By Chris Rands*

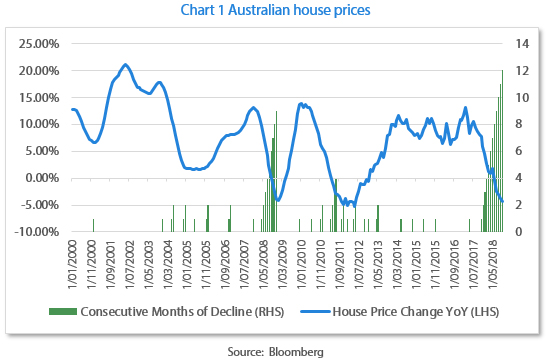

While the performance of house prices has been poor, we don’t believe this is reflecting housing stress. Rather it is due to tightening lending standards, which are constricting credit supply. While this means house prices can continue to fall over the next 12 months, it reduces the risk of a crisis occurring through the housing sector. To analyse this we look at debt service ratios, prepayments, loan to valuations, arrears and household stress levels.

Debt service ratios

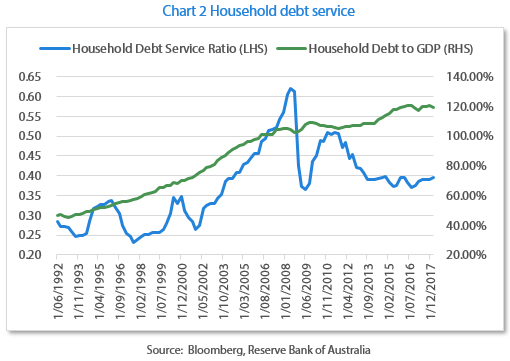

One of the most common criticisms of the Australian housing market is that it is funded by huge household debt. This is undoubtedly true as household debt is approximately 120% of Gross Domestic Product (GDP), which, in the developed world, is only surpassed by Switzerland.

However, this measure by itself misses a key component of housing affordability — the rate of interest paid on that debt. While household debt levels are at historically high levels, the cost of servicing that debt is at an all-time low. This idea is captured in the debt service ratio of households, as shown in Chart 2 below. This ratio shows that while household debt is high, the ability to repay that debt is by no means stretched and that the household debt serviceability remains around the long term average.

The Reserve Bank of Australia (RBA) echoed this message in their October 2018 Financial Stability Review: “Total payments as a share of income have remained broadly in line with their levels over recent years”. This means that while households are highly indebted, it is unlikely that they are struggling to repay what they owe in the current interest rate environment.

Prepayments and equity

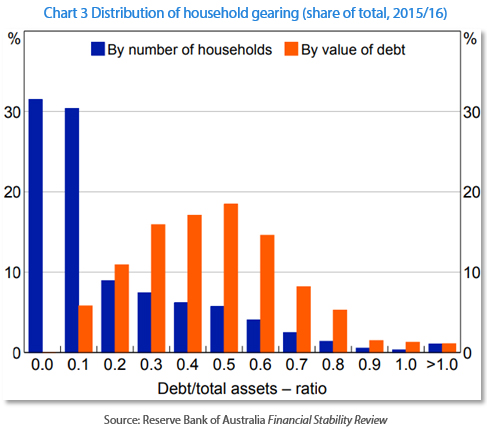

Given household debt service metrics remain around average levels, it is also important to look at the distribution of household debt to determine if vulnerabilities exist. One way to measure this is through loan-to-valuation ratios, which measure the level of debt compared to the value of the asset. Vulnerabilities here involve households with greater than 80% debt, with the households most at risk being those with over 100% debt, which results in negative equity.

From this perspective the current distribution of debt looks relatively robust. RBA statistics show that only a small percentage of borrowers have loan-to-value ratios above 90%, while the majority (approximately 60%) have a loan-to-value ratio of less than 10%. This means the moderate declines we’ve seen in the housing market will not create a situation of negative equity for a meaningful share of borrowers. This situation differs from the United States in the mid 2000s, where loans where written at up to 120% of the housing value, creating a large vulnerability to even moderate declines in prices.

