Today's Top 10 is a guest post from Martien Lubberink who is an Associate Professor in the School of Accounting and Commercial Law at Victoria University. He has worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide and for banks in Europe (Basel III and CRD IV respectively).

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

1) Empty shelves for Greece.

My previous Top 10 was about Greece, and boy, how have things changed for that country since then. In a truly surprising move shortly after my Top 10 post, Alexander Tsipras, the Greek Prime Minister at the time, called a snap referendum that upset Greece's creditors, who stood to lose about €340 billion. Chaos ensued. Greek banks imposed capital controls, the economy went into reverse. Tourism and international trade were badly affected, consumption dropped by 70%.

Eventually and after bitter negotiations, on July 13 an agreement was reached; and last week, the European Commission signed a new Memorandum of Understanding (MoU) with Greece. Greece will receive €86 billion in exchange for deep structural reforms. Despite a German flirt with the idea of a temporary exit, Greece and Europe have shown resilience. Greece is still in the eurozone (and out of the intensive care, again).

2) No fire Sales, promised.

European Commissioner Pierre Moscovici could not hide his enthusiasm for the new agreement. His recent blog post on the EC website shows 10 reasons why Greece's new programme is good news. But it is hard to suppress skepticism while reading Pierre Moscovici’s blog post. What, for example to make of the €50 bn privatisation programme, the cornerstone of the new programme? It will monetise valuable Greek assets to “make the economy more efficient and to reduce public debt.” Sure.

Close reading of the Eurogroup statement on the programme, however, show this disturbing line: which is basically the same as saying that there will be fire sales.

3) Your own holiday resort?

The current Greek privatisation programme offers 23 for-sale projects. Apart from the usual suspects - airports and public utilities - there is this luxurious resort: Astir Palace Vouliagmeni.

4) A Very Hungry Caterpillar.

The current set of 23 projects may not be enough, given that the previous programme realized only €7 bn. To satisfy the hungry creditors, Greece may have to add many more projects before it can turn into a beautiful butterfly again.

5) To bail-in or not to bail-in.

After the collapse of Lehman Brothers, world leaders promised to stop taxpayers coughing up the cost of bank failures. To do so, they proposed the introduction of bail-in regulations.

In theory, bail-in should work: a bank that is about to fail can save itself in an orderly fashion by writing down (bailing-in) claims of debtholders, creditors, and uninsured depositors.

A purported virtue of bail-in is that will make debtholders more vigilant, as they stand to lose their money.

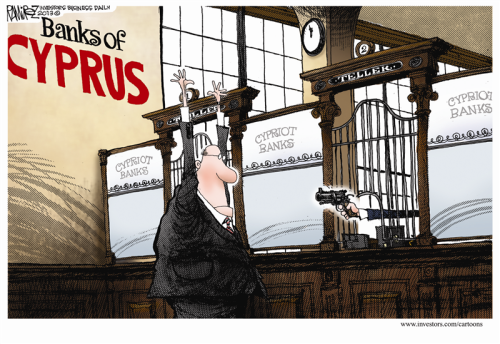

The Bank of Cyprus offers an example of a bail-in of which Eurogroup president Jeroen Dijsselbloem proudly claimed would serve as a template for future bank restructurings.

But did bail in really work?

6) In practise, bail-in is a mess.

I explained problems of bail-in some years ago in my blog. One of the problems is that, after a bail-in, former depositors become the new owners of the bank. Last year, the Wall Street Journal confirmed my qualms: “The bailed-in depositors now hold roughly 80% of the newly issued shares in Bank of Cyprus and essentially control the board of directors. As a result, the new board is now a mélange of Russian oligarchs … , Cypriot pension and provident funds, and a hodge-podge of other representatives who never expected to be running a bank, much less owning one.”

7) Bail-in, it isn't what it appears to be.

In her post on the first Italian bail-in, Bruegel’s Silvia Merler documents the recent liquidation of Banca Romagna Cooperativa. What appears like a bail-in, turns out to be a bail-out: the Institutional Guarantee Fund of Italian mutual banks decided to refund depositors in full.

A similar story, from Frances Coppola, applies to the Düsseldorfer Hypothekenbank. This small mortgage lender failed and then was saved by the Bundesverband Deutsche Banken, Germany’s association of private banks. And last month, in the Hypo Alpe Adria bank case, Austria’s constitutional court has declared illegal a law that would have bailed-in €890 m in subordinated debt.

Cyclist being bailed out by wooden plank.

Bail-ins that turn into bailouts are damaging for financial stability: debtholders will expect to be bailed out. So, instead of becoming more vigilant, they will become complacent - exactly the opposite what bail-in rules aim to achieve.

8) If you're not confused, you're not paying attention.

Bail-in regulations now have become like snowflakes, they are all unique. U.S. banks can be resolved under the Orderly Liquidation Authority (OLA) provided in the Dodd-Frank Act. Europe has its own resolution regulations: the Bank Recovery and Resolution Directive (BRRD) and the Single Resolution Mechanism (SRM). New Zealand has its Open Bank Resolution (OBR) policy.

Other countries, though, are less likely to implement bail-in regulations. Australia’s Financial Inquiry report, for example, recommends against bail-in. Adding to the confusion is the Financial Stability Board’s TLAC initiative for systemically important banks, which Australia does support.

