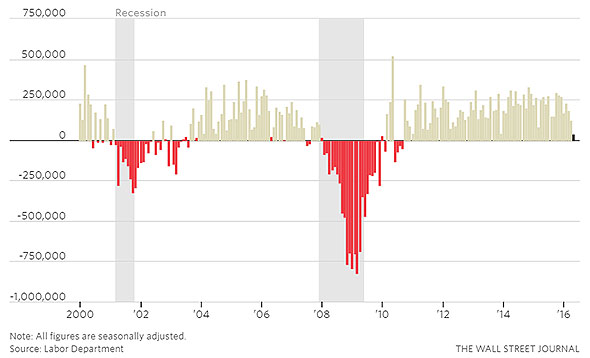

American hiring hit the skids in May.

At least, that is what their non-farm payrolls survey shows.

Other surveys (the ADP Employment Report for instance) did not signal this outcome.

Markets were expecting employment growth of +160,000. They got +38,000.

But the equities markets didn't bat an eye. The S&P barely changed it's track on the news.

But the bond markets did notice. UST 10yr yields dropped from 1.81% to 1.71% on the day.

And gold jumped US$35 to US$1,245/oz.

The US dollar fell, but actually only marginally. The NZ dollar rose as a consequence to 69.6 USc which is back to where it was in early May.

As surprising as the US jobs report is, it does have a history of throwing in a rogue result occasionally. The last one was in March 2015, and prior to that December 2013. Both were followed by 'normal service resuming'.

Today's result may signal a downward trend. Or it may not. Markets will only be convinced if it is followed up next month with a similar result. 'Rogue' results are never sustained two months in a row in this survey. If we do get two consecutive months of low jobs data, that will be significant and not 'rogue'.

Today's US survey shows:

- the unemployment rate falling to 4.7% in May from 4.9% in April

- their participation rate falling to 62.6% from 62.8%

- wages growth holding steady at +2.5% pa.

- the average hourly pay rate up to US$25.59/hr (NZ$36.80/hr)

- the average workweek unchanged at 34.4 hours

The question will be, will this result take a June Fed rate hike off the table? We only have to wait for less than two weeks to find out. The Fed reports next on Thursday, June 16.

21 Comments

So in other words the report proves nothing - it's just noise.

The collapse in UST bond yields is anything but noise for those in position.

Let's revisit the uber- bear site for those that remain unconvinced.

The payroll report missed badly, as the headline “job creation” number gained only 38k in May 2016. That was the lowest monthly gain of the entire “recovery.” Last month’s figure, which had already caused significant angst, was revised even lower to just 123k. The mainstream is predictably apoplectic, and why wouldn’t it be? After all, month after month after month there was only the Establishment Survey and unemployment rate to hold off the steady rise in uncertainty, the determined approach of negative signs in more and more places. If the Establishment Survey turns too, there is nothing left. Even “full employment” will be transformed from a serious signal of full economic health to nothing more than marking the cycle peak. Read more

China is relieved.

Having suffered through more than three weeks of almost sustained “dollar” pressure, the PBOC and Chinese monetary system can only say “thank you” for today’s funding gift. And it wasn’t just CNY, though that was the most pressing and visible, as currencies throughout the EM’s were similarly bestowed a traditional, policy-driven reprieve. Read more

Nonetheless, keep a serious eye on this currently rising commodity index.

It’s now been more than seven years since I first warned of a new “global government finance Bubble.” I had no idea that by 2016 the Fed’s balance sheet would have inflated to almost $4.5 TN. The thought that the BOJ and ECB would each be expanding their balance sheets by about $1.0 TN annually never came to mind. I did not at the time contemplate that the ETF and hedge fund industries would both balloon to $3.0 TN. I would have argued against the possibility for negative interest-rates and $10.0 TN of negative-yielding global debt securities. I expected a Bubble in China, but a $35 TN Chinese banking system and $8.0 TN of so-called “shadow banking” were inconceivable back in 2009. And clearly I expected this “Granddaddy of all Bubbles” to have succumbed before now.

http://creditbubblebulletin.blogspot.co.nz/2016/06/weekly-commentary-mo…

It's still just noise. The long term trend is what matters - the rest is just a roller-coaster ride - with everyone puking their guts out at every turn.

