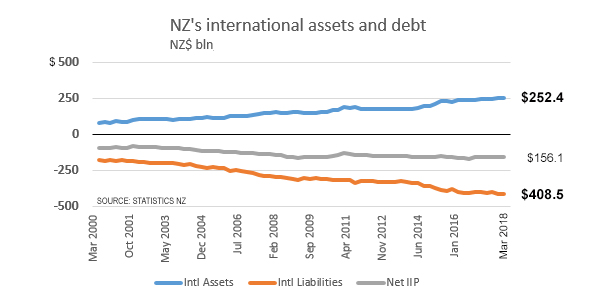

Our overseas debt has now reached $408.5 billion.

On a per capital basis, that is $83,900 for each person in New Zealand.

That debt is made up of both private sector debt, plus Government debt. In addition we have other international liabilities (like carbon credits) and they are included in this total as well.

But the real question is, is that debt growing? And how fast?

And as a proportion of our growing economy, is that getting larger? Are we more indebted on a real basis?

The answer to those questions are less alarming.

Firstly, the data for this is found in our National Accounts, as published by Statistics NZ quarterly. That release tends to be used to record economic growth, but it includes far more comprehensive data than that. It is a full national balance sheet setting out all our assets and liabilities. From the detail around liabilities, you can find the "international position" on liabilities, which is commonly referred to as 'overseas debt'.

A first principle to recognise is that we have long gone past the period where we had to borrow-to-pay-the-groceries. Now debt is incurred almost solely to invest in assets. And every lender requires the borrower to have skin in the game, a level of equity to support the borrowing. So asset levels are a core benchmark. Borrowing by either Government or corporates (including banks) isn't for straight consumption; no lender would agree to such an arrangement anymore. They want to know that the asset being funded has a future income stream that will comfortably allow for repayment.

So the GDP benchmark is the appropriate one when looking at this issue on a national basis.

Focusing solely on the international position, here is the track of borrowing we are on:

On a net basis - our Net International Investment Position, Net IIP - we have a liability now of $156.1 bln to the rest of the world. This net position has been pretty stable over the past 10 years. It grew from $92 bln to $155 bln in the nine year period to the end of 2008, and has staying at that absolute level since.

But over those two blocks of time, nominal GDP grew +65% and +51% respectively (the second block includes the GFC recession).

The lid on net debt is held on by strong growth in our overseas assets, almost all by the private sector.

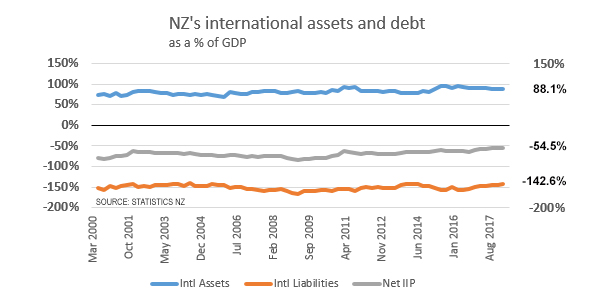

Putting this in the perspective of the underlying economy, here is the same data:

In this perspective, overseas liabilities are now at 143% of GDP and that is its second lowest since the data in this form became available (from 2000). And that is a recovery from its worst level in March 2009 when it was 166%.

On a per capita basis, the recovery is not as strong. It reached its peak at $88,016 in September 2016 and has fallen since then to the current level of $83,862. At the same time, our international assets on a per capita basis were at their peak at December 2017 at $52,017.

Community anxiety about our overseas debt levels has faded over the generations. Prior to 1984 when New Zealand was a closed and centrally controlled economy, anxiety levels were generally high and everyone worried about our overseas debt. Governments set public policy to try and reduce the stress. But since the opening up of our economy, while the debt levels have risen in absolute terms, the shock-absorbing mechanisms of the exchange rate, and the market-driven signals about what debt is sustainable, have both worked to push the issue back down to its rightful place in our economic perspectives and conversations.

98 Comments

David... Some of this does not look right..??

The graph you have labeled " NZ int. assets vs debt" is NOT a debt thing.

The $408 billion is the amount of NZ assets owned by foreigners vs the $252 billion of assets owned by NZers offshores.

$156 billion is the net international investment position.

I dont have the data, .. but the amount of external DEBT NZ owes is alot less than $408 billion..??

I'm thinking total credit in NZ is around $438 billion... so external debt must be alot less than that..??

Agree it is strictly "not a debt thing" rather a liability thing. $408 bln is the sum of all liabilities owed to parties outside New Zealand. That includes debt. This is the basis.

Because it is comprehensive, I think it is a better indicator of what we owe as a country, the full accounting of New Zealand as a debtor country.

Ok.. A full accounting of NZ as a debtor Country and also of a Country that is slowly selling off the "silverware" , to makes ends meet...

