By Alex Tarrant

Economists say New Zealand is still vulnerable to the "whims of its creditors" after figures released today showed its current account deficit was heading back to the "danger zone" where credit ratings agencies would start to worry about the state of the country's external accounts.

Figures released today by Statistics New Zealand showed the annual current account deficit was NZ$9.7 billion in the year to March 2012, equivalent to 4.8% of Gross Domestic Product. This was the largest deficit as a proportion of GDP since the year to June 2009.

Economist polls conducted by Reuters, Bloomberg and Dow Jones all showed an expected deficit of 4.6% of GDP for the year. Treasury had expected a deficit of 4.2% of GDP in its May Budget, while the Reserve Bank’s more recent June Monetary Policy Statement forecast a deficit of 4.7% of GDP.

The annual gap - recording New Zealand’s transactions with the rest of the world - was up from a revised deficit of 3.7% of GDP (initially 3.6%) in the year to March 2011, and a deficit of 4.3% of GDP in the year to December 2011.

The New Zealand dollar had fallen about 20 basis points against the US dollar on the news, which was released at 10:45am, by 3:20 pm on Wednesday to 79.5 US cents. The dollar opened the day around 79.8 US cents, and began falling at 10am.

Danger zone, whims of creditors, ratings agencies to start worrying

ANZ chief economist Cameron Bagrie said the fact the current account balance deteriorated more than expected and was rapidly approaching 5 percent of GDP - "a level often seen as a tipping point" - meant the trajectory of the current account deficit would become more of a focus.

"Despite favourable revaluations, our external debt levels remain high and the current account deficit is moving back towards the 5 percent plus danger zone," Bagrie said.

"While the June MPS and the Budget 2012 forecasts have the current account deficit heading north of 6 percent of GDP by 2014 we continue to expect future deficits to be capped at around 5 percent of GDP, given private and public sector deleveraging. This depends crucially on borrowers continuing to show restraint and deleverage, consumer spending making way to facilitate the Canterbury rebuild, and export commodity prices starting to find a floor," he said.

BNZ's Head of Research Stephen Toplis said the deficit readings were going from "bad to worse," and begged the question as to just how much pressure the external accounts might put on the currency.

"Our medium term view for the NZD is that it will drift lower. Our current account expectations suggest that the risk to this forecast might be significantly to the downside, especially if our current account deterioration coincides with the expected recovery in the US economy," Toplis said.

"As things stand, the annual current account balance has already climbed from a trough of 1.9% of GDP back in March 2010 to its current reading. Our forecasts see the deficit climbing to 7.0% of GDP by year’s end and then further still to a peak at 8.3% of GDP by end 2013," he said.

"Not only is this a direct threat to the NZD but it is also a very clear risk for NZ’s credit rating with Standard & Poor’s, in particular, having recently placed great emphasis on the current account’s progress."

ASB chief economist Nick Tuffley said the recent relatively sharp decline in key export commodity prices would constrain overall export incomes, at a time when domestic demand growth (including earthquake reconstruction) would be lifting imports and profits of foreign-owned companies.

"Consequently, we expect the current account deficit to widen appreciably more than looked the case late last year (when commodity prices were firmer), with the deficit now forecast to peak above 6.5% of GDP around mid-2013. Further out, recovery in commodity prices will help constrain the deficit, and there are tentative signs that the prices are stabilising," Tuffley said.

"NZ’s net foreign liability position will continue to increase over the next few years (and it has been artificially lowered in the short term by earthquake insurance obligations of foreign insurers that have yet to be paid). Consequently, NZ is still vulnerable to the whims of its creditors," he said.

"Encouragingly, signs of gradual rebalancing continue. Private sector reliance on foreign savings is reducing, and eventual stabilisation of the Government’s debt levels will further contribute in time."

Aussie bank profits

“The year-end deficit increase to NZ$9.7 billion was mainly due to higher profits earned by foreign-owned banks and increased imports of petroleum and petroleum products,” Stats NZ said. See Gareth Vaughan's May 2012 article on record bank profits here.

“Services imports and transfer payments to overseas also increased over this time, due to the rising costs of reinsurance in the latest year,” it said.

Quarterly figures showed a current account deficit of NZ$2.8 billion in the March 2012 quarter. That was NZ$0.6 billion larger than in the December 2011 quarter.

