By Bernard Hickey

It is the great conundrum of New Zealand's investment scene and the great mystery of the Auckland economy.

Why has the median house price risen 25% in Auckland in the last two years to over NZ$620,000, yet the median weekly rent for a three bedroom rental has risen just 6% to NZ$550?

Why have rents not kept up with prices in a market that everyone from the Auckland Council to the Housing Minister and the Reserve Bank have said is short of housing supply and faces a migration boom?

The numbers look even more extreme going back to 2007. Auckland's median house price has risen 38% since then, while rents rose just 15%.

Surely the laws of supply and demand say rents should be rising at a much faster rate?

Rents and prices certainly are rising at similarly high rates in Christchurch, which does definitely face supply shortages and increasing demand from more workers receiving higher wages.

Why aren't landlords able to force through rent increases?

It's certainly not for lack of talking about it or a lack of reasons.

House prices have certainly risen, which means already low rental yields have fallen even further below alternative investment options such as bank term deposits. These bank deposit interest rates may feel very low at an average of 4.7% before tax, but they are up almost 0.5% since March and above the current implied rental yield before any expenses of 4.6% in Auckland.

Costs have risen too.

Advertised floating mortgage rates are up 0.75% to around 6.4% this year, although many rental property investors will have taken advantage of the cheap fixed mortgage deals being offered by banks able to borrow cheaply offshore and locally. Auckland's property rates have risen by a cumulative 38% in the first four years of the Auckland Super City and maintenance costs have risen 16%.

The Government's tax changes in 2010 also stopped landlords from claiming depreciation on their buildings.

Landlords have taken an enormous dollop of pain over the last couple of years. Therefore, there's no shortage of incentives to put up rents. Yet still, rents haven't risen very fast.

There is a very free and open market for rentals in Auckland with good information and little regulatory intervention gumming up the works so a market failure can't be blamed.

Essentially, rents are limited by the growth of tenant incomes.

Ultimately, rental property investors are not choosing to buy and hold these properties because they provide a regular after-tax yield that is superior to other investments of a similar risk. They are buying them for the expectation of exceptional and regular tax-free capital gains that can be earned from a highly leveraged investment.

They are taking advantage of the capital adequacy rules in banking systems globally that incentivise banks to lend against land and buildings.

And so far that strategy has worked spectacularly well.

It's also been affordable in the short term because interest rates have been historically low, and remain only just above those lows for landlords who have fixed below 6%.

The New Zealand Property Investors Federation this week even cited IRD figures showing landlords reported NZ$1.476 billion of taxable profits in the year to March 2013, while interest rates were at those record lows.

It all makes perfect sense while house prices keep rising at 10% plus per annum and interest rates stay below 6%. A rise in mortgage rates to over 8%, which the Reserve Bank is currently forecasting, would break the investment logic behind Auckland rental property, particularly when rents are only rising broadly in line with worker incomes.

The scale of the gap that has opened up between rents and house prices was reinforced this week with the release by Strategic Risk Analysis' Managing Director Rodney Dickens of his analysis of national rents and house prices.

It showed how a close relationship between the two broke completely around 2002 and they have diverged dramatically since then.

It has driven New Zealand's house prices 70% above their long term average relative to rents, which makes them the highest in the OECD relative to rents. That measure is a national one, so the Auckland one would be even more extreme.

So why would Auckland investors double down on property that is at least 70% over-valued at a time when interest rates are rising and rents are not even close to keeping up with rates and maintenance costs, let alone interest costs or any sort of comparable alternative?

The simple answer is because they can being given low fixed mortgage rates, and because they are second-guessing the powers-that-be, who have wrongly predicted much higher interest rates and subdued house price inflation for almost a decade.

Property investors have successfully bet that politicians will never impose a capital gains tax, that Auckland's NIMBY home owners and their captured councillors will never allow significant new housing supply, that migration will keep surging and that inflation will not rise sharply.

They could be right on all counts for some time to come. But for how long?

