is sold through Trade Me's advertising sales team, which receives a commission. Also, Bernard Hickey was a member of Trade Me's advisory board in 2007 when employed as Fairfax Media's Head of Digital for NZ.

Here is the full prospectus below hosted on Scribd:

We welcome your comments/analysis in the comments below.

30 Comments

Fairfax are doing themselves & the backing 'brokers a great big favour , but not you ! This is a comparatively expensive IPO .

.... from the figures supplied , TradeMe is being floated at 15.6 times current net earnings . Not overly expensive , but no bargain neither , when a multitude of existing stocks ( such as Michael Hill , NZX : MHI ) trade at PE ratios of less than ten .

And a big chunk , the majority of TradeMe's assets are " intangibles " , A.K.A. goodwill . Actuall casheable assets are a fraction of the share price .

..... and one last Gummy grizzle , this is a low growth stock now . It has saturated the NZ market . It will spin off excellent dividends for retired folk , who want a regular income stream . But TradeMe is being floated at a growth stock multiple . Younger investors are advised to look elsewhere .

Well it has a huge market share that seems at least for the next few years "safe" (ignoring the effects of a depression, which might perversly actually make it do better) Personally I think all growth stock is history......good, safe dividend stock interests me.....guess that makes me old :P but not at 15.6 to 1.......8 to 1 yes...

"Younger investors are advised to look elsewhere"......yet if its low risk....protecting your wealth for a few years until things clear seems fairly sensible.......I will stay in deposits etc for now though...safer still.

regards

Yep, those were my thoughts exactly, gummy. When my broker told me the price had been set at the upper end at $2.70, I said I'm out. At a P/E of 15.6 for a company with in my view limited growth potential (it already dominates/ saturates the market here and it can't go offshore) that's too expensive in my view. And I'm not convinced about those future projected growth in earnings either, (and correspondingly the excellent dividends for the retired that they imply). It's wait and see for me.

Hello DB : I would not be at all surprised to witness TradeMe selling well above the float level , for several months . It may be a good situation to " stag " for a one off capital gain . Much as Rakon did , it become the " tech " darling of the NZX , and the price soared as it was deemed to be the perfect stock , until reality proved that it really wasn't .

...... in it's favour , TradeMe is a low capital business , so it can make a high margin on relatively low revenue . But the flip side to this is that it's margins are vulnerable to competition .

Fairfax are deeply in debt , and are primarily operating within a declining industry , newspapers . As such , I expect that more of their retained 66 % stake in TradeMe will come onto the market , in the years ahead , diluting the public float .

Great Company

Well managed

Low capital requirements

Limited growth prospects

Will be overpriced by mum & dad investors and enthusiastic fund manager investors with very limited analysis skills.

There is nothing to stop an e-bay or the like coming to town and while TM have a dominant position - someone prepared to lose money over time will take market share eg 2 Degrees has had a huge impact on Vodafone & Telecom and their bottom line.

The risks here are geater than many would believe.

but the market is small......lets say ebay comes.....its then a small market with cutthroat pricing and over-valued goods......there is just no point....

regards

Why would any corporation float on the NZX during what could arguably be the worst fiscal crises in human history? Someone needs to tackle the CFO over there!

Its times like this I only wish we were allowed to short stocks on the NZX. :(

Burger Fuel anyone?

"Why would any corporation float on the NZX during what could arguably be the worst fiscal crises in human history? "

Because their parent company badly needs the cash...

Almost all posters so far confirm my suspicion that the high P/E is a complete turn off.

They rely on "soft" PIs for support.

I cannot see how the "Book Builders" helped this on its way.

Don't be too quick to give TradeMe the brush off , Basel . .. . " horses for courses as they say " , TradeMe stock will suit retirees nicely , slow growth , but steady and generous dividends . A reasonable income play , as indeed are the REIT's , the ports , and the Warehouse .

..... us younger investors seek a little more growth potential , and stocks such as Michael Hill fit the bill admirably .

[ Disclosure : GBH has got some MHI shares ]

So a DotCom company is a yield oriented play, not a growth investment? I'm not that keen to see Fairfax pillaging the balance sheet before they float as well.