“The quarterly deficit increase to NZ$2.8 billion was mainly caused by a turnaround in New Zealand’s international trade in goods and services, which was a deficit for the first time since the December 2008 quarter,” Stats NZ said.

“The value of dairy exports fell despite an increase in volumes, as dairy prices fell for the third quarter in a row,” balance of payments manager John Morris said.

Spending by visitors to New Zealand also fell in the March 2012 quarter, as visitor numbers dropped following the Rugby World Cup. Expenditure by British and other European travellers continued to fall, Stats NZ said.

Profits earned by foreign-owned companies in New Zealand fell in the March 2012 quarter, partly offsetting the falls in exports of goods and services.

“Despite the fall in profits, earnings reinvested in New Zealand by these companies increased NZ$0.4 billion this quarter. In contrast dividends paid to overseas investors by these companies fell NZ$0.8 billion, to their lowest level in over seven years,” Stats NZ said.

Despite the wider current account deficit in the March 2012 quarter, New Zealand’s net international liabilities actually fell to NZ$143.2 billion (70.9% of GDP) from NZ$146.3 billion (72.9% of GDP) at December 31, 2011.

“The fall in net international liabilities was due to changes in the value of New Zealand’s overseas assets and liabilities. Overseas investment transactions had little impact,” Stats NZ said.

“An appreciating exchange rate decreased the value of New Zealand’s overseas liabilities, and rising overseas share prices increased the value of New Zealand’s overseas assets during the quarter,” it said.

Reinsurance claims up

Meanwhile, Stats NZ said total reinsurance claims from all Canterbury earthquakes were now estimated at NZ$15.7 billion, up by NZ$0.4 billion from previously published estimates.

“At March 31, 2012, a total of NZ$3.8 billion of these claims had been settled with overseas reinsurers, leaving NZ$11.9 billion of claims outstanding,” Stats NZ said.

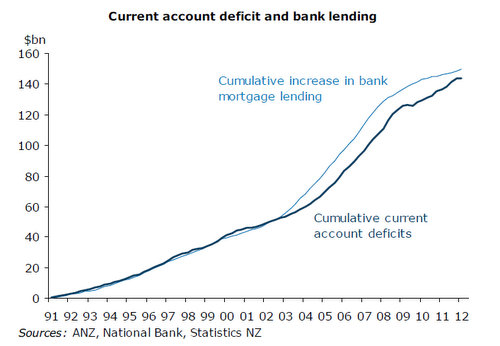

Chart of the day

ANZ's Bagrie included this chart in his current account commentary:

Economist Reaction

ASB chief economist Nick Tuffley

Summary

The quarterly current account deficit, at $1.31bn, was close to expectations (market $1.145bn, ASB $1.43bn). In seasonally-adjusted terms the deficit widened slightly, and that trend was also reflected in the lift in the annual deficit to 4.8% of GDP.

The International Investment Position narrowed to 70.9% of GDP due to asset revaluation impacts.

Trade as expected

The goods and services trade balances were close to our expectations. Dairy prices have fallen substantially since late last year and contributed to slightly weaker export receipts compared to a year earlier, compounded by weaker oil export volumes. Meanwhile the cost of imports was lifted by the spike in oil prices earlier this year.

The Services balanced weakened in the wake of the Rugby World Cup, reflecting the drop back to more normal seasonal tourist earnings and a lift in New Zealanders’ travel abroad after they remained homebound during the RWC. The lift in imports of services was mitigated by the absence of various RWC-related hosting fees and broadcasting rights paid in 2011.

Investment Income, Transfers

The investment income deficit was substantially smaller than we expected, though is a notoriously volatile component. A $470mn dip in the outflow of income attributable to foreign investors, relative to Q4, was the main cause of the lower income deficit. The decline in income was concentrated in direct investments in NZ (i.e. where a controlling interest is held). In contrast to the fall in income, direct investors increased the amount of profit reinvested into the local companies. The income NZ earned from its foreign investments edged down fractionally.

The Transfers balance, in contrast, registered a larger than expected deficit through increased foreign aid payments and a smaller tax take from non-residents.

Earthquake insurance settlements

Statistics NZ gains estimates of outstanding foreign insurance claims and includes these as NZ’s foreign assets in the International Investment Position, given they are a claim that NZ households and companies have on foreigners. The current estimate is that $11.9bn of foreign insurance claims remain outstanding after payments to date of $3.8bn (total foreign claims estimated at $15.7bn, against damage estimates of $20-30bn). Payouts will likely take years, so will provide a degree of background demand for the NZ dollar. However, the implications for NZD flows are uncertain given that some of the outstanding claims could have already been converted to NZD or the NZD exposure hedged.