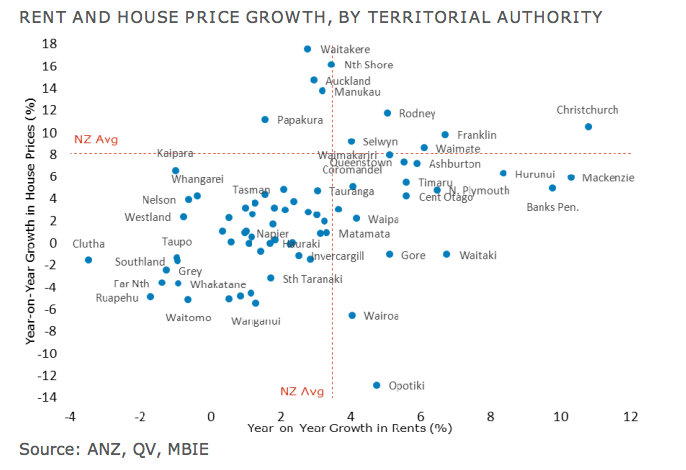

Here's an ANZ compiled chart showing rent and price growth over the last year by territorial authority.

-----------------------------------------------------------

A version of this article was first published in the Herald on Sunday. It is here with permission.

(Updated with SRA and ANZ charts)

47 Comments

.... Auckland house prices were less spectacularly overpriced back in 2007 when you made your 30 % crash prediction , Bernard ...

How much more will they fall now , having defied gravity for an extra 7 long years ...

.... when she pops , this bubble is gonna be ugly for the whole economy ....

It would be better to 'build out' of it now. When we have a housing supply shortage (in Christchurch at least) and we are at a point in the interest rate cycle that gives us room to drop interest rates for increased private sector investment and public debt funded infrastructure spending boom to support the economy if it gets really 'ugly'.

Well things will get a bit tougher and more expensive with more rules about contracts for builders coming in. Because we all know how good builders are for doing legal contracts, after that's why they studied Law in the first place....

Thanks Gummy for the reminder of my 2008 prediction. There's a few people who like to remind me of that. :)

Have a play with this Economist house price valuation tool, which includes house prices to incomes and rents and allows you to compare NZ with other countries over time. http://www.economist.com/blogs/dailychart/2011/11/global-house-prices

It shows NZ national house prices almost as over-valued relative to rents as they were in 2007 and the third most over-valued, just behind Hong Kong and Canada.

What the tool doesn't show is Auckland over-valuation relative to rents, which is what I'm talking about here. Auckland house prices have risen 30% from the 2007 peaks, while the national prices are up only 16%. Here's the REINZ-RBNZ HPI to show that http://www.interest.co.nz/charts/real-estate/house-price-index-reinz-rb…

cheers

Bernard

PS I haven't predicted the bubble will pop here. Sometimes bubbles keep growing, or governments intervene to ensure they don't pop. I'm just highlighting that there is a bubble and some risks rental property investors may not have thought about.

.... Bernard ; my dear old thing , there was nothing wrong with making your prediction that house prices were due to crash 30 % because of their gross overvaluation ....

It's just that alike the $ 17.50 wristwatch you bought from the Warehouse , you gotcha timing horribly wrong ...

All the best , big fella : the Gummster .

Gumster are you saying Bernard is a $17.50 Warehouse wristwatch?

That sounds way too expensive for a watch. I'd suggest a 30% lower price... ;)

cheers

Bernard

The problem is politics not economics. There is many policies that will help housing affordability. The good thing about a capital gains tax is that it is a message to property investors that society no longer considers their interests as more important than tenants and FHBs. Capital gains by itself will do little. But if it is part of a rebalancing between the different segments in society then it could be a turning point.

What would be helpful for NZ is if we got our own version of www.generationrent.org. Especially as the housing debate is much more advanced in NZ compared to the UK.

CGT has made not made homes more affordable in countries that have already had it in place for at least 10 years. A CGT would just make landlords hold onto homes even longer and cut supply to the market therefore actually increasing prices. CGT is not a magic bullet!

.... unless all assets are included in the CGT ( the private dwelling too ! ) , it's just creates more distortions in the market and in the tax system ...