An analogy might be a Farmer selling off bits off the farm as well as continually borrowing more, to maintain the lifestyle.. but blissful because his gross income ( GDP) is going up ( he sells things to fellow farmers ), as well as the value of his remaining farm appears to keep going up ( Farmers sell land to each other at higher prices which makes them feel wealthy, and secure )..

At first glance everything appears rosy.... but the reality is one of a chronic debtor Nation..

https://www.stats.govt.nz/assets/Uploads/Balance-of-payments/Balance-of…

In my view, the best way to look at our external debt position is thru the current acct.

Our current acct deficit is $7.1 billion.

This is how much money we have to borrow and send offshore every year to pay for and maintain our current lifestyle.

I recall reading about a local body that decided to value and include the land beneath roads as an "asset" so they could borrow more...

I'm guessing that in our financialized world, the balance sheet expression of asset values are "gamed" ., and using an aggregate asset/debt metric can be more reassuring than it really is..???

Yes, current account deficit worries me a lot too. Every year we sell another ~7billion of NZ to foreign interests, who demand a return on it, - so another $300 million of additional outflows accruing every year as a result. We desperately need a plan to cut that, which means more exports or less imports.

But current govt (mostly driven by Green wing) seems unconcerned about killing off export industries (oil and gas, plans to hobble dairy, rumblings about film industry support....)

... but in relationship to the growth and size of our economy, most current account components as a ratio to GDP are getting smaller ...

GDP = C+I+G+(X-M)

Consumption (C) + Investment (I) + Govt spending (G ) and Net exports ( x-m).

I think one would really have to dig down to determine if NZ GDP growth is long term healthy growth ... or not.. ( I think I read somewhere , that Govt spending alone is 30%+ of gdp..?? )

There is a big difference between someone who borrows to spend or borrows to invest ...

I'm guessing.. that most of NZ borrowing is in the Household sector..

In contrast to that , in USA most credit growth has been in the Corporate sector. Same in China..

Also... NZ Govt since GFC and been an active borrower.. and I'm guessing that will continue, but am unsure if it will be for productive investment..

For me , the actual debt levels and how that debt is spent is more meaningful than as a ratio with GDP.

I suppose it all becomes more clear and obvious when we go into a recession and credit contraction..??

The gist of your article implies that NZ is robust and might easily handle a recession...

I'd argue that might not be the case... ( especially because most of our debt is in the household sector ).

My view is that Current Acct deficits should be front page news.... call me old fashioned ..!!

Roelof

Thanks, absolutely spot on and you're right that Current account deficits should be front page news but NZ business news in the mainstream media is woeful. The 4 topics that get any coverage being;

1. How much house prices have gone up (they may be short on content here over the next few years).

2. How one of the main companies in the Country has messed up, Fletcher, Fonterra, Air New Zealand (rarely positive stuff).

3. How much profits the banks have made (normally to induce a moan or a whinge from the viewing public that allowed those profits through their stupidity and greed (increasing the current account deficit)).

4. Avocados. The price of and in relation to intergenerational debate around subject number 1.

And that in a nutshell is the business news in mainstream NZ.

Nice one, but you forgot the mainstay of the NZ media.

Faux outrage about a post on a Company's facebook/twitter.

(Although granted it may be covered by 2)

I suppose it all becomes more clear and obvious when we go into a recession and credit contraction..??

What will happen if there is no credit contraction ? why or who will need the credit to be reduced ?

The Debt to GDP is a little misleading because (eg) assuming 300Billion GDP, 3% growth adding 5billion in debt when there is zero debt will increase debt to GDP by ~1.6%, adding 5Billion in debt when there is 300billion in debt will decrease Debt to GDP by ~0.8%. So it flatters higher debt levels.

I should note it is not quite as bad as 7billion/year (though this 2.5% of GDP balance of payments problems is pretty consistent for last decade), because we are currently also adding about 2Billion a year in offshore assets (International investment position).

Taxing future generations to this extent should be illegal. Ditto for selling chunks of land and strategic infrastructure companies. If today's public had to face the true costs rather than shoveling it onto unborn kiwis things might change.

.

"How is that for the relative value we place on the relevant skill sets?"

I agree, but as both earn more than me at present, I also happen to see the flip side.

Why should you need to earn the equivalent salary of a doctor just to survive?

.

Analytical work mainly.

I can earn a lot more but am in a financial position to accept less by choice. So I do, as I get a nicer workplace, better lifestyle, less hours, less commute, etc...

.

but there is no way her in hand pay should ever be in the same league as a graduate engineer or a doctor or any other white collar professional.