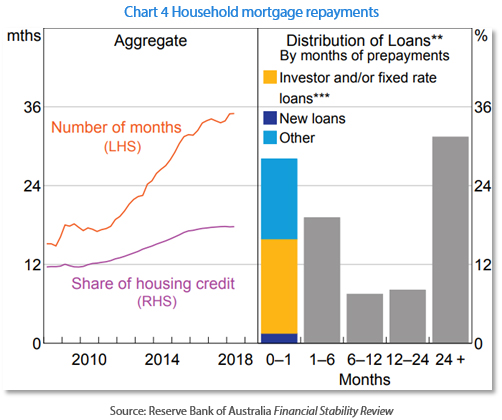

In addition to this, many households in Australia are ahead of their scheduled repayments. This is thanks to the floating nature of the Australian housing market — when interest rates fall, loan repayment amounts are not automatically adjusted downwards. This means households have the ability to repay principal outside their scheduled payments by maintaining the original payment amounts.

RBA statistics show that the average borrower is almost 36 months ahead of their required payments. Of the borrowers who are not ahead of schedule; approximately half are investors or fixed rate borrowers, who do not have the same incentives to repay ahead of schedule, and new loans that have not had time to accrue prepayments. This means for the vast majority of borrowers in Australia there remains considerable buffers against mortgage stress should their situation deteriorate.

Household stress and arrears

Overall, the combination of these statistics suggest that the decline in house prices in Australia is not a demand side or housing affordability problem, but potentially related to tighter lending standards coming through the banking sector. A signal of this is that there are no real signs of household stress or mortgage arrears.

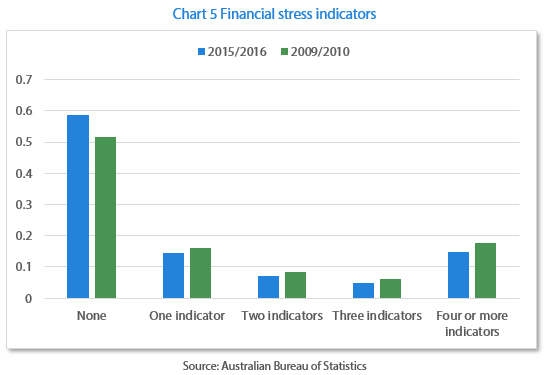

The Australian Bureau of Statistics (ABS) releases a measure of financial stress using indicators on households such as ‘Unable to raise $2000 in a week for something important’. While these statistics are not particularly timely, the 2016 results show that overall there are few signs of stress in households when compared with prior years.

Since 2016, interest rates have fallen, unemployment has declined, growth has improved and house prices have increased, meaning there are few macroeconomic signals to suggest that household stress would have increased substantially since 2016.

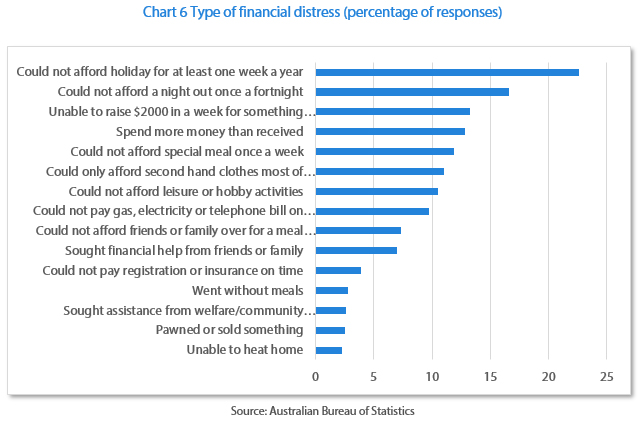

Breaking down the types of financial stress reinforces this point, as the largest percentage of stress shown is the inability to afford a holiday or a night out once a fortnight. While this is a serious issue and should not be treated lightly, it is somewhat comforting that the signs of stress are in discretionary spending categories rather than the necessities of life such as ‘Went without meals’ or was ‘Unable to heat home’.

