Here's my Top 10 items from around the Internet over the last week or so. As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read is 9 on Macquarie Private Wealth. No wonder it is the millionaires factory...and not in a good way for investors.

1. A 50 year bond? - Barry Ritholz makes the case in this Bloomberg piece for a 50 year US Treasury bond.

Apparently there's huge demand and it would make sense in a structurally lower inflation environment. The ultimate in extending (and pretending?).

It would certainly make sense for New Zealand to have longer bonds than it currently does.

It would even help create a base for much longer term mortgages.

That's just what we need. Just imagine being able to fix for 50 years at 5%. That would generate another leg up in property prices...

It all makes sense in a world of lengthening life spans and inter-generational debt transfers...

2. Imputation (dis)credit? - Alan Kohler asks in this provocative Business Spectator piece if Australia's dividend imputation system (which stops double taxation of dividends) is actually distorting Australia's business investment in a way that increases dividend payout ratios and reduces retained earnings and reinvestment.

The same would apply to New Zealand of course. The chart is an eye-opener.

In 1987, dividend imputation was introduced to remove the double taxation of dividends -- one of the many great reforms during the Hawke/Keating era.

Coincidence? Definitely not. Dividend imputation lowered the cost of equity for Australian companies and resulted in a structural decline in gearing, but it has also resulted in sustained pressure on companies to increase their dividend payout ratios and not retain earnings.

The result is chronic under-investment by companies outside the mining industry, and especially in manufacturing.

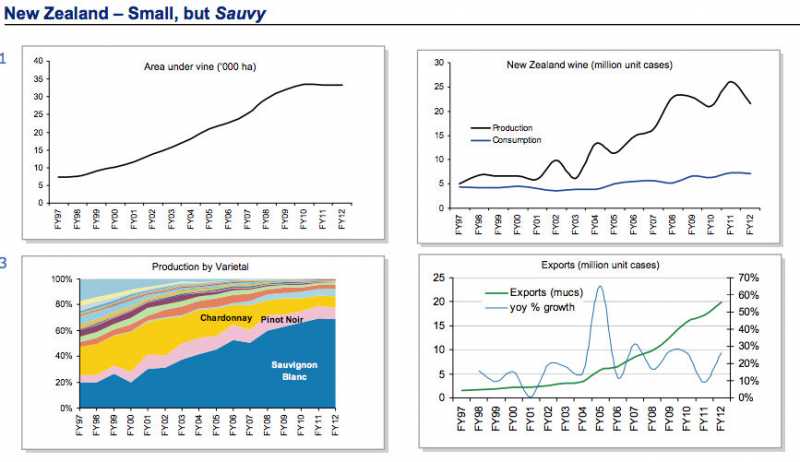

3. Small but 'sauvy' - This Morgan Stanely analysis (via Reuters) on New Zealand's wine industry (Pages 70/71) includes a useful analysis and set of charts. It concludes a global wine shortage is coming.

Things look pretty rosé in the long run. Couldn't resist...

New Zealand relies on three key export markets: Australia, The UK and The US. Export prices for NZ wine are high and rising, almost double Australia’s pricing and second only to France on the global stage. Imports have steadily declined since 2003 from all regions except Australia. Stable domestic consumption, a rebound in export demand, combined with a fall in production has seen NZ move into an undersupply situation for the first time in more than 15 years.

5. Some concrete facts - Bill Gates makes some interesting points about the role of concrete in the modern global economy. He refers to a book by Vaclav Smil.

He argues that the most important man-made material is concrete, both in terms of the amount we produce each year and the total mass we’ve laid down. Concrete is the foundation (literally) for the massive expansion of urban areas of the past several decades, which has been a big factor in cutting the rate of extreme poverty in half since 1990.

In 1950, the world made roughly as much steel as cement (a key ingredient in concrete); by 2010, steel production had grown by a factor of 8, but cement had gone up by a factor of 25

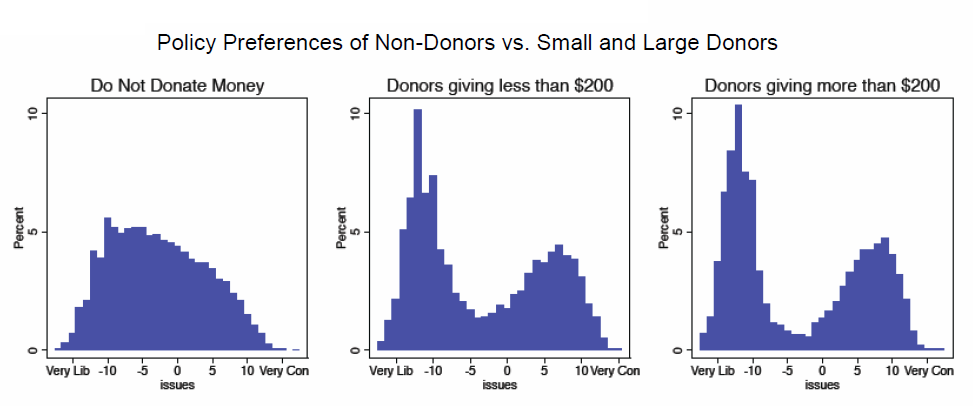

6. How big money makes politics more extreme - Vox does a nice job here of explaining why the advent of really big money in US politics has made politics there more polarised and dysfunctional.

