By Andrew Bascand, Shane Solly, Craig Stent*

The global economy remains fragile and subject to large sentiment shifts.

Small data surprises and nuanced comments from Central Bankers appear to have a disproportionate impact on the pricing of bonds and equities.

We think global bond markets are close to pricing a recession and a complete absence of inflation. Many bond yields are now negative, and credit markets are also very wary of the potential for higher default rates.

The abundance of risks in the global economy justifies caution. Transition in China to a lower growth rate and a remix of their economy, together with price dislocation in energy markets provide significant influences on markets.

However, we are not of the central view that the US economy faces a recession in 2016. Manufacturing trends are weak, but on the other hand employment, household consumption and the government sector are relatively strong. In Europe data continues to provide small positive surprises, despite the headlines on migration and concerns over a number of elections this year.

Against that backdrop the perception is that Australian economic growth prospects are fragile, investment sentiment is poor, and the financial system is exposed to a number of risks including rising resource, energy, agriculture and housing impairments. How can Australia not have a recession given the weakness in resources? This is a question we continue to get asked.

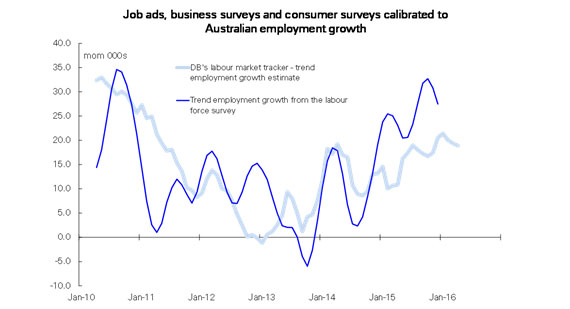

Figure 1 Australian employment has continued to be strong

Source: DB Markets, Harbour

The irony about GDP data is that it measures real added value. Resource export volumes are actually surging, and a decline in imported capital equipment for the resource and energy sectors will also support measured GDP. The mining sector is now actually a smaller part of the Australian economy. Household consumption and broader services sector activity are by far the most important contributors for GDP.

Australian employment growth has been accelerating. In the December quarter, net employment growth averaged +43,000 per month, after averaging a solid +25,000 a month over the 2015 year. It may be the case that employment growth slows a little into 2016.

However, housing credit growth has also been picking up, with owner-occupier credit growth averaging +1.1% per month in the December quarter and averaging +0.8% a month in the 2015 year. These trends are consistent with broader improvements in Australian business and consumer confidence as Australian households and companies react to lower oil prices.

It is important to note, Harbour is not making an “asset allocation” call on Australia. Instead, we think investment markets may be overly negative about economic prospects, and drawing long bows regarding profits. Too many commentators expect for instance a sharp rise in bank loan impairments and expect the housing sector to weaken significantly as the slow-down in the mining-sector impacts on consumption.

There is an upside for lower oil prices

In the last month, lower oil prices have been highly correlated with fears over economic growth and falling equity prices. In recent weeks, these relationships have been challenged by a number of analysts. The world has experienced a surge in oil supply, not a collapse in oil demand.

In 2015, global oil demand grew by 1.7m bpd, the second highest growth rate in a decade. Oil demand is growing as emerging market sales of cars continue to expand at a double digit pace. Larger SUVs have overtaken compact cars as the top selling models. At the same time surging US and Middle East oil output has met head on rising oil demand, providing a surplus of oil output in the last six quarters. Despite lower oil prices, marginal supply has been slow to turn off.

Bank of America Merrill Lynch estimate that the fall in oil prices from US$115 to $30 will transfer US$3trn a year from producers to consumers. They estimate this is equal to a $400 per capita transfer to global consumers, and will have a long lasting impact on consumption. The stimulation of vehicle transport, airlines, and tourism provides one growth avenue. The other is the redirection of money previously spent on petrol and energy into other consumption.

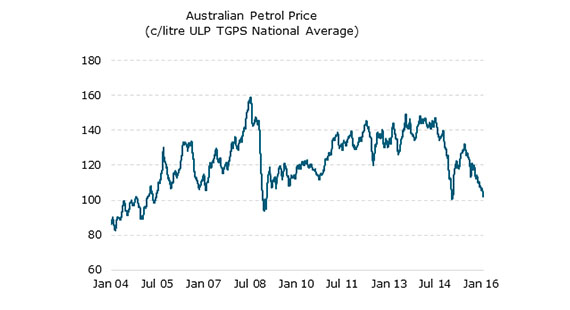

Figure 2: Lower Petrol Prices in Australia

Source: CLSA, Harbour

In Australia and New Zealand, strong travel, migration and tourism look set to continue as durable themes. The upgrade of arrivals data in both countries provides evidence of the direct impacts of lower oil prices.

