Here's my Top 10 links from around the Internet at 10 am in association with NZ Mint.

As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must reads today are #5 and #6 on China's version of finance companies known as Wealth Management Products, or 'Weapons of Mass Ponzi.' Jon Stewart's view on the North Korean tapdancing on the brink is very funny.

This is what happens in an ageing economy with no inward migration that is struggling to cope with the collapses of real estate and asset bubbles.

Japan has been in recession with low to no inflation for decades.

Only now is it getting incredibly desperate.

Desperate enough to print like there's no tomorrow.

They're hoping it will create a tomorrow.

This just reinforces to me the power of demographics and how damaging asset bubbles can be.

The rest of the developed world faces the same ageing problem, albeit with the help of migration and in most cases a higher birth rate.

Here's CNN:

Skeptics abound, however, and even Abe has acknowledged that hitting the 2% target before the deadline could be difficult. In particular, economists are worried about sustained downward pressure on wages in Japan, a trend that makes inflation difficult to achieve.

Economists expect the bank to, at the very least, ramp up its buying of bonds. It is already buying short-term debt and could expand its balance sheet by buying longer-term debt or more exotic assets like corporate bonds, "commercial paper" and ETFs. The bank could also move up the start date for asset purchases.

2. Could Invercargill become a data centre capital? - An idea raised by Paul Brislen from the Teleccommunications Users' Association via NZ Herald is that the Tiwai Pt power could be used to run a rash of data centres in Southland.

Big data - the ability to sift through massive data sets to seek out trends and analyse information on a global scale - is the next big wave to hit the ICT industry and New Zealand could be well placed to take advantage of it.

We have cheap electricity and cheap land. We have a trained, capable workforce and we have political stability and a remote location - all very desirable attributes for a data centre. We also have sustainable, green electricity.

Oregon data centres are typically 60 per cent coal-fired, with 40 per cent nuclear and the companies that build them are under tremendous pressure to clean up their act.

We can absolutely help with that. All it takes is a vision and a willingness to walk away from a smelting business which doesn't make money and which requires corporate handouts to keep going.

Data centers do like power (and the cold), but not nearly as much as aluminium smelters. The NYTimes reported, in September 2011, that Google itself uses a continuous 260 MegaWatts of electricity worldwide.

Impressive as it sounds, all of Google’s demand for data center power is still less than half the freed up capacity from Tiwai. So no – we cannot replace Tiwai’s electricity demand with a data center. Or even 2,354 of them.

4. Portugal no confidence motion - This is one of the themes of the European debt crisis. The Eurocrats are obsessed with using austerity to fix the debt problem. The trouble is the high multipliers for government deficts in recessions driven by private sector deleraging means austerity is failing.

And now the voters are revolting. Understanding Europe's economy and where it goes is now all about watching the politics.

Here's the reliably euro-sceptic Telegraph with its take.

Although the motion is almost certain to be defeated by the ruling coalition, which enjoys a comfortable majority, the move exposes growing dissent over the austerity policies imposed on Portugal since it received a €78bn international bailout agreed in May 2011.

"The time has come to put an end to the austerity policies that are impoverishing our country and demand heavy sacrifices from the Portuguese people without them seeing any results," the Socialist Party said in the motion.

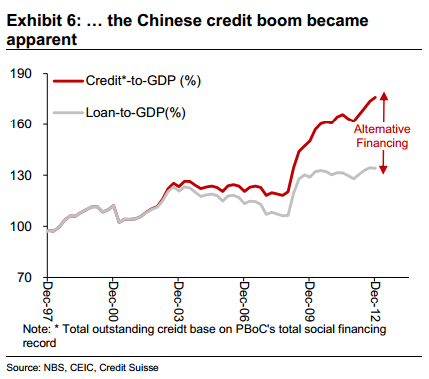

5. China's Weapons of Mass Ponzi - FTAlphaville's Kate McKenzie has written an excellent summary here of the detail of a crackdown announced in China last week on banks' use and promotion of Wealth Management Products (WMPs).

These are the finance company style vehicles set up by China's banks to circumvent restrictions on term deposit rates and to offer higher returns to savers by lending out money to property developers willy nilly.... Now where I have heard about that type of thing...

This can't end well and as McKenzie says and the chart shows, the numbers are now very big. See my bolding. Just reeks of Ponzi.