Gosh, that's a weird perspective. I haven't heard the white collar/blue collar distinction used for years... but when it was more commonly used decades ago, I think it was a dichotomy between office worker vs factory worker - not teacher vs engineer or doctor. That aside, though - I think what you are meaning is that certain professions (in your opinion) have more difficult entry/completion requirements and therefore those starting out immediately post-graduation ought to be paid more... but surely that argument belies the rules of supply and demand.

And teachers, at the moment are in very high demand. Why do we have a shortage - well, apparently few people are going into the profession due to the low pay (in comparison to many of their bachelor degree counterparts), long hours (if you count all the take-home work that is unpaid) and associated stress levels (we should all try managing a room full of 5-7 year olds).

In other words, dear Pragmatist, primary school teachers do "work their ass off" - just as do nurses, aged care workers, plumbers, coal miners, forestry workers, policemen and women and a whole slew of others you might not consider to be "white collar professionals".

Earnings these days are not all that well correlated to work effort and/or degree of difficulty and/or vocational dedication.

.

My husband's birth mother had him at 18 - and he was adopted, as was the common practice in those days. I'm forever indebted and of course, delighted that as the young innocent that she was, she made what you would refer to as a 'dumb mistake' based on your points 1) and 2).

My point being - all children are a miracle, a gift, a precious resource - whether planned or unplanned.

And they all deserve a good upbringing, without hardship.

If we could all just think like that, the world would be a better place - I guarantee it.

.

Sadly those born into poverty often seem to have a poor upbringing

Yes, so let's not have any children born/raised in poverty. And what 'fixes' that is living wages and a lowered cost-of-living as well.

So, this:

https://www.stuff.co.nz/business/105679737/its-time-for-business-to-tak…

And a re-balancing of the economy - away from the rentier class and more toward the productive class.

.

Don't get your point, as the second case relates to an adult with no dependents.

In fact it is likely that a person with no dependents on $835/week wouldn't need any support/assistance in order to house, feed and cloth themselves, provided they shared accommodation costs with others.

But then they are not raising the next generation and of course NZ society as a whole benefits from those who are;

http://archive.stats.govt.nz/browse_for_stats/people_and_communities/ol…

Only if they are net tax payers.

Middle class parents generally produce hard working and capable children who will pay a million or more in tax over their lives, huge assets to the govt.

Welfare dependent baby farmers who don't raise smart, educated, hard working kids (and given ~80% genetic heretibility of IQ will on average have children of far below average intelligence) end up producing more welfare dependent adults cost about a million per kid on average, worse if they end up as criminals as a lot do. They are a huge liability for the govt.

Government policy should have strong preference to not robbing (via tax) middle class of their financial ability to have children in order to subsidise poor, because it only worsens the government's financial position (and NZ societies viability) over the long term.

.

"Btw I calculated that if that $835 income was after tax, then her cash position improves by a mere $30 a week.. Yep, a 30% payrise nets her a 3% actual income in hand increase. Talk about welfare dependancy for life."

Exactly - https://www.stuff.co.nz/national/104490079/when-a-16k-payrise-only-give…

Pragmatist, yes, I'm in favour of the living wage movement as well - given we definitely need to offset WFF at some stage. Thing is, NZ employer lobby groups resist labour law reform at every stage. There does indeed need to be a shift in thinking there for sure.

Regards the landlord subsidy, that's actually a bit easier to reverse out to my mind. I suspect the Labour government will address that as soon as they have strengthen tenancy laws - again, that will occur against strong resistance from the landlord lobby groups as well.

With respect to the notion of waiting until one owns their own home, etc. to have children (i.e., what you refer to as "taking responsibility"), it's not like previous generations did that. I was the third child for my parents and was born whilst my Dad was attending university. My siblings were born whilst my Dad was serving in the Air Force. Everyone on the base was having kids. I was three when my parents bought their first home.

It all comes down to our cost of living here - it's just plain too high - hence the government assistance targeted toward those with dependent children.

No Kate - it's actually too low. Much as that seems incomprehensible.

If you're to give future generations the same chances you have, they have to have the same resource-per-head chances you have. That would put fossil energy out of your and my price-range. Which would collapse the fiscal farce that is debt-issued fiat finance, as a useful collateral.

But a 'living wage' is a level of resource access. That can't be maintained by putting tokens issued at a keyboard stroke, in people's hands. Doesn't matter how often the word 'productive' is parroted.

You haven't actually identified any issue that I can see. You are looking at income only, ignoring her expenditure (raising two kids in our most expensive city), and to hazard a guess because doing so makes for convenient political rhetoric. Am I missing something? Why ignore the fact a bachelor Dr has less obligated expenditure than a solo mum?

.

while the top end of town accelerates its accumulation of wealth at everybody else's expense.