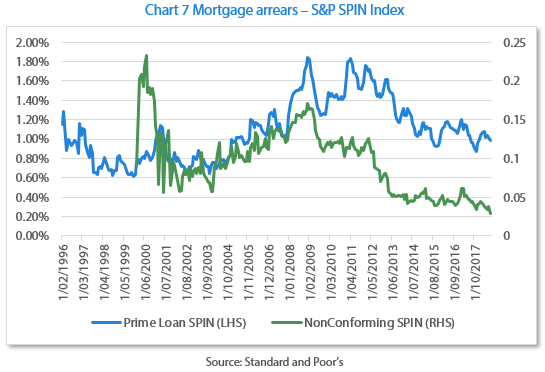

The low level of stress is also reflected in Australian arrears levels, which have been trending downwards over the past four years. Standard and Poor’s SPIN index shows the mortgage arrears for prime and non-conforming loans are well below the 2008 and 2012 levels, which were associated with the previous housing downturn. This highlights that Australian households are not struggling to meet the repayments on their loans, as described by the debt service metric.

Credit supply

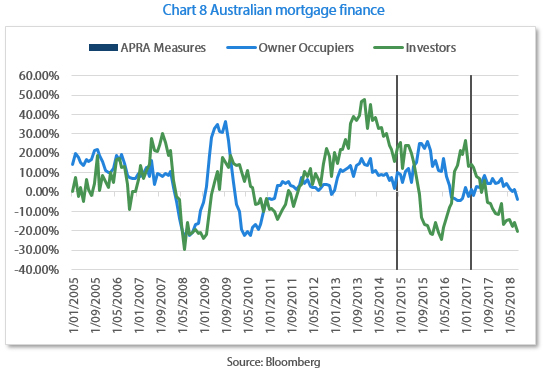

Given that households are not showing signs of stress, this raises the question: “What is causing the decline in house prices?” The most likely answer is that credit standards at banks have been tightening, restricting the flow of mortgage finance in the economy. This reduces the amount of borrowing that households can receive, leading to a lower budget for home purchases. There are two key drivers behind this change since 2017.

The first is that the Australian Prudential Regulation Authority (APRA) announced measures that were designed to slow the amount of investor lending in the Australian market. These measures were similar in nature to earlier changes made in 2014 that led to substantial declines in the amount of investor lending that banks made. A key difference now, compared to 2014, is that the prudential tightening has not been followed by an interest rate cut like it was in 2015. The interest rate cut in 2015 led to an increased demand for owner occupied borrowing, offsetting the decline in investment. The slowdown in investor lending has not been met with accelerating owner occupied finance.

The second factor is that the recently released preliminary findings from the Royal Commission into banking have added greater scrutiny to bank origination practices. One example was the finding into how banks substantiate borrower expenses (it is up to the banks to make reasonable inquiries to a consumer’s financial position before lending money). In the preliminary report the Royal Commission stated that “more often than not, each of ANZ, CBA, NAB and Westpac took some steps to verify the income of an applicant… But the evidence also showed that much more often than not, none of them took any step to verify the applicant’s outgoings”.

This sentence essentially puts the bank on notice that they need to improve their internal processes for determining the expenditures of a borrower, rather than just relying on a benchmark index such as the Household Expenditure Measure. Making these changes will mean that, on average, higher expenditure figures will be applied, reducing the amount of credit that a borrower can receive compared to just relying on a benchmark calculation.

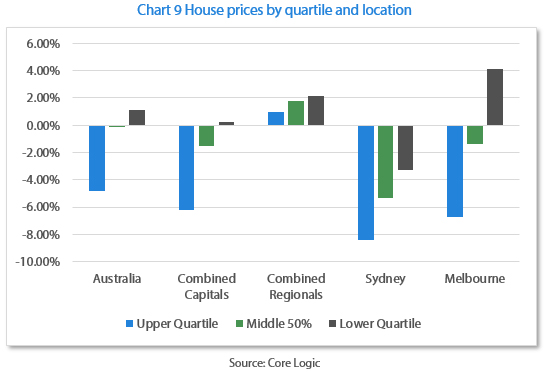

Overall, the combination of tighter oversight from APRA on investor lending and the spotlight placed on banking practices from the Royal Commission has meant that credit has become relatively tighter over the past 12 months. With lower levels of credit available, it has been the higher end of the market that has borne the brunt of the falling prices, as borrowers may not be able to finance quite as much as they could in the past. This idea can be seen in Chart 9 where the price effect is split into quintiles of the property market. The blue bars represent the upper quartile of the market with the largest declines. According to housing data provider Core Logic, the “weak housing market conditions across the most expensive quarter of properties in Sydney and Melbourne” is “a key driver of the housing downturn.”