Confusion has now reached the point that the International Capital Markets Association (ICMA) has expressed its ire about the salmagundi of resolution initiatives in a letter to the European Central Bank. The ICMA calls for more transparency, simplicity, and predictability of resolution regulation. I think ICMA has a point.

9) Promises, promises. Back to Greece.

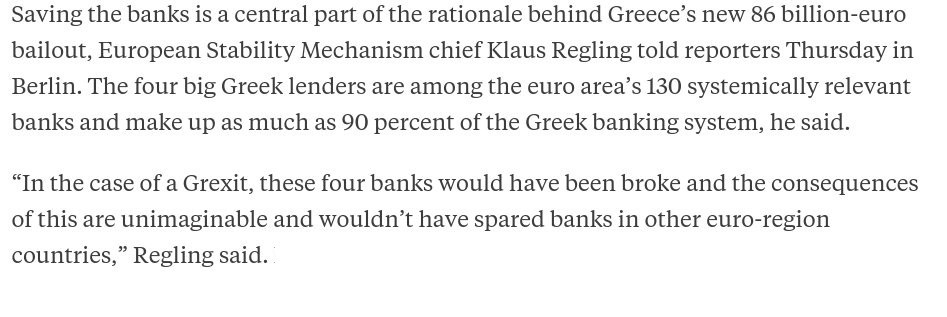

Will Greek debtholders be bailed in? Despite gung-ho promises from the Eurogroup to bail in senior debtholders, I am skeptical. Here is why: Greek debtholders are not Russian oligarchs that relied on Cypriot banks to stash their dosh. Instead, Greek debtholders are likely to be citizens, entrepreneurs. Bailing them in would surely not help Greece’s economy. European Stability Mechanism chief Klaus Regling, confirms my skepticism. Last week he explained the need for a bailout:

10) If you think safety is expensive, try an accident.*

Instead of relying on bail-in, my suggestion would be to try to prevent a bank failure from happening in the first place. Regulators therefore should focus on increasing capital buffers to make banks more resilient. Higher capital levels are a proven way to limit losses imposed on taxpayers.

*The irony is that this quote originates from Greek entrepreneur Sir Stelios Haji-Ioannou, who in 1995 launched easyJet, a very successful low-cost airline.

10 Comments

#10 - Typically governments - instead of making banks safer they stuff about with ideas on how to save a bank when it fails.

because banks want less and less regulations so they can make more and more profit as demanded by the shareholders, who are by and large pension funds and the recipients are, well voters.

What I suspect we need to strong regulation and have that outside of govn control/interference. But of course the right wing pollies in particular will jump to their paymasters tune and de-regulate as its "better"

So who is the fool here? well us the voter accepting such bull doo doo.

While reserve banks of other countries look to ensure overall banking stability by regulation (retained earnings, provision for bad debt, protecting depositors) the RBNZ has looked to the bottom of the cliff and put New Zealand Depositors to prop up the banks after failure by ensuring they lose some or all of their deposits. (with covered bond holders avoiding any haircut at all and getting all the collateralized mortgages to pay them back).

OBR might work, in practice, if a small one of the 25 banking licenses is the one to fail. NZ Financial stability wouldn't be threatened by a single small banking failure.

However, if one of the major four banks is involved with OBR, then the whole NZ financial structure will be in doubt.

I agree with you billsay that OBR is complete rubbish. But what few people seem to realise is that all the central banks around the world have passed (or are in the process of passing) legislation for bail-in execution - they're just doing this very sneakily and quietly without the general public knowing: http://ec.europa.eu/finance/bank/crisis_management/index_en.htm

#11. For the New Age Aotearoa any of the three white feathers of cowardice would do, one even depicts the black tar whereby to afix it. But the prize should really go to the fourth: the sun-baked dog turd! Jokey guarantees it is worth a billion a year.

So we are into the storm season and a never before seen event,

http://america.aljazeera.com/articles/2015/8/31/three-major-hurricanes-…

"Hurricanes Kilo, Ignacio and Jimena, all Category 3 and 4 storms"

yes, El nino's dont matter, no such thing as climate change, sure the soil moisture varies a bit....

Must read little article, with reference to an excellent analogy as to why Central Banks are in such trouble (even little old NZ gets a mention):

http://www.bloomberg.com/news/articles/2015-09-01/morgan-stanley-centra…

Amazingly coming out of MS as well.......

Big miss with Aussie GDP, +0.2% (versus forecast 0.4%), at stall speed. Big slow down from previous quarter. Another commodities country hits the wall it seems....

Those poor insurers - after talking up climate change to boost premiums the weather hasn't come to the party.

"Insurers Could Use More Calamity

On the 10th anniversary of Hurricane Katrina, insurers are suffering from years of calm seas and low rates.

...It might seem disasters on the ground would become financial ones for companies that shoulder those risks. But, if anything, the opposite is true."

http://www.wsj.com/articles/insurers-could-use-more-calamity-1440954444

And those poor peak energy doomsters.

"Drillers Unleash ‘Super-Size’ Natural Gas Output

Applying newer fracking methods to existing field offers potential for more and cheaper fuel

The U.S. may have far more natural gas than anyone imagined, all reachable at a profit even with today’s bargain-basement prices.

...In August, Comstock officials told investors that it could get a 30% return on its new wells even with gas at $2.50 a million BTUs."

http://www.wsj.com/articles/drillers-get-super-size-natural-gas-output-…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.