I agree, some mums and dads will possibly push the share price up initially (unless global turmoil hurts the launch). But whether it's sensible for long term ownership, that I can't say with any enthusiasm.

I'd rather put my money into proven growth companies like Ryman Healthcare, or speculate on a technology company like Diligent or biotech/medical like Pacific Edge.

I wouldn't characterise Trade Me as a 'DotCom' company. Yes it's internet-based, but there's a real business there and more importantly a track record of real profits.

However, I'm sceptical of it's on-going prospects as others have mentioned. There's no real opportunity for growth in the New Zealand market, as everyone likely to sign-up has signed up. The only real way for TradeMe to increase revenue seems to be to increase its fees, which leaves it open to competition.

I think they are going to have to change a lot in the future. They do have potential for growth, but in new products, rather than existing ones. I haven't really seen anything revolutionary from them for several years, since they entered the realestate and job markets, which were very good moves. I can't see them expanding successfully to OZ, as they already that the trademe equivalent, Ebay, which is hte dominent player. I think they may need to become an NZ version of Amazon and also integrate more social media into their products. They are doing this a bit with their daily deals, but I don't think that is partically good, and they appear to now subcontract that out to one of the daily deal companies. They have 'School Friends' which was like facebook , but that webite hasn't kept up. There message boards have huge potential, and I think it is one of NZs biggest online communities, but there are a lot of nutters on it.

There is Sella that could ramp up their offerings, and also Ebay which is the biggest player around the world, so there is potentially huge competition out there.

There are some minor markets they can expand into, like "TreatMe" (their take on daily deals), but I wonder whether Yellow, Localist and APN might start a price war now that TradeMe have had their balance sheet pillaged by the parent company, and might not be so keen to see margins attacked by their opponents.

Updated with detail that about half of the shares being sold publicly are allocated for retail investors through New Zealand brokers.

That's about NZ$160 million worth. A fair chunk.

cheers

Bernard

Heh heh , yes Bernard : The underwriters are being generous to retail investors , offering $NZ 160 million of TradeMe shares .......

...... and that is because Goldmoney Sacks and their ilk care about Mom & Pop ? ......

.. not because they're concerned that it may fail to open at the IPO float price , and leave them holding the bag ........

Silly Gummy , the 'brokers wouldn't do that , they love us private investors , really they do ...

...aha ha ha de haaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaa !

My punt would be to wait for the opportunity to buy in at circa $2.20

What chance of that?

I will wait and see. That has more attraction than trying to stag the open.

Ask youself these two questions :

1 : Why did the originators of TradeMe ( Sam Morgan et al ) grab the $NZ 700 million that Fairfax offered them , and not want to keep a single penny still in the firm ?

2 : Why are Fairfax now cashing up some of their stake in TradeMe ? ..... not a solitary penny from the proceeds of the IPO is going into growing the business .

Those " in the know " are fleeing from this firm , so why would you step into TradeMe , when they're running out .

e bay gum?

GBH - precisely. The Fairfax record with Trademe has been a license to pillage TMs balance sheet in order to reduce their parent company debt.

The money is being used to retire crappy newspaper debt.

TM doesn't need a big cash injection anymore, it can fund it's own growth. If not from banks and private equity, then easily from issuing a bond.

The Trademe IPO then, is for Fairfax's benefit, not for the company.

So why are mums and dads lining up to make Fairfax rich - rather than themselves?

However, I don't blame Sam Morgan for taking his money out of the business. He had other investors who wanted to be cashed up and take the great offer from Fairfax. The deal with Fairfax is much cleaner (and probably superior) when Fairfax could gobble it up lock stock and barrel.

And besides, Sam's entitled to be rich, happy and well diversified.

Why is TradeMe now $ 164 million in debt ? ....... it was started up from nothing , and has been cashflow positive throughout it's lifetime .....

.... so on what basis did Fairfax lumber the firm with a debt millstone ...

( GBH cannot download the prospectus : Meebee someone will be kind enough to enlighten me on this point . )

@GBH you can dowload the dox from the Trademe site - http://ipo.trademe.co.nz/

This is interesting - from page 10 of their IPO document.