The forward indicators

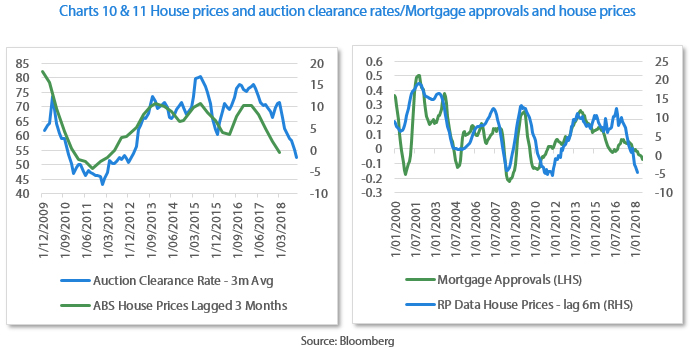

The upshot of this is that as long as credit conditions tighten then house prices can continue to decline, even though no household stress is yet evident. At the moment, forward indicators such as the level of mortgage financing and auction clearance rates have continued to fall and point to declining house prices in the near term. Over the past five years, whenever there were conditions similar to these, the RBA was cutting interest rates, breathing life into the housing market. This time round, however, the RBA seems inclined to sit on their hands, giving little incentive to forecast a quick rebound in these indicators and hence we expect softer prices next year.

What else could go wrong?

Since housing affordability currently looks fine, it is also prudent to ask: “What could go wrong for affordability?” To understand this question it is best to look at the two key components used in the debt service metric: disposable income and the amount of interest paid. This creates two key risks that underpin this analysis: that either interest rates rise or disposable income falls.

Risk 1 – Interest rates rise

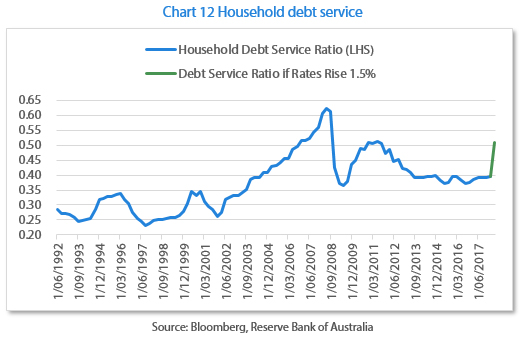

One of the biggest risks to the current situation is that interest rates rise quickly and cause the debt service metrics of households to decline rapidly. As shown below, even a 1.5% increase in interest rates is enough to take the economy wide debt service metric to levels which were associated with household stress in 2008 and 2012. Even small increases in interest rates could have outsized effects on the household sector.

Despite the relatively small moves in interest rates needed to cause the debt service metric to deteriorate, this doesn’t look likely to occur over the short to medium term. The RBA remains in no hurry to increase interest rates and is aware of the risks that the household debt load poses. The above chart shows that even when the RBA is ready to raise rates they will likely be more cautious than in prior cycles, leading to slower cash rate increases. This creates an outlook for stable mortgage rates in the near term and means that while rising interest rates could hurt the economy, it is not likely to occur in the short to medium term.