CGT has been an abject failure in Australia ... raises bugger all tax for the government , annoys everyone contemplating selling a business property ... and hasn't stopped house prices from soaring to infinity & beyond in the slighest ...

.... accountants and tax planners love the CGT .... heaps more employment for them ...

Bernard's land tax idea ticks all the boxes / CGT ticks none of them ...

I don't really get what is so unique about land taxes. Isn't it just a variation of rates -being a tax on the land value rather than total property value. I think some Councils have this option -Waimakariri?

it's not unique, and you're right it IS just double taxation.

(rates used to be land based, then "to be fairer" they went to capital base. Same as any land tax that would be introduced

You are correct - the tax should be for all capital, not just land. Capital would have to include all sources - property, shares, bank deposits, company equity, cars, artwork etc. Depreciation should be allowed for reducing assets such as cars and for practical reasons anyting below a certain value would be exempt. See FIF rules for how this would work.

the tax shouldn't be for capital at all.

where does the capital come from? It is tax-paid income that is not consumed. Why should someone be paying extra taxes just because they don't consume their earnings? Is this some kind of Prudence punishment?

The only kind of capital related taxes are (1) for notable improvements taking the asset from one bracket to another, eg adding or removing a room; or as proportioning _minimum_ cost recovery for _minimum_ community assets. * anything more than minimum coomunity assets should be by voluntary specific donation only - you _really_ think the community needs a "X" then put -your- money where -your- mouth is and donate/fundraise it!!!

The LVR rules are seriously distorting the data with regard to rents versus house sale prices ie with around 20% less sales due to the lower value homes struggling to sell, as buyers cannot get together a 20% deposit, house prices appear to be increasing artificially? Imagine in Auckland if the same volume of sub $400,000 sales had taken place in the first half of 2014 that took place in the first half of 2013 - the median and average sale prices would be significantly lower - in fact we would probably see that house prices have gone nowhere or perhaps actually declined in Auckland over the last 12 months.

On the rental side the official rental figures only come from bonds recieved and that are reported to the Department of Building and Housing. As a result of the LVR rules more people are forced to stay put renting and the turnover of rentals has dropped but in the apartment rental area it has increased as more migrants enter NZ and take up apartment living as their first choice for accomodation.

A property manager that I know personally and who handles a reasonable number of homes says that in many instances rents have been increased by around 9% in the first half of 2014. So by way of example a home that was rented for $595 per week was increased to $645 per week. The bond held for that property is actually only $1,680 as it was originally rented for $560 per week three years ago. The same people still live there but there is no change in the reporting to DBH - ie the bond held reflects a rent of $560 but it is now $645. Had the property become vacant and rented to a new tenant then the new rental level would be recorded at DBH.

This is the case with many multiple property owning landlords where they have had the same tenant for 3 to 5 years and the rent has gradually been increased but the data is not captured anywhere.

As soon as the LVR rules are dropped we will see the median price drop as more sales will take place in the lower quartile level and rents will increase as more homes are re-rented as renters become buyers and higher bonds will then be recorded at the DBH.

Your thoughts Chris J and Big Daddy?

BigBlue, you’re 100% correct; I’ve made the same point on here several times recently and the ‘experts’ like Bernard are choosing to ignore. It shows the clear gap between people in the real world who are involved in the industry and speak from experience and the arm chair experts, many of whom don’t even live in Auckland let alone invest.

Bernard, care to comment why you are drawing conclusions from incomplete rental figures?

Bigblue, Big Daddy, Ollie Newland are you 'guys' worried that the powers that be will stop listening to you? That your politically provided vested interest empire will collaspe?

The whole of Bernards arguement is flawed from beginning to end because he is rushing to judgement far to early. .

It assumes that every landlord bought his property in the last twelve months paying top dollar and thereby needs to push up rents urgently.

The facts are that most rentals were bought in years gone by, and most Landlords don't feel as much urgency as may be imagined.

Furthermore rents can only be raised 6 monthly and often longer so there is a time lag that has to pass through first..