Here we are in agreement. Why owner shareholders of Fonterra ever allowed the remuneration of the top echelon of that company to get so out of hand, I'll never know. I'd certainly have happily done Theo's job over milking the cows any day.

Not related to the article.

I thought she was a primary teacher

She is working and looking after two kids but you want to give her a hard time for that?

I’d like to give her more help. I’d also like to drag the father back to make some payments.

.

The system is broken.

Again, we're in agreement. In fact, single income families should be the norm. Where two parent families, of necessity, must both work to make ends meet, the family unit itself suffers - and the result is that many end up converting to single-parent families through parental separation.

You are right, it needs fixing.

PS - and speaking of two income families, another subsidy arises as a result of this becoming the norm - that being the ECE (i.e., childcare) subsidies. How stupid are we as a society?

.

Yes, note that I said two income of necessity - meaning when both partners have to work to make ends meet. That, in my opinion, should not be the norm. What you describe is not of necessity, but rather of choice. No problem with that.

When I first starting looking at RBNZ data around 6 years back I recall that total overseas liabilities was more or less the same figure as M3 money supply. Money is debt. What is interesting is that both data series have been discontinued in the form they were.

The most interesting comment in your article for me David is that we are not borrowing for consumption, but to invest in assets. If debt is still growing but going into assets, then is this not part of the credit fueled asset bubble? I have proposed here that economic growth is growth is the consumption of resources, all the rest is trickery with numbers. I am with Roelof on this one, I would love to see a much better breakdown of the economy. I would use the example of some claims that China's electricity consumption was pointing to a different story of their economy than official claims. Now looking back we know they peaked in coal in 2013, which I believe is a related event. Energy seems a good proxy for the real economy, just as debt/money supply growth is a good proxy for real inflation.

If those assets are existing (old villas and bungalows come to mind) then the borrowing is a bubble. The problem is that housing is about the only big enough thing left to keep demand up to the 'productive economy' - ie everything else

Also, to relate things to GDP at this late stage in proceedings is a little like denying the findings of Galileo or Darwin because they don't fit your old belief-set. GDP could be increased overnight if we all went out and trashed everything in sight. It would go through the roof. Panelbeaters would be hopelessly short-staffed, glaziers rushed off their feet, builders booked for years ahead. We'd be going great guns. If you're silly enough to call that progress. Chch rebuild was GDP positive - but not one Chch resident would choose the GDP over the quake. And GDP avoids costs if it can - as does all business. The proper price for a litre of finite oil is near infinity. The proper price for butning it is full mitigation. Both are avoided.

Then David has to ignore the comments I and others make about the fact that - even as it's measured - GDP must decline from here on.

https://www.zerohedge.com/news/2017-03-09/it-took-4-new-debt-create-1-g…

So debt gets increasingly hard to repay from here on in, as asset-values (mostly house and property prices) decrease to meet the ever-lower ability to repay mortgages.

Tim Morgan has been analyzing various economies and comes to a similar conclusion to your post. He's calculated in the UK they're adding £1 of reported GDP growth with £5.20 in new borrowing. His blog would be right up your alley too PDK.

Yes. Read this report by another one of your messiahs..

https://ftalphaville-cdn.ft.com/wp-content/uploads/2013/01/Perfect-Stor…

An 82 page report of absolutely no substance.

Tim Morgan manages to have more images of ancient ruins than actual content.

You people are so stupid for blindly following 'experts' who disseminate this BS.

To promote the belief that society as we know it will self destruct due to a (poorly calculated) falling EROEI perspective is proper doom and gloom sort of stuff.

I also just read his blog post on debt to GDP that you mention.

Yes. It's a calculation.

No. It's not at all accurate.

It's a pretty stupid comparison to inflate 2003 GDP to 2017 dollars, difference the debt increase and then assume that the two are comparable.

This is exactly why we use hedonics in economics because the composition of measured aggregates changes substantially over time. One only needs to look at the change of the composition of the UK economy between 2003 and 2017 to see this plainly.

please explain how the composition has changed...

Look for yourself - the share of the services sector has increased, while the share of manufacturing has decreased.

That's just in board aggregate terms.

If you broke it down further into industries, there is substantial differences in industry shares over time.

which makes it worse - services are the equivalent of taking in each others washing and calling it economic growth.

Stop getting your economic advice from the Huffington Post.

None of us (I hope) who are more concerned with the 'resource' side of the economy think society will disintegrate suddenly into collapse as you propose - I very anticipate a slow but persistent decline in living standards.

Most of us are here with this view are highlighting the limitation and the oversights that are routinely made by classical economics and 'economists'. You can crunch and manipulate the financial numbers to the cows come home but at the end of the day society is governed by the laws of physics and physical resources - a number of which have been declining in quality and of which society is currently dependent on.