Risk 2 – Disposable income falls

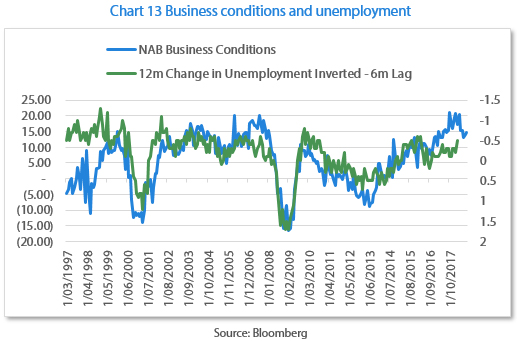

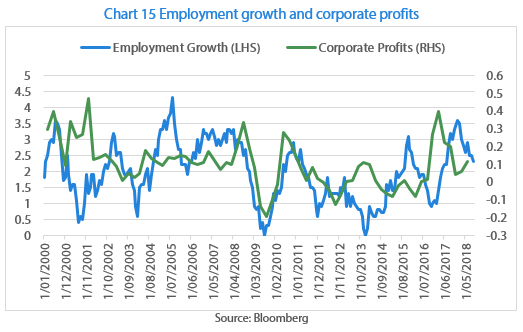

The second big risk to the household debt levels could come from falling disposable incomes, which would usually be preceded by a rise in unemployment. While an increase in unemployment would hurt, the current business environment shows that the employment situation in Australia looks strong. For example, the NAB Business Conditions survey remains just off its all-time high, which often leads the direction of unemployment by approximately six months.

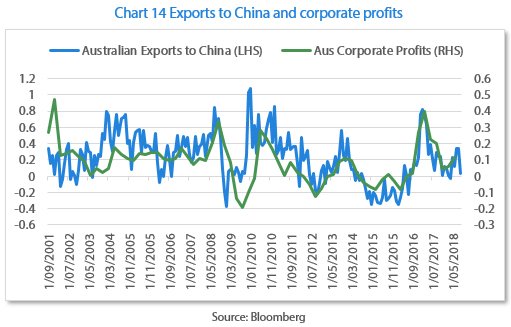

Despite the positive business conditions, the current economic conditions in China bear watching as they can quickly filter into the Australian economy. One way of showing this is the effect that China can have on Australian corporate profits. When Australia records higher exports to China we subsequently see large increases in corporate profits, quite often driven by the commodity sector.

The risk here is the strong rise in corporate profits in 2017 led employers to hire more workers, driving the employment rate higher. The slowly escalating trade war between the United States and China means there is an increasing risk that our exports to China will slow, which would hurt corporate profitability and potentially slow employment. This bears monitoring going forward, as declines in employment would hurt disposable income and hence run the risk that the housing slowdown intensifies with declining affordability.

Putting it together

The high household debt levels in the Australian economy make it vulnerable to risk. However, interest rates remain low, mortgage repayments are affordable and there are few signs that the declines in house prices are being driven by household stress. The declines look to be driven by tighter credit conditions, which have reduced the supply of credit for potential borrowers. This means that while house prices can continue to fall, it is less likely that it will turn into a widespread problem causing large scale defaults. The more likely outcome will be a slow burn lowering of prices, which takes the edge out of consumption and weighs against consumer confidence, leading to slower growth rather than a melt-down similar to the Global Financial Crisis.

Chris Rands is a porfolio manager, Fixed Income at Nikko Asset Management based in Sydney. This article was a briefing posted on Nikko AM’s global website, and is here with permission.

33 Comments

An alternative view from news.com.au on Austrlian Housing Market

https://www.news.com.au/finance/economy/australian-economy/house-prices…

Interesting view. Last meltdown occurred when all and sundry (almost all!) felt everything was rosy and economy fine and risk low etc. of course Nassim Taleb analysis shows this to be typical stupidity on behalf of those in charge of monetary policy. Risk is that equity of banks is 65% mortgages. So, sen-defeating down loop identified starts with negative equity number rising. In fact biggest sign is what Martin North showed yesterday in his excellent Digital Analytics website. This showed growth in money supply in Australia in 2017 as 6%. This year? 1.9%. That drop is substantially more than NZ has had since late 2016 and signals recession by Steve keen criteria. USA seems to be heading same way looking at their housing market and sales. NZ is tail at end of flagging dog

We're just a bit slower to catch on I think Mike... too many people relying on the Herald for their news..

A very indepth report thankyou. Sounds like the situation is much better than some on here painted it to be.

Even Australia would have to correct a long way to make it as cheap as America - a place with higher salaries for professionals, and cheaper goods and services.