Most Landlords who have good tenants are loathe to increase rents by much in any event, as a modest rent 52 weeks a year is better than an empty rental for weeks on end because the rent is too high.

The flood of cheap shoebox apartments hasnt helped either.

But rents are rising at a gentle pace, especialy in the main centres and will continue to rise as interest rates rise and other costs bite e.g. insurance rates etc.

Patience Bernard.

It won't be that long before the headlines will be screaming that landlords are ripping off tenants especially if the Leftie Loonies try to bring in a CGT or other measures to kick investors in the backside and curry favour with the unwashed masses.

I've got scores of tenancies still let well below market because the tenants are clean, reliable, honest and decent people and that's worth more than money in the bank.

This is proof of that you are speculating on capital gains. An investor would look at the return available on their capital and re-allocate accordingly. Just because I bought a share 10 years ago and the dividends it is generating now are 20% of the initial capital invested, it is not a good investment if the dividend to current price (yield) is 2%. I would be better off selling that share and re-investing the money into another one that yields greater than 2%.

You are incorrect.

Not every investor needs to squueze every cent out of every deal.

If that were the case, there would be no slow blue (the steady blue chip stocks, which just kick out a reliable revenue each year but have no intention of being shooting stars.)

The properties held by big daddy are making solid reliable returns, and as he has mentioned, they have low risk tenants in place. The low risk tenant is a godsend, and he doesn't need to make enough to repair damages, cover lawyer fees, store against downtime and cleaning. That tenant is being recognised as no trouble so why not be no trouble to the tenant?

the image of the greedy landlord squeezing whatever the market can bear out of their tenants is sour grapes and deliberate emotive stirring. Yes there are some insecure landlords who make it rough on people, just as there are genuine lazy and negligent landlords who are a menace, but many landlords just want happy considerate tenants and to offer a fair service at a fair price.

Golly gosh, we can't have the loony left skewing the housing market in favour of home owner-occupiers, now, can we?

Or maybe we can

When house prices get irrational blame the fhbs or owner occupiers upgrading. They don't care about yield. They care about missing out and having to pay 100k more in 12 months time.

Specifically, they care that their peers are getting 100k cap gains and they are missing out and it kills them. Emotion is always to blame for irrational market behaviour.

I don't know a single investor who's been buying auckland property to rent out. It's about 15k a year gauranteed loss buying to rent and there is only so many of those properties an investor can buy before they run out of cashflow to keep up with interest payments.

We will see a tipping point soon when the risk (certain loss of 15k a year in extra costs by owning, plus maintenance rates etc) exceeds reward (60kish p.a based on last 12 months, but an actuary/accountant would not be using this figure for future projections, and if prices flatline for 10 years then that's 150k+ loss per property based on the neg geared nature).

Actually Simon, I suggest to you that fhb's are so keen to get into house ownership as all they can see otherwise is upwards of $500 a week disappearing down a hole never to be seen again, paying off someone else's mortgage.

Yeah that's the common story exchanged around bbq's by the financially illiterate. Often just before they mention house prices doubling every 7 years, and asain buyers buying up N.Z.

You can see $500 a week down a hole in rent, or 700-800 down a hole to the bank, council, local tradies in interest payments, rates, insurance and maintenance.

If you read my above post, the 'money down the hole' when buying exceeds the money down the hole when renting the same property. Capital gains are the only reason to take the gamble and buy in auckland. And looks that that is now over.

Certainly make interesting headlines in 6 months time when the recent interest rate rises and further expected rate rises start to impact on the highly indebtness property speculators.

When the cheap money is no longer around and the party is over, wait for the hangover to kick in.

NZ has become a play ground for speculators in the property market and currency market.

Sale prices attributing to the low volumes and higher pricing from the LVR last year make the median price look actually higher than they should be.

Let's put to bed this argument that the new bonds are not indicative of the overall market. Just like house sale prices, the market is set at the margin by a small percentage of sales/rentals. The sampling of new rents is an accurate predictor of the current landscape just as the latest house sales are a predictor of house value.