We have no comparative advantage in forecasting oil prices. However, it seems rational that at current levels of near $30 bbl production cuts will follow. There is an increasing incentive among OPEC members to gain a consensus on supply, although any near term progress seems unlikely given geopolitical events. If oil prices sustain current levels, we would expect an ongoing positive impact on household consumption.

Where do you want to live and travel?

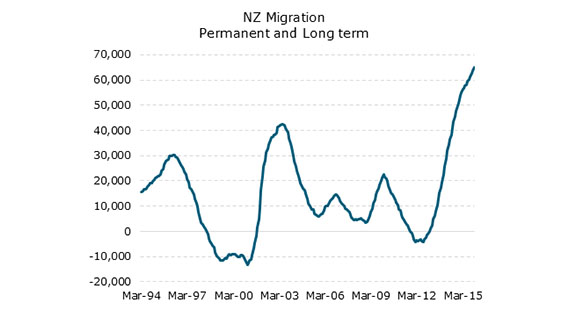

Migration data continues to be strong in New Zealand with a net inflow of 5,500 people in December, bringing a total of 64,900 for the year. The migration continues to reflect low departures, more students and stronger work visa arrivals from the UK and US.

Visitor arrivals were also strong, running at a record 445,000 for the month of December, buoyed by Australian, Chinese and US markets. This was up 10.5% on a year ago.

And why not when New Zealand (and Australia) remain high on most measures of top travel and life style choices. The latest 2016 index of Economic Freedom by the Heritage Foundation puts New Zealand at 3rd and Australia at 5th.

Figure 3: Migration continues to be strong

Source: Bloomberg, Harbour

The earnings season is ahead

In the US, the quarterly earnings announcement season is in full swing. At this stage, with 215 of the top 498 companies reporting the signs on balance been better than expected (+4.6%). Earnings for the technology sector have been better than expected with earnings beating expectations for the quarter by 5.7%. Although, a lot of energy and basic materials companies have yet to report earnings, companies in these sectors have also provided on balance positive surprises.

However, the issue for markets has been the further downward revision of forecast earnings in the US, with top-line revenue forecasts downgraded, and the outlook now for only low single digit earnings growth. To a large extent, earnings growth is concentrated on companies buying back shares. This outlook seems more appropriate given the pull-back in global growth expectations.

Similar trends are likely to be seen in New Zealand and Australia, with the exception that exporters are still likely to show a benefit from lower currencies.

In New Zealand, Forsyth Barr expect the median New Zealand companies to report revenue growth of 4% and earnings per share growth of 6%. Beneficiaries of the lower oil price, Air New Zealand and NZ Refining are expected to report the strongest profit numbers. We think other highlights might include those companies with global revenues, benefiting from the lower NZ dollar and better trading conditions.

In Australia, forecast revenue growth is 5.4%, and earnings per share growth is expected to be only 3.9% for industrial companies. Banks may also report a small positive earnings growth for the period reflecting the repricing of mortgages last year. In sharp contrast the mining sector may report a fall of over 70% in reported profits.

Outlook

After such a brutal start to the year in terms of equity returns, commentators are quick to extrapolate history and suggest we have entered a more general equity bear market. Year to date, oil prices moves have been leading equity volatility. We argue that correlation is likely to fade as the gradual benefit to consumers and companies over-shadows fears of financial contagion. Although we have no comparative advantage in picking the bottom in oil prices, we acknowledge oil sector experts who suggest a significant contraction in oil supply is occurring at current prices. That should start to exert an influence on oil markets as we go forward.

An equity bear market is not our central scenario. Interest rates and bond yields are too low. Global growth is more likely to be moderate, than contractionary. In New Zealand, the economy also seems set for continued moderate growth with both upside (migration, lower oil prices and lower interest rates) and downside (slowing global economy and weaker dairy prices) risks. The New Zealand equity market remains relatively expensive compared with most other markets. This reflects the higher certainty of earnings and relatively high dividends.

We are hesitant to pick strong sector winners at the moment. We retain a balance of quality growth companies, companies with strong defensive dividend growth, and companies with potentially higher growth rates in the technology and healthcare sectors. Although the technology and healthcare sectors have many attractive tailwinds, we acknowledge that these sectors are now relatively expensive. In a number of instances, these companies performed strongly in 2015.