If what many posit here are correct, then the last decade of faltering growth (in the true material sense) appears to be an expected outcome of this hypothesis. I'd love to hear your thoughts on what's driving the declining prosperity most people are experiencing, by all means, please enlighten us.

the last decade of faltering growth

declining prosperity most people are experiencing

Ahhh...what?

How are you normalising this?

By pretty much all measures wealth is increasing throughout the world..

Debt claims are increasing (What you call wealth)

The question is what over.

When that wealth is simultaneously debt, by way of being issued not from wages but by banks with interest, we can also say that debt is increasing throughout the world. The time value of money is paradoxical, and dictates an outcome of uneconomic growth. Wealth may be increasing I agree, but so is debt, and much of that wealth increase would seem to be off the back of flight of debt. How do you even integrate the infinite limits introduced by interest into formulae which model economics anyway?

The time value of money is paradoxical, and dictates an outcome of uneconomic growth.

What do you mean the time value of money is paradoxical?

The time value of money holds under any instance of prevailing discount rate.

What you mean to argue (like all these doom and gloomers) is that somehow we have systematically overpriced debt relative to our true productive potential. Which is a very difficult argument to make when your only evidence is that of your blogger messiahs.

Do I agree that limits are finite? Yes.

Do I think that we have reached peak technology? No.

The argument you silly people should be making is whether we have reached peak technological growth. Until you can prove we have, any argument that we are doomed due to decreasing FF reserves is futile.

https://www.nzherald.co.nz/technology/news/article.cfm?c_id=5&objectid=…

Peak technology in New Zealand for sure. But there are solid principles a logical person can work with, one being that increasing complexity takes a surplus.

That's a very difficult argument to make based on an NZ Herald link.

And not in line with the research, either.

I think estimates of ~1.8 have been used by the RBNZ in terms of their assessment of the human capital ratio of migrants to domestic New Zealand citizens. It sounds awfully high, but even so, that suggests we have a huge scope for growth in productivity.

How many patents have you got Nymad? I just got my second New Zealand one through last week. A quick look at the intellectual property website stats was pretty telling, only about one hundred patents New Zealand patents a year issued to New Zealanders. That total will include corporates and institutions, so the stand alone inventor such as myself is quite rare. I am at the sharp end mate. I can assure you patents don't come easy, it is getting harder to do things that haven't been done. The trend in patents is down. Same for Aussie, where I also have the first of my patents granted. The US is even tougher, although I expect to get it granted there eventually.

"The argument you silly people should be making is whether we have reached peak technological growth. Until you can prove we have..."

The steady decline in interest rates and debt build up since the 70s says so.

Otherwise, we wouldnt need either.

https://www.theguardian.com/business/2018/jul/17/iea-warns-of-worrying-…

Real interest rates are negative?

Interesting.

The peak won't be reached until this is true.

We are quite a ways off that, yet.

As long as they are positive, with low volatility, the expectation is for productive growth.

If you (or powerdown) have developed some reliable forecasts about when this will occur, do share.

"We are quite a ways off that, yet."

Cmon Nymad - although you need no sources, no links, no anything .... you seem to making some sort of prediction here ...

Let us in on your bank of knowledge

I'm not the one always proposing the counterfactual - that's you.

Typically in science you don't have to repeatedly prove the known. It's when you propose the new theories that you need the proof.

I just rely on the existing data and theory, instead of spreading unwarranted doom and gloom manifested by blogging outsiders.

Do we have negative real interest rates - no.

Do we still have scope for technological advance - yes.

Does population grow unfettered, exponentially - no.

Do we only have ~10 years of fossil fuel reserves left - mo.

All the stuff you (and PDK) propose takes literally 10 seconds to disprove with the use of google.

you can only hope for a slow and persistent decline - but that sounds like a nice slope which ignores how a deflationary spiral works ... see Venezuela for the speed & spread of a decline ... once a neighbor loses his income, you lose a customer etc

Economies to scale and leveraged debt wont like a downslope for long and once faith is lost that growth is coming back ...

It is always interesting to see how people avoid. First you call the purveyors something - doomers and gloomers, say, then you denounce doomsaying and gloominess. Or you rubbish any 'source' or linked-to site/commentator.

Some of us just deal in facts, physics, real stuff.

It must be hard for someone who was taught that the planet is infinite, that at some price point a substitute will always be found, that growth in consumption (physical consumption, not virtual, which is a diferentiation that seems to be missed too) can continue indefinitely.

I heard this lady speak at the Otago Chamber of Commerce - made more sense than most:

https://www.theautomaticearth.com/2016/02/where-deflation-comes-from/

"However, given that they all studied the same faulty economics textbooks, we can’t rule out this possibility".

Spent an interesting night with her discussing the whole gamut.......... But at the end of the day, it is hard to change people's beliefs. You can put the facts in front of them, but .........