Asking someone to count all the rents in progress in addition to the new is the same as asking someone to value every house in the country to work out the average house price. Note that when houses are valued en masse by the council to get CVs, the results are not very accurate due to the time taken to perform this anlysis - recent sales are a better predictor of house price. Same applies for recent rentals vs all rentals.

The tenancy turnover rate is higher than the house sale turnover rate (simply put tenants tend to be involved with a property for shorter periods than owners or investors) so, if anything, the rental figures are more accurate.

No.

To use your example, all house sales are included in the REINZ, QV, etc stats, every single sale giving accurate data. The DBH figures do not include all new rents and specifically exclude increases, which skews the data and makes any conclusions based on the data meaningless.

And your comment regarding timing is also wrong, sales are reported the day they happen, most tenancies are fixed for 12 months so there is a, up to, 12 month delay for rents to catch up to prices.

Couple of questions Bernard

IRD figures show landlords reported NZ$1.476 billion of taxable profits in the year to March 2013

That NZ $1.476 billion is a meaningless number unless it is accompanied by comparative data for previous years

What it does mean is that property owners have either moved into profit, or increased their profits, and/or didn't pass on the savings in interest rate reductions

You need to categorise between commercial and residential numbers

and

With the numbers of people receiving Rental Assistance is it possible WINZ is acting as a brake on base-load residential rent increases?

Is there anyone here who is familiar with WINZ who can shed some light on whether WINZ just ticks-off on rent increases and ups the rent assistance when the landlord ups the rent?

I can report that an absentee landlord of a suburban Wellington property recently dropped the weekly rent from $440 to $350.

The tenants are six state dependent refugees who were considering seeking cheaper alternative accommodation given the imminent departure of an adult member of the group wishing to strike out on his own.

The remaining five members must face the prospect of extending the lease for another six months since cheaper state alternatives are not readily available for larger groups.

Please note

$1.476 billion are "net profits" after deducting interest and expenses

If the IRD can produce those figures it can also produce

(a) Gross rentals - residential - only then you will see if they are rising or flat-lining

(b) Gross rentals - commercial

(c) Gross interest cost in arriving at Net Profits

For each of the past 5 years

Bernard is forcasting that the property market will soon be:

"bursting in landlords' faces" which is simply a crude attempt to grab a head line.He has previously forecast a "burst" and drop in values by 30% and was wrong then and he is wrong now.

Sooner or later there will be a correction and levelling off, but barring some catastophic event that is all that will happen.

In the meantime rents will gently rise to meet the new values no matter what.

It should also be noted that Olly Newland wrote his best seller "The Day The Bubble Bursts" in 2004 and he was much closer to the mark then Bernard or anyone else ever was.

If you bothered....actually Im pretty sure BH said 30% drop as a long term trend due to demographics etc and that was 2009? What BH didnt allow for (and doesnt ever seem to have acknowldeged) was the effect of peak oil which is at most 5 years away.

Persnally with NZ being in a x2 bubble with BAU let alone the effect mentioned above I think we'll see a 60~75% correction...

That frankly is an OBR event, and why pray do you think it was brought in if there wasnt a substantial chance of it being needed?

The unwinding of this massive debt will be painful. It will take 20~30 years to dig out of, a 2nd Great(est) Depression. I fully expect a lot of private and probably Govn (around teh world) default and a debt jubilee, there is no other option frankly IMHO.

regards

Bernard Hickey

" They are buying them for the expectation of exceptional and regular tax-free capital gains that can be earned from a highly leveraged investment."

That is absolute friggin bollocks.

IF they are buying in "expectation of exceptional and regular capital gains" where are they going to get those capital gains? Because if they have sold to realise those capital gains, THEN the 'expectation' means they are liable for tax on the profit. ie clearly not "tax-free".

YOU KNOW DAMN WELL THAT'S THE LAW. Report properly and quit the trolling crap.

cowboy.

How prevalent is it that that law is being ignored which is not being picked up, do you think ?

Evaded....and I think there is a % there....

Bring on a Land tax and dump GST...

regards

who is ignoring it?

not me.