Release of guarantees

Trade Me has in the past guaranteed certain indebtedness of Fairfax Media and its other subsidiaries. The relevant guaranteed monies have been repaid in the ordinary course and, accordingly, Fairfax Media has requested formal releases of the guarantees but some of these have not been obtained. The most recent of the repayments of guaranteed monies of approximately A$167.7 million occurred on 27 June 2011, so as at the date of the Offer Document the six month period commencing on the ‘relation back day’ under Australian insolvency law has not yet expired.

If the formal releases were not obtained before 27 December 2011, in the event of an insolvency of the relevant Fairfax Media group entity which repaid the guaranteed monies before that time, and if any liquidator claimed repayment of amounts claimed as unfair preferences, Trade Me could be required to make a payment under the guarantee which could have an adverse effect on the Group.

As at the date of this Offer Document, Trade Me is party to a number of guarantees in respect of the Fairfax Media group’s existing external financing arrangements totalling approximately A$2,309 million. It is intended that Trade Me will be released from these guarantees with effect from the moment of allotment of Shares to the Fairfax Media Subsidiary Shareholder under the Restructure. (For a description of the arrangements relating to the Restructure, see page 61.) For these releases to be effective:

at the date of the release, there must be no event of default or potential event of default under the applicable financing arrangement;

-

Fairfax Media group must be in compliance with certain requirements as to the composition of its guarantor group; and

-

each holder of the guarantee must receive notice of the release in the manner contemplated in the applicable financing arrangements.

Here you go, gummy.

In the notes (4) to the statement of the financial position of the company (pg 81) it says Long term interest bearing loans and borrowings relates to a cash advance revolving facility that is assumed to be drawn to $166.0 million immediately following the offer and which will be used to part fund the acquisition of the company by Trade Me. The $166m will be drawn down immediately.

And on pg 86

Borrowings

The company will obtain debt financing by way of a revolving cash advance loan facility, which will be used to fund part of the acquisition price of Trade Me. The facility is assumed to be drawn to $166.0 million immediately following the Offer and no principal repayments have been assumed in the forecast period.

Aren’t you pleased you’re not buying any shares in the offer? I am.

Thankyou DB & Effendi : I am suitably informed . ..... . reading between the lines , Fairfax has loaded a debt onto Trademe's balance sheet , before the IPO ..... so this is Fairfax lining it's own pocket .....

.... not a cent of this debt , nor any of the IPO proceeds are going towards expansion of Trademe , or to improving the business of Trademe ....

( by all means , correct me if I'm wrong ) : Gummy .

$2.20 - not even I'm that negative about the stock!

If they had priced the IPO around $2.40, I might be more enthusiastic.

My guess is a small stag, investors will eventually lessen their holdings and the stock will trend down or meander along.

However, I conceded that if Trademe had some bad news, this stock could easily drop to $2.20.

Exactly, Effendi. If it misses an earnings forecast, watch it get badly punished!

They should float their own shares - on TradeMe.co.nz! How awesome would that be? They could probably branch out and compete with the NZX after a while....

The Fairfax family themselves are bailing out of the firm which they founded . John Fairfax has placed his 9 % stake in the company with institutions to sell on his behalf . He'd bought back into the company at $A 4.50 / share , some years ago . And hopes to achieve an 80 cent return per share .....

...... if Mr J. Fairfax ever lands on this side of the Tasman , and tries to set up & manage a Kiwisaver fund , flee ! ..... grab the kids , the dog , wheelbarrow ... grab the kit & ka-boodle and head for the hills !

[ Pre-GFC , Fairfax shares reached $A 7.20 on the ASX , they fell to 75 cents during the GFC ]

One of the reasons they have grown so fast in the last few years is they keep increasing fees eg for rentals the fee has gone from $19.95 initially to $99 to list a flat. They have done this with most categories- they get them going and people used to using them at a cheap price, then they ramp up the fees. I don't think there is much scope for increasing fees left so I would be surprised if they grow at their predicted rate. If the fees are higher I think they'll lose customers.

Woodward Research - http://www.woodwardresearch.co.nz/ - have just released an equity research report on Trade Me. The report is available for free on the site.

Full disclosure - I am part of Woodward Research.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.