By Brad Carr*

Since the financial crisis of 2008, global banking regulators based in Basel with the Financial Stability Board and Bank for International Settlements have worked on ways to improve the financial sector’s measurement of risk.

Basel’s Internal Ratings Based (IRB) approach, where institutions undertake their own strictly defined risk measurement has supported greater sophistication in risk management and created incentives for a greater emphasis on risk in strategic decision making.

But current proposals stand to reverse this trend, in our view diluting the focus on risk which makes it timely to revisit the lessons of the pre-crisis Basel I era.

As well as providing misincentives, Basel I saw material reductions in banks’ average Risk-Weighted Assets (RWA). Contrary to several claims, average RWA has at least stabilised, and often increased, since banks moved to IRB.

Simple risk weights

Developed in the 1980’s, Basel I provided simple risk weights for each asset on a bank’s balance sheet, based purely on the borrower’s category, namely:

• Sovereigns: 0 per cent

• Banks: 20 per cent

• Mortgages: 50 per cent

• Corporates: 100 per cent.

These risk-weights were mandated with no reference to the creditworthiness of the individual borrower. Capital requirements were the same for all mortgages (prime or sub-prime) and for all corporates (low-geared blue-chips or highly leveraged start-ups).

Where market yields might have some sensitivity to risk but be applied over a flat capital requirement, banks could grow their ROE by lending to the riskier borrowers. They were rewarded for being riskier.

This created some obvious arbitrage opportunities: where banks did lend to a strong corporate, they could hedge this with another bank, immediately reducing the risk-weight from 100 per cent to 20 per cent.

Entering a transaction to achieve this 80 per cent reduction made economic sense for high-grade corporates (where the hedging cost was relatively small), though not for weaker credits with expensive spreads (risk premia), meaning banks were being driven toward adverse selection within their corporate portfolios. Similar opportunities existed with securitised mortgages.

There were many contributing causes to the crisis, not least insufficient total levels of bank capital and liquidity. But the misincentives and arbitrages also exacerbated some of the distortions and imbalances allowed to develop in the pre-crisis years.

Gradual process

Significantly, the next iteration of global regulation, Basel II, was not yet implemented during the run up to the crisis. Basel II and internal models commenced only for the first banks in Europe, Japan, Canada and Australia during 2008. Even this was a gradual process: all internal models had to be assessed, validated and approved by national regulators.

In the US, this came much later, with the first approvals in February 2014, and Wells Fargo and Bank of America only approved in 2015.

It is therefore a mistake to blame Basel II models for the crisis. If a bank had managed its capital efficiently to its prevailing constraints, it entered the crisis with a Basel I portfolio, before Basel II's risk-based modelling reversed the misincentives, promoting better credit quality and the exiting of arbitrage positions.

Basel 2.5 and Basel III retained these strengths and built on them further, raising the required capital ratios and improving risk coverage in areas such as counterparty credit and market risk.

The system and industry are better for these changes.

The Bank of England’s Andrew Haldane gave a speech in 2012 about the “Dog and the Frisbee”. He argued risk-based capital was no better at predicting a bank default than a non-risk-based Leverage Ratio, across bank failures up until 2006.

However, the crucial point is Haldane’s data is all prior to the commencement of Basel II and internal risk models.

In contrast to Haldane's Basel I comparisons, Moody's compared the Leverage Ratio against Basel II risk-based metrics in their 2015 updated Bank Rating Methodology, affirming the predictive power of RWA as the best indicator of potential default.

“In our failure study, the TCE/ RWA [Tangible Common Equity divided by RWA] measure was the most predictive indicator of failure amongst a number of other measures, including an un-weighted leverage measure,” Moody’s said.

RWA trends

While some claim banks’ risk-weights have reduced because of internal models (and models are merely a way to reduce capital requirements), post-crisis data reveals a different picture.

