By Rees Logan*

Two difficult seasons of below-average dairy payouts, and a third being forecast, have delivered a big wake-up to the dairy farming industry.

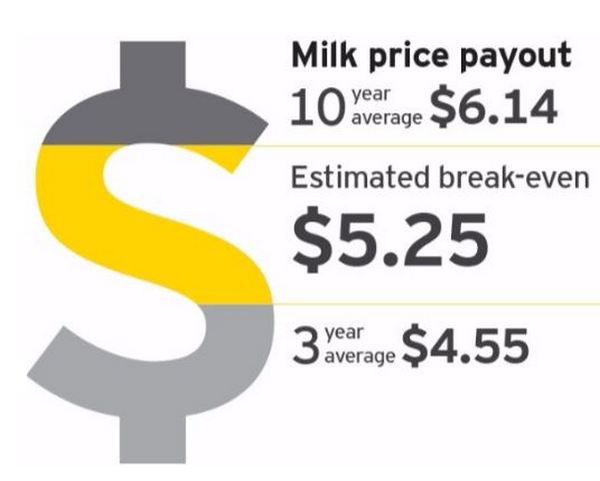

The average payout for the current and last two seasons is approximately $4.55 (including dividend) against DairyNZ’s estimated average breakeven payout required by farmers of $5.25. This means three seasons where most farmers have had to take on additional debt just to survive.

Dairy farmers have been forced to take a ruthless approach to expenditure and to switch their focus from production to profitability in a bid to cut debt.

While reducing productivity, the drive to cut costs is improving the bottom line at current payout levels. But some farmers have gone too far by cutting too much essential expenditure to operate within banking facility limits.

Slashing essential expenditure, such as fertiliser applications, re-grassing, and repairs and maintenance, may provide a temporary reprieve but is likely to compromise both productivity and profitability in future seasons. The longer the under-expenditure occurs, the more future seasons will be compromised.

Surplus assets, such as livestock, have been sold, again to assist operating within banking facility limits. Any capital expenditure has been minimised or eliminated which is not sustainable for an extended period as equipment and machinery routinely requires replacing or upgrading.

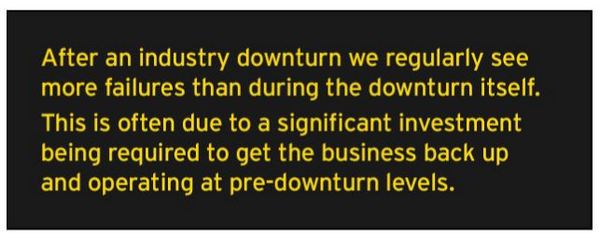

After an industry downturn we regularly see more failures than during the downturn itself.

This is often because significant investment is needed to get the business back up and operating at pre- downturn levels. In the dairy industry, this investment will be needed in areas of under expenditure such as pasture quality and fertility, repairs and maintenance. There will be demands for catch up capital expenditure, repayment of Fonterra advances (if used)) or repayment of any deferred creditors.

This is all before considering repayment of term debt. So, it will take longer than normal to return to pre-downturn operating levels with some farming businesses going under.

Fonterra’s average milk price payout in the past 10 years is $6.14 (including dividend). Therefore, if farmers cannot break even at this payout with normalised operating and capital expenditure, as well as making a contribution towards term debt repayment, they must be realistic and consider exiting before further eroding their remaining equity and being forced to exit.

Any farming business requiring a higher-than-breakeven payout will be closely monitored by the banks, particularly those with lower equity levels. Farmers in this position must seriously consider how much more debt their business can sustain before the burden becomes too heavy.

While making a decision to sell sounds simple and rational, it is much more difficult for farmers as farming is not only a business but also a home and a lifestyle, 24 hours a day, seven days a week. For a number of farmers it is also their superannuation and succession plan for the next generation which further complicates matters.

As any surplus assets are likely to have already been sold, raising equity is the only other option to reduce debt to sustainable levels at current payouts if farmers in these precarious positions do not wish to sell. Unfortunately farmers needing the most equity are the least attractive to investors because of their high debt burdens and under-performance relative to the industry.

Formal insolvency, such as appointing a receiver, is always the last resort for banks and usually occurs only as a result of a breakdown in the relationship and divergence of views between a customer and its bank.