As Capital Economics’ Mark Williams and Qinwei Wang write, around 60 per cent of WMPs were of less than three months duration, far shorter than the underlying assets:

WMP issuers have adopted two main strategies to deal with this problem. One is to repay maturing WMPs using money raised from new WMPs. This would leave any given product highly exposed to a downturn in confidence in whichever asset class it was invested in.

Stevenson-Yang is sceptical that these measures are intended to seriously curtail the volume of shadow financing activity. She writes:

The elephant in the room is that the shadow institutions are the co-dependent evil twins to the commercial banks. This is true in two ways: banks are reliant on the shadow institutions to supply their liquidity, and shadow institutions get a lot of their capital from the banks.

6. More excellent background on China's shadow banking system - This is another excellent piece from McKenzie from late February on China's fast growing shadow banking system and the risk that much of China's growth since 2009 has been debt fueled and that debt is rising far too fast to be sustainable.

It also raises the question: how is all this extra cash in China leaking out into the rest of the world? How much of it is ending up here to inflate our own property bubble?

There are clear signs, for example, that the central Chinese authorities are again worried about excessive property prices. And the pace of innovation in unregulated products is at times astounding.

There are numerous reasons to think China’s credit growth is at unsustainable levels. Morgan Stanley’s Ruchir Sharma sums up some of these reasons in a WSJ op-ed, citing a BIS paper by Mathias Drehmann and Mikael Juselius which finds that if the private debt-to-GDP ratio increases by 6 per cent or more above its 15-year average, that is a “very strong indication that a crisis may be imminent”.

The risks are huge. These investment properties and their derivative financial products make up the life savings of many Chinese people. If the credit growth contracts, what happens to the asset values?

More than a decade ago, the Dutch central bank recognized the dangers of this euphoria, but its warnings went unheeded. Only last year did the new government, under conservative-liberal Prime Minister Mark Rutte, amend the generous tax loopholes, which gradually began to expire in January. But now it's almost too late. No nation in the euro zone is as deeply in debt as the Netherlands, where banks have a total of about €650 billion in mortgage loans on their books.

Consumer debt amounts to about 250 percent of available income. By comparison, in 2011 even the Spaniards only reached a debt ratio of 125 percent.

New Zealand's household debt to disposable income ratio is around 145%.

8. 'The Fed's nuclear reactor' - The CFA Institute reports that hedge fund manager James G Rickards is worried about the Fed's efforts to 'tweak' the economy. HT Nikki

”The Fed thinks they are playing with a thermostat,” Rickards said. “They think, ‘If the economy is too cool, you dial it up a little bit. If the economy is too hot, you dial it back down. It’s linear, it’s reversible, it’s all good. Everything is under control.’”

But in reality, he continued, “capital markets and financial markets are complex systems, which respond and correspond to complex dynamics, including critical state dynamics.” The metaphor is not in fact a thermostat, Rickards said. It is a nuclear power plant: “You can dial a nuclear power plant up and down,” he said, “but you had better get it right. Because if you get it wrong, you will cause a catastrophic meltdown, and it is an irreversible process. There’s no such thing as a melt-up; if you destroy it, it stays destroyed.”

Rickards believes the Fed, its staff, and its economists “misapprehend the statistical probabilities of risk” because they don’t understand how risk works in complex systems. “They are using Keynesianism, they are using monetarism, they are using modern financial economics,” he said. “Most of this stuff is deeply flawed, if not completely junk science.” He believes the right way to think about risk is by using complexity theory. “When you start looking at things that way, you will see that this is a system that is bordering on the critical state and potentially prone to collapse.”

9. Will Obama be remembered for widening inequality? - The FT's Edward Luce thinks so.

In June the US will enter its fifth year of post-financial crisis recovery. However, each year has brought slightly lower middle-class incomes than the last. According to data from Sentier Research, US median household income dropped by 1.1 per cent from January to February, to $51,404. It is now 5.6 per cent below where it was in June 2009, when the recovery began ($54,437). And it is 8.9 per cent below where it was at the start of the century. At this rate – and for all Mr Obama’s efforts – the middle class could suffer a double-digit fall during his presidency.