The increase in reinsurance premiums in the wake of the Canterbury earthquakes have meant a $390 million increase in service and transfer payments to overseas insurance companies for the year to March 2012, relative to the previous year.

International Investment Position

NZ’s net international liabilities fell to $143.2 billion in Q1, from $146.3 billion in the previous quarter. This decline was largely driven by valuation changes, reflecting the appreciation in the NZ dollar and rising share prices. Relative to GDP the IIP has reduced to 70.9% from 72.9% in 2011Q4. If the outstanding earthquake reinsurance claims were excluded the IIP would be 76.8% of GDP.

There was a net investment outflow of $0.2 billion in the March quarter, reflecting investment in both overseas assets and liabilities. StatsNZ attributes the discrepancy between a net investment outflow and a current account deficit in Q1 to the non-measurement of some transactions in the financial account, such as in financial derivatives.

Implications

The current account deficit has been gradually widening since early 2010 but we expect the pace to pick up over the next year. The relatively sharp decline in key export commodity prices will constrain overall export incomes, at a time when domestic demand growth (including earthquake reconstruction) will be lifting imports and profits of foreign-owned companies. Consequently, we expect the current account deficit to widen appreciably more than looked the case late last year (when commodity prices were firmer), with the deficit now forecast to peak above 6.5% of GDP around mid-2013. Further out, recovery in commodity prices will help constrain the deficit, and there are tentative signs that the prices are stabilising.

NZ’s net foreign liability position will continue to increase over the next few years (and it has been artificially lowered in the short term by earthquake insurance obligations of foreign insurers that have yet to be paid). Consequently, NZ is still vulnerable to the whims of its creditors. Encouragingly, signs of gradual rebalancing continue. Private sector reliance on foreign savings is reducing, and eventual stabilisation of the Government’s debt levels will further contribute in time.

ANZ's Cameron Bagrie:

IMPLICATIONS

Today’s current account deficit was worse than market expectations and the June MPS pick. There are limited immediate market implications from today’s release, However, the fact that the current account balance deteriorated more than expected and is rapidly approaching 5 percent of GDP (a level often seen as a tipping point), means that the trajectory of the current account deficit will become more of a focus. Over the past few years, a positive goods balance has tended to counteract the large invisibles deficit, but the camouflage appears to be wearing thin given the terms of trade are now past their peaks, the higher import intensity of (recovering) investment and there is limited margin to boost primary production in the short-term.

Despite favourable revaluations, our external debt levels remain high and the current account deficit is moving back towards the 5 percent plus danger zone. While the June MPS and the Budget 2012 forecasts have the current account deficit heading north of 6 percent of GDP by 2014 we continue to expect future deficits to be capped at around 5 percent of GDP, given private and public sector deleveraging. This depends crucially on borrowers continuing to show restraint and deleverage, consumer spending making way to facilitate the Canterbury rebuild, and export commodity prices starting to find a floor.

Strengthening property market activity will provide a test to this first assumption, and credit growth figures will provide early warning signs. While some slippage in export prices is likely, the last two GlobalDairyTrade auctions have been encouraging, and suggest demand may provide more of a floor to export prices and a ceiling in the current account deficit. This will help, but improving export sector performance will depend on trading partner demand holding up, and the lower NZD acting as a safety valve. Historically low interest rates are likely to help mitigate our debt servicing burden and help at the margin.

Tomorrow’s Q1 GDP is the last major local data print for the March 2012 quarter. Today’s numbers suggest a slightly more negative net trade position than underlying our Q1 +0.5 percent GDP pick. However, what matters for the degree of capacity pressures and medium term inflation is the level of GDP. Today’s data suggest a higher level of nominal GDP than what we had expected. If this translates into a higher level of real production-based GDP it suggests a less benign capacity starting point than earlier assumed by the RBNZ.

BNZ's Stephen Toplis:

The New Zealand dollar lost ground immediately following the release of today’s current account data which showed the country’s annual deficit with the rest of the world climbing to 4.8% of GDP from 4.2% a quarter earlier.