Simply put, the current debt is unrepayable - there I disagree with the article, which assumes BAU.

/sustainable.unimelb.edu.au/__data/assets/pdf_file/0005/2763500/MSSI-ResearchPaper-4_Turner_2014.pdf

https://www.debtdeflation.com/

Deflation indeed starts at the bottom... the problem though inherent in this article is it suggests that if the rich shared more wealth, we could keep deflation away.

Which ignores resources.

Did she also present at Otago University?

Or did they perhaps require a bit more scientific rigour than the Chamber of Commerce?

You accuse economists of being poorly educated?

Yet, ironically, you are no better. Pretty much everything you propose is predicated on the idea that we are doomed. No scientific process, just poor data and bad theory confirming your bias.

No economist believes in an infinite planet. That's just a soundbite from your 'expert' bloggers.

What they believe is that the limits to technology are unknown. The fatal mistake everyone of you gloomers make is that you assume fossil fuels to be the core driver of economic activity, when that has not been provable on the basis that it and technology, energy, and FF are essentially endogenous in all observable contexts.

You also seem to believe that population is destined to grow at exponential rates until collapse. Just 5 minutes to look at the data and understand the theory as to why this is not true would probably be enough to understand why this isn't at all a foregone conclusion. Feigenbaum might be a good start if you don't believe in economics specific approaches.

You want good science - start proving things.

Until then, don't claim any intellectual or moral highroad.

I've presented myself at Otago Uni.

And the best Professorial retort I've ever heard was at the Otago Uni Staff Club.

Presenting at the 'Staff Club" isn't really akin to an academic seminar, mate.

Nymad - then perhaps try this series of articles...

https://dothemath.ucsd.edu/2011/07/galactic-scale-energy/

https://dothemath.ucsd.edu/2011/07/can-economic-growth-last/

https://dothemath.ucsd.edu/2011/10/why-not-space/

Yes why not space indeed. Surely our tech prowess is so awesome we should be up there at the weekends?

H&E - to quote your source...

The approach is often playfully quantitative, with the aim of arriving at a fresh perspective on our world. Posts stress estimation over exactness, because in many cases a reasonably complete picture can be developed without lots of decimal places.

But hey, I guess accuracy doesn't matter right?

On a long enough timeline we are all dead.

sigh ... its not a source.

Its a blog which highlights dogma and faith in givens .... and whoooosh

Oh.

Sorry for assuming that you were actually going to give us something of substance for once.

Support this idea of better metrics.. the shipping manifests of gold suggest there are some bloody large currency movements that do not feature in official statistics.

Gold movements are counted in official statistics - although I agree they are hard to find (probably because most people have lost interest in gold these days). Look in StatsNZ Infoshare tool, BPM6 Quarterly, Current Account Goods, then select Non-monetary gold (either imports or exports). There is a long, detailed series there.

Gold movements are counted in official statistics - although I agree they are hard to find (probably because most people have lost interest in gold these days). Look in StatsNZ Infoshare tool, BPM6 Quarterly, Current Account Goods, then select Non-monetary gold (either imports or exports). There is a long, detailed series there.

Simplest way to assess our debt is to open your eyes.

Where does all that stuff you see come from?

Where does all that stuff you see come from?

If you're being literal - physical resources and energy inputs. Am I missing something here?

Very literal - Nearly everything we consumer comes from overseas, from predominantly overseas resources, using predominantly overseas energy and transport.

We sell low value commodities, and import high value consumables.

Most of our land, housing, and enterprise is technically owned by offshore interests (Via security on the mortgages/loans)

How could we ever be in credit?

We could be in credit if we had greater productivity and we weren't a quasi-socialist country with govt controlling 30%+ of the economy. However, with communism/socialism back in vogue, this is unlikely to happen.

Communism killed 10 times more people in the last 100 years than Hitler did, yet every other current headline is now trying to justify and validate it in some twisted manner. Oh, how far we've come!

Remember, the wealth of a nation is predominantly about the productivity of its people and not its resources. Japan, Germany and Switzerland have proven this clearly. Russia and Africa might control way more land and resources but they are still essentially third world. Sorry for the rant, just had to get that off my chest...

Agree with Communism, Disagree with the rest. The three countries you have mentioned haven't proven a thing.

Japan has been in economic decline for as long as I can remember.

Germany is showing every conceivable red flag for a major and catastrophic collapse.

Switzerland is nothing more than a store of other peoples "wealth" (Much of it ill-gotten historic gains)

Who are the Super powers? USA, Maybe China, Maybe Russia? Why - because they have the resources to control the resources.