IRD? then they need to personally be responsible for the "evasion" they are causing.

rorting people who are not liable for the charge/tax is not a valid way of doing their job correctly.

There is the law and there is tax evasion of it as Im sure you well know.

Also the IRD cannot read your mind, and hopefully isnt allowed to bug your house (assuming you talk to your wife about such things like I do). There is also no compulsion/need to sell short term especially if a renter is picking up the costs.

Think its not going on?

regards

IRD can seize any financial records without a warrant to do so. They can enter any area if they believe financial records are being held there. The only people with more power in this regard are NZ customs.

That IRD don't police this is the "slippery path" I referred to the other day where since I'm not affected I can't take IRD to court for their behaviour or get my MP to act. By not doing their job properly, the IRD can then complain it's "too hard" (using your 5yr old whiny voice for that one), and that new laws need to implimented that "catch all evaders". They also tend to let slip hints that such shortcuts are occurring. This way they can claim it's a widespread problem,. and that "comprehensive" taxation needs to be in place "to be fair" across the whole of the market. Then flash some fistfuls of promised cash at the MP's.

Then the law will change and everyone will be taxed - even though legally, at the moment, many of those people _don't_ owe taxes.

But if it was properly persued then IRD won't get the tax take for all those homeowners, inherited properties, and rentals that were thought to be permanent (eg retirement, for the kids to rent out or sell).

I have two property "bought with intent to sell at a profit". this of course, means I plan never to sell them... Others are all ones I've personally lived in for some time.

I read somewhere that 47% of New Zealand families DONT own their own home.

Now I dont know whther that statistic is correct , but , thats nealry half of the population who rent their houses / units / apartments / cottages , etc

If rents do start going up , its a real problem for tenants , and Capital Gains tax is not going to help anyone , least of all the tenants as landlords will be even less inclined to want to crystlaise the gains , and pay the tax when the dont have to.

For all those enthusiasts for a CGT may I wearily recycle (no, wait, that sounds Too Green) Repeat my CGT mantra and let y'all chew over its wide-ranging effects:

- It will have to be on all assets including the Fambly Mansion or else fails to capture the tax base needed for an effective revenue stream (the essence of GM's Big Kahuna)

- It will have to be on a Unrealised basis, as waiting for a Trust, Granny or the local Property Company to expire/go bust/liquidate and thus the CG to crystallise/Realise, is far too long for yer typical revenue-strapped Gubmint to wait: better to deem the value every tax year, and tax 'er there and then

- It will lead to a lotta Valuation headaches, as some capital ( property, land, vehicles, factory plant, herds of coos and sheeps) has an easily ascertained value and an active market. But try that with Brands, Software, a Stamp Collection or a New Patent.

- It will lead to a lotta Corruption, as Valuations and their Valuers can be - shall we say - Persuaded to lean towards one figure or another, by the application of Cash, Honey-pots, various Chemicals or good old-fashioned Violence. And of course, the Gubmint Officials who have to approve the Deemed Value will prove ultimately to be similarly Malleable. For a working example, see India.

Devil's in the Details, CGT afficionados......

The CGT is about expanding the tax base....taxing weath as well as income.

The property discussion is a mere somkescreen.

Even though there are too many investors who are buying for tax free capital gains (even though they will not admit it)

How many more Villas on 1,000m2 in Epsom can you build ?

Do these not increase in price ?

Fortunately, that idea is as much make believe as numerous "facts and figures" as you have quoted to this site recently.

Excellent comment.

The majority of the Tax Working Group recommended a low-rate land tax and/or a risk-free rate of return for investment properties back in 2010 - instead of a CGT, which only a minority of TWG members supported.

FYI I've updated with the SRA chart and with another useful chart at the bottom from ANZ showing rent and house price growth by terrritorial authority over the last year.

cheers

Bernard

While I'd love to get in the market once sanity returns - sitting on a chunk of cash, just not enough, sadly - my rent is lower than it was in 2007, and the recent "increase" was $5 p.w.

Guess I'll have to forgo a happy hour tower at the pub to pay for that one.

Good tenants hard to find? ;)

So, not too fussed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.