It is a different story at the top. According to David Cay Johnston of Syracuse University, the wealthiest 10 per cent of Americans have taken 149 per cent of the growth since 2009 (the bottom 90 per cent have seen their incomes shrink). The top 1 per cent – those earning $366,623 or more – have taken 81 per cent of the fruits of the recovery. And the top one in 1,000 – those starting at $7.97m a year – hogged an astonishing 39 per cent of the growth. That means America’s top 15,837 households have gained almost as much as the remaining 158.4m.

10. Totally Jon Stewart on the 'Nuke Kid on the Block'

It seems North Korea wants to blow up Austin Texas.

Hugh Pavletich is going to be very unhappy... ;)

And Part 2. I laughed a lot.

42 Comments

So my new LED lights have dropped my power bill heaps...wonder what LED will do to power demand across the country over the next 5 years!

#7 is a great example of unintended consequences....

The Dutch Govt. allowing the interest payments of home mortgages to be tax deductable.. ( thou they do offset that somewhat with some kind of capital yield tax..)...

U can see how this sort of stuff gets capitalised into the Asset values...

A few people here are crying out for lower interest rates... but what would happen..??

Would people prudently pay off thier loans... or would the lower interest rates simply get capitalized into higher asset prices.... creating a bigger problem down the road..??

Kimy...

I hear what u are saying but I disagree...

Firstly..I'd suggest that the current generation of home buyers do not expect to pay much of their mortgage off... They expect Capital Gains to be their saving grace when they retire...........( I'm guessing that u are in ur 50s' ... as I am )

Secondly... I don't follow the logic that high indebtedness comes from high interest rates.??.. Sure.. I do undertand the issue of interest rates affecting cashflow...as does any increase in input costs.

The relationship I'm talking about is between interest rates and Capital values...

This is what has lead us down the road of Financialization..... over the last 40 yrs.

Buffet has a great article about mkts and interest rates....and how interest rates capitalize into asset values.

http://www.jeffreyluke.com/Financial/Mr_Buffett_on_the_Stock_Market.html

Kimy I hope you think carefully about what I am going to say to you as you are one step short of fully understanding the problem. I can appreciate what you are trying to do as I have been in that mindset myself.

You identify hight interest rates as a problem but don't grasp that interest is the entirety of the problem. The underlying principle is unearned income. The Bank, or bank shareholders, are taking a portion of the wealth you create from you.

What you are trying to do with your investment properties is exactly the same, you want to earn income from your tennants without actually producing anything for that money. You think high interest rates are destructive, well so is landlording.

Kimy - we've had that debate here over quite a time, but here's the recap:

Trading quickly turned to a proxy - coin, metals, whatever - to take cognisance of the diffo between a needle and a chariot.

As populations - and consumption - grew, the system of proxy-trading was inevitably growth-based. That worked, while the planet could supply resources, particularly energy resources (without which nothing else gets gotten) in a growing manner.

Growth is exponential, and is expressed in terms of doubling-time. With finite resources, the last doubling-time is from 50% gone, to 'all gone'. Nobody sees it coming.

At the 50% point, the growth-requiring proxy system set up in the left-hand half of the Gaussian (profit, rents, interest, dividends, c/gains) cannot be underwritten, in real terms.

Which leaves the options of default(s), Cyprus(s), or inflation (proxy devaluation via the bidding war inevitable in the face of ultimate scarcity. (Econ 101 doesn't do ultimate scarcity, it does 'alternatives at a certain cost', which with finite resources, is guaranteed to not happen at some point.

You are piggy-backing on your tenant's income, presuming they are doing something real. If - like you - they are not (journalist, lawyer, 'pollie, there's a lot of them....) then they in turn are piggy-backing.

The SHTF after peak oil in 2005 - and the already-happening artificial 'wealth' increase (increase in 'values' of existing housing, mainly) which after then could no-way be maintained. That is not resolved, yet, and I'm not sure it can be. You may well get to spend your rent, on a provcessed part of the planet, but at the expense of someone else.

With respect, most folk like you didn't 'work hard' - they had fossil fuels working hard for them

Even a simple man should be able to understand this http://www.youtube.com/watch?v=F-QA2rkpBSY

As I said Kimy try a little harder to understand what exactly interest is. A claim on the future ? That required exponential growth because every simply mind like you thinks someone else can pay. Watch the video series (1-8) and then come back and tell us how you think it can continue.