Across 30 major international banks (globally systemically important banks (GSIBs) plus Canadian and Australian Domestic SIBs), post-crisis Average RWA has been reasonably stable, before stepping up when US banks first reported Basel II in 2014, as follows.

Underlying this is a mix of offsetting factors since the height of the crisis: regulatory and methodology changes (Basel 2.5 & III) have incrementally increased RWA banks have actively reduced risk on their balance sheets, both in responding to the crisis and heeding the risk-based incentives of Basel II, as well as holding more low-risk liquid assets for Basel III liquidity regulations.

More notable is the trend preceding the development.

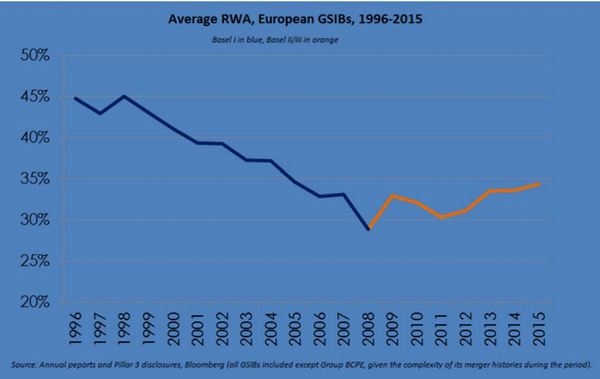

In Europe (which has the deepest historical data), average RWA fell consistently when Basel I prevailed. While banks had different risk appetites and responses to incentives, it would appear many had successfully identified how they could maximise opportunities under a blunt, standardised regime.

When banks moved on to Basel II and had their internal models accredited by regulators, average RWA plateaued, as shown in the below chart.

This firstly contradicts claims internal models are merely used to reduce capital requirements.

Banks do try to rationalise and efficiently allocate their capital across businesses and grow their ROE, as any commercial business with shareholders should.

When capital is risk-based, this efficient allocation is pursued by trading returns directly against risk, so the trajectory after the Basel II implementation should not surprise:

• If you pursue high-yield (and high-risk) credits, you grow both the numerator and denominator of the ROE equation; and

• If you seek to reduce capital requirements by improving credit quality, you concurrently reduce revenue; ie contract both the ROE numerator and denominator.

In contrast, a simple regime gives relatively easy routes to optimise (and reduce) capital without sacrificing yield. Far from internal models having had a role in leading to the crisis, they might have actually helped to avert or reduce it if we’d started using them earlier.

And now?

We all agree models are imperfect: for low-risk assets, there are (by definition) insufficient historical cases of borrowers defaulting to give a richness of data and banks do need to reduce the variance between their respective models.

However, as the trends in banks’ portfolio composition and risk metrics over the last two decades show, we need risk-sensitivity to be at the forefront of the capital framework. We are so much better and the system safer and more stable, for having moved on from the Basel I conditions.

As adjustments to the Basel framework are considered this year, care is needed to ensure the Basel I pre-crisis conditions are not inadvertently re-imposed.

Rather than overriding models with blunt approaches, the industry and regulators should collectively work to pursue new initiatives that can deal to model shortcomings while preserving risk sensitivity.

-----------------------

*Brad Carr is deputy director of the regulatory affairs department at the Institute of International Finance. This article first appeared on ANZ's BlueNotes website here and is used with permission.

2 Comments

There's a few things there that I wasn't aware of. I know there was an issue with downgraded debt causing problems in the US. The risk weightings aren't perfect but what were the US banks using at the time? Even if they were using a system they were completely clueless as to the risk from their positions. There's very few risk experts in the world I suspect that very few actually work in the banking sector.

Hmmmmmm.

Australia’s banks turned into giant building societies, lending almost exclusively against residential property and rarely, if ever, making unsecured loans to businesses or people any more.

If someone asks for a business or personal loan these days, the banker asks for the house.

The result is that traditional small business lending has dried up, and with it business investment, while Australia has the highest ratio of household debt to GDP (134 per cent) in the world, since business owners have to borrow against their houses. Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.