This is likely when the bank does not believe the business can survive and does not wish to continue funding losses but the customer is adamant it can survive and does not accept the bank’s encouragement to sell voluntarily.

While some farming businesses will fail as a result of the downturn, as happens with any industry in that economic situation, ultimately the industry as a whole will benefit, with most surviving businesses becoming leaner, and more agile and resilient.

--------------------

*Rees Logan is the joint leader of EY’s corporate restructuring practice and advises agri-sector clients.

51 Comments

US Subprime housing should have been an opportunity for prudent investors to snap up the bargains ......

Didn't work out so well though.

As I see it and you note here

For a number of farmers it is also their superannuation and succession plan for the next generation which further complicates matters.

The current "price" of a diary farm includes a huge tax free capital gain that farmers have been willing to risk longer term to avoid paying short term tax's in the good years. Goodwill normally carries little value at a mortgagee sale.

This situation is much like the situation we find ourselves in with residential property investment... the asking prices are distorted by the assumed continuing capital free gains...

http://www.interest.co.nz/rural-news/53495/dairy-farmers-pay-lower-tax-…

Buccaneering Private Equity privateer Blackstone piled into foreclosed houses with its ears pinned back and is now the largest landlord in the USA

http://www.businessinsider.com.au/blackstone-is-largest-owner-of-real-e…

Worked out very well for them

There are some fundamental differences between a foreclosed house and a foreclosed farm....

Alternatively you could say surviving farms will be run down and under capitalized.

NO - the industry as a whole wont benefit - this isnt some boom bust cycle - this is the end of growth - the consequences are far more drastic. The industry as we know it wont exist.

And if you don't believe it, work backwards. How can commodity prices rise, particularly Oil? More (consumer) debt. How do you add more debt? Lower interest rates. What do you do when we hit zero interest rates and below? You lose faith in money.

Dead right Ham n Eggs! Money has no real value only an expectation of what is going to be worth next year.

Yanks printed heaps and the U.S dollar should have gone down but it went up!? How does that work..

In Vanuatu pig tusks are highly sought after......ha!

Only thing Ham, is that people still want things like food and oil. Those are the fundamentals, not the value of the means of exchange. The issue with dairy isn't some end of days scenario, but that our farmers are spending more to make what they sell than some of their competitors. We are a long way from markets, and most of what we sell is a commodity so we have to compete on cost. Speculation on land, therefore cost of debt, and lack of innovation compared to competitors contribute and the way out will be restoring competitive advantage. Some have it, some don't, and the best are still lower cost than anyone. It's just that the bar has shifted.

so what was the farmers competitive advantage, and why has it all but evaporated?

Our competitive advantage could have been extensive, GE free and as much as possible organic diverse farming, from crops to dairy sheep and everything in between, rather this almighty rush to turn the whole country into a WMP supplier. Even I could see how dumb that was going to be. There are people in this world with lots of money who would be prepared to pay top money for top produce, regardless of WMP prices

but is that not our history for everyone to try to jump on the bandwagon then it goes tits up,

i remember the kiwifruit goldrush then the ripping up of the vines,

what about the vension boom

people before my time remember the wool boom.

we have a history in NZ of farmers all investing heavily in the same thing many to late to catch the tide and when it goes out its bad news

I think the current one is beef

Belle, I see in Aussie the cattle have got too expensive for the processors.

http://www.beefcentral.com/processing/beef-plant-closures-start-in-the-…

I got an Agrihq report this week. Smallish r1 angus heifers making between 750 to 850. As you would know Aj the potential in an angus heifer can be pretty limited. Its desperate stuff. The dairy crash has totally skewed the beef market. Interesting times.

Australian beef prices ' top of the tree'.

http://www.beefcentral.com/markets/australian-cattle-prices-now-top-of-…

http://www.cattlenetwork.com/news/markets/what-ranchers-can-expect-catt…

Good links as always. Thanks Aj. How are things in the Hawkes Bay now? Did you get rain? Peeing down out there right now. Winter has been pretty good so far.

Belle, I moved north for winter, I'm in Cornwall for a few more weeks. But I have only mowed my lawn twice since Christmas and the people in my house tell me it's still short.