It was a tad higher than market expectations of a 4.6% reading. This begs the question as to just how much pressure the external accounts might impart on the currency going forward as these deficit readings are almost definitely going to go from bad to worse.

Our medium term view for the NZD is that it will drift lower. Our current account expectations suggest that the risk to this forecast might be significantly to the downside, especially if our current account deterioration coincides with the expected recovery in the US economy.

As things stand, the annual current account balance has already climbed from a trough of 1.9% of GDP back in March 2010 to its current reading. Our forecasts see the deficit climbing to 7.0% of GDP by year’s end and then further still to a peak at 8.3% of GDP by end 2013. Not only is this a direct threat to the NZD but it is also a very clear risk for NZ’s credit rating with Standard & Poor’s, in particular, having recently placed great emphasis on the current account’s progress.

The most significant driver of future current account deterioration will come through the Goods and Services balance. A balance that is already under some pressure.

Alas, the growth that we are forecasting for the New Zealand economy will largely be domestic demand driven. In the first instance this should be due to a rapid increase in residential construction activity. But this is also likely to be accompanied by an increase in consumer spending, assisted by recent past increases in the household savings ratio and low interest rates. An increase in domestic demand is invariably accompanied by increasing imports.

The eventual payment by insurance companies to New Zealand policy holders will promote this domestic spending. Statistics New Zealand estimates that as at the end of March offshore reinsurers had only paid out $3.8 billion of claims and still had $11.9 billion to go.

When this money hits New Zealand not only will it boost domestic spending but it will widen the economy’s already parlous net international investment position as the unpaid claims currently count as an asset on New Zealand’s balance sheet.

Simultaneous with the pick up in imports, export receipts, which already appear to have peaked, will be adversely affected by relatively weak global demand and, in time, the impact of the recent and expected drop in commodity prices. As if this isn’t problematic enough, primary sector export volume growth will be compromised because of the high base we are starting from thanks to the spectacular growing conditions that we have experienced over the last twelve months.

Currently, we have a goods surplus of 1.4% of GDP. That surplus is likely to be gone by year’s end and for a deficit to grow to around 2.5% of GDP by late 2014.

At the same time the country’s travel balance seems to be under some pressure with visitor spending struggling to strengthen while, concurrently, New Zealanders remain encouraged to spend offshore thanks to the favourable exchange rate.

It is notable that the travel surplus in the year to March 2012 was just $2.4 billion. This was the lowest annual travel surplus, in dollar terms, since September 2001 – despite the fact that these data include the spending of overseas visitors during the Rugby World Cup.

We think there is a very real risk that the current account deficit grows to a level greater than we are forecasting. In part this is because we have taken a very conservative view on the investment income balance which we have flat-lining at current levels. The risk is that that the conditions which create the deterioration in the trade balance also result in a modest deterioration in the net investment balance.

As is oft the case, one of the ironies of the way the current account works is that an outperformance of the domestic economy can cause deterioration in the investment balance. Symptomatic of this is the fact that any improvement in the stability, and hence profitability, of the New Zealand banking sector will have a negative impact on this balance. Realistically, this should be seen as a positive for the economy but this positive is, implicitly, turned into a negative by the way these data are constructed.

More immediately, today’s data suggest a slightly worse net export contribution to Q1 GDP growth than we had anticipated. Indeed, when we poke this data into our GDP estimates it delivers us an expenditure based measure of activity growth of just 0.3% for the quarter. Our published estimate of GDP (as measured on a production basis) is 0.6%. We’ll stick with this but, clearly, the current account figures suggest some downside risk to our pick. Q1 GDP is due for release tomorrow morning.

The Achilles heel of the New Zealand economy’s prospective growth story has almost always been the impact that growth might have on our already poor external accounts position. This remains the case. Accordingly, it also remains the case that policy makers, businesses and individuals alike need to do what they can to raise New Zealand’s saving ratio.

Householders have done their bit so far with the household savings ratio moving from markedly negative to an estimated mild positive. Further progress would be helpful but won’t occur if recent enthusiasm for the housing market gains too much more momentum.

Businesses seem to be obliging as well but if they are to oblige much more than is already the case this could act as a nasty constraint on investment activity, which is probably not in the best interests of the economy medium term.

What the data do say, with absolute certainty, is that the Government must remain hell-bent on achieving surpluses so that the rating agencies do not have the excuse of twin deficits to downgrade our sovereign debt.