The chart comes from Ray LaRaja and Brian Schnaffer and it shows what most people intuitively know: the small minority of people who fund American politics are much, much more politically polarized than the vast majority of people who don't contribute to campaigns.

Which makes sense. You're a lot likelier to contribute to a political campaign if you think the fate of the nation rests of your guys defeating the other guys. You're a lot less likely to contribute to political campaigns if you don't much care which party wins.

But what happens next makes sense, too: politicians have to appeal to the people who fund their campaigns. The people who fund their campaigns really believe the other party is terrible. And so spending a lot of time working across the aisle or questioning your party's political strategy is not going to make your donors very happy.

There is evidence enough in this book for a pretty withering attack on Malthusianism, if not on Malthus. Mayhew, however, prefers the role of calm and evenhanded guide. At the end he’s even hinting that today’s Malthusian prophets of environmental doom are on to something.

They may be: Just because Malthus was wrong about nature’s limits in 1798 doesn’t prove we won’t ever hit those limits. Past performance is no guarantee of future results. Still, you’d think it would put more of a damper on people’s Malthusiasm

8. Are they really worth it? - Former Clinton Labor Secretary Robert Reich has written a good piece comparing the worth of hedge fund managers and kindergarten teachers. He makes some good points and has an intuitively satisfying recommendation.

One study found that children with outstanding kindergarten teachers are more likely to go to college and less likely to become single parents than a random set of children similar to them in every way other than being assigned a superb teacher.

At the other extreme are hedge-fund and private-equity managers, investment bankers, corporate lawyers, management consultants, high-frequency traders, and top Washington lobbyists.

They’re getting paid vast sums for their labors. Yet it seems doubtful that society is really that much better off because of what they do. They don’t even build the economy.

Most financiers, corporate lawyers, lobbyists, and management consultants are competing with other financiers, lawyers, lobbyists, and management consultants in zero-sum games that take money out of one set of pockets and put it into another. They’re paid gigantic amounts because winning these games can generate far bigger sums, while losing them can be extremely costly.

Graduates of Harvard and other Ivy League universities are also more likely to enter finance and consulting than any other career.

The hefty endowments of such elite institutions are swollen with tax-subsidized donations from wealthy alumni, many of whom are seeking to guarantee their own kids’ admissions so they too can become enormously rich financiers and management consultants. But I can think of a better way for taxpayers to subsidize occupations with more social merit: Forgive the student debts of graduates who choose social work, child care,elder care, nursing, and teaching.

9. The silver doughnut - This SMH piece from Adele Ferguson and Ben Butler is a must-read for anyone considering investing with Macquarie Private Wealth. It's also a cautionary tale about the dark side of Australia's A$1.7 trillion compulsory pension money pit.

‘'We suffered every possible worse scenario imaginable,’’ he says. ‘‘We had a margin loan account and so got caught out with margin calls, and we were transferred into managed funds that were invested in a number of non-equity, derivatives-based, currency-exposed managed funds – the risk of which was not properly explained – and didn’t help us when the markets rebounded.’’

The low point of the disastrous investment advice was tipping $238,303 of the Wallers' money into a series of funds run by Australian group Basis Capital – funds that were, via a company in tax haven the Cayman Islands, pumped into one of the worst investments in the world: complex collateralised debt obligations issued by the financial wizards at Wall Street’s ‘‘vampire squid’’, Goldman Sachs.

Those CDOs included the notorious ‘‘Timberwolf’’, described by Goldman Sachs’ then-head of sales, Tom Montag, as ‘‘one shitty deal’’ in a June 22, 2007, email.

10. Totally John Oliver on Native Advertising. Juicy. Painful. Funny.

6 Comments

#6 Why do commentators always seem to believe that the vast majority of voters do not care who wins elections? They actually do care, as they know that they will be impacted by the outcomes, and broken promises. They also realise that because they are not wealthy, and therefore unable to contribute significantly, they are highly unlikely to be able to influence policy or law when there are really wealthy people buying influence! Lots of examples exist that demonstrates Governments the world over act in favour of a few, protect the power and priviledge of the rich while spinning what they are doing to the masses.

I think as long as the majority of ppl have skin in the game they accept.. When however we see a massive housing price collapse and I mean 60%+ losses I think there will be some changes, a debt jubilee is going to be one of them.

Which of course wipes out pensions etc.....the follow on effects are mind boggling and all bad.

regards

murray86 : The vast majority of voters are so apathetic they wouldn't bother to turn up to vote for a pay increase for fire-fighters even if their own arses were on fire !

#5 and concrete's CO2 footprint isnt so good. Invent a process there to save a decent % CO2 and we have a big win.

regards

#7 Its simple Math. Expotential growth does not fit on a finite planet. Malthus is correct the only Q is when.

Many seem to be gambling the final doubling time is a long way off, ie outside of their lifespan...not very likely, unless you are 70+

regards

"Expotential (sic) growth does not fit on a finite planet."

Soylent green....

Noaa on the oceans: "The ocean covers 71 percent of the Earth's surface and contains 97 percent of the planet's water, yet more than 95 percent of the underwater world remains unexplored."

IT, where the silicon usage sits at around 7.6 million tons/annum, will surely eat the finite planet up, because its the second most common element of the Earth's crust, which weighs in at 3 x 10^21kg. Oh, wait....

Well, there's a lot we clearly don't know. So we shouldn't assume.

A more nuanced view here....with some good thinking about the Future.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.