We had a daughter getting married, now we are two down but getting very spread out which is causing my wife grief.

Cornwall has been wet but two good days this week,

I envy your lifestyle Aj. You sure get around the globe. Congratulations on getting the 2nd one a wedding. I imagine after the next 3 (?) you might be forced to curtail that globe trotting. We must be greatful for cheap messaging skype and phone calls. Distance to loved ones doesnt seem so bad when you can chat for hours any time. I think winter is finally kicking in here. The regrowth is pretty slow. Hard to believe spring so close....yep spring...I call august spring as thats when all the calves and lambs arrive. Plus the 1st rhodo is already starting to flower.

Getting a bit boring chasing children around with them studying in three different countries. Our jet setting ways need to come to an end, I'm sick of it.

A Hawkes Bay winter not so bad eh...or would you settle somewhere else. Not sure why the title to this was dairy farmers will be more resiliant etc etc....he clearly says they may damn well not be after having to cut some pretty basic stuff out.

I agree - people will always want food and Oil. But it comes down to what they can afford to pay for them.

Since 2008 money printing has been used to effectively "disguise" a collective insolvency. ie the cost of producing all those commodities is actually greater than the system can afford - ie Low Oil price reflects demand /affordability issues (which appears as a "cheap oil" glut) - hence ever greater debt loading. This can only ever be a temporary fix.

If you've been starving for 3 years, that will make you leaner, less resiliant, and less agile.

There is the inbuilt assumption that high prices are normal, but the evidence on the ground is that low prices are normal, and we can't produce milk at a low price, so we are fkt.

exactly - lower prices are new normal. Thats what the Oil companies are finding too, so they are not exploring for new fields ... which can only mean a big energy problem is on the horizon.

I read an article over the weekend but can't find it now . Basically it said that $55 oil is about the same margin $90 oil due to efficiency gains in Shale. Has any else seen or can confirm this ?

"The Shale Revolution and low oil and gas prices go hand in hand. Because the initial production rates of most shale wells are so much higher than conventional wells, the per-unit cost of production is lower, even though the wells themselves are more expensive. In other words, each barrel of crude or each cubic foot of gas from a shale well costs less, because the volume produced per dollar of invested capital in the well is greater. And it is this lower cost that makes these wells profitable even at low prices.

Now that lower prices are a part of the landscape, producers are finding ways to drop those costs even lower – more efficient drilling, lower services costs, even higher initial production rates. As costs continue to drop, the pressure on prices will continue."

https://rbnenergy.com/cover-of-the-rolling-stone-shale-econ-101-from-oi…

Yes it is begining to look like there has been a structural change in the dairy market and somewhere between $3-4 will be the new normal. (currently sitting at $3.70 farmgate price according to AgriHQ).

I think Keith Woodford has accurately pointed out the different factors that cause European farmers to be paid more than NZ farmers, basically the fact that we are still producing mainly on a seasonal basis, which means most of our milk has to go into low value products is the main difference.

European farmers are starting to get higher prices for their milk again now, while NZ is staring down the barrel of a payout cut in the near future if things don't turn around.

A payout cut to anything starting with $3.-- will be absolutely catastrophic to the industry after several years of low prices already.

Dairy farming itself needs to undergo a structural change to survive. My opinion is back to how it was 30 years ago, milking half the number of cows, fully self cotained, a little bit of lime and a bit of super, thats about it. That way your cost of production is low enough to survive.

Average dairy land prices down 16% over last year, a $3.?? payout and prices will be down another 16% before the actual stressed sales begin. The 50% of the 40bill book that is owed by 20% of the farmers, will be will underwater by then. Sure bank losses in a situation like that are probably constrained at 10-20% of total book as land has residual value, but we are talking really big numbers here. This scale of write down would limit a banks ability to lend into a residential property crash if they both happened at the same time.

Credit would get really tight. Across all NZ sectors, a World recession will probably impact Tourist number growth as well.

Rockstar Economy ?