And for the Reserve Bank, there is a clear message that it must not let domestic demand growth become overly excited through the availability of cheap credit.

Balance of payments ratios

Select chart tabs

26 Comments

I know what I would like to post as a comment on the bank economists who have so much to blurt out on the matter...but Bernard would boot me out and the cops would come a calling...far as I am concerned the bank spin agents should take a long hard look at the role their masters have played in stearing SS NZ into a morass of debt with one aim in mind...to fatten the bank bosses bonuses and bloat their salaries....it was and remains a case of "bugger NZ, let's extract as much as we can"

HERE'S AN IDEA , follow me on this one

As is common elsewhere , multinationals trading in NZ should have a joint lisitng on the NZX.

This way , some of the dividends would stay here .

It would also help if we have compulsory Super , as Kiwis would indirectly own these Bank shares thru their superannutaion fund . The dividends would stay here , effectively incresasing the pool of capital, increasing domestic money supply , and reducing strain / pressure on the Current Account

This concept of dual listings is common elsewhere , BHP is listed on the Sydney and Johannesburg Stock Exchanges because BHP trades in South Africa .

Why cant Aussie banks have dual listings on the NZX ?

Under the present system ,by listing only in Sydney , if we (Kiiwis) buy the shares the dividends are effectively double taxed as the are not treated as PIE INVESTMENTS.

Its a cock up that should have been addressed by the former Labour Govt when they introduced the PIE SYSTEM , and the current National Govt is frankly a disappointment in dealing with any legacy issues

Are you sure the profits are finding their way to the dividend pool or is it more likely the first cut of the action is the bonus pool? - these executives cost lots of dosh and they are just the lowly outpost bozos.

For the record, it doesn't matter that dividends 'go out' of New Zealand, ultimately, there is no outflow.

If you don't believe me, check out my blog post here and take the challenge. Show me how I'm wrong in the example I give on that post.

Tribeless , you are fundamentally right , the dividend flow and conversion to Pesos in your example makes it a zero sum game , almost .

In practice, however , when dividend flows start to impact detremantally on our Current account deficit , it has consequences for our capacity to borrow and the costs of borrowing .

If the Government's borrowing costs go up , they will need to tax us more to service debt , or if they dont service the debt , they risk default .

I am also neutral about sales of state assets , the Government has no business running businesses ,its there to govern.

I agree with your assertion that the costs of electricity are a form of tax and when the cost for households goes up in winter it is opportunisitc pricing , and is like a tax surcharge.

The sooner the energy Companies have to compete properly for customers the better.

Right now the created perception of energy Companies competing for customers is just an illusion

Boatman,

Financial issues aside, gow convinced are you that new "competition" is going to lower prices for customers? Certainly, the research from overseas is very mixed on the price effects of privavtisation of energy companies. I think NZ is too small to have a seriously competitive private energy market, given the investment required.

..... wouldn't it be simpler to just hock off the NZX to the Australians , then it would be run properly ( check out the ASX website & regulations , compared to the NZX ! ) .......

And whilst we're at it , apply imputed dividends on all ASX listed companies , to encourage Kiwi savers to haul some Aussie profits across the ditch , back into New Zealand .......

Good idea - but would they haul their profits back here? Gotta have some income to spend on that side of the Tasman while basking in the sunshine.

Some observations:

1) our CA deficit is primarily a function of borrowing more than we lend, hence overseas profits to banks. This is mostly housing related due to bubble.

2) if interest rates are higher, so are our payments oseas, and irgo CA deficit - big dangers here.

3) if we force house prices lower via tax changes then we stop adding to our CA deficit AND pass benefits to those who generate income v speculation

4) it is a lot easier to reduce our deficit via 3) than it is to generate additional exports / earnings etc to fund deficit. We should try to increase exports, but this takes effort and smarts. Lets focus on what is easy first (eg if you have a leaking petrol tank, fix the leak. Dont get an extra job to pay for the leaking gas!!)

5) are John and Bill aware of this? Bills a good guy, but JK is a banker and serves banks (contrary to some I think he lacks charisma and is a bad speaker as well, the Letterman thing was a cringe)

It will get even worse when this numby government sell off the state owned assets.

Have updated with economist comments and now got Top Gun's Danger Zone in there too.