I agree that they are now in decline, but their post WWII ascent was significant and undeniable. Like us, they are now in the decline phase. USA and Russia also in decline, much like Rome and every other empire since. The next financial and military powerhouse will be China...until it too enters the decline phase of the cycle, well after we're gone....

I'd disagree Ludwig. Without control of their own energy supply, food and the Seas, China will never be truly great. You particularly need to be in control of the power sources to be the biggest.

Dutch hegemony was lead by the wind, for production at home and trade across the oceans.

British hegemony was fuelled by coal to power the factories (the British had plenty of it) and the seas to control the globe.

American hegemony. They have everything they could ever need, all the fuel they could ever need, all the food they could ever require (if they had to) and access to both of the biggest seas. Geographically they have massive advantages too, a friendly neighbour to the North with an impassable landscape beyond.

The Chinese currently fall short on food production, fuel resources and control of the seas and it will be a difficult ask for all three of those to be satisfied between now and the more likely national revolution of the underclasses. Those that fear this have already been jumping the country with their wealth and having had a taste of democracy prefer the freedoms it presents. Interesting times indeed, in a digital age with information opening up, the Chinese state may struggle to control the next generation to the same extent that they have been able to control the current one.

"I agree that they are now in decline, but their post WWII ascent was significant and undeniable."

It's a false economy though (Just like Chch). They were rebuilding from the war. It wasn't "Productivity" or "Economic activity" or any other economical buzzword. It was the literal replacement of destroyed nations to return them to the state they were in before the war.

To ask you a question. Why are they (Germany, Japan, even Rome) in decline if they were so "productive"? My guess is the answer lies with resources (or lack there-of)

Oh dear Oh dear. Both communism - actually, it never is communism, it's totalitarianism via the inability of the masses to oust the dictator(s) - and capitalism draw down resources. We are so grossly overshot, thanks to fossil-fuelled food production, that the die-off to come will make all mass deaths of the past seem minor.

Productivity - how many time have i got to point his out? - is merely the more efficient use of resources, particularly energy. The problem seems to be that economics-trained people think that wealth can be created by taking in each other's washing, and that we just have to do it ever-quicker.

The reality is that every washing-taker-inner, expects to exchange some tokens for some bits of the real planet, on the supermarket shelves. Those took resources and energy to deliver. Doesn't matter how productive the washers are, if there's no stuff on the shelves they won't be buying anything.

Japan, Germany and Switzerland do it by ripping the resources off the third-world - as we do once removed. Has nobody told you about the Monroe Doctrine, the United Fruit Company, Union Carbide, King Leopold, Cecil Rhodes? I;ll add to the list if you want..........

As the article and (well-argued) comments suggest, Debt, can be looked at in many ways. As all reason, it's not 'the amount' of debt that's an issue, but 'what's done with it'. (NB: It's not Debt, as such, that's good or bad, but the application of it)

I recall being stunned some years back when a multiple property investor was being interviewed on Australian TV and was asked "So how much debt do you have?" and the answer came back "About $10,000. It's all on my credit card!". The interviewer, puzzled, then followed up with "But what about the $12,000,000 in mortgages you have? '

"That's not debt!" was the response,"That's mortgages. Everyone has those..."

I have seen a similar one (on an aussie show about 10 years ago)

It has always stuck with me, as I distinctly remember choking on my dinner when I heard it.

"It's not my debt - the rent covers the mortgage."

Saw a survey a couple of years ago that showed that an astonishingly high percentage of Canadians thought that when the value of a house dropped, that the amount of the mortgage owing on it dropped at the same rate.

If your assets comfortably exceed your debt then you don't really have worries about debt. Say you had 24 million in gold and 12 million in mortgages, would you feel you were in debt? Or if the income from the indebted assets was comfortably covering the cost of the debt.

I guess it comes down to confidence in the asset. It's a silly, almost meaningless, question to ask in isolation. I suppose only the DGMers, who seem to believe that real estate has no value, would spit out their weet-bix at the 'no debt' answer.

100% correct - Ironically MasterCard sum it up the best

$500k = Debt

$750k = Assets

Explaining to the family why you sold your family home, car, and furniture to now live in a sh!tbox rental down the road, with a 90s Lada, and some pellet furniture (that is not the sort hipsters have) = Priceless.

That's one way to lie to yourself. You have an asset which can and does change in value against a debt which is of fixed value. And tell that to people with negative equity.

Debt is slavery.

Zachary that reminds me of a story from a mate in the UK.

In 2004, a good friend of mine bought a house in the Home Counties, over 1000 square meters set in large grounds 35 miles from Central London. He paid £2.8 million putting down £1.5 million and borrowing £1.3 million (the stamp duty he settled in cash). Now this guy had done well and his business, which was selling recycled paper to China was churning money. He had the cars, a few good holidays a year and kids at private school. In 2007 his business lost its main contract into China. 2008 the business went under, the house went to the market at £3.2 million (he'd spent a bit on it). He turned down an offer of £3,000,000 in March 2008 (Spring was coming and he thought he'd get more).