If Dairy farm prices value going forward on a return on investment with little implied capital gain .... its got a long way to correct yet

this is grandfather stuff. howsoever

http://www.teara.govt.nz/en/cartoon/34529/the-wool-boom-1950

and the dislocation that followed:

the 1951 waterfront strike.

https://www.google.com.au/search?q=1951+waterfront+strike&rlz=1C1LENN_e…

what pots of ours look like boiling over

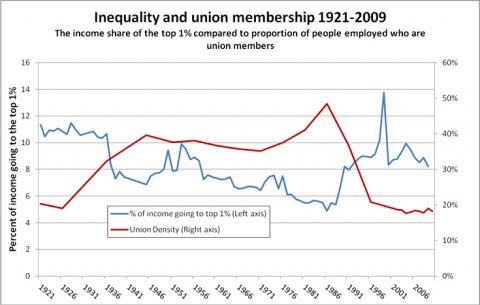

Thanks for the links Henry,

a graph half way down the second page caught my eye (on unionism and income inequality)

http://1951waterfrontdispute.weebly.com/uploads/2/2/5/3/22534060/511280…

{kind=link}

It surprises me just how easily the huge issues in the dairy industry have disappeared off the radar. That level of debt cant be serviced on the current level of forecast for any length of time without blood on the floor.It wont be until farmers start walking off their farms in numbers that the issue will re enter the public consciousness, just like it took the TV3 report of people living in garages for people to become aware of the extent of the homelessness issue.

Kudos to Keith Woodford, who from my perspective, appears to be the only one capable of digging into the detail and extrapolating out the real global situation and reporting it straight. If he continues to be correct then there is a lot of pain to come.

JK will be wearing out his knees praying that the housing bubble and the dairy crisis don't come to a head simultaneously, completely blow up in his face before next September.

What surprises me is that dairy farmers still 100% agree that prices will be back to $6+ by the end of this season, Europe will just stop producing and NZ will be the big dairy super power again.

Nobody seems willing to consider that prices won't go up, everybody just keeps saying that this is just a cycle and it will go up to new record highs again soon.

The banks are still flat out approving more finance and getting people into more debt and selling the idea that big price rises are coming to help people feel comfortable with the debt they are in when really they are in well over their head and just don't know it yet.

Fonterra are trying to keep people happy by announcing a higher forecast for this season than last season, but soon enough they will have to face the music, and that is when things will start crashing.

now you are talking the big stuff.

same ideas over and over again.

https://en.wikipedia.org/wiki/Echo_chamber_(media)

and an example of: all (but exactly 7:30 onward) from the other day

https://www.youtube.com/watch?v=XAGBBt9RNbc

Brainwashing

Jaf - your comment is interesting in that down my way, I have yet to find a farmer that doesn't believe low payouts are here to stay. I think you are a North Island farmer? Could it be a North v South difference?

I was at a function recently where an ASB banker spoke. They said farmers have to understand the global view of things and to ask for that information. One stalwart that has being around a while replied - 'the last place I would go for that advice would be my banker'. Others in the room concurred. The banker replied saying that we should take overseas trips to see the way of the dairy global perspective! Yeah Right.

Yes I am in the Waikato, and I run a large service bull and bull finishing operation, so I talk to quite a lot of dairy farmers through the service bull side of things.

From what I understand, banks are being a little harder on dairy farmers in the South Island. I guess there is a higher proportion of recent conversions, as well as larger farms so you would think there is more debt and higher costs there too.

I think to be fair, now we are coming into a 3rd season of low prices I think that farmer attitudes are starting to change here in the Waikato, and there is a little more awareness that this is not a part of the regular dairy cycle, or we would have seen prices start to head upwards again by now.

Banks won't admit it yet though, obviously ASBs official number for this season is still $6.

I found it interesting that ASB canned their usual market update type breakfast they normally host before the National Fieldays at Mystery Creek, in favour of a light talk about their new partnerships with Xero, and other technology firms.

Not a single word was uttered about payouts which is usually a key topic at that event.

This is certainly an interesting time to be in the rural industry, I get the impression that even the the people we would presume are experts, at Fonterra have been completely taken by surprise at the extent of the downturn.

A lot of interesting comments above. I have never had any connection to farming, but spent my life in the UK, in financial services. Farming here and dairy in particular has always seemed to me to be a strange business, with a poor return on capital and almost entirely dependent on the price of land always rising to give the retiring owner a tax-free capital gain. I certainly wouldn't invest in any company with that model.