Cheers

Alex

Answer is to impose a Foreign Transactions Surcharge on all imports and use that revenue to pay down overseas debt. Make it fiscally neutral by lowering GST at the same time. It's allowable under GATT and even the new TPPA regs, in terms of dealing with current account issues.Start with a 10% charge.....that should get things moving in the right direction.

It's a very simple equation.

Mind you, as JK reminded as, we could always sell the whole country!! What do I hear for NZ..$170bln cover it?

Clearly all of those Free Trade Agreements are not working in our best interests.

What we need is a Free Trade Agreement with ourselves.

Like we did after the 1958 BLACK BUDGET - and the 1968 MULDOON FIASCO #1 and the 1976 Muldoon Fiasco #2.

Muldoon called it Import Substitution. Good name. We should use it.

We made most of what we needed. The quaint workplaces were called factories! Employment improved and the factory workers pay packets did the rounds - enhancing everybody.

All of you guys above can debate financial resolutions till the cows-come-home. But in the end I will be correct. Import Substitution is coming to a place near you soon.

What we need most are lots more customers with cash. And the factory workers will have plenty of that.

Thank goodness for the US FED! They will save us! borrow, borrow, more interest, borrow, borrow, more interest..........la le la le laaaaa life is good

Here's a footnote for Bernard (who loves talk of an Epsom property boom!), a typical bungalow on an 873m2 site in Selwyn Rd (1 owner for 30 years) sold for $1.561m today (a third above 2011 GV). It was a potential 2 unit site (if the house was demolished or relocated forward) and in the double grammar zone, but it was a fairly standard house on a reasonably busy street.

A townhouse in Bernard's street fetched over $2.3m at the same auction.

More evidence of National's poor performance.

National are attempting to open up mining and oil exporation. This would greatly help with CA and reduce our reliance on agriculture and forestry for export returns. If you ask me National are trying to help but aome of us dont seem to want to give them a chance. Selling of SOE's will provide a short term boost to CA (sale of shares less profit distribution plus development expenditure = net gain in the medium term to CA)

Matt in Auck - just tell us how you would have handled the GFC, the earthquakes and all the other issues that have blown up in our economy??

Mist42nz - well we already have "epic saga of inefficiencies" and it's across the country. Isn't that what the problem is?

One of the biggest problems in Chch has been that the bureaucrats have all been like stunned mullets floating on the water. The Organisation of Disorganisation is still floundering in the water after all this time they haven't learnt to swim. All the quaifications but not an once of common sense. Grrrrrrr - I'm not going to get started.

Will be looking out for this female candidate!!!!

Philthy selling state assets will improve the CA deficit. At the moment kiwis have a shitload f cash sitting on bank balance sheets. Transferring this into SOE removes future growth opportunities for the banks and hence constrains lending and therefore distributions moving offshore Furthermore banks will have to compete more aggressively for deposit funds to meet the new RBNZ core funding requirements. interest margins will likely narrow. What I would like to see is kiwibank growing by receiving superannuation funds, Kiwisaver funding etc. And nationalized. We should never ever have the scenario where we lose control of our banks to our Aussie neighbors. Whoever allowed this to happen was a mug

1) NZ currrent account effectively caused by two issues, a) borrowing too much to fund increasing land prices, b) too higher outflow of profits from NZ companies (eg the aussie banks)

2) What can we do about it:

2a) Increase savings

2ai) - Increase kiwisaver contributions rate to increase the savings pool. The savings will buy overseas assets and return dividends or buy foreign NZ assets & reduce the dividend outflow. The increase in compulsory savings rate would have to be carefully balanced so as not to throw the economy into recession, i.e. -ve gdp growth

2aii) Get some of the smaller NZ banks/building societies to amalgamate and take on the Aussie banks which are making monopoly profits

2b) Decrease borrowing through:

2bi) Allowing the Reserve Bank to mange the 12 month rolling migration rate. The NZ market is so small it cannot handle high inward migration rates. There have several graphs printed by the Reserve Bank showing the correlation

2bii) Allowing the Reserve Bank to control the maximum Loan/Value Ratio on mortgages. This would need to be carefully implemented to avoid destroying housing values and pushing everyone into negative equity. A long flat period of housing prices would be better.

2biii) Stop stupidly bidding up the price of land. Hugh has it right. Require land developers in the main cities to bid to develop greenfield land or increased density & mitigate all below ground service capacity (water, sewer etc) issues. These would most likely be bids with requested subsidies like public transport but would drive more efficient development.