@saving4AUhouse .......just have to concur with you totally about the USA ...have been in the Maryland property market (just outside DC, 8 miles from the White House ) for 6 years now and my trips there and back always leave me with a sour taste in my mouth, with just how "friggen expensive" NZ is when it comes to property and related products and services here - especially Auckland. The build quality is utter crap ie how many "white covered" new apartments do you see round town being rebuilt !? ...wouldn't happen in the States - those builders/developers/councils etc woulds be faced with a lawsuit !!

TL;DR? Here is the summary:

This means for the vast majority of borrowers in Australia there remains considerable buffers against mortgage stress should their situation deteriorate.

...there are no real signs of household stress or mortgage arrears.

...overall there are few signs of stress in households when compared with prior years.

...there are few macroeconomic signals to suggest that household stress would have increased substantially since 2016.

Breaking down the types of financial stress reinforces this point, as the largest percentage of stress shown is the inability to afford a holiday or a night out once a fortnight. While this is a serious issue and should not be treated lightly, it is somewhat comforting that the signs of stress are in discretionary spending categories

The low level of stress is also reflected in Australian arrears levels, which have been trending downwards over the past four years.

Given that households are not showing signs of stress...

"This means that while house prices can continue to fall, it is less likely that it will turn into a widespread problem causing large scale defaults. The more likely outcome will be a slow burn lowering of prices..."

This will be an interesting one to look back on in a year to to eighteen months. If they are going to continue to fall, at what point will the become a problem? Already nearing 10% in Sydney with many forecasts now of 20%. Will 20% be a problem? How about 30%?

Yes at what point indeed. Slow burn = frog in slowly heated water.

Yesterday I didn't get one upvote, not one, for questioning mortgage stress claims in Australia.Can't help feeling a little vindicated. I actually started to doubt myself. Lying awake through the night. Had i lost my mind? Was i being unreasonable? Dare I show my face here again?

Look at the stress chart, ignore the first two lines (can't afford holiday.. etc, just noise), and look at the third and forth lines: Spend more money than received, and couldn't find $2k in a week. 12% spending more than they are receiving, and a similar number that couldn't deal with a major car/house repair.. Lets just gloss over that one, its nothing.

It could be fairly normal. Like the 5% unemployment rate and numbers of homeless. I also have doubts about the veracity of the responses. Australia is one of the richest countries in the world. The average Australian is wealthier than the average American.

Australia is the second-wealthiest nation in terms of wealth per adult, after Switzerland,[27] however, in 2018 it overtook Switzerland and it became the country with the largest median wealth per adult - Wikipedia

If they are spending more than they are receiving one week out of 10 or something, then yeah, that gets averaged out over time and no problem. But if they are spending more than they receive 3 weeks out of 4.. then unless you have a huge pool of savings you are going to shortly end up in debt and out of lines of credit. That's a fundamental problem, unlike not being able to afford a holiday.

You cant safely take averages or per capita wealth when the top 10% owns much/most of the wealth (and income). You need a substantial % of the ppl to be spending money for a bouyant economy, if they dont as they are broke then the economy will tank.

It may be "rich" but do people have the income to support the "wealth" / debt. The old asset rich cash poor conundrum.

Agree....

Also I wonder on what % sets the market value. Not sure how to word this but by this I mean a sort of "marginal cost" so if say only 5% of buyers sets the price (excessively) high, removing that 5% of would be buyers depreciates the price significantly. In these numbers then 12% might actually have an massive impact, way out of proportion to only 12% implied, sort of non-linear.

You dismiss one source of mortgage stress, you embrace another. You might be right in your questioning, or it might be confirmation bias.

While this analysis tells us everything is awesome, there are umpteen analysis that show why Australian property values are falling and will keep falling.

The thing about mortgage stress is that it will kick in as values keep falling, as all those people who are negatively geared, and those with interest-only mortgages, realise it's time to get the hell out at the same time. They were only in it for the capital gains. A lot of people will be baby boomers nearing retirement age, who can't wait 10 years for values to get back to anywhere near where they are now.

The above article is looking at mortgage stress through a slightly different lens.