Andrew Bascand, Shane Solly, and Craig Stent are analysts at Harbour Asset Management. This column does not constitute advice to any person. www.harbourasset.co.nz/disclaimer/

11 Comments

Otterwood,

This week credit continued to deteriorate and as readers know, credit leads the stock markets (see here for more details). The bleeding continued in European banks as can be seen by Euro area bank CDSs this past week (see the chart below). A credit default swap (known as a CDS) is a contract which acts as an insurance policy against a borrower defaulting. When the line goes up it costs more to get insurance against default on the bonds and as a result banks stocks were crushed.What the banks really hated this week was the fact that rates went even more negative in Europe. Rates being set into negative territory by central banks in Europe (and now Japan) are proving out to be the biggest policy blunder ever I think. This link illustrates the correlation with bank stock performance and negative rates.

Given I expected all kinds of stress in the markets as a result of a strong US dollar (see here for video explanation) I'm still in awe at how fast things are unravelling. I have grave concerns that Deutsche Bank in Germany will go under in the near future. The market seems intent on making this so and historically it is best to get out of the way.

If Deutsche Bank were to go under, it would not be like Lehman Brothers where the doors were shuttered one day and everyone was out of a job the next. The German Government would take it over but not before much distress in the system. The problem is that Deutsche Bank has the second largest derivative book in the world behind JP Morgan and that is a serious concern. If the viability of Deutsche Bank were put in jeopardy, we would see many other Euro banks go under which would kick up all kinds of stress in the system reminiscent of 2008.

In sympathy to the emerging stress in the Euro area banking system, gold finally broke out of its long-term downtrend this week (see the chart below). Last year we established a position in gold shares in the funds we manage. The thinking was that the Fed would eventually end up NOT hiking rates but instead embark on QE4 and gold would benefit from this latest policy flip-flop and growing lack of confidence in central bankers everywhere. This is just starting to play out.

This is not the time to be a hero and play for bounces in risk assets. We remain very conservatively positioned in our funds and the only things we're buying in this dip are gold miners.

Beneficiaries of the lower oil price, Air New Zealand and NZ Refining are expected to report the strongest profit numbers.

So, reduced pass through benefit to fly - drive consumers, which in reality is reflected in airfare and pump prices? Hence the consumer can never pick up the baton dropped by the dairy sector, given rising costs elsewhere.

And what about that prognosis for the debt laden dairy unit and the spin-off recreational properties tacked on to the so-called production IOU?

Not good apparently, according to another pundit.

Kiwis have failed to learn the lessons of their debt gorging ways Read more

It was predicted that it would be derivatives that would become the greatest threat to the banking system potentially causing an even greater collapse!

Well these people are in serious denial, global equity markets are already in a confirmed bear market! Russell 2000 Index is -25% from the high, Nikkei -28%, DAX -28% and all likely heading a lot lower after the current feeble bounce is over. Things are bad and getting worse. This analysis denies the harsh reality of a more serious than 2008 global financial meltdown currently in accelerating motion.

Hang on, humans act with no sense, just greed and fear.

and the Great Depression?

Never forget that GDP is a completely phony measure of wealth and is largely a measure of the rate at which resources are squandered and the environment polluted, so a high GDP growth rate equates with digging a deeper hole faster, as Japan has discovered and China is in the process of discovering.

I will personally be very surprised if present global economic-financial arrangements are still intact at the end of 2016.

How daring! The world's ability to survive has however surprised me (and lots of others) every year for the last 7. Though I will admit I dont think its been this bad since 2008/9, but I think its 50/50 myself.

"we acknowledge oil sector experts who suggest a significant contraction in oil supply is occurring at current prices."

I would love to know who because I see no such "experts" saying this, minor maybe for a bit. Other experts say no there is little sign that oil output is dropping off and in fact more, ie Iran will want to pump lots of oil, and maybe libya (assuming it can sort itself out in a bit). Then the US oil storage issue seems to be coming to a head. For me then I am hard pressed to see oil climbing in fact $20 seems more likley. Now future oil supply, yes indeed, many oil majors seem to slashing future work but generally that looks 3+ years out maybe 5.

Yes, more likely to be an expansion of supply causing further price drops, Iran coming on-line in a big way plus we hear now that US shale sector costs are lower than at first thought meaning they will pump for longer at low prices. Coupled with soft demand, we have a glut. WWIII could change all that though, things are heating up badly in Syria today with Turkey now shelling Syria and plans to send in ground troops with Saudi Arabia.

In other words, keep feeding the fund manager, don't change shares for cash, or the fund manager will be on the streets...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.