2biv) Requiring Regional Councils (preferably unitary authorities) to remove urban boundaries and accept sufficient bids to provide, say, a moving 10 year buffer of land capacity or within their infrastructure budget

2bv) Requiring Local Government to mitigate above ground transport issues of less constrained urban growth through the implemenation of road tolls

So how is this then, we all know that Greece is stuffed with Spain and Italy and others likely to follow suit in the next few years. England is on a knife edge short of selling the Queen's jewels to pay for a day's interest. The United States is stuffed as they have no way of getting their house back in order apart from printing more money. And then comes little old NZ. I say sell some of the assets to get our balance sheet back in order and reduce the current borrowings we are doing to service the interest on the debt that we can't afford. That's just plain business sense!

But it is only a short term fix! We then need to look at our mineral assets and get over ourselves about how they are mined. Yes we might be the clean and green country of the world who prides itself on keeping the Greenies happy, but it doesn't count for jack if we are going down the toilet with the rest of the world. Or here is an idea, can we design a hose to fit on a sheeps butt to collect all that natural gas to sell instead?

Right, time to get back in my Remuera tractor and head off to the airport to get in my private plane and head back to the Gold Coast where life is so much better. Gee, that's a thought did I stick some Tuis in the esky before I left?

etekup, You are keen to sell assets to "fix the balance sheet". Assuming you have in mind assets like power companies, you presumably share Key and English's view of accounting and economics.

On first principles, selling these assets worsens the balance sheet immediately. We will have lost assets giving a return of 15% apparently; and certainly significantly more than the cost of capital of 3.6%.

I understand Goldman Sachs and other advisers will be salivating over the $100 million in fees they will get for the transaction, so no doubt are also advising why selling these irreplaceable strategic assets is a good idea. But fix the balance sheet it does not do.

The only plausible solution to the current account is through a lower dollar. Selling these assets merely increases the dollar, so we also blow the money immediately. But managing a lower dollar would involve some slightly tough decisions, so Key and English pretend they cannot do it.

The dollar is not going to magically drop overnight without active management; too many foreigners like the idea of owning a piece of New Zealand for that to happen, and until there's nothing left to sell or mortgage ( a situation we are close to) the dollar will not drop.

A clue is in the BNZ economist commentary on the travel balance. We are borrowing from our children's generation to take winter breaks in Hawaii, Vietnam, Europe (to use the examples of nearly all my friends), and many other places. The price signals are all wrong. The lose lose is that by doing so, we are also cutting employment at home in say the travel and holiday market.

Maybe the Government should start buying Lotto tickets then?

To fix the balance sheet we need to reduce our debt levels (both central and private). To do that selling assets is one way and probably the easiest. The other is to either increase income (taxes) or reduce expenditure. So tell me then who wants to pay more in tax or have less education, health, roading, etc, etc...

Or is there another magic fix that you can think of?

My understanding of general accounting principles is that If you have say investment properties worth $1 million, and returning $150k a year, but with debt of $500k, on which the interest cost is $35k; and you sell half the assets for $500k to pay off the debt, your balance sheet situation is as follows:

Before: Net assets $500k; net earnings $115k.

After sale: Net Assets still $500k Net earnings $75k.

So your balance sheet is effectively the same; but your earnings have declined. Any financial analyst I believe would say that your situation has deteriorated.

If the cost of capital is higher than the return on the assets, then a sale may make sense. My understanding of the power companies is that is nowhere near the case.

In my opinion we need to fix the underlying problem with New Zealand's accounts; and that is the current account. That doesn't need less health or education (because they are primarily sourced in New Zealand); but may mean less overseas holidays.

It is interesting that the deteriation in our current account deficit began with the sale of our state owned assets to offshore interests. See the chart above.

It seems that offshore interests borrow money offshore to buy NZ assets and then pay interest offshore for the borrowings and also export their profits earned from the NZ assets offshore. The claim they would invest profits in NZ to grow the NZ economy has not happened.

Hnch the spiralling increase in the deficit.

The Aussie banks are a prime example - borrow offshore, lend high in NZ and then send the profit somewhere offshore safe from taxation.

As the deficit expands the New Zealand borrower has to pay ever higher interest rate so the banks can borrow from offshore at the higher rates their profit stripping is causing and on it goes.

Having read that it the Aussie banks profits that is driving so much of the deficit I'm going to get off my backside and change to an NZ owned bank.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.