Decline in house price has very little impact on your ability to pay the mortgage. The nominal value of the house does not impact your day to day spending (although it may add some mental stress to those not accustomed to price drops)

So no, the drop in housing values is not going to stress out most mortgage holders.

What will stress them is any impact on their day to day income/expenditure.

Interest rates increase = Stress.

Job loss = Stress.

Living costs increase (e.g. food or petrol) = Stress

The stress is real. Just remember house price changes are the effect, not the cause.

Your so right Noncents, its a point missed by many on here. Basically you need a place to live if you have a family and you just keep on paying that mortgage. Rising interest rates would begin to affect home owners the most.

Noncents - you read any works by Kahneman on loss aversion? Thinking Fast and Slow is worth a read if you have time. To claim there will be no stress involved in seeing house prices drop, perhaps means you don't fully understand human psychology and desire to avoid losses which we find quite painful. To some it will become unbearable and they will start selling on the way down - even if its not in their best interest to do so - simply because they can't stand looking at the losses they're making.

All very true, and agree with the psychology. Mental health wise, we are disintegrating at a rate never seen before. Loss aversion is just another trigger for everyone (renters, freehold, mortgage, etc...) at this particular point in time.

I would add that loss aversion it is not strictly Mortgage Stress. It doesn't impact the persons ability to pay the mortgage, rather it changes their mindset on whether those ongoing payments are worth it?

In the long term I would say probably. But most people barely think about net week (financially speaking) let alone 30 years into the future.

Like all things half will look back and wish they sold. Half will look back and wish they didn't.

Australia housing market will be the one to watch. They will have Federal election next year; Labor will scrap the capital gain tax concession and put restrictions negative gearing. For the Liberal, their chance of winning is about as thick as hairs on my bald head!

The problem isn't stress. The problem is that at current pricing - and without capital gains - Sydney housing is a crap investment. All this is saying is that people can easily afford to service the debt on a crap investment. It does not answer the question of why people would hold a crap investment.

Australia is fine, they have on average 36 months repayments in the bank that they can coast on, right?

Can they tell their bank that they will stop repayments for 36 months because they have a buffer?

Does the typical mortgage household in NZ have 36 months extra up their sleeve?

Another 5% price fall and it will become interesting. 10% and the banks will sweat hard.

One for Zachary, and anyone else wanting an overview of the Australian property market;

https://www.youtube.com/watch?v=vrY2KLavsoQ

Starts properly around 3:30

The title is a bit sensationalist, but if you can look past that you'll find it's a pretty balanced analysis from some good analysts.

Looks like the Australian property market is going to be getting hit with a Global downturn at the same time it is already having a correction. I have a feeling this is going to escalate the falls and we could see major carnage over there. Time will tell what will happen in NZ but there will be some risk coming to our big 4 banks from across the Tasman if things go south in Australia.

So Australia has household debt of 120% of GDP, NZ is just 90%. Doesn't sound too healthy to me. If we have another global recession there is going to be an awful lot of pressure on those high debt households.

When they tell you not to Panic, it is definitely time to do so.

So the advice appears to be.. HODL!

Great analysis, but.... it assumes nothing unexpected or disruptive ever happens and things just travel along happily. Typical use of statistics, first assume a normal distribution. You only get a normal distribution when nothing unusual happens. Mandelbrot says that in the real world of finance you get periods of mild risk when such statistical approaches work, periods of moderate risk (ie 3% up and down days in the S&P500 as now) and periods of wild risk (eg Lehman collapse).

There is a global slowdown taking place if you look at the US treasury yields, combined with high levels of instability in global stock markets. These are warnings of interesting times in the near future. It's got bugger all to do with Trump, by the way, and everything to do with the global build up of unrepayable debt. Maybe it will all just settle down. Maybe the authorities do actually, really, have it under control, honest. Equally, it could all spiral rapidly out of control. Markets are risky.

The author is the stock market equivalent of a real estate agent, only brighter and therefore much more dangerous. He works in a show business type area where it is always a good time to buy (for him, not necessarily for you). The media depends on these people for advertising revenue.

We appear to be in a moderate volatility regime with Aussie housing, so it is riskier than it appears.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.