No wonder there is a repent the end is nigh fetish......

I take the money chunks one step at a time and review success with content at a latter stage.

And that is the problem - you are being dragged about by each piece of financial information which is just increasing volatility without knowing it's true relevance.

Made a career out of it.

So you pray on people's fear , uncertainty and doubt.

Not really, just their lumps of industrial sized funding which was secured by sovereign collateral via repurchase agreements.

If you want to talk long term trends then treasuries are in a long term trend of remaining unconvinced about sustained US growth. If the job market truly had the potential to ramp up inflation 10 year treasuries would be well north of 2%, if not 3%. Ben Bernanke believes he won't see a 4% 10yr again in his lifetime. So far so good on that one.

For sure.

Having struck out with negative "real" interest rates, negative nominal rates are proposed and already enacted across large sections of the global financial system (including yields on "risk free" securities). At some unknown and really unknowable point, people and really more so banks will interview and become more open to alternatives which escape this authoritative repression.

This is wholly different than the "hoarding" vilified of the 1930's in both cash and gold. It represents the contradictory tensions that serve to illuminate the inconsistency of the dominant economic and monetary theory. To save the global economy, and the US with it, the central bank "must" tax short-term "money" rates so that banks will instead lend rather than hold to their own liquidity preferences (to reuse a Keynesian term more at home wholesale interbank than in the economy), and if they don't they will pass along those negative nominals to deposit holders so that they will spend rather than save.

It's reprehensible on so many levels, including the assignment from above about when and how people are supposed to engage in commerce. And if one might be so inclined as to exercise free authority to deny the command, then they are instead to be denied increasingly the means by which to escape the authority; the monetary noose can only tighten.

As I described last week, the only reason to hold a negative "yielding" money market balance, whether in the private money markets or on account at some central bank, is to remain in good standing of the virtual wholesale system. In other words, you accept -30 bps for now because at some point you expect to put that liability "to work" in some positive yielding opportunity in the near future. If you instead convert to cash, you will have both additional costs in doing so but then face the prospects of having to again convert back to virtual cash in money market accounts in order to carry out participation in any future opportunity; physical cash is illiquid. It might be too much hassle at -30 bps, but perhaps not at -50 bps? -100 bps?

That is the current danger facing global NIRP; there exists already quite negative nominal rates around the world and now the dimming prospects for those future opportunities. At some point, and it is impossible to determine the level that might trigger it all, banks will make the same determination that people were once free to make in the 1930's; getting the hell out because they can and because there is only increasingly more cost and risk and no upside to remaining under such repressive conditions. Read more

Unfortunately opinions are like arse-holes everyone has one. While it's fine to use obscure websites that may or may not be reputable - there are no hard facts - it's just opinion.

I think Stephen makes a rather nice living from his opinions.

The ADP report is compiled from actual payroll data and is therefore very accurate and timely - No Novapay's

in the US.

That's why no-one's worried as it shows a steady +173,000 net new jobs.

The US is very fortunate in having this very large payroll bureau that pays millions of US workers and so provides extremely accurate and up to date data on time every time.

Forget the stats - ADP is the bible for employment in the US. Pity we don't have an equivalent operation here.

One thing I will say is that the US has much better and timely economic information compared to New Zealand.

Surveys are expensive. StatsNZ wants to do CPI and unemployment monthly, but is only funded to do them quarterly.

But ANZ stepped into the space and does a monthly CPI. Non-one has the money to do the employment one monthly. Proper surveys are large and expensive things. However, perhaps other ways (using 'big data') will open up soon.

Why go slow when you can go fast?

Monthly IRD PAYE schedules and receipts are a proxy for payrolls, employment and GDP

Data is collected and held - just not published - or used - or made available

Simply press the button

Usa surveys are really only estimates. These estimates are usually revised each month for the following 2mths. So in actual effect you have to wait 8more weeks for the true may data. Stats nz doesnt do estimates. Hence if u want reliable data on usa, wait 8 weeks longer

i love it when someone starts there rebuttal with...So...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.