Iconoclast has it right below in that the bank is just an intermediary. You as a landlord are simply an intermidiary as well. Once you have outlived your usefullness then you will be expendable.

Edit because PDK did a better job :-)

kimy says:- I am just using the banks money to make money

No you are not

The bank is merely the intermediary

It is lending you money deposited by savers

what is your gearing? your total borrowing?

You must be leveraged up over $5 million

Nothing worse than having your circumstances require you to deny reality.

I feel sorry for you, but I don't really. All those pathetic middle-classers who got on the band-wagon, levered up a set of renters, expected to live off others thereafter. Expected to live off future others, too, given that the level of existence expected, is depleting any future resource inheritance.

The joke is the "I would have made 5 million". Underwriten by what? The buildings hadn't changed. Neither had the amount of planet available for sale/extraction. That meant you either expected to outbid others (presumably due to your smartness?) or you aren't capable of working it out.

That cumulative debt can't be underwritten now - I was telling the Dunedin City Council their Stadium debt wasn't underwriteable, back in '05. Good luck when the music stops. Don't say you weren't told.

"when the music stops" The problem is PDK when the music stops the likes of kimy are quickly bankrupted and living either under a bridge or in Housing NZ accomodation. The move then is to look for someone(s) else to pay. That leaves ppl that are still standing, you and probably I. The councils wont have many rate payers so will lookfor funds, the Govn's tax take will be down so will look for new taxes. The bank's wil be in a bad way so depositors ie OAPs who have saved will be decimated.

I really couldnt care less about kimy's downfall its just that it will impact me (and the far less fortunate) despite my best efforts for it not to. PS. There is some suggestion that Victorian debtors prisons will make a return.

regards

Interest on $2,600,000 + insurance + rates makes that almost marginal

Bollard's 50 basis points reduction in the OCR due to the Christchurch Quakes was a christmas present to you .. and you still want more?

No you are not

The bank is merely the intermediary

It is lending you money deposited by savers

Actually it's far more correct the way kimy put it. Also under law when you deposit money at a bank the ownership transfers to the bank (and presumably you receive a balancing deposit liability of the bank). How they choose to use it or, who they decide to lend it to is basically the banks decision from there. If banking actually transfered money from lender to borrower then there wouldn't be bubbles, or not nearly on the same scale, as you would run out of lenders. As it stands however, optimistic leverage feeds into the overpricing, creating a positive feedback loop in the economy.

Actually this fact of banking is quite obvious, because nobody loses access to any of their deposits when a bank lends money. The increased balance of resulting spending power obviously means something has been created during the lending process. The thing created is the banks money (called bank credit).

"...and that was when I had to borrow more money to keep my investment properties."

So, kimy, you borrowed more money to meet the interest bill on already borrowed money?

Did you not instead consider selling down some properties - collecting the tax free capital gain on them and then use that earned income to meet the interest bill on the balance of your properties?

Oh dear. You have got to be kidding.

Well here's my thoughts for what it's worth. When the banks find you paying the mortgage with borrowings - which it seems you have already done before, and admitting that your business is presently marginal - we can only assume you plan to do so again with the O/D that you have secured for just that purpose - they will move in - and it won't be pretty..

http://www.stuff.co.nz/national/8452494/Evicted-Taranaki-farmer-vows-to-fight

Note the last line of that article with extreme caution. All the equity in the world won't save you when your income doesn't cover the repayments on your loans. Remember - it's their money you are playing with and they won't want you paying them what you owe them with their money.

Deleverage - now. It's a good time for it. Prices are good - and it seems the market is buoyant as well. What can be wrong with owning your own assets in full? I reckon the only way to ride out what's coming is to own everything you have outright. If you are paying off no principle and no interest - your income is yours - as is your future. JMTCW.

Own you own assets in full. Radical thinking in today's world - I realise :-).

Well yes I've heard it all before in theory. From a girlfriend (a valuer) doing all just that in Phoenix Arizona just prior to the US property crisis. Problem was when crisis hit - the pre-approved O/D (that which was as yet not drawn down) was withdrawn - no notice. What did she do - well tried to liquidate, just like every other man and his dog all at the same time. She also lost her job as a valuer - as did most of her tenants. All within about a month or two. Tried harder to liquidate (i.e. dropped prices - sold nothing), first missed mortgage payment - well, the beginning of the end, although it took about a year for the bank to finally wind her up, selling her own place of residence last. She is no longer of this earth - a choice she made herself.