House finally sold in September 2009. He'd hung on for a while and had turned down higher offers at £2,000,000 and £2,100,000 wanting back at least what he'd paid for it, but it finally had to be sold or he would lose control to the banks. the price was £1,400,000. His net worth at the end of it all was just £100,000 having put in £1,500,000 5 years before. The power of leverage!

And that's how any leverage can destroy your position when there are no buyers and the banks want their capital back.

(It's not all sad though, he's made his money again since 2009, but he's a lot smarter than most property speculators I've met and has a good mind for business)

If your mate had put down 1.5 million pounds and borrowed 1.3 million pounds on ten or so well chosen rental properties I don't think he would have had any losses at all.

Your example is an extreme one.

It is purely an example of what can happen when credit conditions tighten. How many here have re-financed the farm/family home to get into buy to debt and what happens if the banks decide they want more protection come re-financing time? Remembering that the majority of NZ loans are short term, a couple of years, what happens if re-financing becomes a beauty parade?

It can never happen to New Zealanders....we is immune....We is unvested in property......Rich as Crosseus..

We is leveraged, we is famous for it...ain't we not..We is OK...big time. Da Banks are our Friends.....Ya boo sucks.

https://www.businessinsider.com.au/rich-famous-celebrities-who-lost-all…

ZS - actually, land and useful structures are some of the best ways to secure your 'wealth'. At least they're real, although it may get to the point where you need to defend your ownership......

But RE is not an asset if debt is involved - the banks will all fail at some point in the coming - and permanent - decline, but they may well hang around long enough to mop up the mortgage-defaulters as per the mid-west farms in the 1930's,

And a mortgage-serving income has to continue - which means the tenant has to keep earning (because capital gains don't go upwards forever),. Worse, if the tenant has a rentier-on-the-energy-system 'job' - real estate salesperson, say - then there has to be someone in the real world supporting both that tenant and you. Almost nobody thinks this stuff through.

You are right PDK but currently we don't have this apocalyptic scenario occurring and it doesn't seem likely to happen in the near future.

I don't buy into the decline theory as I have observed that most of our problems are caused by too much abundance and not scarcity: obesity, pollution, cheap travel, gadgets, ennui...

Ah, that'll explain the angry young men in the desert and the incressing refugee streams and the sprawling shanty towns and places like Haiti and Rwanda and Bangladesh and Mexico City.

They all reek of abundance.

silly me, there I was thinking that poverty was a lack of resources per head.

Yes, indeed silly you PDK, haven't you noticed their chubby cheeks, their cell phones and their fashionable clothes? Most are quite Westernized and many speak English. Abundant technology has enabled them to see what it is like in the West from afar. Abundance has made their journey feasible. Abundant wealth in the destination countries beckons them. Western politicians feel they have abundance to spare.

Many of these refugees come from the more well off families in Africa and other places as they can afford to pay the traffickers.

Abundance enables them to have very large families averaging seven or more in some places. Abundance enables their countryman to buy huge amounts of weapons and feed armies and wage wars for many years as in Syria and the Congo. They even have jets and tanks and helicopters, an automatic weapon for everyone, even children and no shortage of ammunition.

Abundant aid continues to sustain large and growing populations. The problem is too much abundance.

And abundance of debt to pay for it all.

The $247 trillion global debt bomb

In the first quarter of 2018 alone, global debt rose by a huge $8 trillion. The figures include all major countries and most types of debt: consumer, business and government.

What Tran is suggesting is a global shift away from debt-financed economic growth. The meaning of the $247 trillion debt overhang is that many countries (including China, India and other emerging-market countries) will be dealing with the consequences of high or unsustainable debts — whether borne by consumers, businesses or governments. There will be a collective drag on the global economy.

“If you are in a high-debt situation, you need to bring the debt down, either absolutely or as a share of GDP,” Tran said at the briefing. “[Either] will result in slower economic growth. You don’t have the borrowing needed to maintain strong investment and consumption spending.”

https://www.washingtonpost.com/opinions/the-247-trillion-global-debt-bo…

you may have to google the header to get past the filter at the Washington post.

The statement "every lender requires the borrower to have skin in the game, a level of equity to support the borrowing" is not exactly true. Unsecured debt like Credit cards in particular are an example of this.

A borrower using Visa or MasterCard only needs to establish they have some moderate source of income. A means to repay.

That is a minor exception. Total NZ private sector debt is $438.0 bln (May 2018). Total credit card debt is only $7.2 bln of that, a tiny 1.6% of the total. It's not relevant in the New Zealand economy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.