I am not at all surprised that the entire edifice is under extreme stress and will have to change drastically. Fonterra strikes me as a very poorly run operation, with vastly overpaid, underperforming senior managers.

Fair observations Linklater. I think part of the problem is that farming works best with family farming operations managed by owner operators or committed sharemilkers who are aspiring to farm ownership. That model largely survives the ups and downs because they understand the cycles and can hunker down if necessary for a period and consolidate their wealth through the good patches. Mostly these farmers love what they do and are prepared to sacrifice and often have a multigenerational perspective.

When you start getting corporates and syndicates with multiple layers of management and high cost structures and Queen street farmers who have never milked a cow in their life, leveraged up to their eyeballs and expecting an annual dividend. Farming is too volatile to sustain that sort of structure.

I have some genuine fears for how the next couple of years play out but the upside of that is that it may provide some opportunities for motivated hands on farmers to get ahead. I hope we don't see widespread buy ups by foreign investment trusts, finance by cheap credit.

Any farmer wanting to get out........do it now land will not hold up at the current value......try find a buyer at 30% below RV

Everyone relax, ASB says the payout will be $6 this season. When was Nathan Penny last wildly wrong about the payout........

One dairy company is doing the rounds saying to suppliers that customers are refusing to enter in to long term contracts and as a result they have no idea as to what the 2016/17 season payout will be. So tighten the seat belts folks we may be in for a bumpier ride this year.

Was talking to a mate who supplies services to one of the foreign owned southern dairy processors. Their invoice to the said processor is now in excess of 140days over due. When comment was made in reference to Fonterra (who they also supply services to) not paying for 90 days, the reply was 'Maybe, but at least Fonterra does pay you'. I wonder what a financial WOF would show for dairy processors - are some of them sailing closer to the wind than is believed?

Head of the Snake - The Poisonous Gap Between Paper Wealth and Real Wealth

July 4, 2016

Head of the Snake - The Poisonous Gap Between Paper Wealth and Real Wealth

John P. Hussman, Ph.D.

All rights reserved and actively enforced.

Reprint Policy

“Understand that securities are not net economic wealth. They are a claim of one party in the economy - by virtue of past saving - on the future output produced by others. Fundamentally, it's the act of value-added production that ‘injects’ purchasing power into the economy (as well as the objects available to be purchased), because by that action the economy has goods and services that did not exist previously with the same value. True wealth is embodied in the capacity to produce (productive capital, stored resources, infrastructure, knowledge), and net income is created when that capacity is expressed in productive activity that adds value that didn't exist before.

“New securities are created in the economy each time some amount of purchasing power is transferred to others, rather than consuming it. Once issued, all of these pieces of paper can vary in price later, so the saving that someone did in a prior period, embodied in the form of some paper security, may be worth more or less consumption in the current period than it was initially. That’s really the main effect QE has - to encourage yield-seeking speculation that drives up the prices of risky securities, but without having any material effect on the real economy or the underlying cash flows that those securities will deliver over time.

“If one carefully accounts for what is spent, what is saved, and what form those savings take (securities that transfer the savings to others, or tangible real investment of output that is not consumed), one obtains a set of ‘stock-flow consistent’ accounting identities that must be true at each point in time:

1) Total real saving in the economy must equal total real investment in the economy;

2) For every investor who calls some security an ‘asset’ there is an issuer that calls that same security a ‘liability’;

3) The net acquisition of all securities in the economy is always precisely zero, even though the gross issuance of securities can be many times the amount of underlying saving; and perhaps most importantly,

4) When one nets out all the assets and liabilities in the economy, the only thing that is left - the true basis of a society’s net worth - is the stock of real investment that it has accumulated as a result of prior saving, and its unused endowment of resources. Everything else cancels out because every security represents an asset of the holder and a liability of the issuer.”

Spot on, AJ.

Its even worse than this. Because in reference to 4) above, theres a big problem with a huge % of the value assumed in the "accumulated saved investments" referred to after netting off the paper; That is, they all assume a continuity of "business as usual" on which to base their value.

So for simple example, a combine harvester becomes a worthless stranded asset if fuel becomes unavailable etc. Given the debt problems coming up which will flow on to energy problems, our net position is in a far worse state.