We should note that mortgage rates fell substantially prior to 2009, so if you were paying 10% around 2011 then you probably fixed with quite poor timing.

http://www.rbnz.govt.nz/keygraphs/Fig3.html

We should also note the OCR, even at 8%, proved a fairly weak deterrent to Kimys high wire act in the housing market. This should make anybody sceptical of the reserve banks ability to prevent a housing bubble. Paying the mortgage using an overdraft facility is basic ponzi behaviour, and the reverse is actually the financially prudent course. Actually I am mildly surprised this isn't a breach of mortgage contract.

http://www.rbnz.govt.nz/keygraphs/Fig7.html

Sounds like it is not only amazing how rapid the recovery has been, but quite fortunate for kimys sake as well...

You appear to have some pretty serious miss apprehensions about what kind of gamble you are engaging in. Good luck with that, your likely to need it.

Yes, let's drop interest rates so Kimy can make bigger profits at the expense of his renters and future purchasers.

Its a catch22, a lower OCR helps to stop our economy falling into a recession with the resulting job losses and lower Govn tax take....So raise rates and maybe impact kimy a bit and screw everything else....

regards

Time for the RBNZ to hike interest rates again then Kimy.

cheers Bernard

;)

On the other hand kimy...higher rates on savings would encourage saving and lead to sufficient kiwi capital to provide the funds that are otherwise supplied by Tokyo Rose et al....and discourage those who borrow the cheap credit created by the banks to prop up the bank property bubble....think about it Kimy.

Yes. and if the cash flow is nothing but credit, then burning the flood would be best...!

Kimy you have Beijing fever...an economy that encourages saving and discourages debt will always be better in the long term...they do exist in the world economy...why must we always do what the banking elite demand....why!

No good reason why the NZ govt cannot impose rules to control property speculation by foreigners wanting to stash their loot here....and Key's grasp for said wealth would die away if we had policies that encouraged saving at home!

mist, are you a wealthy person yet?

I don't need any further example case studies. I'm talking the real life experiences of the many folks I know and have known who have got themselves into a pickle over borrowing. Some pickles ending more tragically than others.

mist - you don't need a million dollar loan from the bank - all you need to do (according to you) is borrow $10 bucks from a friend - and repeat the above exercise less than 10 times - and you have your own million in earned income.

So why haven't you done it?

It's funny as we are talking at cross purposes. You are telling us all how to get rich from a not rich position and I'm telling us all how not to go broke from a not broke position. There's some irony in that.

And sometimes the stupid get lucky

Good for you Kimy...easy task now for IRD to track your income( search all sales 570sqm in that zone!)...and so I hope you declare that gain as income!

From here the IRD can demand you provide income details going back a decade or more! oops.

Good luck with that Kimy!

Kimy... I would qualify your statement about... " time in the mkt...not about timing ".

Kates' example about her friend in Phoenix, Arizona ...surely... should make one step back and ponder...???

My on view is that timing is everything ... in regards to risk.

Extrapolating the past to predict the future is dubious at best. ( time in the mkt )

A more moderate view might be that .... the greater the leverage that one uses... then the more critical the timing is.

Plenty of people got caught out with commercial Real Estate in the 1980s,

One of my friends father lost all his industrial buildings in the lates 80s' because the Bank he was with called in the mortgages... He said his buildings were tenanted and he was meeting his mortage payments.... so go figure..

My feeling is that when banks are cornered....and need to recapitalize... they are like the walking dead... ( unemotional and ruthless ).

So... because the future is uncertain... we roll the dice and take our chances..

We are a funny lot. Never happy unless we have something to worry about. We have been lying awake at night for years wondering how we would find enough gererating resources to keep the lights on and now we are desperately worried about a huge surplus of renewable energy.

You would think that, if we have excess capacity and the marginal cost of production ( if not transmission ) is practically zero, in a competitive market prices for electricity would fall and demand would rise. That would be a good thing would it not? As long as the price received by the generators is above the price paid by Rio Tinto both consumers and the generators overall would be better off. Not much fun if you work at Tiwai point but there should be a net economic benefit to the country.

