Content sourced from Treasury's Special Topic in its Monthly Economic Review for February 2017

Core Crown tax revenue is currently around $70 billion a year and is forecast to increase to $90 billion by 2020/21. Tax revenue is by far the largest share of core Crown revenue ($76 billion in 2015/16) and is necessary to fund core Crown expenses ($74 billion in 2015/16).

The Financial Statements of Government (FSG) for the six months to December 2016 were released on 16 February. The FSG showed that core Crown tax revenue had increased by 9.2% on the corresponding period of 2015. This was a sharp increase on the 5.7% reported in the 12 months to June 2016.

This special topic explores the reasons behind this comparatively strong growth rate, whether or not it was expected and the likelihood of it continuing.

What’s behind the tax revenue growth?

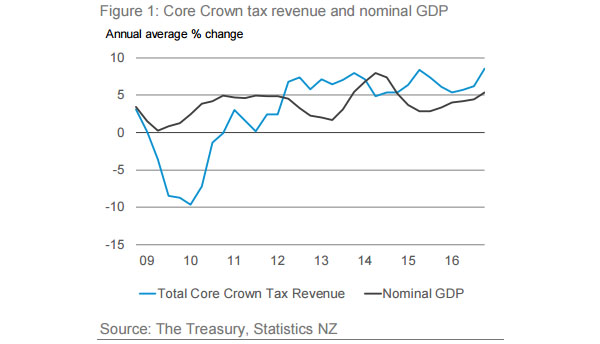

Core Crown tax revenue grew by 8.5% in the 12 months to December 2016. This was above the growth rate of nominal GDP (estimated at around 5%) and has been for the past two years.

The main components of the tax revenue growth were:

► GST, which was up $1.7 billion, or 9.8%, on the previous year

► Source deductions, up $1.8 billion (7.1%), and

► Corporate tax1, up $1.8 billion (16.8%).

GST

GST was $173 million above forecast for the six months to December and was the main factor in total core Crown tax revenue being $313 million above forecast. Growth in GST accelerated through the second half of 2016, supported by growth in:

► nominal private consumption, estimated at +4.8% in the year to Dec 2016

► nominal services exports (spending in New Zealand by international visitors attracts GST), which was up by just over 6%, and

► nominal residential investment, which is estimated to have grown by nearly 20% through 2016.

Services exports captures spending by international visitors in New Zealand, which has been boosted by record numbers of tourists coming into the country. Residential investment is experiencing strong growth owing to the high demand for new houses around the country. Although private consumption accounts for most of core Crown GST revenue, the rapid growth of these other components recently has made a noticeable positive contribution to GST’s growth rate.

Source deductions

Source deductions are the total of:

► Pay-as-you-earn (PAYE) tax, deducted from wage, salary and social-assistance benefit income, and

► Employer Superannuation Contribution Tax (ESCT), deducted from employer contributions to registered superannuation schemes including Kiwisaver.

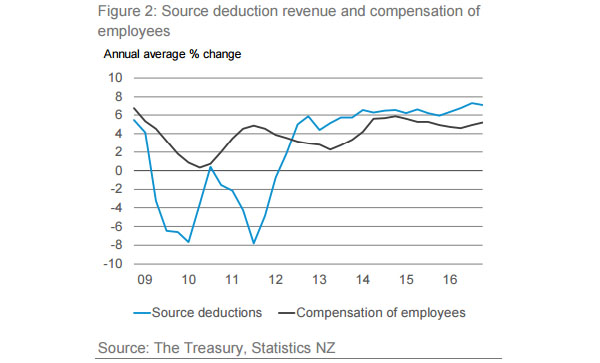

Growth in source deductions has been running ahead of growth in its principal economic driver, compensation of employees (COE), for the past four years as shown in Figure 2.

A gap opened up between the two growth rates through 2012 and 2013, as the ESCT base was broadened to include employer contributions to Kiwisaver. The gap closed somewhat in 2014, one year after the Kiwisaver change, with the remaining gap through 2014 and 2015 being mainly due to fiscal drag, ie, the effect whereby, owing to the progressive nature of the personal income tax scale, average PAYE rates increase as incomes increase.

The widening of the gap through 2016 is a little more puzzling, as it cannot be completely explained by nonCOE factors such as fiscal drag and PAYE on benefits.

The gap may become smaller should past growth rates of COE be revised upward in the future. Total growth in source deductions was close to expectations, with source deductions for the six months to December 2016 just 0.1% above forecast.

Corporate tax

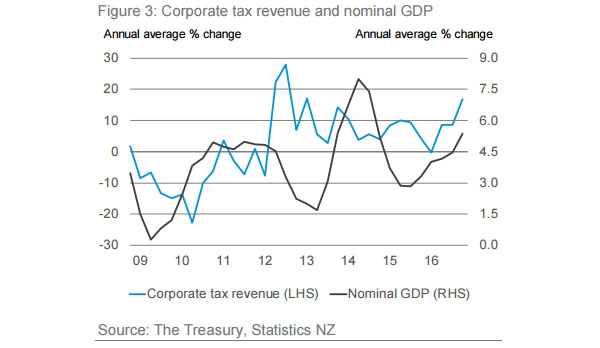

The annual growth rate of corporate tax increased noticeably in the December quarter as shown in Figure 3.

Part of the reason for this is that, in the calculation of the annual growth rate, the comparatively weak December 2015 quarter’s corporate tax outturn has moved from the numerator to the denominator. The weak December 2015 quarter was part of a longrunning trend which has seen the filing of annual income tax assessments, which form the basis of the revenue calculation, move to later in the tax year as tax pooling has grown in popularity. On top of this, there was noticeably strong growth in provisional tax through the second half of 2016.

Similar to source deductions, corporate tax was in line with expectations, just 0.8% above forecast.

Future implications

Based on the GDP outturn for the September 2016 quarter and indicators for the December quarter, growth in economic activity over the latter half of 2016 was stronger than was forecast in both the 2016 Budget and the 2016 Half-year Update. This has been reflected in tax revenue outturns, with all tax types at least slightly above forecast for the six months to December.

However, the degree to which these above-forecast trends continue through coming months is uncertain. For instance, residential investment and the number of inbound tourists are not expected to continue to grow at the comparatively high rates of recent times. This means that the current growth rate of GST is unlikely to be sustained. Furthermore, monthly tax data can be volatile so, even during periods of stronger- or weaker-than-forecast economic growth, there may be individual instances of monthly tax outturns being lower or higher than forecast.

The FSG for January 2017 will be released on Tuesday 7 March. Revised economic and tax forecasts will be published in the 2017 Budget Economic and Fiscal Update on 25 May.

The full Monthly Economic Indicator report is here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.