Interesting comments CO.

Nathan Penny is still predicting $6! Clearly ASB will be standing behind all their dairy clients given glory days a due back again! Under the circumstances that is just an irresponsible statement.

What farmers desperately need to hear is the truth not wishful thinking. GDT is telling us the current market is only capable of sustaining an $NZD price that is 15% below last season and time for recovery is running out before the spring production surge. The extreme seriousness of this situation seems to have completely vanished from the public consciousness.

SS the reality is that no one really knows what is happening and rather than tell farmers to take a conservative approach and forward budget on current payout, those who rely on everything 'coming right' are saying what they need farmers to believe in order to have them to continue to receive their bonuses/protect their income stream.

The real elephant in the room is what new regional council rules/NPS will mean for farming and it appears that its not even being seriously considered by banks. Take the Southland Water and Land 20/20 Plan currently out. (You are in ORC country I think?) Environment Southland is the first council in NZ to use physiographic zones as the base of all their land use rules. This is a paradigm shift (and due to complexity of just how they are made up, not easily understood) and a farm can have more than one physiographic zone. It is more complex than just soil type. http://waterandland.es.govt.nz/southland-science/physiographic-zones/ge…

The three zones that will affect existing farming businesses the most are Alpine (>700m asl), Old Mataura (very ancient and unique geology that has high natural nitrogen production) and Peat wetlands. Though the 20/20 Plan appears to be very dairy-centric the rules relating to the physiographic zones are the same for all types of livestock agriculture. So there are professional dairy graziers who may find that their zones will require them to reduce their grazing numbers (and in turn income) or in worst case scenario, stop grazing. There will be sheep farmers who take on dairy grazing that will be affected by the rule relating to intensive winter grazing where limits are currently set at 20 & 50ha of forage crops (depending on their zone(s) ) being permitted, any more than that will require a consent, which isn't guaranteed. There are intensive sheep farmers that currently graze up to 2500sheep/ha on forage crops that will potentially be affected by the intensive grazing rules - especially if they also take on some dairy grazing. In some zones it will be virtually impossible to convert to dairy, so those non dairy farmers who thought selling out for conversion is their retirement plan, will not only have to rethink, but potentially face a considerable loss in equity/value as well. For all farmers there is a substantial requirement for a very significant increase in paperwork and with current income levels it means a considerable increase in cost.

And we haven't had the nutrient limit setting process yet. ;-)

Dairy farms with barns are not selling for any more $/ha than farms without. The talk around the traps is: If you want a barn on your farm, the cheapest way to get one is to buy a farm with an existing barn as the capital expenditure invested in barns etc is not being reflected in farm sale price - moral of the story - don't over capitalise or you won't get your money back.

I understand a certain 'highly proclaimed' barn near Rakaia in Mid Canterbury abandoned indoor farming this season in favour of a lower cost grazed outdoor system.

This wouldnt perhaps be linked to a fed farmers spokesperson from a couple of years ago? I was wondering how the bloke was getting on. Went all out cut and carry as I recall. It was quite an interesting set up.

I think this is just the new reality CO, although as you point out I am ORC.. I don't have a problem with that if it is based on robust evidence and given the detailed nature of the zoning it must be. The point you are making is that farmers have just buried their heads in the sand and are unprepared for the (significant) implications.

It shows the necessity of moving away from commodities as we are reaching the limits on ever increasing production through intensification. This could be as much an opportunity as a cost.

Exactly SS. I understand that some other regional councils are looking into using physiographics in their planning after seeing the results of it in Southland.

ORC rules are potentially a disaster waiting to happen for dairy farmers, especially those in South & West Otago. The more they 'tweak' Overseer, the higher farmers leach rates seem to be. To get to a leach rate of 30 for a significant number of dairy in those areas is going to be nigh on impossible. One advantage of physiographics is that you don't need such a reliance on Overseer when making policy/rules. Overseer currently has no ability to recognise mitigations such as wetlands, management of critical source areas etc so the sooner planners are able to move away from it and to physiographics the better.

Extremely serious situation and yet seemingly ignored by the average man on the street.

The write ups of the National field days would suggest more than just the man in the street are ignoring this.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.