There would be winners and losers among the power companies as Meridian's average price would rise even if power prices fell overall, while the others would face a reduction. No new investment in generating capacity for a long time though so if prices do now recognise the marginal production cost from proposed new capacity they can forget all that. All those campaigners against wind farms can relax as well.

Really good Jon Stewart today....... have you ever seen " Team America, world police"...?

A must see if you want to follow the North Korean historical from ILL before UUN.....

....funny as they come....

#8 is essentially a re-stating of NNT's 'black swan', and doesn't add much to the debate. Because core economic activity is never 'destroyed' - just like energy/mass equivalence, it changes form.

A melt-down in the formal economy is feasible, but as humans have four irreducible core needs - food, shelter, security and transport - these needs would transfer to other 'black' networks outside the green (!) glowing heap of the formal, 'white' cash economy:

- tribe, criminal gang, locality, kin and other social networks.

- re-emergence of mediaeval city-states, feudalism, and other groupings

- re-emergence of subsistence farming and other forms of activity which tend not to generate reliable surplusses

- etc.

History (particluarly mediaeval history) is a useful guide to all this: as Bill Bryson points out in 'At Home', the comfort we currently enjoy is an extremely recent (and if one listens hard to PDK and others), not sustainable at current levels - condition.

Sure we have physical comforts Waymad but somewhere along the way we traded this for community, or emotional comfort. Physycally rich but a phychological desert. I think what you predict is on the money but the time span might be a generation or so.

#2 data centres in Southland...

Sounds like a bad idea to me. People want their data center to be 'close' by with fast links. We are neither close by, nor are our international links fast. Face it, we're at the end of the world. We could make use of that fact however. We could promote NZ as a place to store back-ups of your data. Might catch on with the (growing) number of 'doomsday preppers' out there.

Bit late I'm afraid

Google and Facebook are moving their data farms to Iceland

Mainly for the cooling costs which are 30% of total energy consumed

UK university currently commericalising a fluid coolant that is non-conductive for data centres

Haven't you seen a PC filled wil oil? The look pretty cool if done with some neon lighting :-)

I also think Iceland has an excess of geo-thermal generation (so I assume kwh is very low) as well as low air temp.

regards

How quickly things change. In 2006, just before the GFC, Google commenced a massive program of decentralising its data centres to in-country locations to improve SERP speeds

AE on the EU,

Over the past week, Europe, or rather the present EU leadership, has done damage to itself it will never be able to repair.

It seems to escape everbody, but that doesn't make it any less true: people from Portugal to Spain to Italy to Greece to Cyprus and Ireland are worse off today than they were when they first adopted the euro. Moreover, their economies are all getting worse as we speak and projected to plunge further. The once highly touted blessings of the common currency are by now lost on most of southern Europe; for them, the euro has been a shortcut to disaster.

Until Cyprus, the EU had always maintained two prime objectives (and spent €5 trillion over 5 years to prove it): keeping all members in the eurozone, and guaranteeing all bank deposits under €100,000. These objectives exist from now on only in words. Brussels has threatened to both grab deposits of small savers and throw Cyprus out of the monetary union. Two watershed moments in one.

regards

http://theautomaticearth.com/Finance/the-lesson-from-cyprus-europe-is-p…

There are many mistakes in this article.

A sweeping claim is made that the populations of Portugal, Spain, Italy, Greece and Cyprus are worse off than when they each respectively joined the EU. But no evidence for such a sweeping claim is given. Not even of any kind.

It claims the EU's two primary objectives have always been keeping members and guarantee of bank deposits. Any quick skim of the Maastricht treaty wil show this to be utter bollocks.

It claims EU membership provided endless credit that created an illusion of wealth. Maybe true to some degree but endless credit was not a EU specific phenomenon as Ben Bernanke could well attest.

It claims EU financial policies are the cause of unemployment, high inflation, pension cuts and high personal, corporate and sovereign debt levels. It's quite incredible the power a monetary union has. He discounts all political policies, all fiscal control, all business decisions and all personal choices. He also ignores facts like Greek government fraud of its national accounts and the Cypriot economic model called Russian mafia money laundering.

He then sets out to criticise European politics as if a monetary union and national politics are one in the same thing.

Big on rant but barely rational

200 gigabytes of Britsh Virgin Island tax haven records leaked. Many political resignations expected worldwide.

http://www.guardian.co.uk/uk/2013/apr/03/offshore-secrets-offshore-tax-…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.